BORR - Borr Drilling: The Rating Agencies Are Turning Positive Too

2023-11-14 21:24:33 ET

Summary

- Borr Drilling completed a successful refinancing, pushing most of its maturities out to 2028-2030.

- The rating agencies have turned positive on the improving industry fundamentals, suggesting the debt will be less of a concern going forward.

- The leverage should now start working for the equity investors as modest improvements in EBITDA or the valuation multiples will have a big impact on the share price.

Investment thesis

Borr Drilling ( BORR ) completed a major refinancing that pushed most of its maturities out to 2028-2030. This milestone seems to have been perceived positively by the rating agencies that now note the positive outlook for BORR's shallow water drilling business.

With any residual debt concerns out of the way, the market's focus should shift to the rapid utilization and dayrates for premium jack-up rigs. The improving environment may also turn the refinanced debt into a good thing by adding "torque" to the equity.

It's worth mentioning the refinancing was accompanied by a modest equity raise of $50 million. While this was dilutive, the silver lining is the equity offering was targeted toward large investors (read "smart money") who purchased shares at an average implied price of $6.64.

As BORR can be currently purchased for $6.10, this looks like a buying opportunity if you missed the rally from the summer 2022 lows. Wall Street analysts have an $11 average price target.

The refinancing was a success overall

I have written about BORR on Seeking Alpha before, so I will refer to my prior pieces for context to the recent events:

Borr Drilling : What To Make Of The Refinancing Mess ((NYSE:BORR))

Borr Drilling : The Jack-Ups Orderbook Is At 20-Year Lows ((NYSE:BORR))

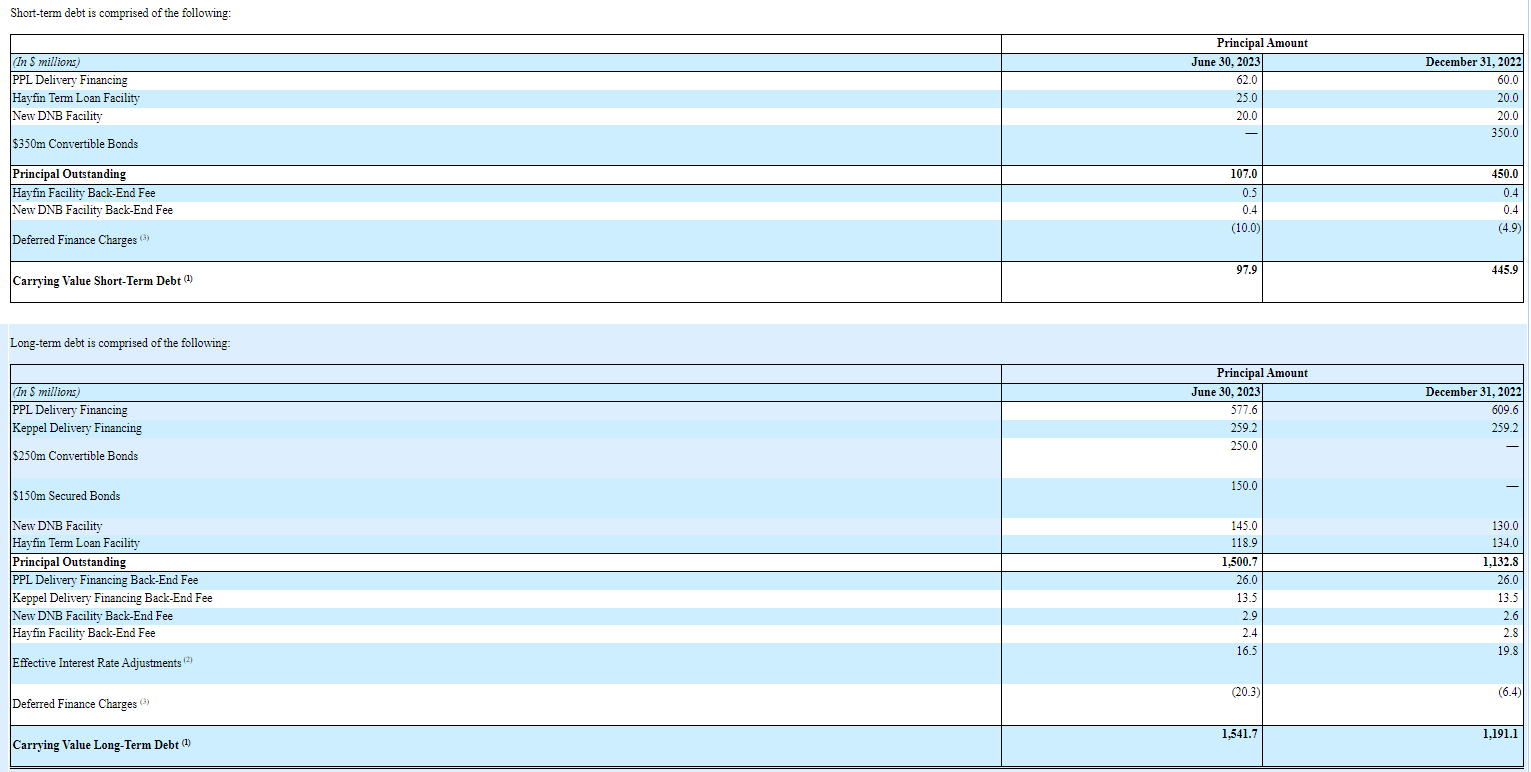

Borr Drilling exited Q2 with about $1.6 billion of debt distributed among a couple of shipyard financing facilities, a DNB facility, and secured bonds:

{kind=link}

The bulk of these maturities fell in 2025:

{kind=link}

All of these borrowings plus back-end and other fees are now being consolidated into two senior secured note tranches:

| Maturity |

| Principal |

| Coupon |

| 2028 |

| $1,025,000,000 |

| 10.000% |

| 2030 |

| $515,000,000 |

| 10.375% |

The obvious outcome was to lengthen the maturities. In my view, consolidating multiple secured facilities and dealing with fewer lenders and covenants is also a positive side effect. Adding further flexibility, Borr also entered into a $180 million "super senior" revolving facility, secured on the basis of same collateral as the new 2028 and 2030 notes.

The 2028 notes trade this week basically at par with option-adjusted spread of 531 bps per Refinitiv. The 2030 notes trade a sliver below par at 582 option-adjusted spread.

Considering risk-free rates are almost 5%, the coupons aren't a bad deal. Compare also to Tidewater's ( TDW ) 2028 notes which trade today at a 468 bps option-adjusted spread. Given Tidewater emerged from bankruptcy with very little debt, the slightly higher spreads on BORR's notes appear to be a vote of confidence from the market.

The rating agencies have turned positive

I have talked about the vastly improving fundamentals in my prior articles so I won't reiterate my offshore services thesis, but it's quite encouraging the notoriously nearsighted credit rating agencies seem to be picking up on these trends too.

Borr earned positive commentary from S&P which was mulling a BB- preliminary rating for the new notes:

We believe Borr Drilling's modern fleet will allow it to maintain high utilization and generate above $500 million of EBITDA from 2024 and above-average profitability compared with drilling peers...

The stable outlook indicates that we anticipate a rapid deleveraging that will allow Borr Drilling to quickly move FFO to debt toward 30%, and potentially above 30% from 2024, as well as a supportive liquidity profile with no maturities in the next few years.

Yesterday Fitch came out with B rating and also very positive commentary hitting on all of the key points in the Borr bull thesis:

Positive industry dynamics:

The jack-up rig market is showing signs of recovery as some supply of rigs has left the market over the last five years. Further security-of-supply concerns alongside supportive hydrocarbon prices have resulted in renewed demand for jack-up rigs from major producers as they look to replace reserves. Fitch expects Borr's day rates and rig utilization, which have been increasing year-to-date, will continue to improve as recently signed contracts ramp up and existing contracts expire and are repriced.

Backlog provides near-term Revenue Visibility:

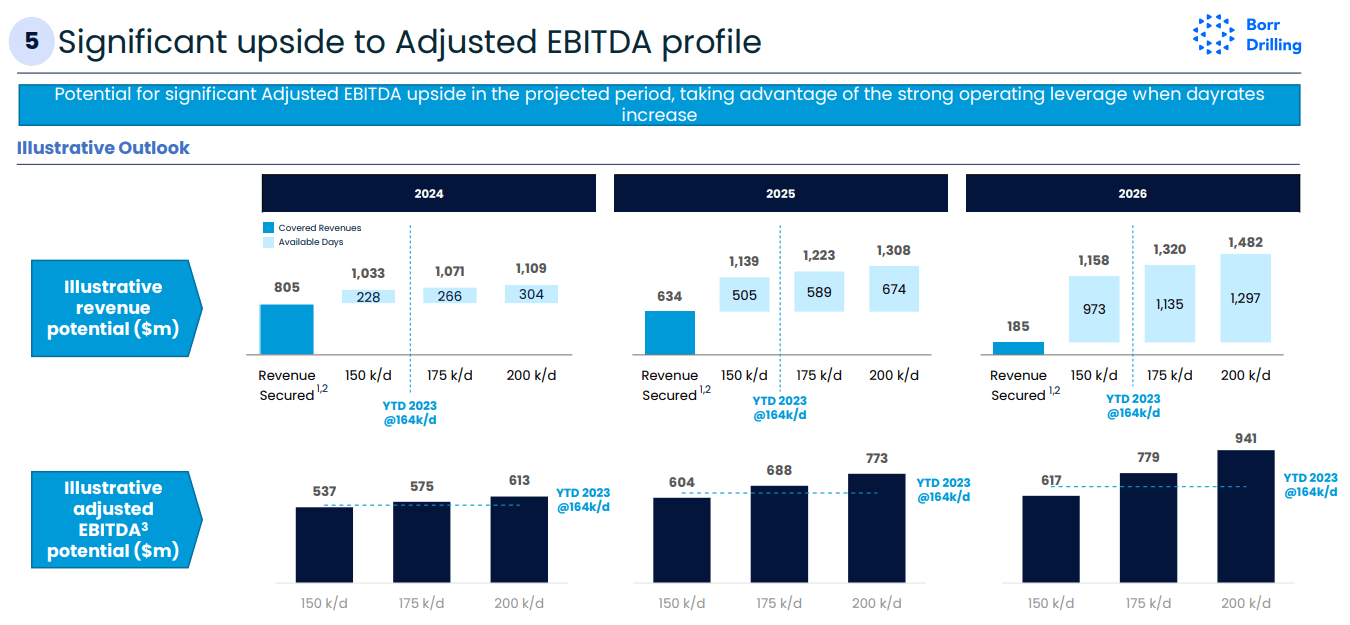

Borr's 2Q23 backlog was $1.9 billion. Of this, $805 million is set to be realized as revenue in 2024 and $634 million in 2025, covering around 86% and 62%, respectively, of our revenue forecast for these years. This substantially reduces the downside risk to our expectation of deleveraging and a return to positive free cash flow generation.

High-spec jack-up fleet:

With an average age of around six years, Borr's jack-up fleet is among the newest on the market. The fleet of high-specification rigs is expected to have relatively low run-rate capex requirements of around $30 million-$40 million a year, with assets able to service complex projects in a variety of geographies. We expect the company's assets to be sought after by customers looking to develop higher complexity shallow-water projects where the efficiency and technical specifications of rigs are key.

Particularly on the last point, Fitch also draws comparison in BORR's favor to the older jack-ups owned by Shelf Drilling ( SHLLF ) and Valaris ( VAL ).

The leverage should start working in favor of the equity investors

BORR's projections suggest $750 million in EBITDA can be attained by 2025 or 2026:

{kind=link}

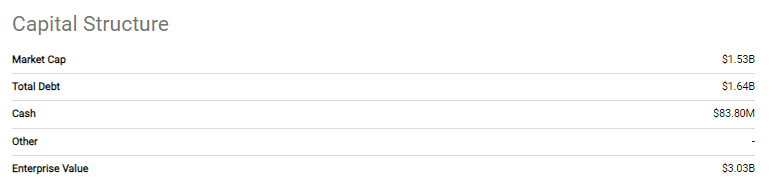

Given today's capital structure, that is a 4x enterprise value to EBITDA multiple:

{kind=link}

To illustrate the leverage effect of the 50:50 debt to equity capitalization, consider a re-rating of the multiple to 5x. That is an additional $750 million enterprise value which translates into a 50% upside for the equity for $9 per share. In a strengthening environment when the debt is getting de-risked, the leverage can be a positive factor.

Lastly, the Fitch report also alludes to a $3.4 billion valuation on a liquidation basis for BORR's existing assets, sans the newbuilds, based on a recent appraisal. Even this liquidation value exceeds the current enterprise value.

Target and risks

At a 5x multiple to 2025-6 EBITDA, BORR is worth $9 per share. At a 6x multiple, that could be $12.

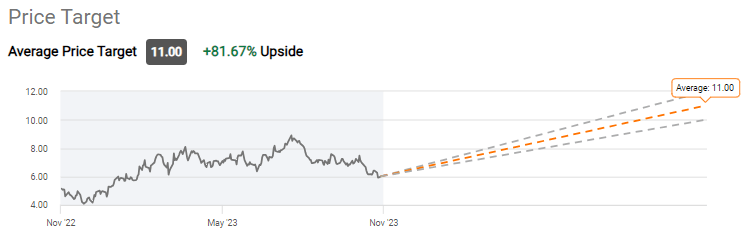

Seeking Alpha's reported Wall Street average is $11:

{kind=link}

According to Refinitiv, Fearnley Securities issued a NOK 118 (Norwegian krone) or $10.65 target on Nov. 1st; Arctic Securities, another broker, was at NOK 105 or $9.48 as of Oct. 30th.

When it comes to risks, I am less worried about the oil industry macro. BORR caters to long-cycle projects that won't be as affected by cyclical drops in the oil price. One item worth noting though is the exposure to PEMEX cited as a negative factor by Fitch too. If you follow the energy industry, you know that PEMEX is undergoing a lot of trouble and is late on its bills to suppliers. According to this recent article , oilfield services major SLB ( SLB ) was owed $1 billion by an "unnamed" customer in Mexico. This could be an issue for BORR too.

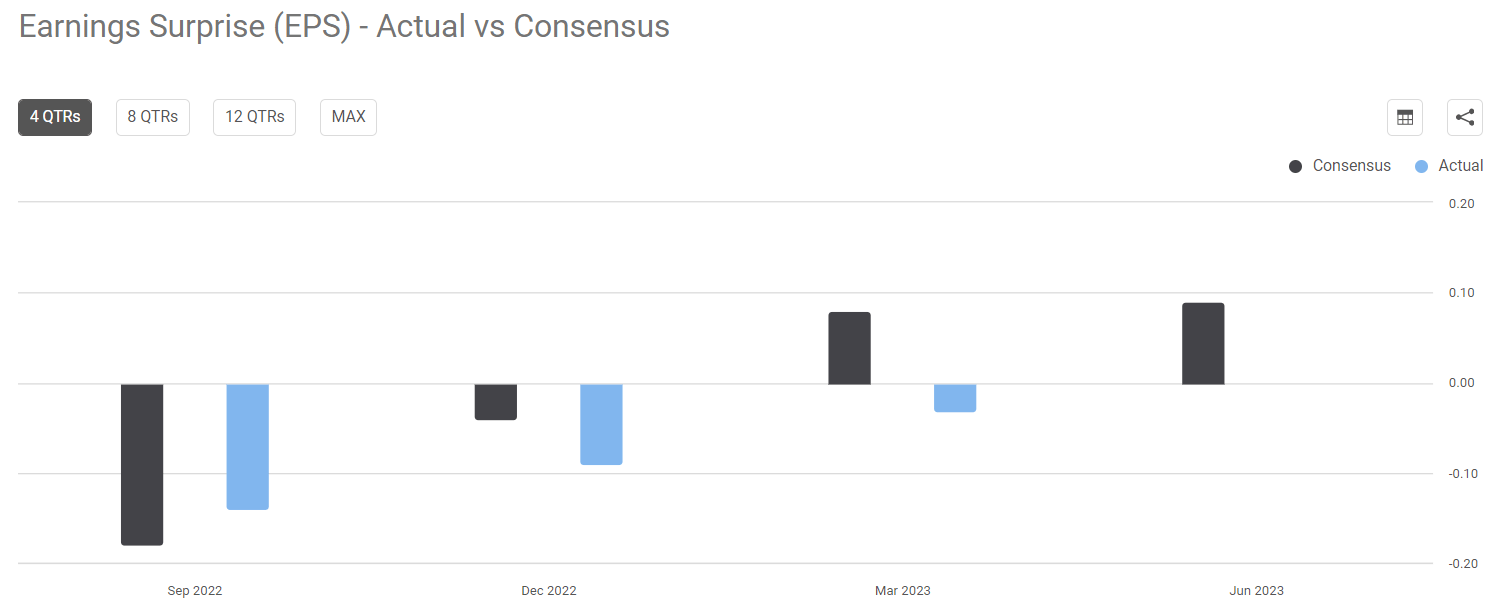

Q3 earnings preview

The consensus estimate for the coming Q3 release is $0.07 earnings per share. BORR has missed estimates for the last three quarters:

{kind=link}

If that happens again and the stock reacts downward, I may add more to my position. Ultimately, the EPS for BORR and other offshore drillers is bit of a non-event given the slow re-rating process of legacy contracts. What I will be watching for is the forward guidance on the industry trends.

An earnings beat on the other hand may push up BORR considerably, considering both Borr Drilling and other offshore drillers have been a bit oversold lately.

Bottom line

I am having a hard time rationalizing the recent BORR correction, except as driven by overall oil prices and negative sentiment from the $50 million equity raise. Obviously, earnings are due soon so there always could be surprises, but given the slow and steady trend in dayrates, I am not sure what will change that much. I think the current $6 is a buying opportunity, and, technically, the stock is also close to oversold territory, though not as extreme as July 2022, when I was fortunate to be able to add in the $2s.

For further details see:

Borr Drilling: The Rating Agencies Are Turning Positive Too