BORR - Borr Drilling: Q2 Results And Outlook Disappoint - Buy On Weakness

2023-08-17 22:27:03 ET

Summary

- Leading offshore driller Borr Drilling reported mixed Q2/2023 results and reduced full-year EBITDA guidance by approximately 10%.

- Comprehensive refinancing and initiation of a shareholder return policy are not likely to happen before some time next year.

- However, with utilization levels not witnessed in almost a decade, management remained optimistic on the near-term prospects of the jackup markets.

- Company has started discussions with the shipyard to accelerate the delivery of its two remaining newbuilds by approximately one year.

- Given strong market conditions and prospects for 2025 Adjusted EBITDA to more than double from current levels, I am reiterating my "Buy" rating on the shares and would advise investors to initiate or add to existing positions on any major weakness.

Note:

I have covered Borr Drilling Limited ( BORR ) previously, so investors should view this as an update to my earlier articles on the company.

On Thursday, leading offshore driller Borr Drilling Limited or "Borr Drilling" reported mixed Q2/2023 results and reduced full-year EBITDA guidance by approximately 10% at the mid-point of the ranges provided by management.

Company Presentation

In contrast to management's expectations stated on the Q1 conference call , both revenue and profitability improved substantially on a sequential basis but still fell short of consensus estimates .

Unfortunately, the company continues to burn cash, albeit at a moderate level. Given this issue and considering the strong performance of the stock, I wasn't exactly surprised about the company selling approximately 1.3 million newly issued shares into the open market for gross proceeds of $9.7 million last month.

Even worse, Borr Drilling lowered full-year Adjusted EBITDA expectations quite meaningfully from the previously provided $360 to $400 million range (emphasis added by author):

In July 2023, one of our customers in West Africa cancelled previously exercised options for our rig “Gerd” . Subsequently, we were immediately able to secure new work for the rig in the Middle East at economics which we view as even more favourable, and in a region where we see better long-term prospects.

The change of contract for this rig will lead to some idle time before it commences its new contract in December 2023, which will impact results in the second half of this year , however this will improve our position in 2024 and beyond. We also intend to bring forward the rig’s periodic surveys during this idle period which will mitigate out of service periods previously anticipated in 2024.

Based on these developments, our full year Adjusted EBITDA in 2023 is now estimated to be between $330 to $360 million . We expect our financial performance in the third quarter of 2023 to be similar to the second quarter, which we expect will be followed by an increase in the fourth quarter, when for the first time all of the Company’s 22 delivered rigs will be in operation.

To be perfectly honest, I was surprised about the cancellation of previously exercised options not triggering an early termination fee.

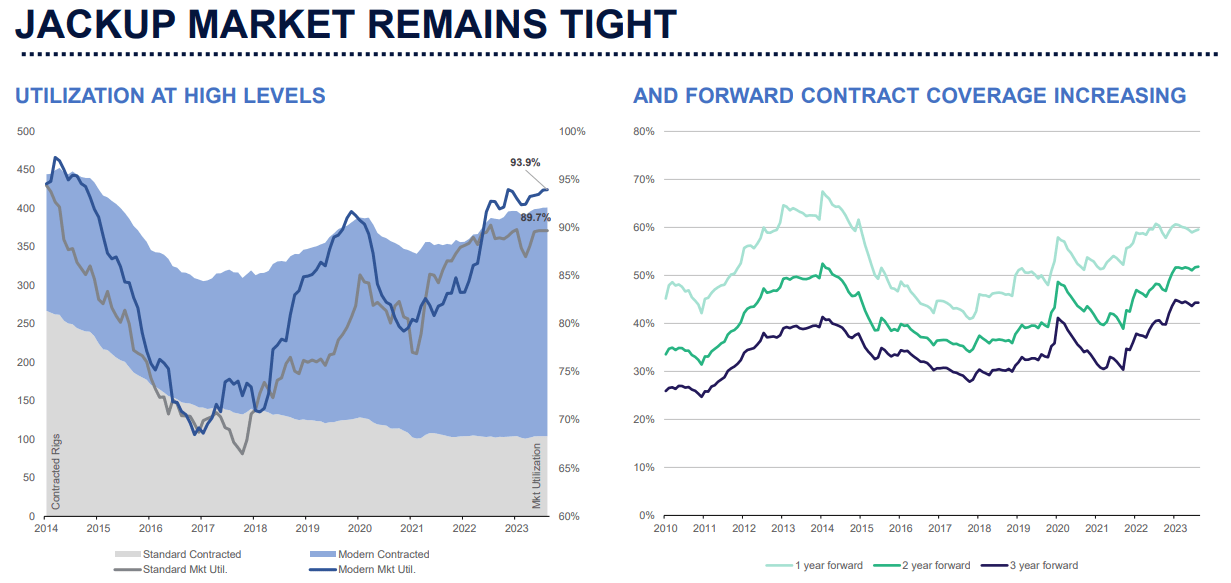

However, with utilization levels not witnessed in almost a decade, management remained optimistic on the near-term prospects of the jackup markets.

{kind=link}

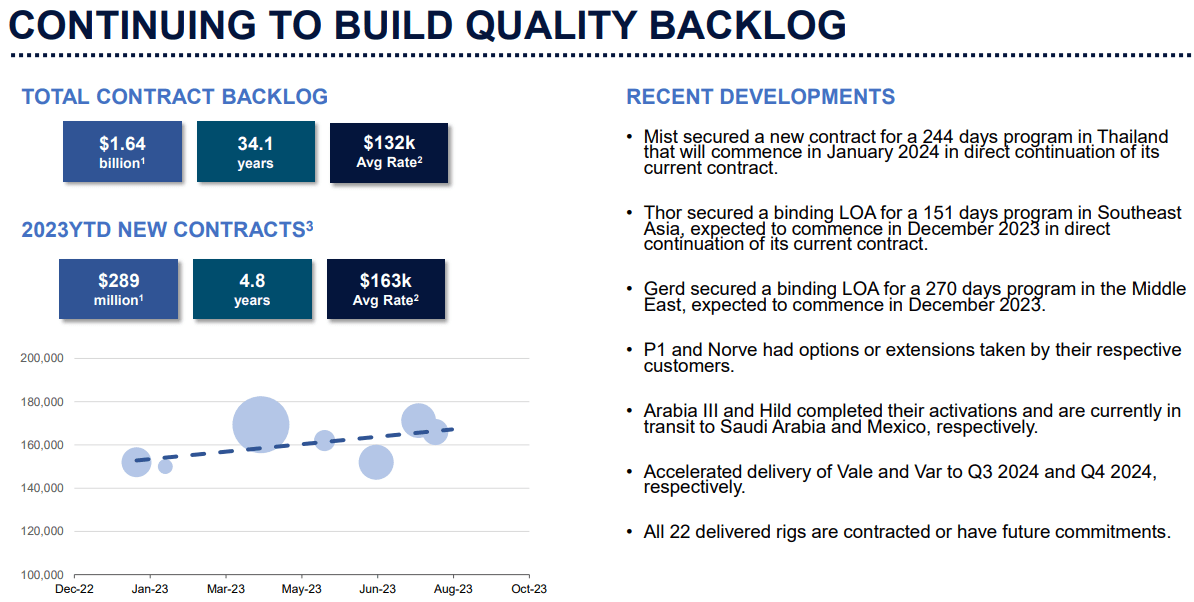

In fact, with the entire fleet being contracted, the company has started discussions with the shipyard to accelerate the delivery of the remaining newbuilds (emphasis added by author):

Supported by our confidence in the jack-up rig market, we are in active discussions with Seatrium, formerly Keppel, for an expedited delivery of our rigs Vale and Var to August and November 2024 , respectively as we see significant opportunity to increase earnings with having these last two top-tier rigs available.

At the end of Q2, total contract backlog amounted to $1.65 billion, basically unchanged from the end of the first quarter:

{kind=link}

Looking further out to 2024, with 70% contract coverage at an average dayrate of $127,000, management projected Adjusted EBITDA of between $500 million and $550 million for next year.

With a substantial number of rigs expected to roll over from legacy contracts to prevailing market rates over the next 18 months and considering the anticipated delivery of the remaining newbuilds, 2025 should see a further jump in profitability with Adjusted EBITDA potentially reaching $800 million.

Assigning a 2025 EV/EBITDA ratio of 6x would yield a $12.50 price target for the shares.

During the questions-and-answers session of the conference call, a number of questions focused on prospects for a near-term refinancing of the company's debt facilities in order to create a path for shareholder returns similar to competitors Seadrill ( SDRL ), Noble Corp. ( NE ) and Valaris ( VAL ) in recent months.

While management reiterated its intent to " refinance at the earliest opportunity " and expected to be in a position " to make the first steps towards this refinancing within this year ", it seems pretty clear that a comprehensive refinancing transaction is unlikely to be completed before sometime next year which removes a potential near-term catalyst for the shares from the equation.

Bottom Line

Suffice to say, I am disappointed by Borr Drilling's lowered 2023 outlook and apparent lack of prospects for a comprehensive near-term refinancing.

However, with the company still generating negative free cash flow, dividends or share buybacks do not seem to be appropriate at this time anyway.

But even after lowering my profitability expectations for 2025, the company is trading at an inexpensive 2025 EV/EBITDA ratio of 4.3x.

Assigning a 2025 EV/EBITDA ratio of 6x would yield a $12.50 price target for the shares.

Given strong market conditions and prospects for 2025 Adjusted EBITDA to more than double from current levels as well as the likely initiation of dividend payments and/or share repurchases at some point next year, I am reiterating my "Buy" rating on the shares and would advise investors to initiate or add to existing positions on any major weakness.

Risks

Offshore drilling stocks often trade in close correlation with oil prices so investors need to prepare for some elevated volatility from time to time.

In addition, a further increase in interest rates could hamper Borr Drilling's refinancing efforts.

Lastly, the company needs to secure additional work at sufficient terms for next year in order to deliver upon management's projections.

For further details see:

Borr Drilling: Q2 Results And Outlook Disappoint - Buy On Weakness