BYD - Boyd Gaming Corporation: Leveraging A Digital Expansion

2023-10-22 04:02:31 ET

Summary

- Boyd Gaming's digital expansion taps into a burgeoning online casino market.

- Q3 earnings are expected to rise due to heightened summer vacation activity.

- Given its current undervaluation, Boyd stock presents a compelling investment opportunity.

Thesis

Boyd Gaming Corporation (BYD) is an American gaming and hospitality firm based in Paradise, Nevada. Over the last 6 months, BYD has seen a 9.60% decrease in its stock price, a trend that I see turning around as we enter the latter quarter of the year. Historically, casino gaming firms see disproportionate returns during the holiday season relative to the rest of the year. On October 24th, BYD will hold a conference call to review their Q3 results, which are likely promising as the summer months are a historically profitable period for casino firms. This will likely result in a short-term stock price bounce back.

Company Overview

The Boyd Gaming Corporation operates 27 casino entertainment properties in Nevada, Illinois, Indiana, Iowa, Kansas, Louisiana, Mississippi, Missouri, Ohio, and Pennsylvania. These diverse formats include brick-and-mortar, dockside riverboats, racinos, and barge-based casinos. The firm offers 1,723,126 square feet of casino space, 29,836 slot machines, 626 table games, and 10,751 hotel rooms. 80% of their revenue comprises their gaming operations, with the remaining 20% consisting of food & drink, room revenues, and “other” revenues. Boyd also has two primary subsidiaries: Boyd Interactive Gaming and the recently acquired Pala Interactive. Additionally, in 2018, the company partnered with online sports betting firm FanDuel, adding to their market opportunity in the digital sphere.

Brand Name

Despite the profitability of the casino industry, the barriers to entry are incredibly high due to federal regulation. Having an established presence in the casino industry and demonstrably profitable physical locations is an often underrated facet of BYD’s competitive advantage. Due to their expansion strategy primarily including acquisitions, Boyd can selectively choose locations performing strongly and bolster them with their integration strategies and brand name. This phenomenon can be seen across the board, specifically in the 2016 Aliante Casino merger. Independently, this firm brought in around 17 million dollars in revenue in 2016. After their acquisition by BYD, this number has jumped to 84 million dollars this year. Overall, Boyd’s brand has reflected positively in growing its revenue YoY. With the widespread success of similar firms such as DraftKings, Boyd looks to continue to acquire and integrate their way to a dominant market share in the casino business, both in person and online. I see this impacting BYD’s growth rate to a relatively large extent. When paired with their existing FanDuel partnership, the company will be a safer investment for those looking to buy into the casino gaming industry.

Statista

Firm Acquisition and Digital Expansion

BYD’s primary growth catalyst over the long term will be its expansion into the digital casino gaming space. Other purely online firms like DraftKings have seen enormous valuations and growth over the past year. With the acquisition of Pala, Boyd can hit the ground running and begin cornering a more significant portion of the market without being plagued by the onus of startup costs and issues brought on by inexperienced management. The digital gambling and casino market as a whole is expected to grow substantially over the next eight years, with projected growth from 61.5 billion dollars in 2021 to 114.4 billion dollars by 2028 . I see BYD's entrance into this market as the true driver of their future ticker growth simply because of its novelty. In terms of the firm's existing brick-and-mortar locations, it can be expected that revenues will, at worst, stay consistent, barring a one-off global event that limits in-person visitorship. This means that any substantial growth will come via acquiring more in-person locations or, more crucially, the growth of their digital sector.

The most significant takeaway from BYD's Q2 10-Q should be the “online” account under revenues almost doubling over the past 6 months. As previously discussed, BYD’s ability to hedge shoddier in-person numbers is clearly displayed, with gaming revenue decreasing from 684 million dollars to 660 million dollars, but overall revenue still increasing. Specifically, online revenue has jumped to 207 million dollars in 2023 from 111 million dollars in 2022.

GrandViewResearch

Industry Cyclicality

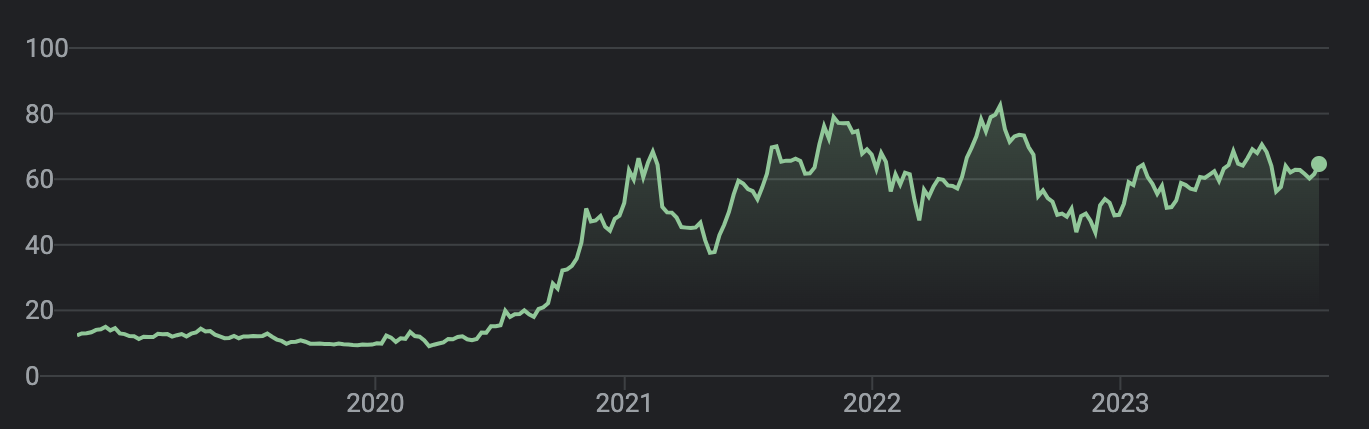

Boyd’s 2023 Q2 10-Q shows quarterly revenue increased from $894,450,000 in 2022 to $916,950,000 in 2023. While these numbers are essential in understanding BYD’s current state and potential for growth, they are not entirely applicable to performance over the next 6 months. By virtue, the casino gaming industry is cyclical, mainly in parallel with vacation periods, meaning that the upcoming Q3 results will be better understood when juxtaposed with 2022’s Q3. This also means that until the relevant position of the firm is disclosed, the current market will not be accurate and will update immediately when the 2023 Q3 earning report is divulged to the public. I think this makes the next few weeks an optimal investment period for a potentially sharp gain on October 24th, the date for the earnings disclosure. Below, the gains seen during the summer months and the drops during the latter part of the year highlight BYD’s performance in parallel with typical “vacation periods.”

{kind=link}

Valuation - BYD

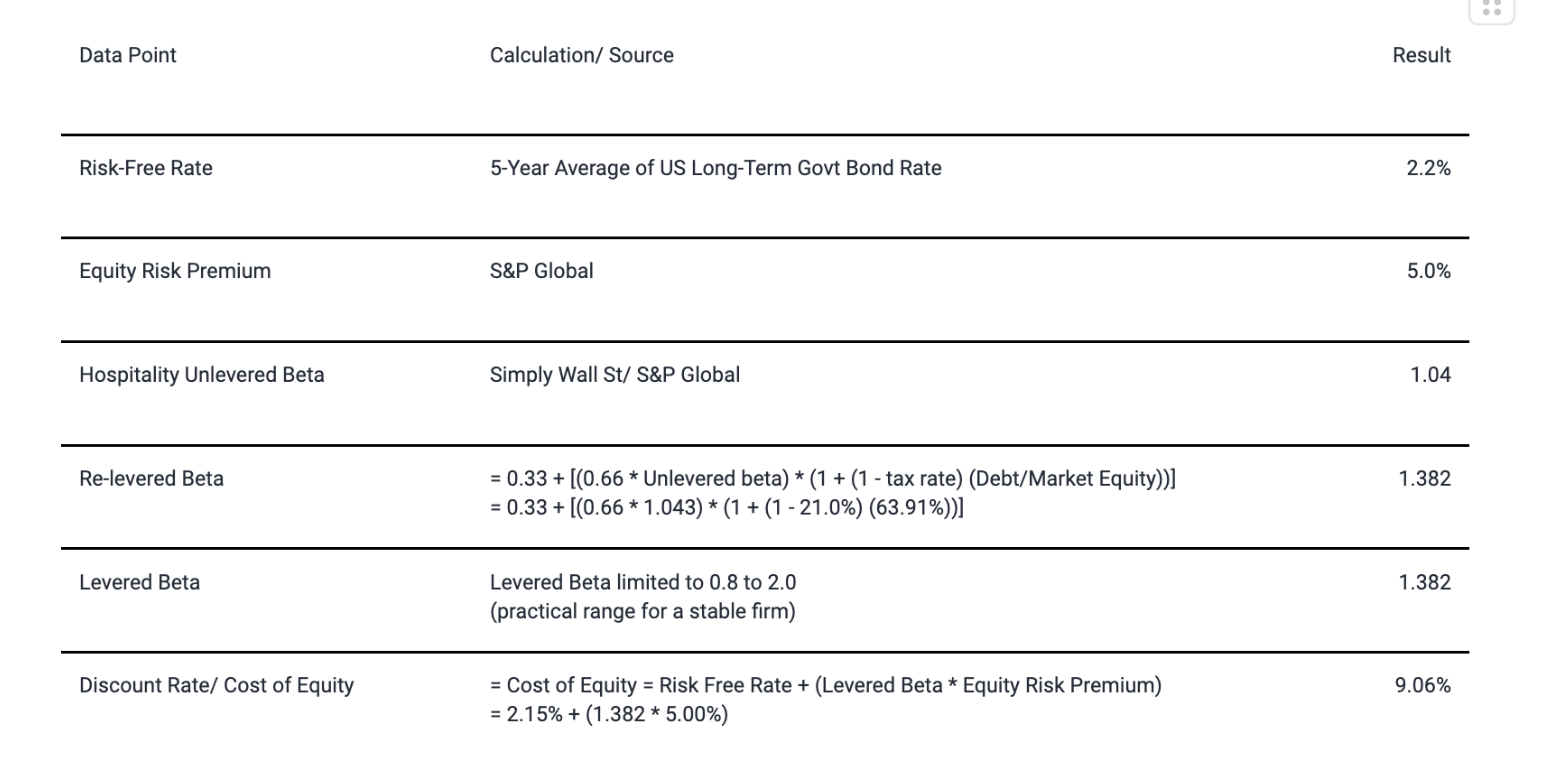

As seen in the DCF below, despite moderately conservative estimates on discount, terminal growth, and projected growth rates, BYD is undervalued by around 74%. I see Boyd reaching its intrinsic value as ambitious but possible. The inherent uptick in user traffic during the holiday season should provide a baseline boost, which, coupled with steady growth over the past year, could push BYD to the mid-60s at the least. Figures for revenue, net income, and free cash flow were acquired from BYD’s 10-q. Growth rate, terminal growth rate, and discount rate were sourced from Simply Wall Street estimates . Their discount rate calculation is as seen below, and their perpetual growth rate is equal to the 5-Year Average of US Long-Term Govt Bond Rate, providing a fairly accurate assessment of Boyd’s cash flows over the next few years. Their current growth rate is the average of up to 5 public analyst estimates from S&P Global.

Google Sheets

{kind=link}

Risk

The primary source of risk that investors face when holding or purchasing BYD stock is its highly leveraged position. This concern would only be realized in a worst-case scenario where BYD is forced into default on its outstanding debt. This could occur via the disclosure of a covenant-breaking action, such as fraud, an inability to refinance before an upcoming maturity wall, or an inability to fulfill an interest payment on an existing debt. The firm's debt is a point of risk for investors should a one-off event similar to COVID occur. BYD is highly leveraged and not very solvent, providing a 2.10 debt-to-equity ratio . Parallel to this, BYD’s current ratio of 0.84 is not reassuring as it indicates a lack of capital to pay down any immediate debt. If something were to make Boyd’s in-person locations unprofitable, the risk of defaulting on a debt interest payment would skyrocket. With over 3 billion dollars in debt, solvency should be a concern for potential investors.

Conclusion

BYD is in a somewhat uncertain place, with an upcoming earnings call being a significant factor in its stock price. This uncertainty, however, stemming from the cyclical nature of the casino industry, has created a unique opportunity for investors to take advantage of a sharp potential increase in the firm’s stock price. Many of BYD's businesses are effectively stable with a strong brand name and consistently profitable physical locations. Beyond this, however, BYD has worked to acquire a digital casino firm that will streamline Boyd’s entrance into the digital gambling space. With these factors in mind, I see investors profiting relatively short term (next 1 month) as the most recent quarterly earnings are published and the next 6 months during the December holiday season if stock purchases are made soon.

For further details see:

Boyd Gaming Corporation: Leveraging A Digital Expansion