BOC - Boston Omaha Corporation: Valuing The Potential REIT Spinoff

Summary

- Boston Omaha is a small conglomerate that has been slowly building its businesses and adding new industries.

- It currently operates in the highly profitable insurance, billboard, and broadband industries.

- As of late, management has announced a new venture, real estate.

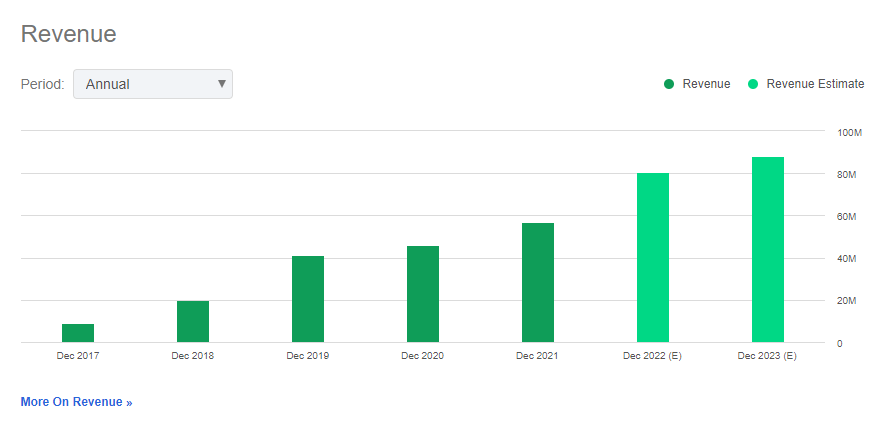

I have previously written an article that details the operations and valuation of Boston Omaha Corp. ( BOC ) to gain a better understanding of its business units. At a high level, the company operates across several industries with high margins consisting of indemnity insurance, billboards, fiber infrastructure, and asset management. Each one of these divisions has grown substantially over the past several years and each have strong potential for large future growth.

History

BOC has benefited from excellent execution and a disciplined mindset by choosing to operate with minimal debt and involving the company in high cash flow producing industries. Per the most recent earnings report, the company possesses a total value of $674.7mm in assets and currently has a price to book ratio of 1.49. Book value per share is the metric that management prefers and early stage Berkshire Hathaway ( BRK.A ) preferred for valuing their conglomerates. BOC has been successful in consistently growing this value and believe they have identified a new path for accelerating the book price and cash flow to the company.

{kind=link}

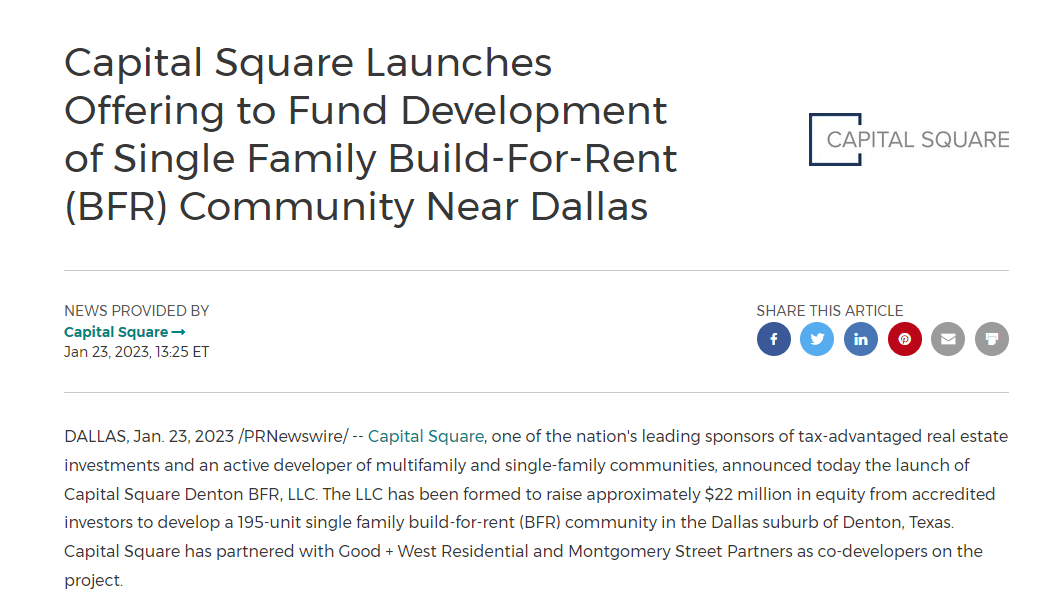

Build For Rent

In 2022, a major announcement was made that a new additional business route would be pursued in the form of real estate. Leveraging the Boston Omaha Asset Management arm, capital is being raised to the tune of $150 million from outside investors and 10% being raised by the company itself. This capital is to be used for developing "build-for-rent" housing, an economically efficient and focused real estate development model to capture market share in the ever-growing rental market. To highlight how attractive this business is, take a look at several major players that have recently announced their involvement in this space.

{kind=link}

{kind=link}

As stated in the most recent annual report, the ultimate goal for this fund is to spin it off as a standalone REIT. This intention is extremely appealing, above the appeal of just becoming involved in real estate development alone. In order for me to display the attractiveness of this venture I will attempt to quantify the potential impact this could have for BOC.

REIT Value

To begin this estimate, we will use management's stated goal of a 7% cap rate for these properties and assume BOC sticks to the goal of having a 10% ownership of the fund with its own capital. We also will use a comparison in the market to give us a baseline for valuation multiples and profitability. American Homes 4 Rent ( AMH ) will serve as a peer as they operate with a similar business model.

| American Homes 4 Rent |

| P/FFO |

| 22.40 |

| FFO/Total Revenues |

| 36.09% |

| Net Income Margin |

| 16.30% |

To value BOC's Build For Rent Fund, I will calculate my first estimate using the same metric values as AMH above. Also, I will assume the 7% cap rate is proportional to the net income margin of the revenues. What I mean by this is that I will implement the ratio of FFO margin/Net Income Margin as the multiple for FFO versus NOI.

AMH (FFO/Total Revs)/(Net Income Margin) = 36.09%/16.30% = FFO expectations of roughly 2.2x the net income.

So, to calculate the estimated FFO for BFR I will do the following:

- ($150 million in real estate assets)*(7% cap rate) = $10.5 million in net income

- FFO = (2.2 multiple)*($10.5 million) = $23.1 million for BFR

Lastly, I will use my industry peer P/FFO multiple to determine the market value of the fund.

- BFR Mkt. Value = ($23.1 million)*(22.40) = $517.4 million

While this is based on several assumptions, it is a staggering number to see. Theoretically this means if Boston Omaha were to spinoff this fund as a REIT, it would be valued at $517.4 million, a 245% return from the initial capital raise. Specifically to BOC, with a 10% stake, they would possess an ownership stake worth $51.7 million. Based on most recent asset reporting of $674.7 million, this would represent nearly an 8% increase in total assets. The icing on the cake would be the roughly $1 million in dividends received per year.

I believe BOC has the opportunity to take advantage of its other business units and actually improve the profitability of their real estate portfolio. By owning the fiber optic infrastructure of each home and using its own property management software, I believe FFO margins of 40% are achievable.

- 40% FFO margins translates to an FFO/Net Income multiple of 2.5x

- BFR FFO = (2.5 multiple)*($10.5 million) = $26.25 million

- BFR Mkt. Value = (26.25 million)*(22.40) = $588 million

Therefore, my bull case for the near term would call for $58.8 million stake in the newly formed REIT.

Boston Omaha Corp. Valuation

I have previously detailed my assumptions for the value of the assets on Boston Omaha's balance sheet in my original article and will use them as the basis here as well.

- $517 million in total common equity excluding BFR

- $58.8 million long term asset from BFR

- Fair Value P/B of 1.6x

Using these inputs, total common equity for BOC would be $575.8 million across 29.7m shares, giving us a Book Value Per Share of $19.39.

Bull Case Valuation = ($19.39)*(1.6) = $31.02, a share price more than 20% higher than current.

The important thing to keep in mind is that this doesn't take into account any other growth in assets across the rest of Boston Omaha's business divisions. Over the last 6 years assets have grown 10-fold, meaning a rate anywhere near this kind of growth would skyrocket the bull case valuation.

Risks

The most glaring risk here is execution risk. Boston Omaha will need to hit a home run and prove themselves in a space they currently do not contend in. The housing market is also historically volatile and bad timing could have a huge negative effect on the success of this venture. Lastly, the assumptions and inputs used for the analysis are generous and subject to variation based on real rates of return and lack of pure comparison in the market.

Conclusion

Boston Omaha has been a poster child of responsible growth since its founding and has shown its ability to expand into new areas and execute on its business plans. The track record they have displayed gives me confidence that they will be able to find success in their lofty REIT goals. The accelerator for this conglomerate will be its ability to shed its dependence on secondary offerings for raising cash that dilute total share count and become self-sustaining through REIT distributions and growing profitability of other divisions.

I believe the combination of a strong real estate portfolio and fast-growing, high cash flow businesses will allow for BOC stock to be a cash cow in the future that continues to expand and drive home value for shareholders.

For further details see:

Boston Omaha Corporation: Valuing The Potential REIT Spinoff