BRAG - Bragg Gaming: An Operating Leverage Opportunity

2024-01-17 08:13:26 ET

Summary

- Bragg is growing in the online gaming industry through new content releases and deals with customers globally.

- The company operates at around breakeven, but further growth could surface value with operating leverage as Bragg's operating model doesn't seem to require too much marginal SG&A.

- The valuation only prices in modest growth and margin expansion below my expectations, making the valuation seem like a good risk-to-reward.

Bragg Gaming Group (BRAG) operates in the online gaming industry. The company offers B2B iGaming technologies in the United States, Europe, and globally. The offering includes player account management ((PAM)), turnkey solutions for gaming providers, third party gaming content, as well as proprietary casino content.

Bragg Q3 Investor Presentation

The company is expanding its game offering - in 2023 as of Q3, Bragg's plans included 68 new content titles, with 30 of them being Bragg Studios' creations. The new content releases, and acquisitions in the industry, have created the foundation for Bragg's revenue growth so far. The third party content is overall representing a growing part of Bragg's business, with proprietary content also increasing in share at the cost of PAM & Turnkey solutions' revenue share.

Bragg Q3 Investor Presentation

{kind=link}

The stock jumped significantly in July, and the stock has maintained the higher level. The stock could still have room higher as Bragg is growing its operations with a potential undervaluation. The stock is also only at a fraction of its 2021 peak price.

One Year Stock Chart (Seeking Alpha)

{kind=link}

Growth in a Growing Market

Online gaming as a whole is an interesting industry, especially in the United States - especially the online gambling industry is growing rapidly with legalization. Many of Bragg's customers in the United States are growing rapidly, as for example DraftKings' revenues grew by 72.9% in 2022, the FanDuel brand's owner's, Flutter Entertainment's , revenues increased by 13.9% in USD. In-person casino operator BetMGM's revenues also increased by 38.4% as the Covid pandemic started to subside.

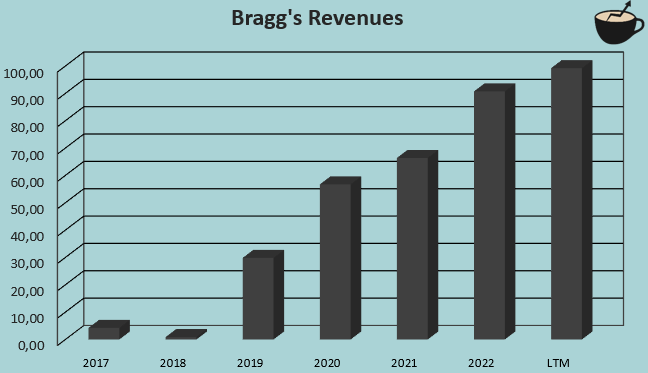

Bragg has been able to scale revenues from near zero in 2018 into a current trailing amount of $99.2 million . In Q3, revenues increased by 8.0% year-over-year, and Bragg's customers' wagering increased by 24.6%. Bragg's product mix is constantly evolving, and the significance of PAM & Turnkey solutions is diminishing - in Q3/2022, the segment represented 30.1% of revenues, but in Q3 of 2023 the share was only 20.6%. The shrinking revenues have been more than offset by the content segment's revenues, and as PAM & Turnkey constantly represent a smaller share of revenues, the underlying growth in the content segment should start to show increasingly. Bragg still plans to grow the PAM & Turnkey segment as well, but as the growth has been lacking in several quarters, I would need demonstration of a better performance to believe in the segment's growth.

The company's contract changes and product mix have resulted in a lower ratio between revenues and customers' total wagers, as the revenue growth of 8.0% significantly trails the wagering growth of 24.6%. The trend seems a bit worrying; Bragg needs to stabilize the share of wagering that the company gets as revenues to sustainably grow revenues very well. As the underlying wagering had a good growth, such a scenario could fuel a very good amount of growth for Bragg, but further decreases could be detrimental both to growth and margins.

Author's Calculation Using Seeking Alpha Data

{kind=link}

The growth is also partly due to Bragg's acquisition of Spin Games. In Q2/2022, Bragg completed the acquisition of Spin Games for a consideration of around $30 million, fueling Bragg's proprietary and third-party content revenues. The acquisition has so far seemed great operationally as revenues in the content segment are constantly growing.

Significant Potential for Margin Expansion

Bragg has potential to scale earnings very well with revenue growth. The company currently operates near breakeven on an EBIT level. The company has a current trailing gross margin of 54.2% and plans to leverage the gross margin to 60% by 2025, making achieved growth highly valuable. As a technology provider Bragg's needs for SG&A should be quite limited with revenue growth, making significant operating leverage possible.

The gross margin expansion is meant to be achieved from a growing share of Proprietary content revenues and PAM & Turnkey solution revenues. So far, the share of Proprietary content has performed well with constant increases, but the PAM & Turnkey segment has performed poorly for several quarters - until the segment starts increasing in revenues again, I wouldn't expect the 60% gross margin to be achieved in 2025. Gross margins have quite consistently increased from 43.5% in 2020, but at a slower pace than needed for the 60% target. Even if the gross margin target isn't achieved, though, the profitability improvement should be significant. Bragg is able to consistently improve revenues providing operating leverage, and the company's cash flow conversion is good due to a relatively low amount of investments and quite high depreciation & amortization.

Revenues Could Scale Valuation

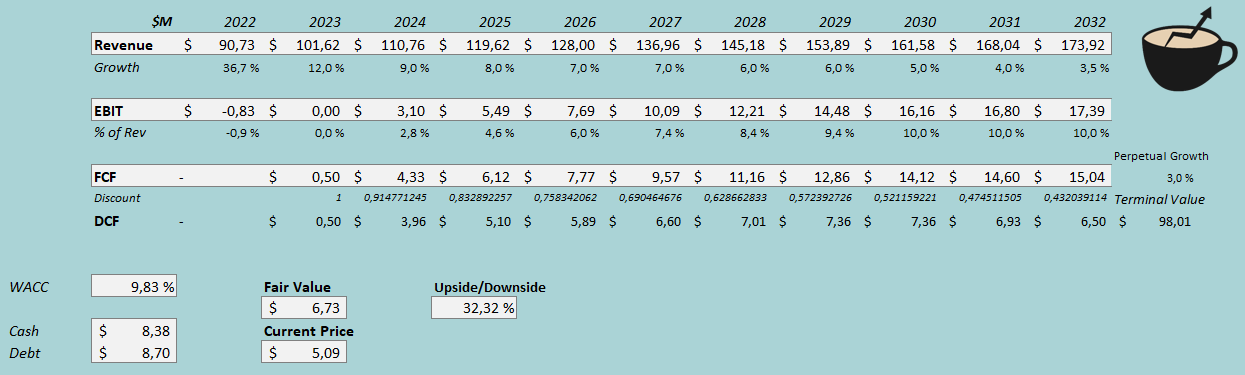

The fair value of the stock is largely a result of Bragg's future growth rate, as profitability is largely a result of further growth. To demonstrate the valuation and to estimate a rough fair value for the stock with my baseline expectations, I constructed a discounted cash flow model in my usual manner.

In the DCF model, I estimate the growth to stay similar and to scale down slowly. For 2024, I estimate a revenue growth of 9%. Afterwards, I estimate the growth to slow down in steps into a perpetual growth of 3%, representing a CAGR of 6.7% from 2022 to 2032. With the growth, I estimate Bragg's EBIT margin to slowly rise to 10.0% with operating leverage and slightly higher gross margins. As told, the company has a good cash flow conversion which is factored into the DCF model.

With the mentioned estimates along with a cost of capital of 9.83%, the DCF model estimates Bragg's fair value at $6.73, around 32% above the stock price at the time of writing. The fair value is very volatile and correlates highly with the future revenue growth, though - with growth that comes in below my expectations, the stock could still be fairly valued or even overvalued. With my baseline scenario, though, the stock has upside, and could have even more upside with faster growth.

DCF Model (Author's Calculation)

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

With Bragg's current amount in interest-bearing debt and interest expenses in Q3, the company's interest rate comes up to 24.37% - it seems that the interest also covers other debts that don't typically bear significant interest. Still, as interest expenses have to be paid, I use the extremely high estimate in the CAPM. Bragg's balance sheet isn't very leveraged, though, and I estimate a long-term debt-to-equity ratio of 10%. For the risk-free rate on the cost of equity side, I use the United States' 10-year bond yield of 3.95% . The equity risk premium of 4.60 % is Professor Aswath Damodaran's latest estimate for the United States, made on the 5th of January. Yahoo Finance estimates Bragg's beta at a figure of 0.66 . Finally, I add a small liquidity premium of 0.5% and an ESG addon of 1.5%, crafting a cost of equity of 8.99% and a WACC of 9.83%.

Intriguing Management & Owner Moves

In recent years and months, Bragg's management has seen a very significant amount of turnover. After already significant turnover, Bragg changed its CEO in August into Matevž Mazij, Bragg's largest shareholder and the founder of Onyx Gaming, which was acquired by Bragg in 2018. More recently in November, the resignation of Lara Falzon, president and COO of Bragg, was announced . The turnover leaves investors wondering about Bragg's future, and potential strategic outcomes - recently in November, a letter was sent to CEO Matevž Mazij suggesting a sale of the business to create shareholder value, as Raper Capital's Jeremy Raper argues the stock to be significantly undervalued on the stock market.

Takeaway

Bragg seems to be a potential opportunity for investors. The company is growing its revenues in a stable manner, making margin leverage from the current EBIT breakeven likely in my opinion. The stock has significant underlying value if executed on properly, and with quite modest financial expectations, the stock already has quite a good amount of upside. Bragg does still have quite a high risk profile due to currently poor earnings making growth critical, but the risk-to-reward seems favorable. For the time being, I have a buy rating for the stock.

For further details see:

Bragg Gaming: An Operating Leverage Opportunity