BORR - Borr Drilling: Accelerated Refinancing Could Provide A Near-Term Catalyst - Buy

2023-06-05 11:30:56 ET

Summary

- Borr Drilling reported Q1/2023 results in line with expectations and maintained its full-year outlook for revenue and Adjusted EBITDA.

- The company's entire fleet of 22 modern jackup rigs is now working or preparing for near-term contracts, with dayrates for new contracts 30% higher than the average.

- On the conference call, management stated expectations for leading dayrates to increase above $175,000 in the second half of the year.

- In addition, the company is currently working on an accelerated refinancing of its 2025 debt maturities in order to create a path to shareholder distributions.

- With the accelerated refinancing providing a potential short-term catalyst and the company likely to initiate a sizeable dividend at some point next year, Borr Drilling's shares remain a buy.

Note: I have covered Borr Drilling Limited ( BORR ) previously, so investors should view this as an update to my earlier articles on the company.

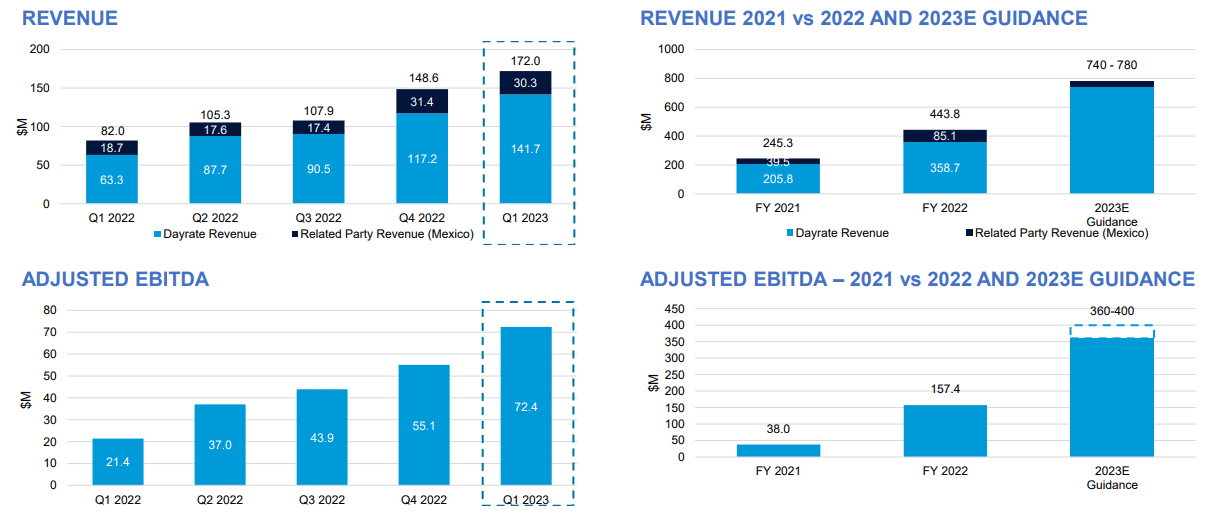

Two weeks ago, leading offshore driller Borr Drilling Limited or "Borr Drilling" reported first quarter 2023 results largely in line with expectations and reiterated its full-year outlook for revenue and Adjusted EBITDA:

{kind=link}

Company Presentation

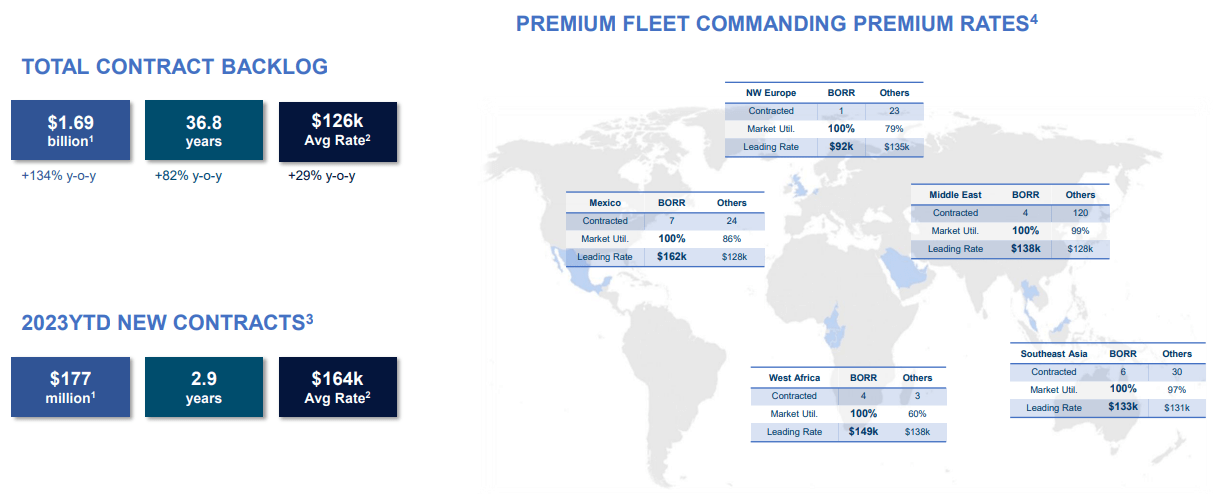

The company also released a new fleet status report . Year to date, Borr Drilling has been awarded eight new contracts, extensions, exercised options, letters of awards and letters of intent representing 1,797 days, or 4.9 years and 253 million of potential backlog. Total contract revenue backlog at the time of the Q1 report amounted to $1.69 billion.

{kind=link}

Company Presentation

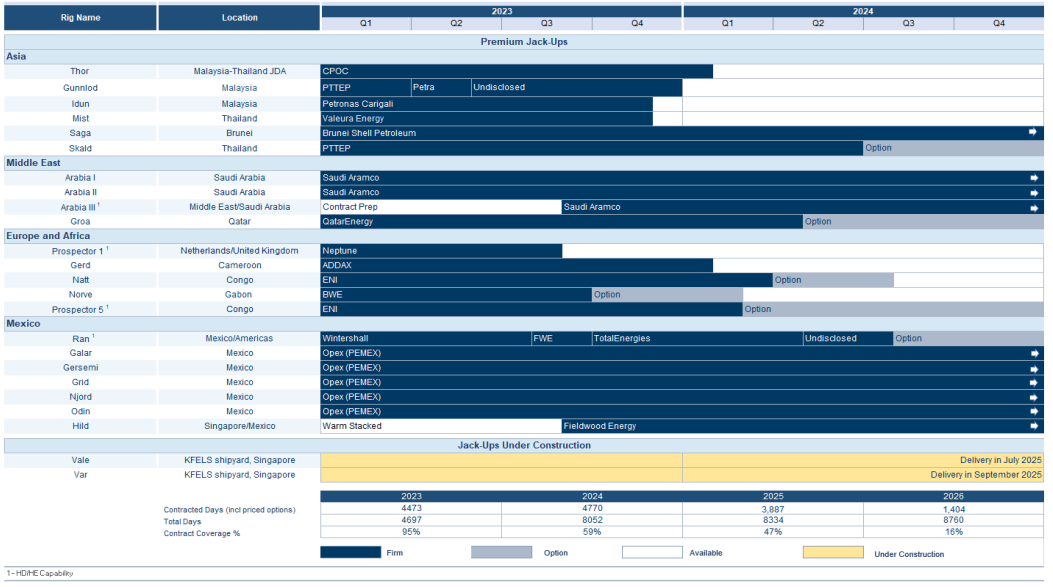

With the company's entire fleet of 22 modern jackup rigs either working or in preparation for near-term contract commencements, results should continue to improve in the second half of the year with additional upside expected for 2024 as rigs are re-contracted at higher dayrates in a further strengthening market environment.

{kind=link}

Company Presentation

Please note that dayrates for new contracts signed this year have been 30% higher than the company's average dayrate of $126,000.

On the conference call , management stated it expects leading dayrates to increase " above $175,000 " in the second half of the year.

In addition, the company is currently working on an accelerated refinancing of its 2025 debt maturities in order to " create a path to shareholder distributions ".

Given recent successful moves by competitors Transocean ( RIG ), Valaris Limited ( VAL ) and Noble Corporation ( NE ), I expect Borr Drilling will be able to close on the contemplated refinancing before the end of this year.

Bottom Line

Borr Drilling reported Q1/2023 results largely in line with expectations and affirmed its guidance for the full year. With two additional rigs scheduled to join the contracted fleet over the course of the year, results are expected to get another boost in the second half.

With leading dayrates expected to increase even further, the company's longer-term outlook remains strong.

Despite the stock price remaining in striking distance of recent multi-year highs, shares are still trading at just 3.5x my 2025 EV/EBITDA estimate.

With the accelerated refinancing providing a potential short-term catalyst and the company likely to initiate a sizeable dividend at some point next year, Borr Drilling's shares remain a buy.

Despite recent volatility in oil prices and related stocks, I remain positive on the entire industry, including leading U.S. exchange-listed players Noble Corporation, Transocean, Valaris, Seadrill ( SDRL ) and Diamond Offshore ( DO ) or offshore support vessel providers like Tidewater ( TDW ) and SEACOR Marine Holdings ( SMHI ) as well as specialty services provider Helix Energy Solutions ( HLX ).

For further details see:

Borr Drilling: Accelerated Refinancing Could Provide A Near-Term Catalyst - Buy