BWMN - Bowman Consulting: Great Company But Already Fairly Valued

2023-07-18 22:47:02 ET

Summary

- Bowman Consulting Group Ltd. is a $450-million market-cap engineering consulting company based in the United States.

- From what I see, Bowman reported record-breaking revenue and demonstrated exceptional YoY growth, further solidifying its position in the industry.

- But by my valuation analysis, BWMN has turned out to be already fairly valued. It's a Hold with limited upside potential from here.

The Company

Bowman Consulting Group Ltd. ( BWMN ) is a $450-million market cap company based in the United States that provides a wide range of solutions in real estate, energy, infrastructure, and environmental management. They offer services such as conceptual land planning, permitting, roadway and highway designs, construction administration, traffic studies, wetlands delineation, endangered species surveys, NEPA documentation, and mechanical, electrical, and plumbing engineering.

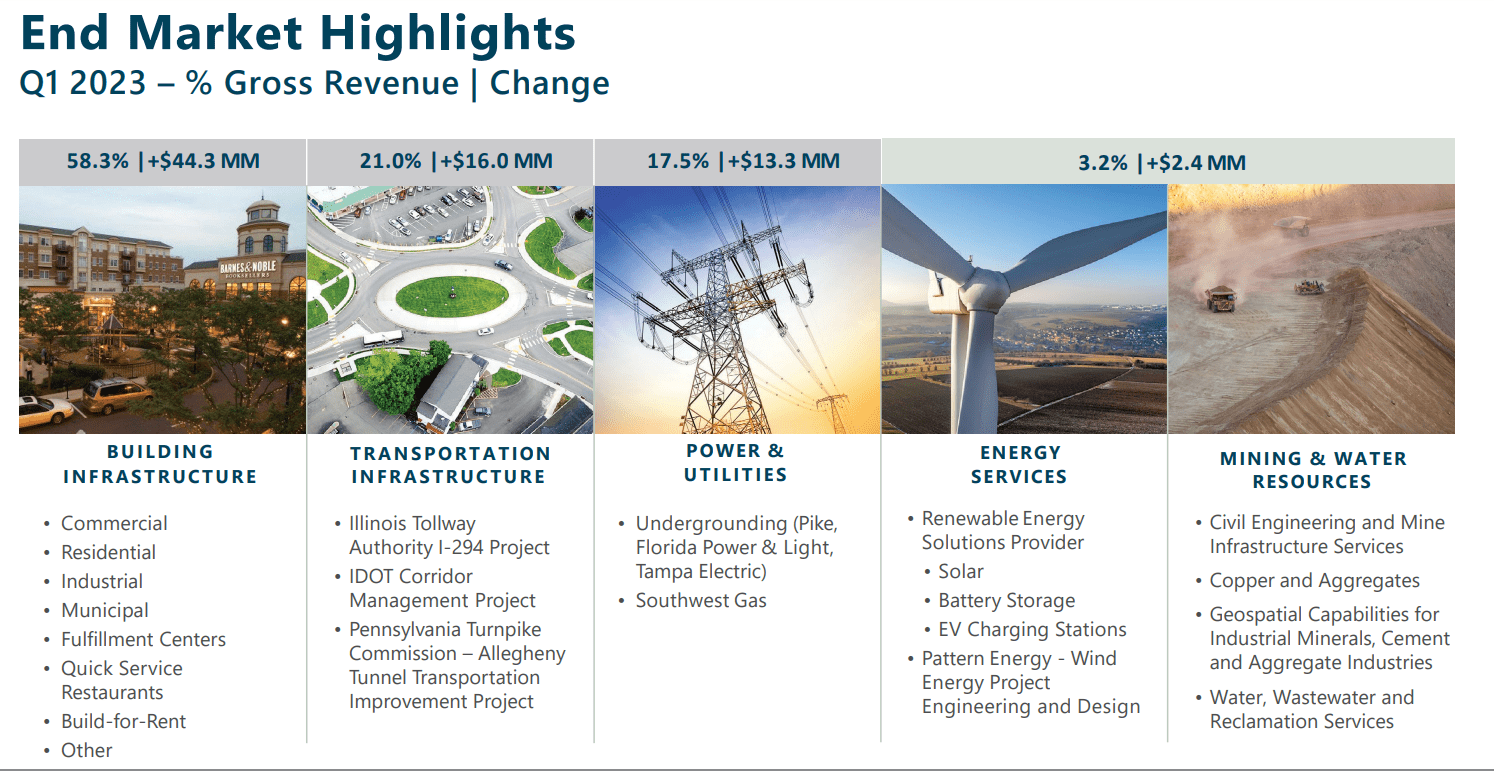

The company operates in a single segment focused on providing engineering and related professional services to its customers, which forms its core business. We can only look at the end markets to assess the firm's diversification:

{kind=link}

BWMN's IR materials for Q1 FY23

From what I see, Bowman reported record-breaking revenue and demonstrated exceptional YoY growth, further solidifying its position in the industry.

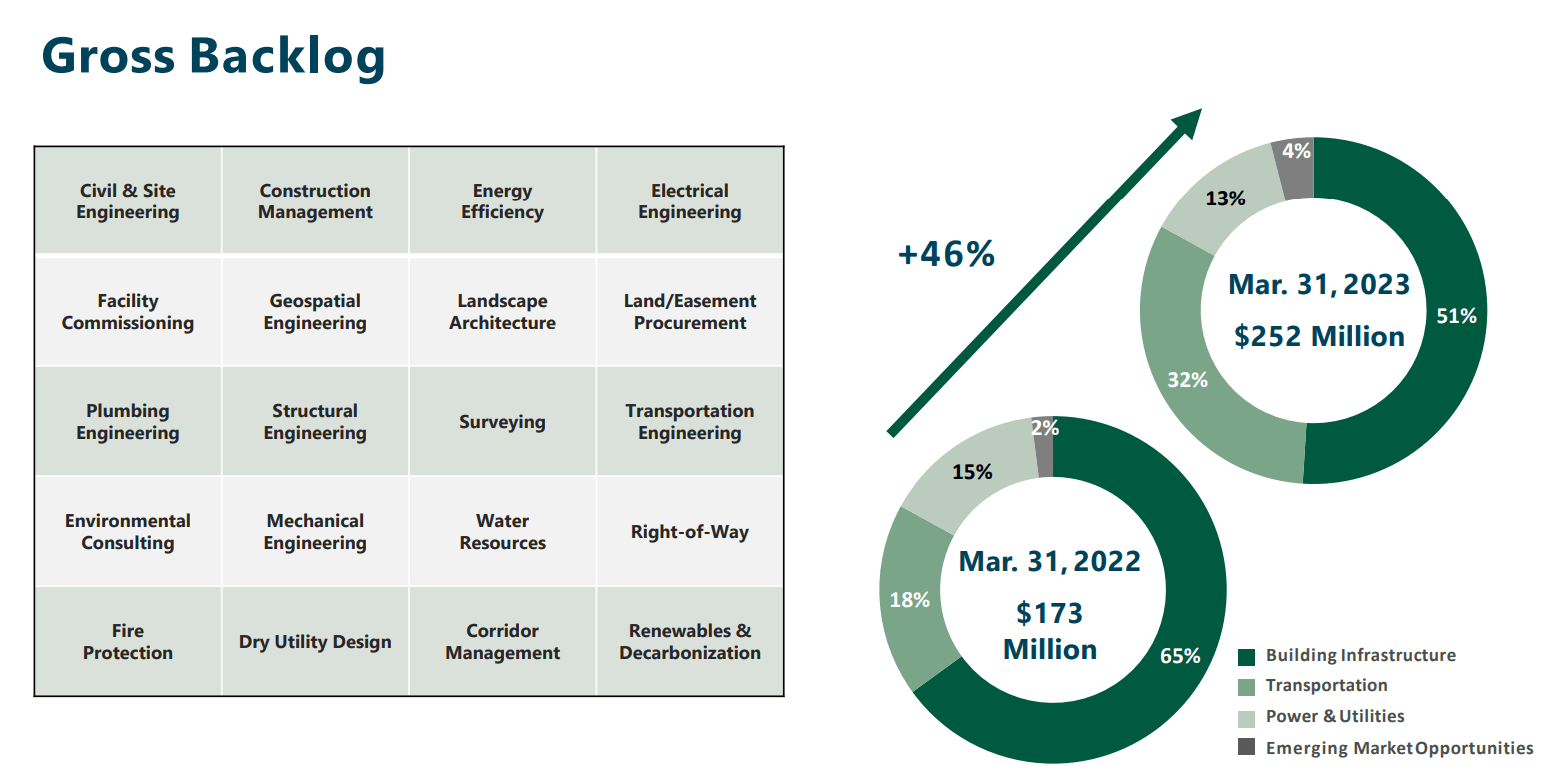

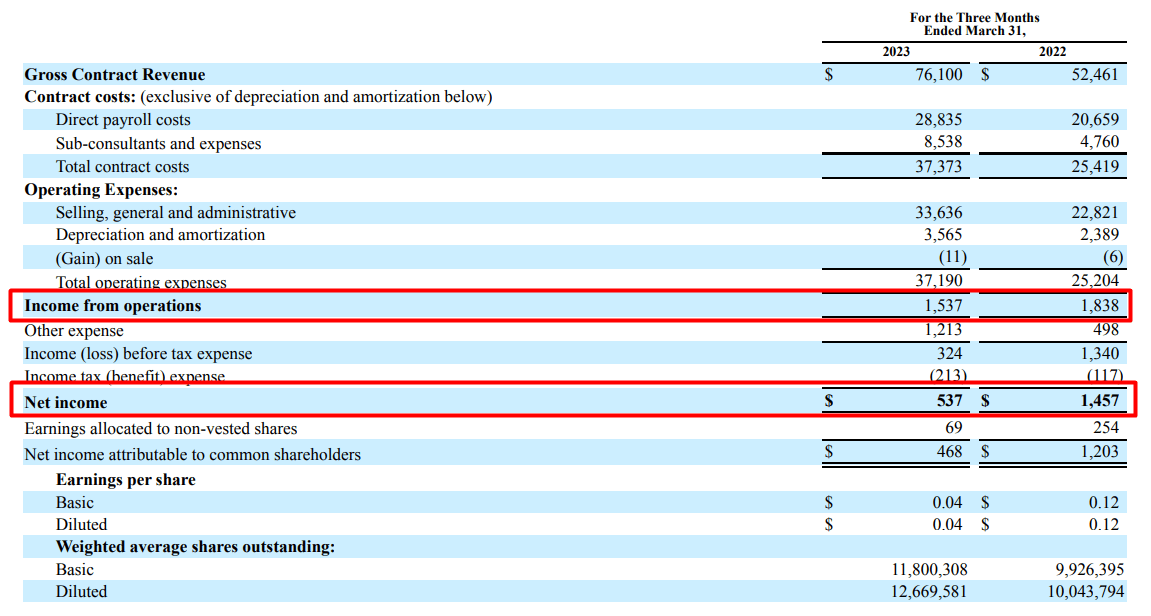

In Q1 FY2023 Bowman achieved a remarkable 45% YoY total revenue growth, amounting to $76.1 million compared to $52.5 million in the same period last year. This outstanding performance was driven by a combination of organic growth and successful acquisitions. The company's backlog, an indicator of future revenue, experienced a substantial increase of 46% YoY, reaching a robust level of $252 million [~56% of market cap]. This indicates strong demand for Bowman's engineering and professional services and positions them for continued growth in the coming quarters.

{kind=link}

Bowman's Q1 FY23 IR materials

The company's strategic focus on the transportation market proved fruitful, with significant contract awards from prestigious entities such as the Illinois Tollway Authority and IDOT, according to the words of the CEO during the latest earnings call . Bowman's revenue mix displayed a balanced portfolio, with building infrastructure representing 58% of total revenue. The remaining 42% consisted of floating infrastructure revenue, which grew by nearly 14% during Q1. Notably, Bowman's revenue from commercial projects accounted for just under half of the building infrastructure category, while approximately 40% was derived from residential activities. Furthermore, the company's revenue from homebuilding-related projects contributed ~30% of the building infrastructure revenue. The remaining portion [~12%], was related to municipal projects. I like this diversified revenue mix that speaks of BWMN's ability to capitalize on various sectors within the built environment.

Financially, Bowman achieved a gross profit increase of 43%, amounting to $38.7 million compared to $27 million in the previous year's Q1. The gross margin remained strong at 50.9% [-60 b.p. YoY] - the slight weakening was primarily due to the shift in the mix of work during the quarter.

However, it puzzles me that BWMN had a "slip" below gross profit:

{kind=link}

BWMN's 10-Q, author's notes

This was mainly due to M&A activities and the consolidation of new assets. Management said during the conference call that the company has managed to achieve positive operating leverage, with the growth rate of SG&A expected to be significantly lower than the sales growth rate. So this is a temporary difficulty rather than a new reality for BWMN.

Bowman maintains a strong financial position with a net debt of $30 million, representing a leverage ratio of 0.83x trailing adjusted EBITDA and 0.6x forward adjusted EBITDA at the midpoint of their guidance. They have a healthy cash position of $14 million, providing them with the flexibility to meet acquisition requirements. The company recorded a provision for uncertain tax positions related to the deductibility of research and development costs, reflecting responsible financial planning.

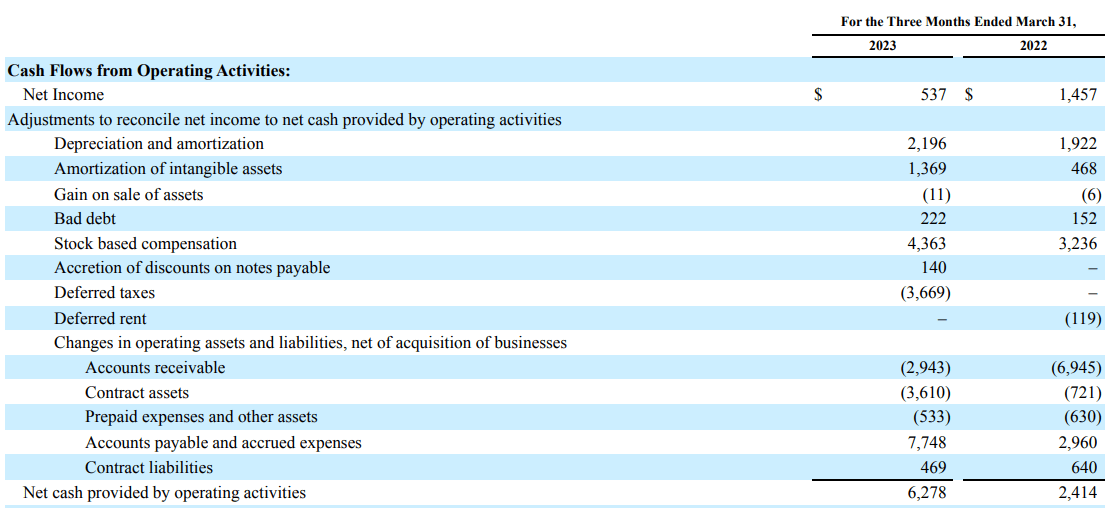

As we all know, cash is king. So it's worth taking a look at the cash flow statement to see the real ability of a business to generate what we buy assets for - free cash flow.

{kind=link}

BWMN's 10-Q

Net of CAPEX, BWMN increased its FCF to $5.7M [+159% YoY] in Q1 FY2023, and this strong growth is largely due to an increase in contract assets on the balance sheet. Demand for the company's services appears to be high in the market.

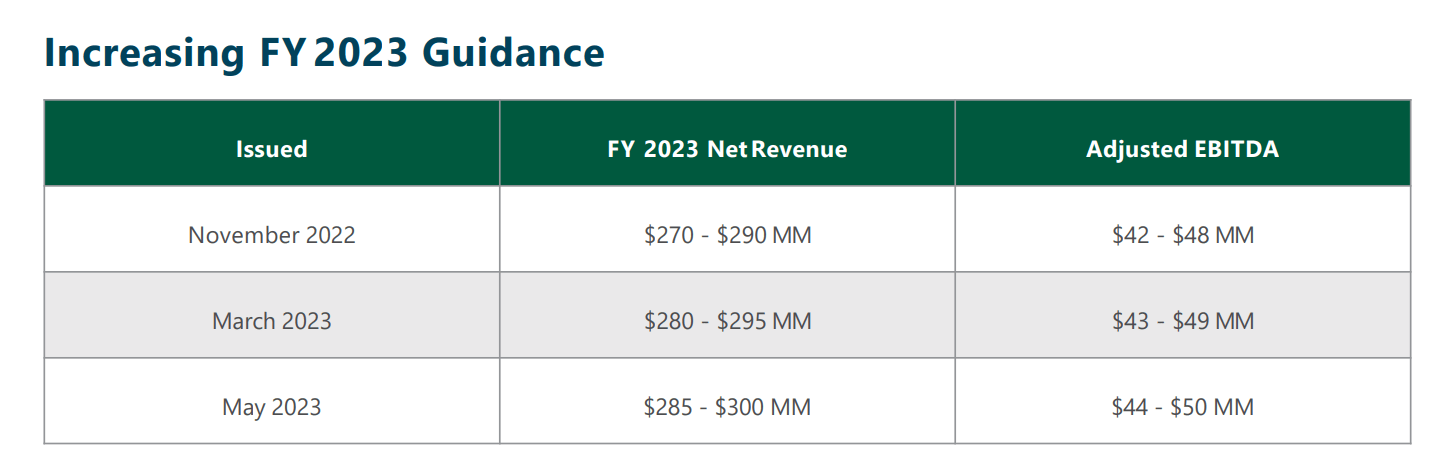

Looking ahead, Bowman is confident in its projected growth trajectory and increased its net service billing guidance for 2023. The revised range now stands at $285 million to $300 million, reflecting their optimistic outlook and recent acquisition activities.

{kind=link}

BWMN's IR materials

Valuation

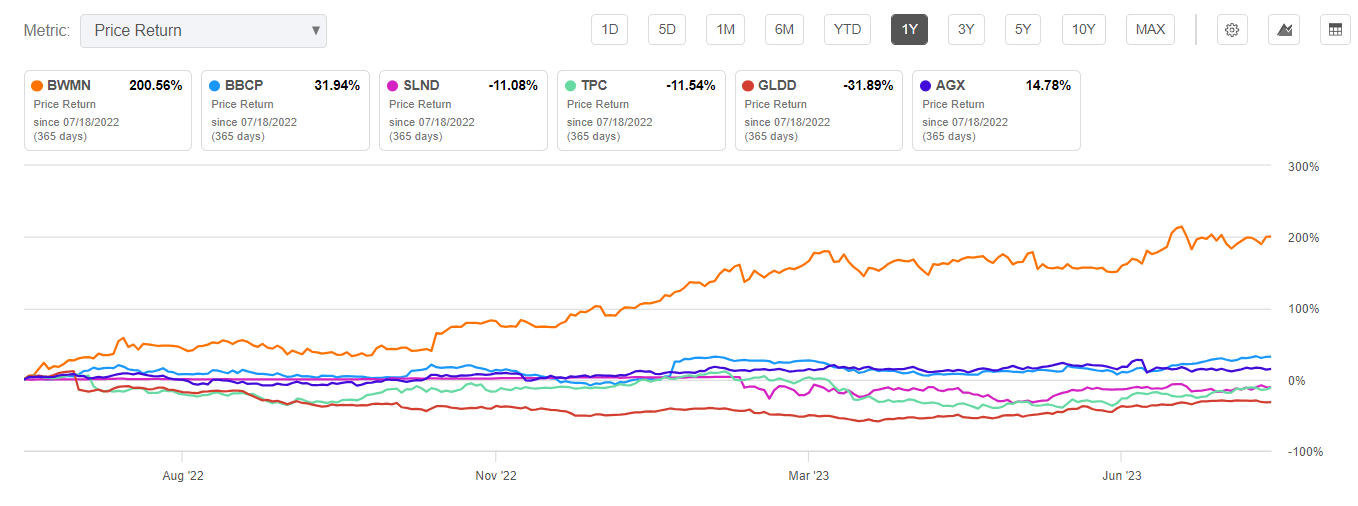

Apparently, the market is already quite aware of the prospects for the company's organic and inorganic expansion in the foreseeable future - which is why Bowman leads by a wide margin among comparable companies with relatively similar market capitalizations:

{kind=link}

Seeking Alpha

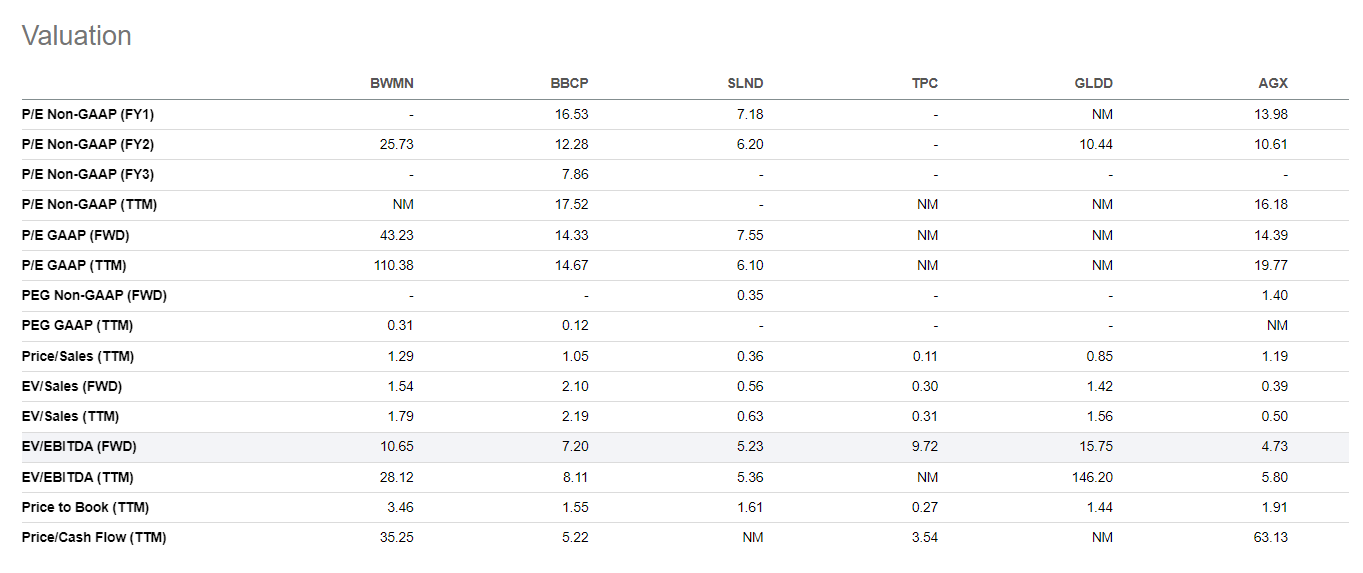

Unsurprisingly, the stock is the most expensive in absolute terms among the listed peers, trades at the largest premium to book value, and has a forwarding EV/EBITDA multiple of ~10.6x:

{kind=link}

Seeking Alpha

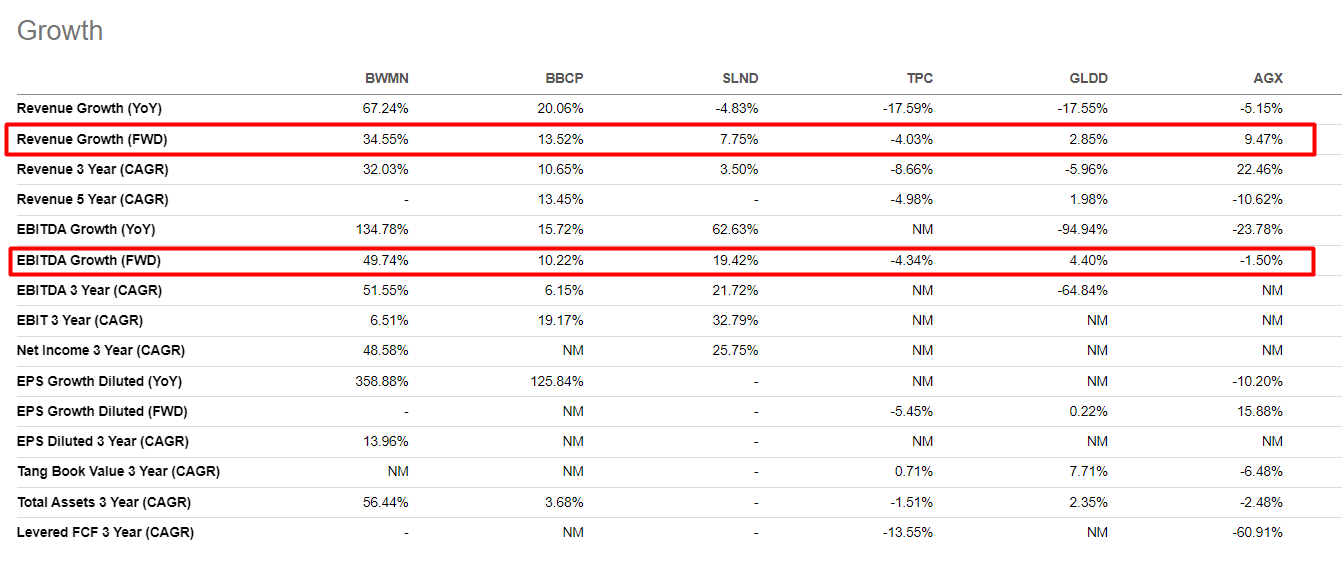

As a rule, such a high comparative premium should have an explanation - I find it in above-average growth rates:

{kind=link}

Seeking Alpha, author's notes

So far, BWMN has not been able to boast superiority in terms of margins - only its gross profit margin is significantly higher than the others. However, if we recall at this point that the company's EBIT has been relatively low due to presumably temporary difficulties, then it is possible that other margin metrics (below gross margin) will likely strengthen in the future. This assumption makes BWMN a rather interesting company.

Moreover, Wall Street analysts see another strong year for revenue growth in FY2024, as well as double-digit EPS growth. Also, for some reason, the pace of EPS lags behind revenue growth in their forecasts, which is a bit incomprehensible given plans to slow the growth of SG&A expenses.

In my opinion, a fair valuation of BWMN stock is 10 times FY2024 EV/EBITDA. The EBITDA figure for FY2024 should be $55.35 million, [+15.8% YoY] according to analysts.

Then, the company's enterprise value ((EV)) should be $555.3 million, which, adjusted for net debt of $66.3 million, should yield a value of $489 million. That's an upside of just 3.6% from today's share price.

The Bottom Line

By my calculation, BWMN has turned out to be fairly valued - I think that is the most likely conclusion.

First, the story of its future expansion is somewhat muted by the approaching real effect of the central bank's rate hike cycle, which has some lag. Second, while analysts' forecasts are very pessimistic, when we compare EPS implied momentum to revenue momentum, I still feel that the revenue forecast is a risk - the projected 76% year-over-year growth seems too large. Third, my valuation model was based on management's guidance and still could not show sufficient undervaluation for a Buy recommendation.

Therefore, I rate BWMN as Hold.

Thanks for reading!

For further details see:

Bowman Consulting: Great Company, But Already Fairly Valued