BORR - Borr Drilling: Still Undervalued But The Easy Money Has Already Been Made

2024-01-05 04:58:56 ET

Summary

- Borr Drilling is a top choice for capitalizing on the current bull market in the shallow-water offshore sector.

- BORR has the youngest and most modern fleet among its peers, which puts it in the best position to outperform.

- Day rates still have a significant upside and may rise to $250k per day based on historical analogs, the status of the order book, and current utilization levels.

- The company trades at a forward EV/EBITDA multiple of less than 4x.

- Further share appreciation can come from debt reduction and an increase in dividend payments, underpinned by strong cash flow generation over the coming years.

As the saying goes, there is always a bull market going on somewhere. One particular market that may not have received much attention, but has certainly made fortunes for attentive inflection investors, is in shallow-water offshore drilling.

Deep-water drilling attracts the majority of attention in the offshore oil industry, making the shallow-water sector often overlooked. However, the vast majority of drilling operations take place at depths below 500 feet. This is the realm of jack-up rigs. Jack-up rigs are mobile drilling platforms. They differentiate themselves from "floaters" (semisubmersibles and drillships used in deep and ultra-deep waters) by their "legs". The legs can be raised or lowered, allowing the rig to be placed firmly on the seabed and later moved to a different location.

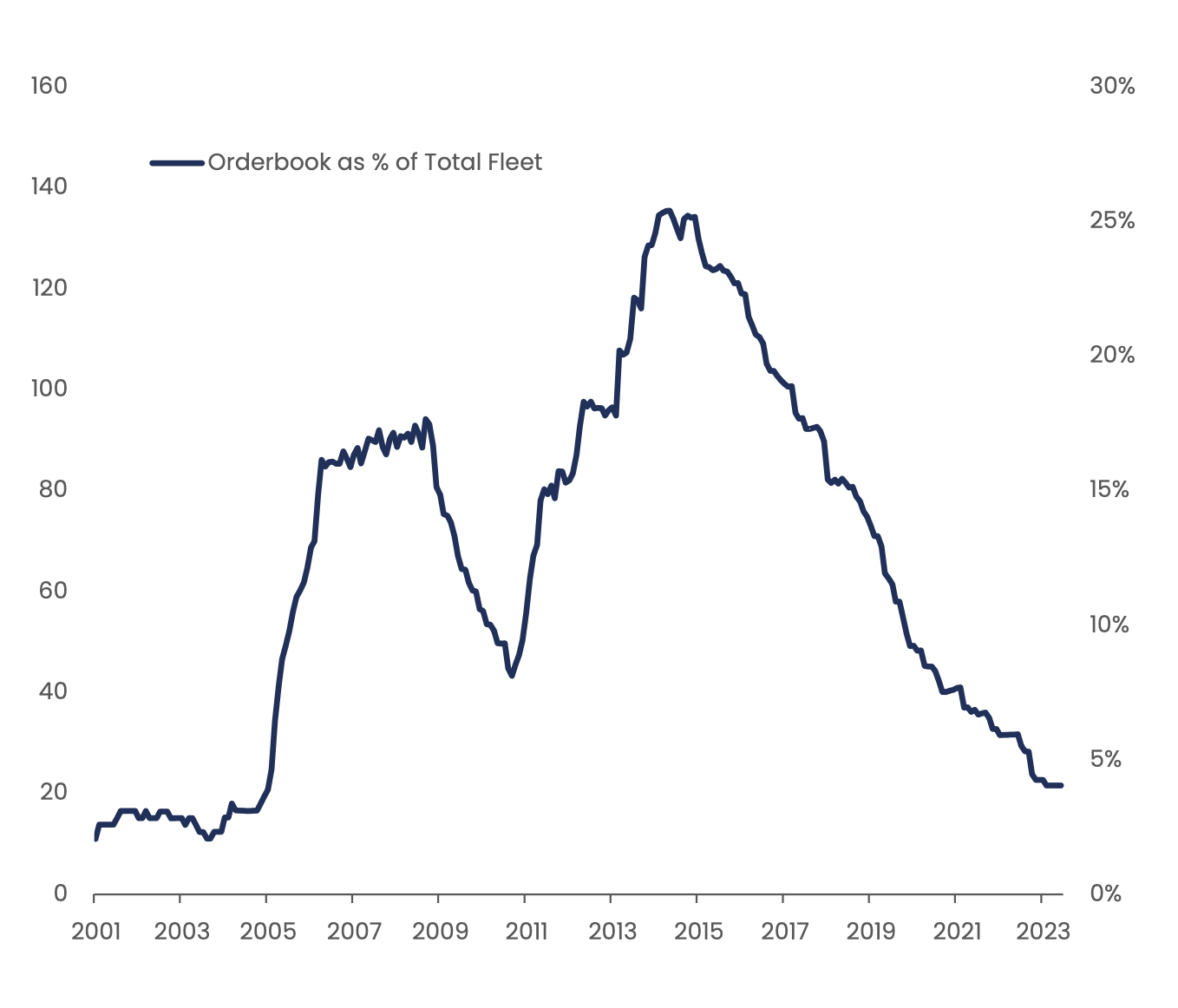

The market for jack-up rigs hit a bottom following the oil price crash in 2014, as US shale became the world's swing oil producer. As demand started to rapidly contract, supply kept expanding. The order book for jack-up rigs reached a peak around 2015 at 140% of the existing fleet. Since then, the order book has fallen dramatically and now stands at just 3%, a level not seen since the early 2000s.

The orderbook is near an historical minimum (Company's Presentation)

{kind=link}

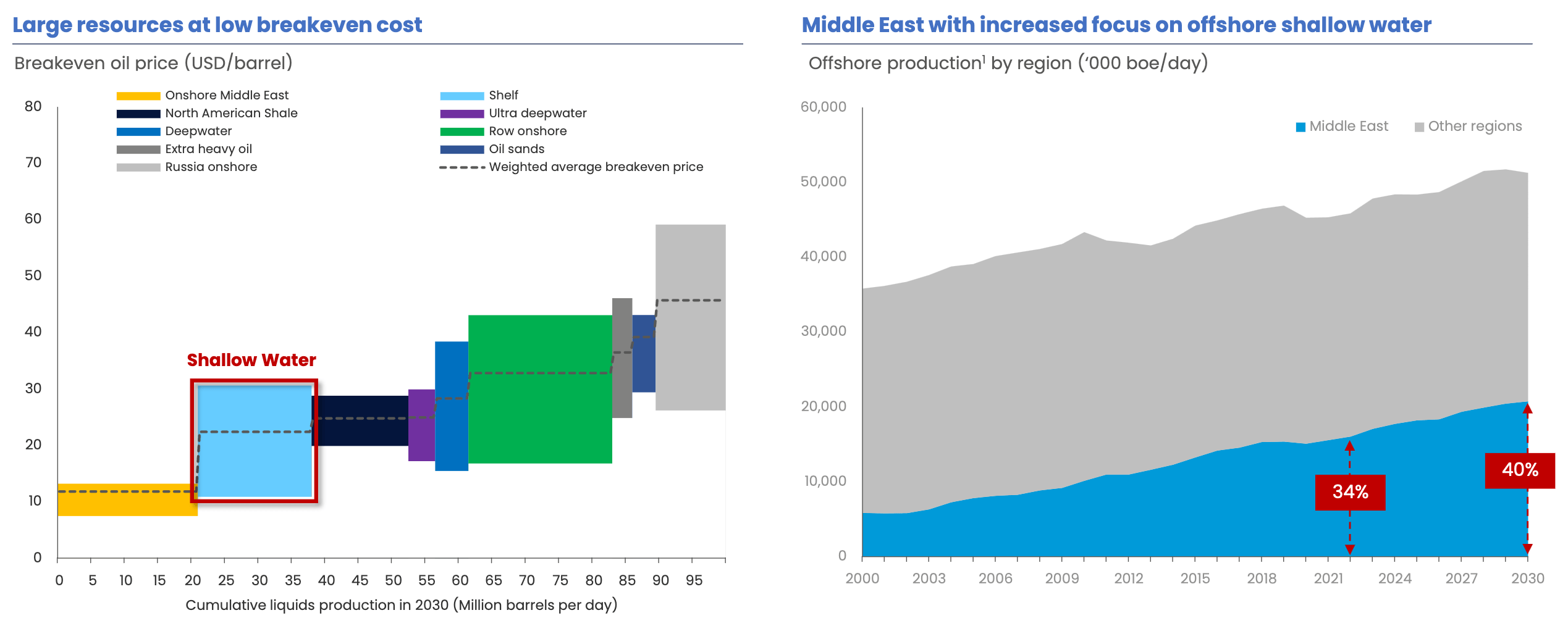

Despite the reduction in supply, the market has been slow to recover. Offshore projects are long-cycle: they require many years to pay out, so demand doesn't respond immediately to price signals. The risk is always that shale may ramp up production and balance the market before offshore projects have even started generating cash flow. Nonetheless, after a rapid recovery post-COVID, US shale may now be close to peaking. Most analysts believe that oil demand will continue to rise over the coming decade and that the majority of supply growth will come from offshore shallow-water resources . In fact, as shown by the following visualization, shallow-water represents the largest and most economical untapped resources available (after onshore Middle East), with an average breakeven price just above $20 per barrel.

Shallow-water resources are the next untapped, low-cost oil resources to be developed after onshore Middle East (Company's Presentation)

{kind=link}

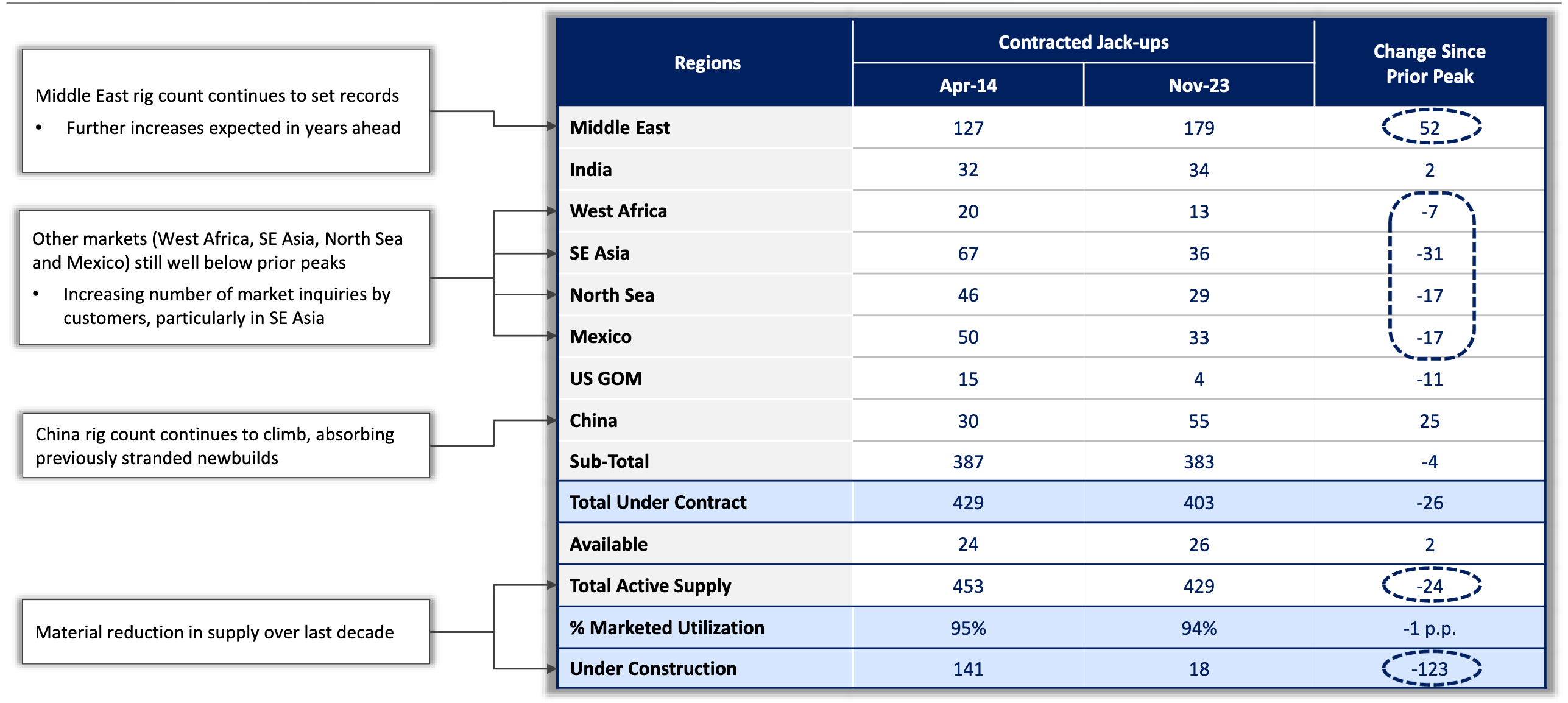

It is, therefore, no surprise that demand for jack-up rigs is rising . The following table shows that most of the demand is coming from the Middle East, where the number of contracted jack-ups between 2014 and 2023 has increased by over 40% (from 127 to 179 rigs). Demand from other regions still remains below the historical peak. However, the increase in demand from the Middle East has absorbed excess supply and created dislocations in the rest of the world. Currently, utilization stands at 94%, with a spare capacity of only 26 rigs (out of a total of 429 rigs in the global fleet). Correspondingly, the number of cold and warm stacked units has rapidly declined. The market has tightened, and day rates have been steadily surging.

Jack-up rigs by region, 2014 vs. now (Company's Presentation)

{kind=link}

As a result, the profitability of jack-up operators has increased, which has allowed many of them to start deleveraging and paying out dividends. In turn, share prices have appreciated significantly. For example, Borr Drilling is up 60% over the last 12 months. It is unquestionable that most of the easy money has already been made in this sector. However, this does not mean that there is no further upside. The key questions now are whether day rates will continue to improve or will mean revert, and, assuming they will continue to rise, how much of this is already priced into the equities.

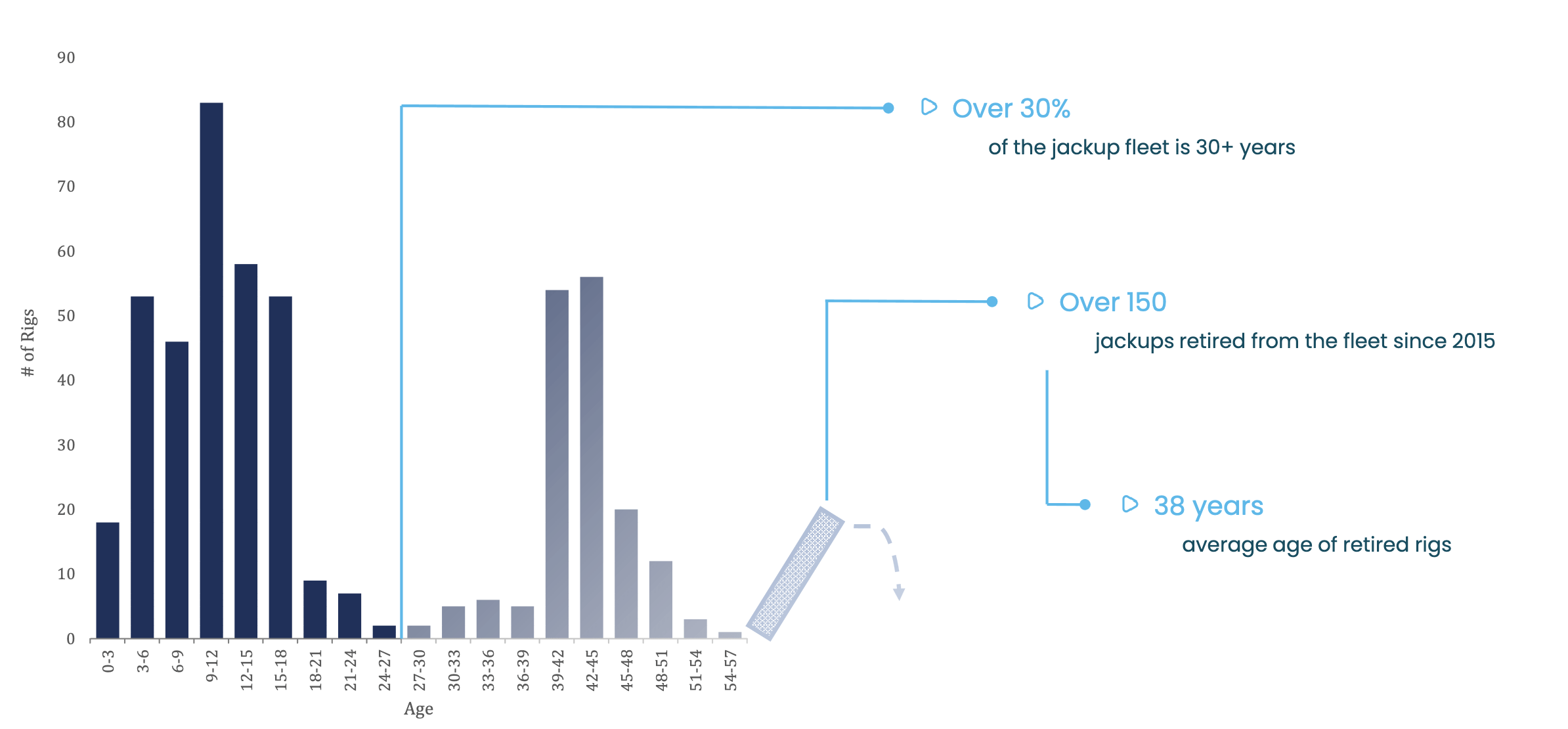

The answer to the first question is that rates are likely to keep rising in the near and medium term. This is because rates are mostly a function of utilization. Utilization is already near its historical peak, and it is unlikely to contract meaningfully. Offshore contracts are long-lasting; they cover several quarters, providing significant visibility into future demand. For example, Borr Drilling ( BORR ) discloses that the average duration of its contracts is around 1.7 years. Moreover, supply is also slow to respond. It takes more than three years to build a new rig. Because of inflation, construction costs are skyrocketing. Shipyards' capacity is constrained by a flurry of new orders in other shipping segments. Furthermore, the global jack-up fleet is aging, with over 30% of the fleet being over 30 years old.

{kind=link}

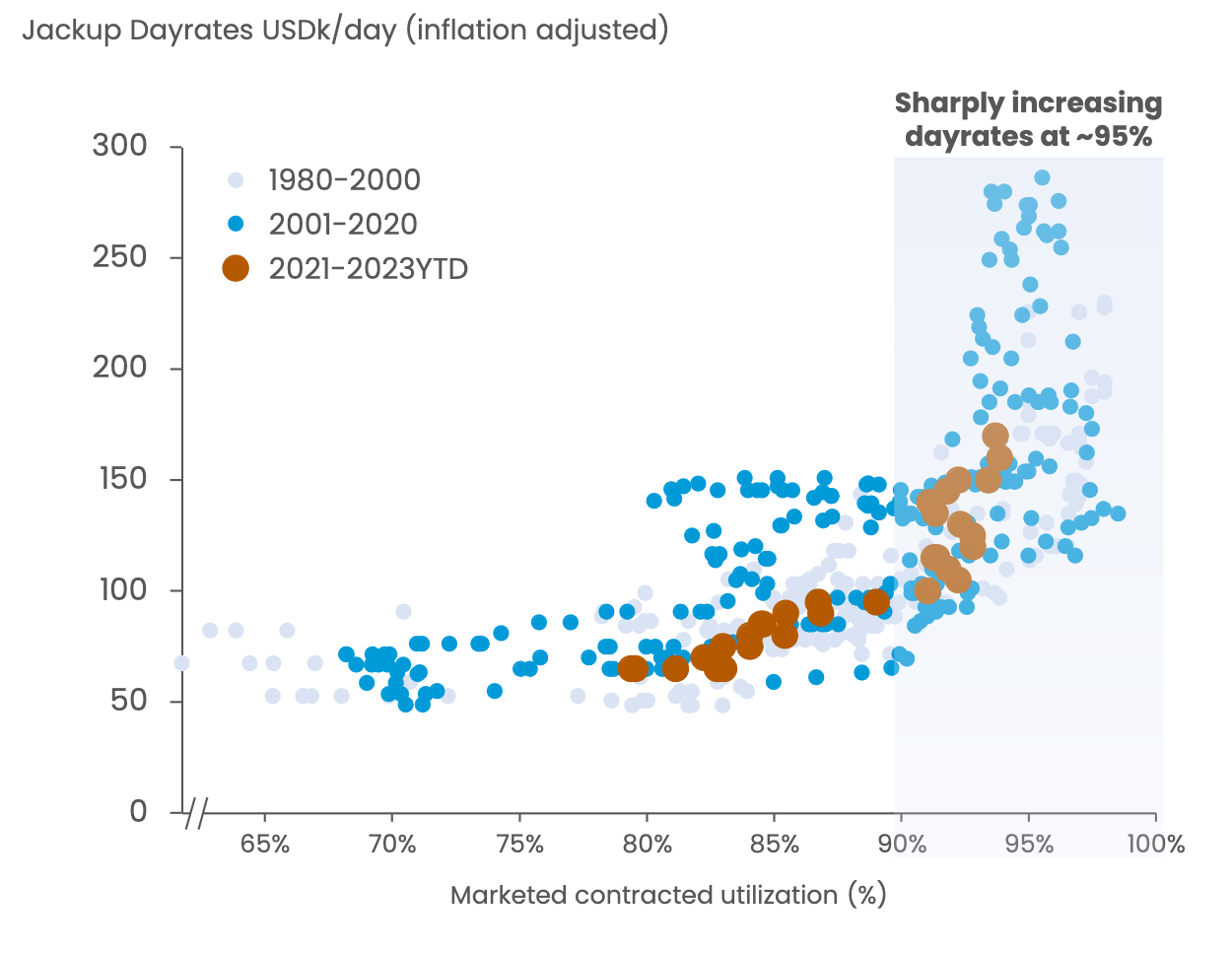

How high can rates go? Borr Drilling provides the following interesting visualization. Historically, when utilization approaches 100%, rates have gone as high as $250k per day in inflation-adjusted terms. Jack-up rates are currently around $160k per day, so there is still some meaningful upside. Moreover, as already explained, it takes some time for new rates to trickle down into the financial results of companies. For example, according to its latest Q3 2023 presentation, Borr Drilling has already contracted 84% of its 2024 days at $132k per day, 60% of 2025 at $135k per day, and 8% of 2026 at $134k per day. Therefore, the downside is protected. Simultaneously, new contracts are being signed at an average rate of $161k per day, and day rates are expected to continue rising.

Correlation between dayrates and utilization (Company's Presentation)

{kind=link}

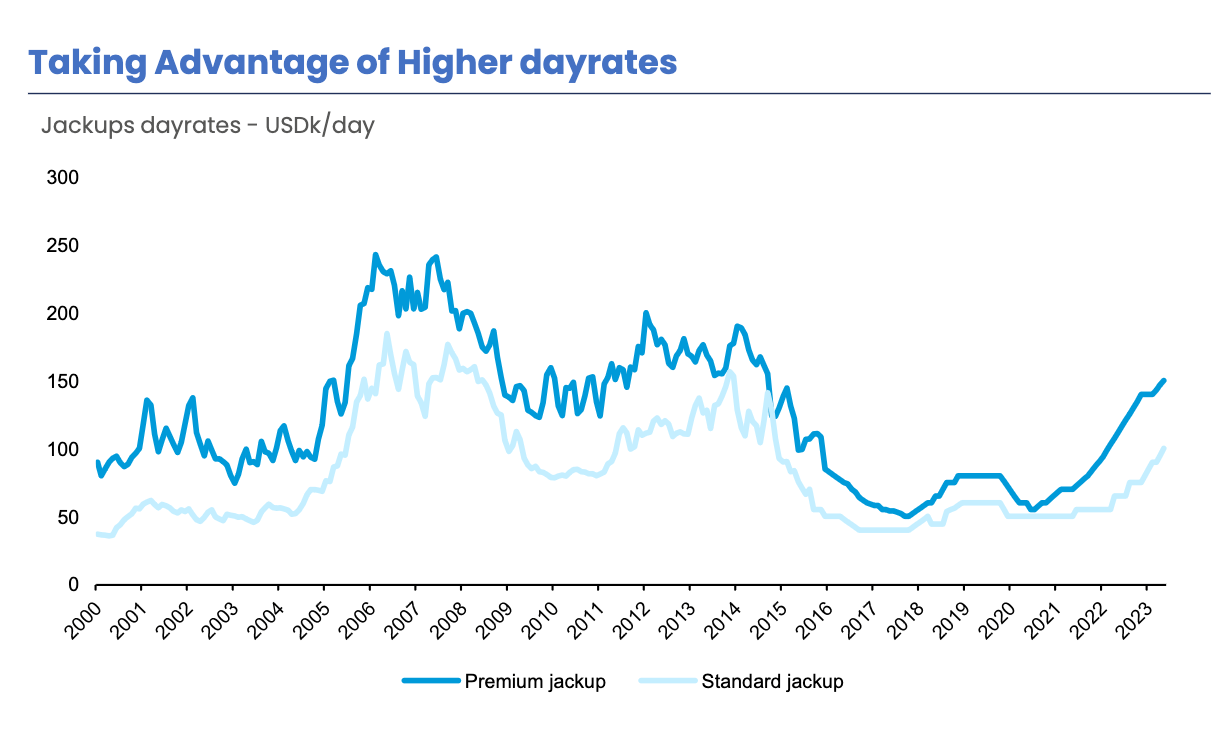

This is particularly true for premium jack-ups. Premium jack-ups are recently constructed rigs featuring the most modern designs. Customers prefer premium rigs over standard rigs due to their higher specifications, lower costs, and stronger operational KPIs, such as faster connection times and higher tripping speeds. Premium rigs outperform in a bull market and are more resilient during a downturn.

Premium rigs outperform standard rigs (Company's Presentation)

{kind=link}

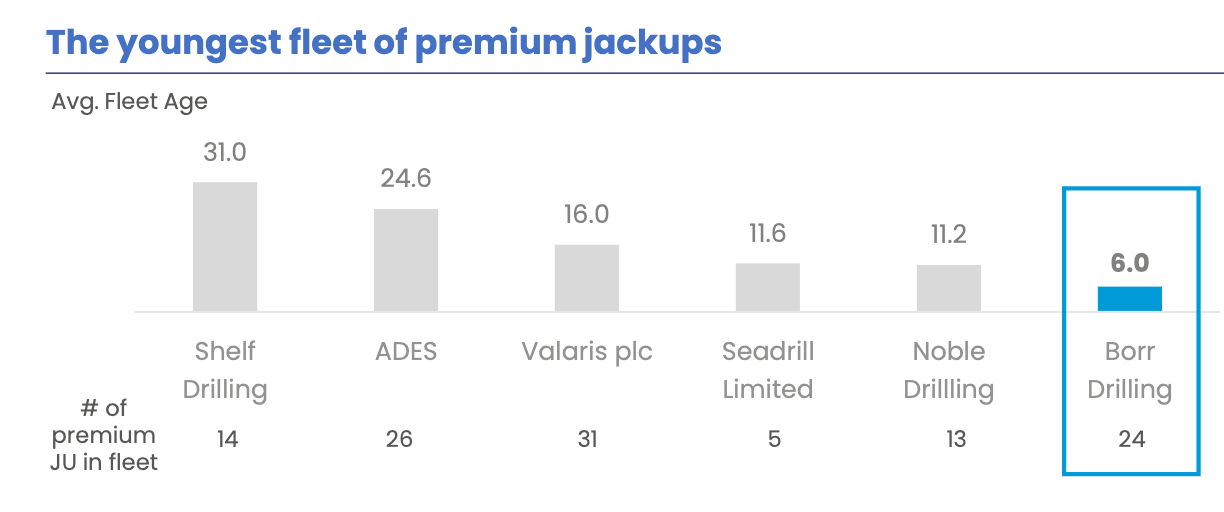

Borr Drilling owns 24 premium jack-ups (two are still under construction and will be delivered next year). The average age is only six years, which is the lowest among its peers. This is key to Borr Drilling's ability to outperform financially.

BORR has the youngest fleet among its peers (Company's Presentation)

{kind=link}

Let us now examine the valuation. The company has a market capitalization of around $1.8 billion and approximately $2 billion in debt. Recently, it has managed to refinance its debt, which had significant near-term maturities in 2025. After refinancing, the new maturity profile peaks in 2028 and beyond. The company has generated $88 million in Adjusted EBITDA over the last quarter, with an Adjusted EBITDA margin of 46%, an uptime of 99.1%, and an average rate of $137k per day. Assuming that rates continue to improve until they reach $250k per day by 2026, and maintain the same uptime and EBITDA margin as above, a straightforward back-of-the-envelope calculation indicates that Borr Drilling could generate around $1 billion in EBITDA. If one is bullish on the jack-up market, Borr Drilling is trading at a forward EV/EBITDA multiple of less than 4x. The company can use the cash to deleverage in the near to medium term. In fact, it has already expressed its intention to reduce total debt to below 1.5 times EBITDA. After deleveraging, the focus will shift to shareholder returns, i.e., to increasing the current dividend of 5 cents per share and the extent of share buybacks.

In conclusion, Borr Drilling is a top choice for capitalizing on the current bull market in the offshore sector. It benefits from being a pure play on shallow water offshore, which is likely to see faster and less volatile growth compared with deep water. Moreover, the company has the youngest and most modern fleet among its peers, which suggests lower operating expenses and higher day rates. While the inflection point has passed and the initial re-rating of the entire sector has taken place, I still perceive some meaningful upside. This is particularly true given the undemanding current valuation. As day rates continue to improve on the back of a record-low order book and record-high utilization, Borr Drilling will have the opportunity to renegotiate contracts at higher rates. The potential for cash flow generation is significant: Borr Drilling may generate about $1 billion in EBITDA by 2026. The cash will initially be used to aggressively reduce the debt burden, which will eventually enable the company to significantly increase dividend payments. For all these reasons, I am bullish.

For further details see:

Borr Drilling: Still Undervalued, But The Easy Money Has Already Been Made