BWMN - Bowman Consulting Group: Best In The Industry With Strong Growth Prospects

2023-03-21 12:25:16 ET

Summary

- BWMN reported strong fourth-quarter results with 80% y-o-y revenue growth and adjusted EBITDA margin of 14.2% compared to 9.4% in the same quarter last year.

- The transportation solutions segment proved to be an outperformer for BWMN in Q4, reporting a remarkable 378% y-o-y revenue growth.

- The management has provided optimistic guidance for FY23, with net revenues and adjusted EBITDA estimated to be in the range of $280-$295 million, and $43-$49 million resp.

- I assign a buy rating for BWMN.

Investment Thesis

Bowman Consulting Group Ltd. ( BWMN ) is a development solutions provider headquartered in Reston, Virginia. In this thesis, I will be analyzing BWMN’s fourth-quarter results and its future growth prospects. BWMN has adopted an aggressive acquisition strategy to boost its growth which is successfully paying off in the form of significant revenue and income growth. I think it is one of the best prospects in the real estate and infrastructure consulting industry, and therefore I assign a buy rating for BWMN.

Company Overview

BWMN is a professional services firm providing a broad range of infrastructure, real estate, environmental planning, transportation, and energy solutions across the United States. The building infrastructure solutions segment is the main revenue contributor for the firm. This segment includes commercial, residential, and municipal infrastructure development planning, construction administration, supervision, and land permitting services. BWMN caters to the government as well as the public and private companies.

Investor Relations BWMN

Q4 FY2022 Results

BWMN recently reported fourth-quarter results with significant revenue and EBITDA growth. BWMN is on a solid growth track with multiple acquisitions to boost growth in the long term. The transportation solutions segment proved to be an outperformer for the company in Q4, reporting a remarkable 378% y-o-y revenue growth . In addition, the Q4 FY22 revenues and EPS beat the market expectation by 3.5% and 51.3%, respectively.

BWMN reported fourth quarter FY22 revenues of $75.6 million, a stellar 80% increase compared to $41.9 million in the same quarter last year. As per my analysis, the acquisition of eight firms during FY22, coupled with strong demand, contributed to this increase. Now let us further dive into the revenues. The building infrastructure segment contributed 58.6% of the total revenues at $44.3 million, up a solid 40.5% compared to $31.5 million in the same quarter last year. I believe the increased contracts for commercial infrastructure projects played an important role in this growth. The transportation solutions segment contributed 24.3% to the total revenues at $18.3 million, a massive increase of 378% from $3.8 million in the same quarter last year. The company expects transportation to be a key player for revenue growth in FY23 as well, given the strong and consistent demand experienced by the transportation solutions segment. The power and utilities segment reported revenues of $8.3 million, an increase of 68.6% compared to $4.9 million in the same quarter last year. Lastly, the emerging markets experienced y-o-y revenue growth of 186% at $4.5 million compared to $1.6 million in the same period the previous year. The gross margin for the quarter was reported at 52.1% compared to 50.7% in the same period the previous year. The operating expenses for the quarter were reported at $38.5 million, up 72% compared to $22.5 million in the same quarter last year. Though the increase in expenses is significant, I believe it is justified given the high inflationary environment and increased workforce to cater to the increased demand. Even with a significant increase in gross and operating expenses, the company managed to improve its gross and operating margins. BWMN reported an adjusted EBITDA margin of 14.2% compared to 9.4% in the same quarter last year. The net income for the quarter stood at $470 thousand, compared to a net loss of $600 thousand in the same quarter last year. The diluted EPS for the quarter stood at $0.03, up $0.10 compared to a loss per share of $0.07 in the corresponding quarter last year.

Overall, the fourth quarter results managed to outperform on multiple parameters. The solid revenue growth rate and improved profit margins were the highlights of the quarter. The management has given optimistic guidance for FY23, with net revenues estimated to be in the range of $280-$295 million . The FY23 adjusted EBITDA is estimated to be in the range of $43-$49 million, representing a 45% increase on the higher end compared to the FY22 adjusted EBITDA of $34 million. I believe that BWMN should be able to achieve these targets given the accumulated backlog of $243 million, an increase of 46% compared to $167 million in the same period last year. I think the smooth execution of this backlog will significantly boost the revenues for the company in the upcoming quarters.

Key Risk Factor

Dependency on third party sub-consultants: BWMN hires a significant number of third-party sub-consultants to execute parts of its contracts. Third-party consultants bring along a risk of performance uncertainty which could have a material impact on the company’s performance. Along with consultants, BWMN also hires third-party equipment manufacturers and suppliers for the execution of its contracts. However, they have managed this risk efficiently till now, but with the significant revenue growth and increased contracts, the firm should come up with an improved strategy with respect to dependency on third-party workers.

Quant Rating and Valuation

Seeking Alpha

Seeking Alpha has a Quant rating of strong buy for BWMN. This clearly reflects its upside potential. BWMN is ranked 1st out of 34 companies in the construction and engineering Industry and 2nd out of 656 companies in the Industrial sector. These rankings are representative of the company’s performance compared to its peers in the industry and its future growth prospects. I believe the Quants rating and rankings accurately represent BWMN’s current financial position. The Wall Street rating of strong buy for BWMN further solidifies my thesis.

{kind=link}

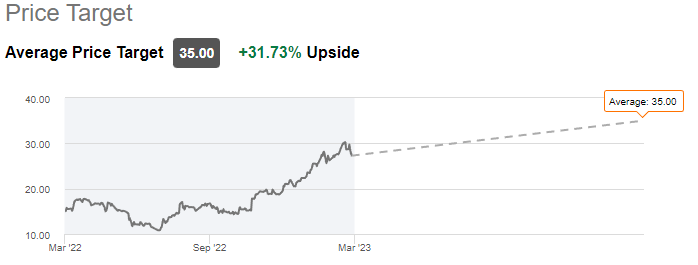

BWMN is trading at a share price of $26.5, a YTD increase of 33%. It has a market cap of $370 million. BWMN is trading at a twelve-month trailing PEG multiple of 0.07x, against the industry standard of 0.55x, with an annual EPS growth rate of 11.3 times from $0.03 in FY21 to $0.37 in FY22. This clearly shows that BWMN is undervalued compared to its peers with respect to its earnings growth rate. The Wall Street analysts have an average price target of $35 for BWMN, representing a 32% upside from current price levels. I believe it is a great investment opportunity for investors looking for growth companies at a cheap valuation.

Conclusion

BWMN is on a significant growth trajectory with solid revenue growth and improving profit margins. A substantial backlog of $243 million will prove imperative for future revenue growth. The aggressive acquisition strategy is helping BWMN is expanding its operations throughout the United States. BWMN is trading at a cheap valuation compared to industry standards. Considering all these factors, I assign a buy rating for BWMN.

For further details see:

Bowman Consulting Group: Best In The Industry With Strong Growth Prospects