BWMN - Bowman Consulting Group: Uncertain Tax Position

2023-12-27 10:58:49 ET

Summary

- Bowman Consulting Group Ltd. is a player in civil engineering and consulting services for infrastructure projects.

- The company has an uncertain tax position worth close to 10% of its market cap, and the need to pay higher taxes in the future will impact cash flow.

- Despite resilient revenues and growth in the megaprojects, we'd rather go elsewhere with our money given the already pretty full valuation.

Bowman Consulting Group Ltd. ( BWMN ) is a player in civil engineering, surveying and other general consulting services for getting mostly infrastructure projects off the ground. They are in the megaproject segment, which has been entirely resilient in the current economic environment, and the idiosyncratic and regional profile sees them likely growing without too much consideration needed for macro trends.

The problem is that Bowman has a current uncertain tax position worth close to 10% of the current market cap, and if they have to pay higher tax later, that will obviously impact their cash flows. In light of this, the valuation ends up not being particularly compelling, and there are headline risks.

Bowman's Business

There is still a lot of founder control in the business, with Gary Bowman running the company as CEO. They do civil engineering and other consulting services to help clients, which include infrastructure developers, governments and utility companies, complete projects. Surveying activities are a big part of their business, the geospatial revenues currently sitting at around 30% of revenues .

Other ways to split the revenues are in terms of customers. Building infrastructure is 55%, transportation is 21%, and power and utilities are 20%. Most of it is non-residential at 66%, and in general they are trying to develop residential revenues to diversify their income, so recent Fed Chair Jerome Powell comments are welcome.

These businesses have been resilient. Revenues are up around 30%, and infrastructure initiatives in the U.S. support their business with tailwinds in areas like battery production and energy. This megaproject resilience has been confirmed in some other parts of our coverage as well with Herc Holdings ( HRI ) claiming the development , including of backlog, remains very solid, which is corroborated here.

Taxes

The company spends quite a lot on R&D in order to develop resources and technology to conduct their civil engineering activities. This means they are running into the issues around the TCJA Trump cuts from some years ago, where R&D rules come into effect for the fiscal year 2022 and onward. This affects companies where R&D expense is growing. The rules, which are better detailed elsewhere , stipulate that there is less opportunity to expense R&D to reduce tax burden, and that US-domestic R&D needs to be capitalized over a period of 5 years. Effectively, 20% of the R&D expenditure can be deducted, since that would be the proportion coming in as amortization, and the rest will simply come out of cash flow with zero tax benefit in that year. Over time, if R&D doesn't grow in expenditure per year, it'll just result in expenditures offsetting the amortization, and the tax burden would be the same as in the pre-TCJA treatment.

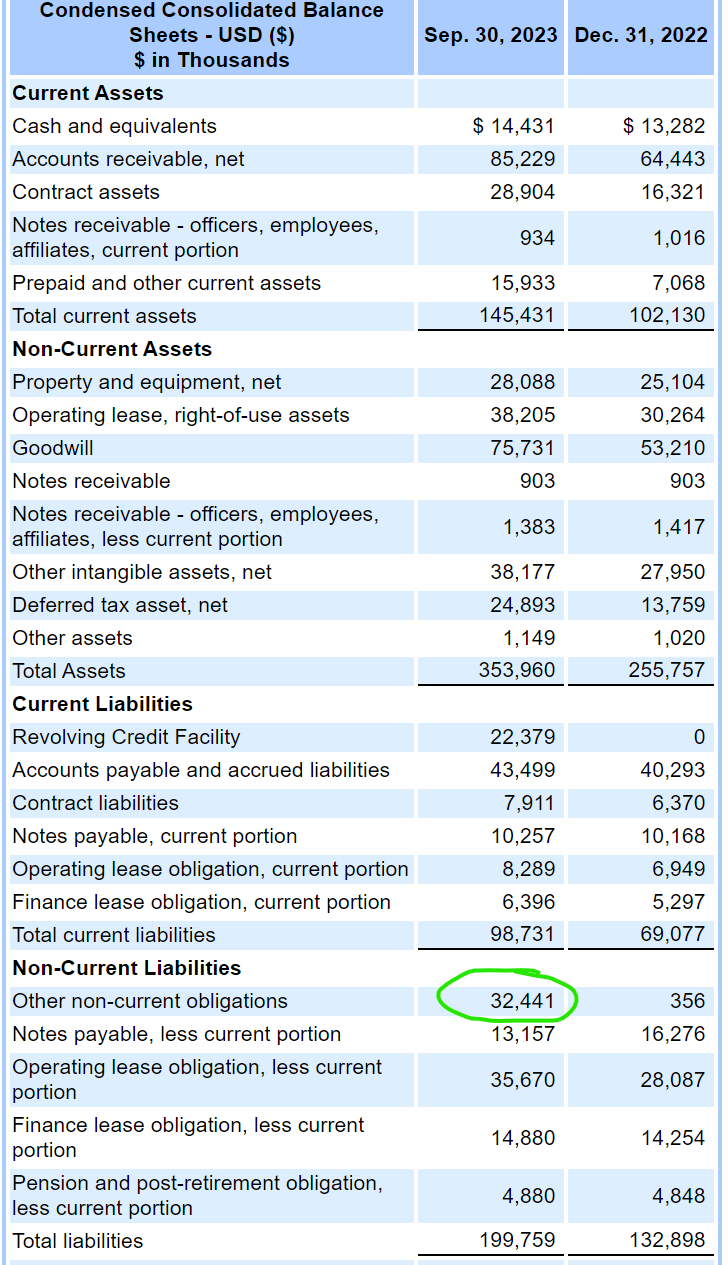

For 2022, the burden for Bowman was around $17 million, and as of now it's about $32 million found in non-current obligations, which is quite a lot on around $511 million market cap.

{kind=link}

The cash flow impact annually would be around $15 million per year if they scale at the current clip, assuming that they have to adopt this new methodology. For the income statement , it is accruing as an expense and would have no impact from current run-rates.

The uncertain tax liability is reflected on our statement of cash flows before changes in working capital as deferred tax as if it were spent, but it is later added back to cash from operations through accrued expenses since we are not actually expending the cash. This neutralizes its impact on cash from operations. On our balance sheet, the UTP is included in other noncurrent liabilities along with accruals for contingent consideration.

Bruce Labovitz, CFO of Bowman, Q3 Earnings Call .

Bottom Line

Current operating cash flows are around $16 million annualized, so the operating cash flow yields would suffer a lot if the new treatments come in and cause new outflows of $15 million. The OPCFY is around 2.3%, which isn't great. FCFY is obviously going to be negative as they continue to invest. While there is growth, it's going to less efficiently move into income as the quite high possibility of the new tax treatments. High interest costs have also hurt the income situation substantially.

EV/EBITDA is above 10x, which is a lot in this day and age. However, we do feel that they will continue to perform in their markets and generate top line growth. But with the claims on Bowman Consulting Group Ltd. being larger than screened figures, and a valuation like that, we think we would rather go places where things are more certain and valuations easier to benchmark.

For further details see:

Bowman Consulting Group: Uncertain Tax Position