BCLI - BrainStorm: Upcoming AdCom Meeting For NurOwn For ALS Could Be Start Of Major Turnaround

2023-03-30 09:16:18 ET

Summary

- BrainStorm just announced that it has secured an FDA advisory committee vote for treatment candidate NurOwn for the treatment of ALS.

- NurOwn’s results on biomarker NfL have actually been remarkable good, outperforming Biogen’s/Ionis’ Tofersen which has its PDUFA date on April 25, 2023.

- As BrainStorm has amended its biologic license application using the file-over-protest route, a possible PDUFA date may come sooner than expected.

- BrainStorm’s stock has known two major sell-off events the past years, which may create an opportunity, even though its cash position is low.

Thesis

I have covered Brainstorm Cell Therapeutics’ (BCLI) in August 2022 with a buy rating, after the company had announced in mid-2022 it would file a BLA for NurOwn for ALS. The company’s stock has sold off more than 60% since that coverage, in light of a refusal-to-file letter which BrainStorm had received in November 2022. That letter from the FDA led investors to believe that there were little chances that BrainStorm’s drug candidate NurOwn would be approved for amyotrophic lateral sclerosis or ALS, a devastating disease that rapidly affects motor neurons and function. It left the stock trading around less than $60 million. Currently it is trading around $90 million after a strong move upwards in light of the recent news.

BrainStorm subsequently requested a Type A meeting with the FDA, which was secured and scheduled to occur in January 2023. Though investors had hoped to receive any news from the company thereafter, the market has been left in the dark, and the stock sold off further.

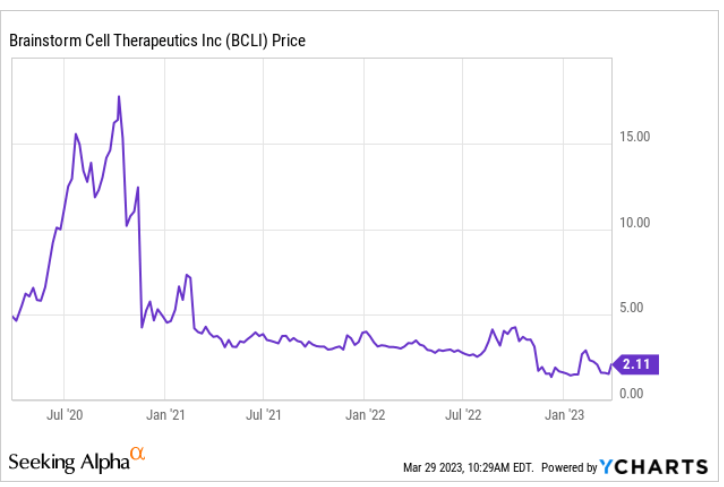

BrainStorm announced on March 27, 2023 that subsequently to its type A meeting with the FDA, it has been able to secure a meeting from the FDA’s advisory committee to discuss the Biologics License Application or BLA for NurOwn for the treatment of ALS. The pathway used allowed BrainStorm to adapt its BLA without suffering delays, allowing an AdCom meeting in days or weeks according to management, and a PDUFA date possibly soon after. The stock has been moving up since that announcement. This is the three-year stock chart which also shows the 2020-related sell-off.

{kind=link}

Three-year stock chart (Ycharts)

In case of approval, peak market sales potential of $600 million or perhaps higher should be possible, making this a company with multi-bagger potential at this point.

Very recently, on March 22, 2023, the FDA’s AdCom has convened to discuss Biogen’s Tofersen for ALS in patients with a rare SOD1-mutation. That meeting has been widely reported on in the scientific community, mostly because the AdCom voted in favor or using a biomarker that may be predictive of clinical benefit, and hence could be used as a surrogate endpoint allowing conditional approval. It concerns the biomarker Neurofilament Light or NfL. The Tofersen AdCom vote was unanimously – 9 to 0 – in favor of using NfL as a surrogate endpoint marker, and though the FDA does not need to follow it’s AdCom’s advice, it has historically done so in about 80% of cases.

NurOwn outperforms Tofersen on its NfL readout, in the entire ALS patients population, and that biomarker readout is confirmed by numerous other biomarkers of neuroprotection, neurodegeneration and neuroinflammation.

In light of all of this, I believe the company’s recent press release could see the stock reverse, and in case of further promising news or success, the stock may see a quite considerable upside.

Company

Introduction

As the present article intends to follow-up on my initial coverage , discussing the developments of the past eight months and its possibly exciting near future, I invite readers to study my initial coverage.

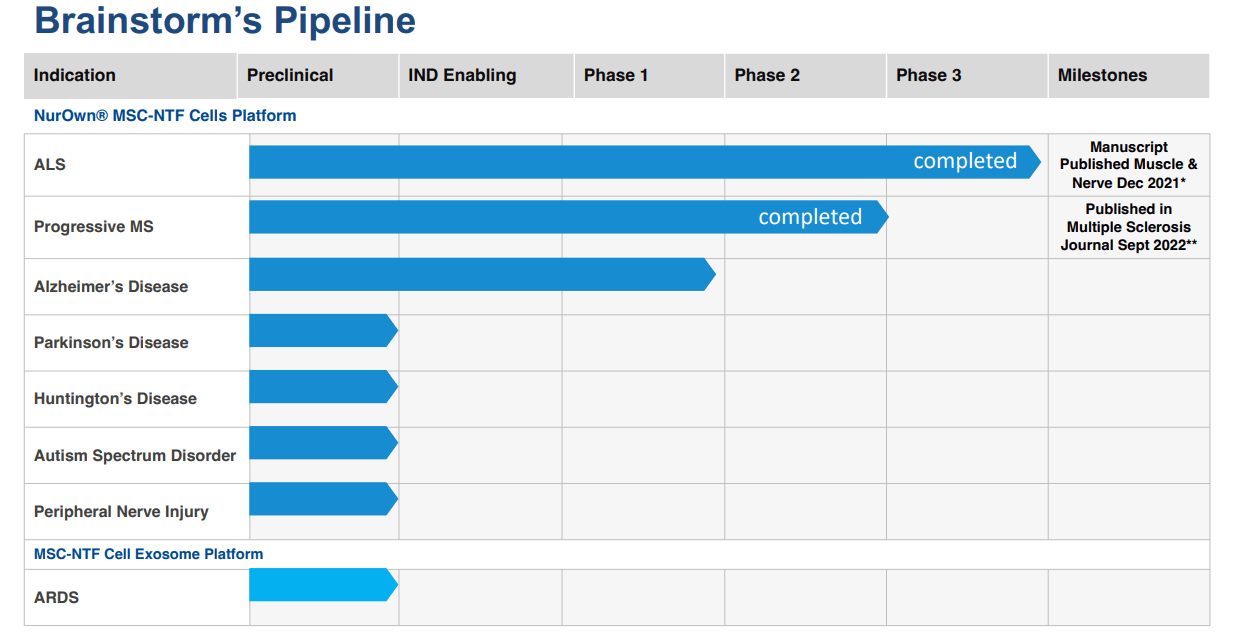

BrainStorm has a broad pipeline with two developments for ALS and multiple sclerosis or MS sticking out, as they have respectively passed a Phase 3 and Phase 2 trial.

{kind=link}

BrainStorm's pipeline (Biotech Showcase presentation)

The focus is currently mainly on NurOwn for ALS, a devastating disorder that destroys motor neurons over time, leads to death on average in 2 to 5 years’ time , and which affects over 31,000 cases in the US alone. Some may know ALS for the ice bucket challenge that got worldwide attention some years ago, or because scientist Stephen Hawking was diagnosed with it – and was one of the rare cases having lived with the disease for more than 50 years after diagnosis. Familial ALS accounts for 5-10% of all cases. The other 90% of all cases is not related to a known family history or presence of a genetic mutation.

NurOwn’s history for ALS

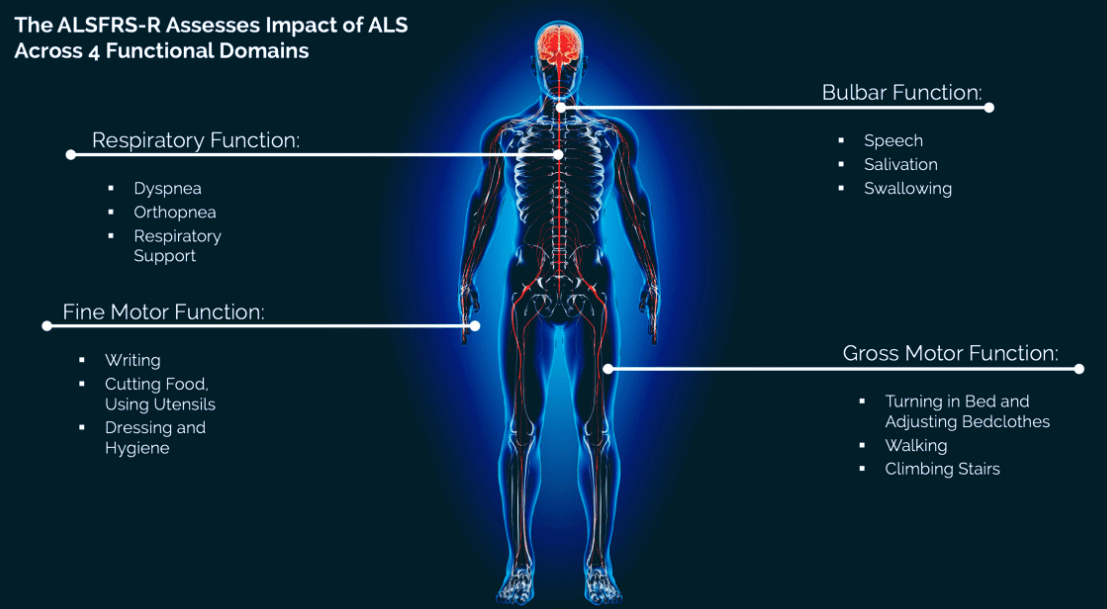

NurOwn is the company’s autologous treatment candidate harvesting stem cells from a patient’s bone marrow, isolating and multiplying them in a lab, and reinjecting them into the patient’s cerebrospinal fluid. The therapy aims to reduce neuroinflammation and to modify glial activity. It has passed Phase 1, Phase 2 and Phase 3 trials, the latest having ended in 2020. The standard primary endpoint here is the ALSFRS-R scale, measuring motor function of different parts of the body. The difficulty here is that several of the standard measuring scales in neurodegenerative diseases have floor effects, which may be of particular importance in a fast-progressing disease like ALS.

{kind=link}

ALSFRS-R scale (Corporate website)

The Phase 3 trial’s initial results in 200 patients as announced in November 2020 showed no statistical significance on the primary endpoint, and led to a cliff-like sell-off , the likes of which the company re-experienced in November 2022 – this time falling off a much lower market cap - when it received a refusal-to-file letter from the FDA.

In August 2022, BrainStorm announced that a correction had been made to the publication describing the Phase 3 results, which showed a statistically significant treatment difference of more than 2 points for the average change from baseline in ALSFRS-R, in the pre-specified subgroup of patients with a baseline score of at least 35.

On March 27, 2023, the company announced that it has been able to secure an FDA Advisory Committee Meeting to discuss the company's Biologics License Application for NurOwn for ALS. Apparently, the FDA provided BrainStorm with multiple paths to such AdCom, and BrainStorm chose the one that could lead to approval fastest, namely the File-Over-Protest procedure, allowing the company to amend its BLA to respond to most of the outstanding questions the FDA had.

Three Bearish Facts To Be Taken Into Consideration

I see three main arguments that should caution investors considering an investment here.

i) The consistent failure of BrainStorm so far

BrainStorm has failed so far with NurOwn because the drug failed to reach its primary endpoint with statistical significance in a Phase 3 trial. One could argue that therefore, BrainStorm is likely to fail again.

In that framework, set aside the NfL vote which I will discuss below, the FDA’s AdCom considered on March 22, 2023 that the data from Biogen’s placebo-controlled Phase 3 trial and extension study along with the biomarker data did not provide convincing evidence of the benefits of Tofersen, with a vote of 5-3 with one abstention. Tofersen’s Phase 3 trial had missed its primary and secondary endpoints, similar to NurOwn’s having missed its Phase 3 trial’s primary endpoint.

ii) FDA has already in 2021 taken a stance regarding NurOwn

In March 2021, the FDA had even put down in writing that NurOwn did not show clinical benefit. The FDA has presumably provided a written statement to inform the powerfully-voiced ALS community supporting the drug candidate. As the FDA took the liberty of taking its considerations public, a rare thing for the governmental institution to do, One could argue that in light of that, a reversal of FDA’s view is unlikely.

iii) BrainStorm is low on cash

BrainStorm has reported earnings for the last quarter on March 30, 2023, mentioning that as of December 31, 2022, it had cash and cash equivalents of $3 million compared to $22 million the year before. BrainStorm does have an at-the-market facility, but using that - if BrainStorm hasn't already - would dilute shareholders and may put pressure on its share price.

Eight Bullish Developments To Be Taken Into Consideration

I now outline eight bullish developments that I believe may considerably raise the stakes of seeing a conditional/accelerated approval of NurOwn for ALS soon.

i) The FDA could have explained its refusal at the Type A meeting

If the FDA had been of the position that NurOwn’s chances to ever become available as a therapy for ALS were inexistent, the FDA could have chosen to explain its reasoning for refusing to file the BLA to BrainStorm. The Type A meeting that took place on January 11, 2023 would have been the ideal moment to do so. Instead, the FDA apparently gave BrainStorm the opportunity to amend or refile a BLA, which could indicate the remarks the FDA had were addressable.

ii) There was no need to allow an AdCom meeting

Without any necessity to do so, the FDA allowed BrainStorm to have an AdCom meeting. An AdCom meeting may give guidance to the FDA, and the FDA has in the past followed that guidance about 80% of the time. Though an AdCom meeting is a rare and exceptional event for most diseases, in neurodegenerative diseases it seems to be more commonplace. There have been AdCom meetings for Biogen’s Aduhelm, Biogen’s/Eisai’s (ESALF) Leqembi, Amylyx’s Relyvrio and recently Biogen’s/Ionis’ Tofersen. All of the documents that are published ahead of or after such an AdCom meeting reveal good insights into the FDA’s current thinking on the matter of neurodegenerative diseases.

iii) BrainStorm provided compelling new data since 2020

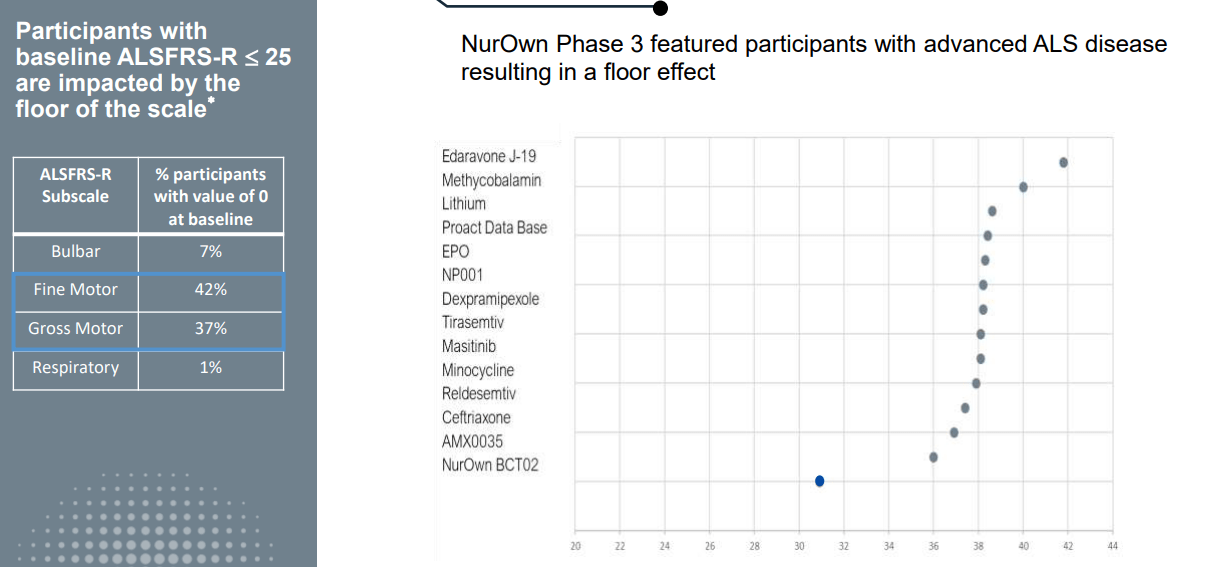

BrainStorm has shown that the lack of statistical significance may have been related to floor effects of the ALSFRS-R scale in several patients, which it estimated at about 23% of all trial participants. The floor effect could lead to the inability to measure further decline, and hence misclassification of response on the primary endpoint.

The company also showed that measured biomarkers of neuroprotection, neurodegeneration and neuroinflammation consistently outperformed placebo in the Phase 3 trial, suggesting improvement over placebo. I refer readers to my previous coverage for more detail here, but will below reiterate some points, and I will cover recent developments shared by BrainStorm.

iv) The FDA may be applying more regulatory flexibility

Since years of not having seen any drug approved, the conditional approval of Aduhelm in mid-2021 was the first of several approvals in different neurodegenerative diseases. These approvals were both in Alzheimer’s and ALS at this point in time, and I believe they are a sign that the FDA may be applying more regulatory flexibility than before.

v) The FDA may not have an issue with changing its mind in light of new data

The FDA’s department of neuroscience may be more flexible when it comes to approval than first thought. Amylyx’s checkered approval history – first a negative vote by the FDA’s AdCom, then an approval in Canada, then a positive vote by the FDA’s AdCom and finally conditional approval – shows how opinions can change in light of new data.

vi) The effect on NfL and perhaps other biomarkers could be accepted as a surrogate endpoint for conditional/accelerated approval

In 2021, Biogen’s Aduhelm received accelerated approval on the basis of a surrogate endpoint , namely the reduction of amyloid-beta, a traditional hallmark of the disease, without the link to cognitive benefit. This was a first in neurodegenerative diseases for the FDA, though it is commonplace in other diseases such as cancer, and the FDA has provided a list of surrogate endpoints that have in the past been accepted. I believe it has set in motion a completely new approach. Discussions having taken place with Amylyx showed how the FDA had repeatedly requested the sponsor how its drug candidate performed on neurofilament light or NfL, another possible surrogate endpoint with a high prognostic value of treatment effect. I have previously quoted the FDA’s former director of the office of neuroscience, who considered that the FDA repeatedly asked Amylyx about that biomarker, which ‘while not suitable as a stand-alone measure, could provide important contextual and supportive information of an ostensibly beneficial clinical effect’. NfL, which picks up the tiniest structural elements of neurons which have crossed into the bloodstream, may be able to predict clinical benefit of treatment candidates. Prior to its AdCom meeting of March 22, 2023, Biogen had Biogen drafted an extensive note on NfL which can be read here (pages 33 to 47). Biogen’s phase three trial, though not showing statistical significance on the primary and secondary endpoint, did see a 55% reduction in NfL over 28 weeks, and patients who had been on placebo saw a 44% decline in NfL levels when they were put on the drug in the open label extension study. At Tofersen’s AdCom meeting of March 22, 2023, the FDA unanimously voted 9-0 that Tofersen’s effect on levels of NfL led to reasonable likeliness of a clinical benefit, opening the pathway of accelerated approval, if the FDA agrees with its AdCom’s view.

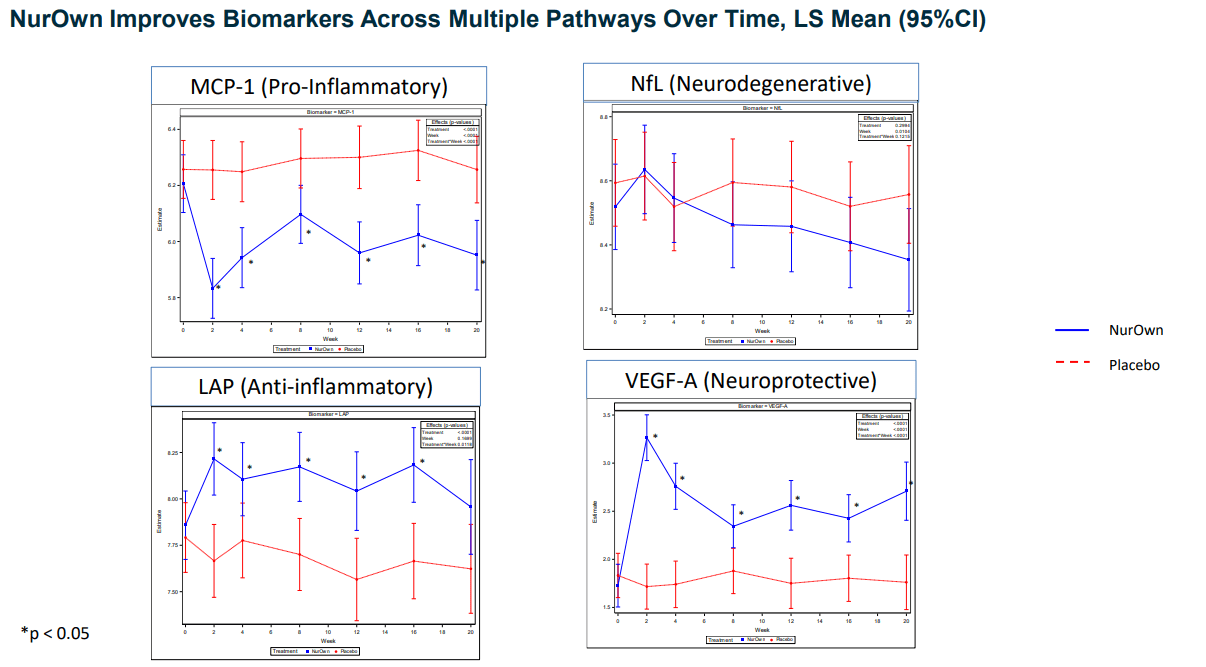

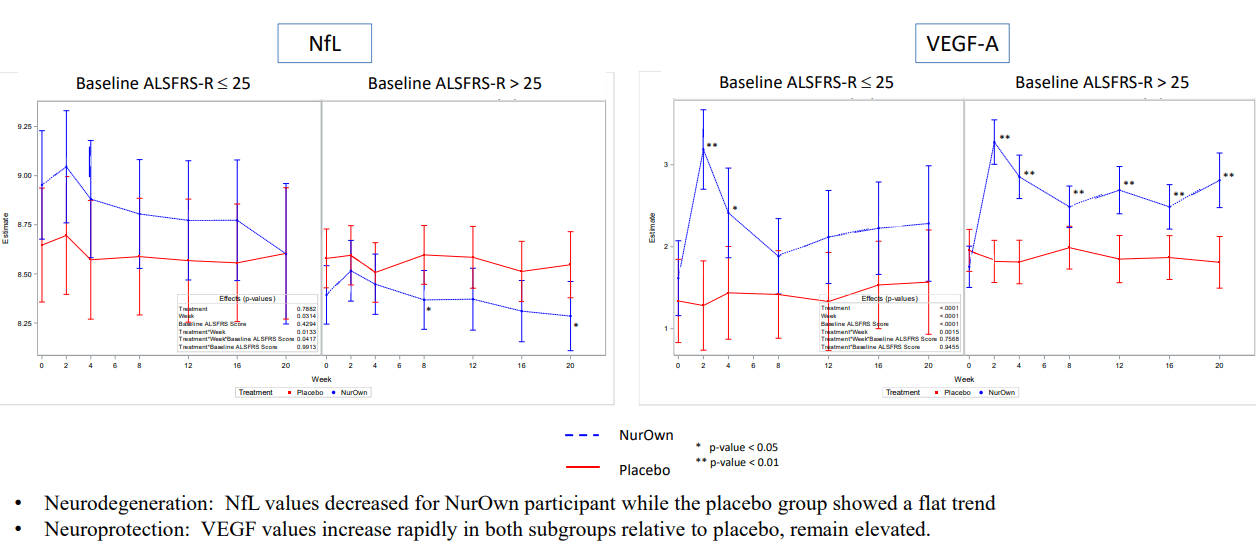

NurOwn, a treatment candidate for the entire ALS population, did much better, reducing NfL levels by 82% compared to placebo over the course of 20 weeks, in both the more and less-advanced patient population. Plus, other biomarkers of neurodegeneration, neuroprotection and neuroinflammation all moved in the same direction.

{kind=link}

NurOwn improves different biomarkers (Biotech Showcase presentation)

{kind=link}

NurOwn improves NfL and VEGF (Biotech Showcase)

{kind=link}

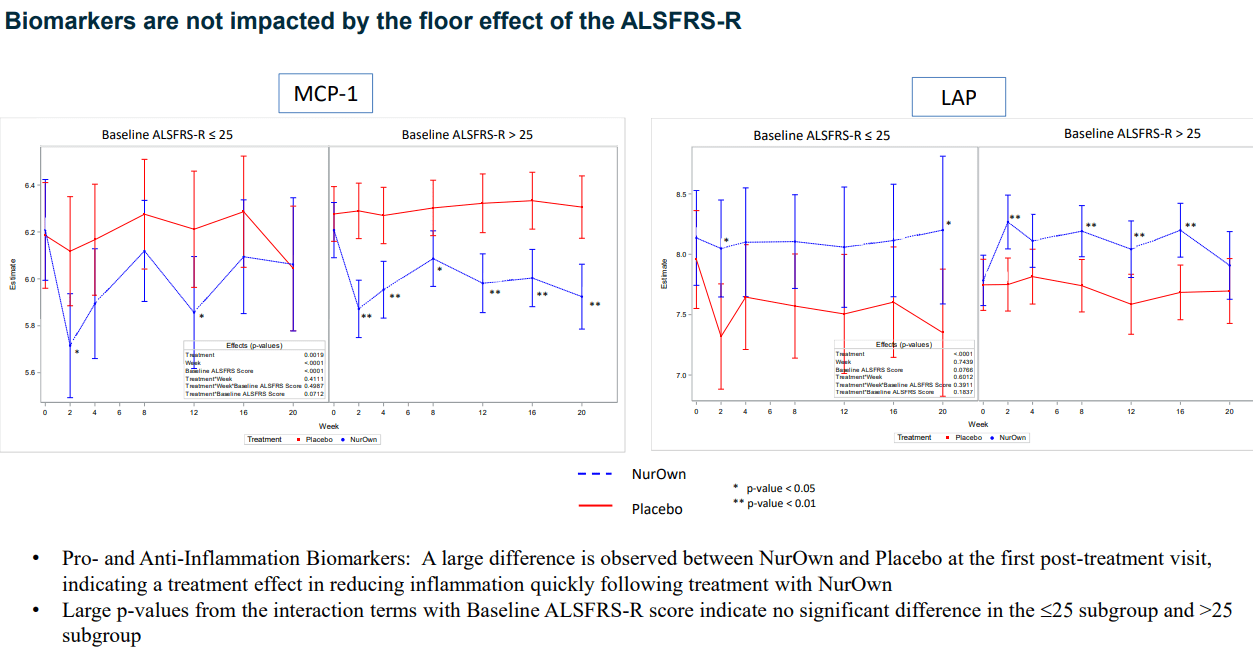

Biomarkers MCP-1 and LAP not impacted by floor effect (Biotech Showcase presentation)

vii) Neurodegenerative diseases’ late diagnoses or fast progression may have led to failing trials

There is a need for tests which should allow detection of neurodegenerative diseases in the earlier stage, as these diseases often seem irreparable once they hit the final stages. It may also become increasingly clear to the scientific community that floor effects in further-progressed patients are, in part, the cause of trials not meeting statistical significance. The ALSFRS-R is a bounded scale, meaning at some point the slope of decline must slow. At what level this happens is uncertain. There is, hence, a risk that people with lower ALSFRS-R scores at baseline may experience slowing of decline due to a floor effect of the ALSFRS-R which could result in a misclassification on the primary endpoint (floor effect).

{kind=link}

Floor effect Phase 3 trial (Biotech Showcase)

There may be a reason why Aduhelm and Leqembi have been tested in patients with mild cognitive impairment or mild Alzheimer’s, also called early AD. Cassava’s ( SAVA ) open label study data in 200 patients over a year’s time reveals that among the further-progressed patients, its drug candidate is not able to reverse cognition. BioVie ( BIVI ) also noted remarkably more treatment effect in the younger Parkinson’s patient population , and less advanced Alzheimer’s patients respectively. The FDA may realize that BrainStorm’s excuse of not having been able to reach statistical significance is actually entirely legitimate, and should at least allow conditional approval conditioned upon a confirmatory trial.

viii) The AdCom and PDUFA dates may be for the near future

BrainStorm had been informed by the FDA last Wednesday March 22, 2023 that an AdCom meeting would be convened. A PDUFA date typically follows such an AdCom meeting, and on the basis of BrainStorm’s March 27, 2023 webcast, these events may all be for the rather near future, as BrainStorm’s CEO mentioned the following when asked about the timing of the upcoming AdCom meeting during the investor call of March 27, 2023:

The FDA in the notification said, they would be advising us very soon on the date. They’ve been working on this quite a while to get the date. […] So we have got to give them a few more, I don’t know, days or weeks, I don’t want to say then they’ll quote what I said, but we understand we’ll get that date very soon. But the FDA wanted us to be able to communicate to patients.

The question of clinical benefit

Apart from the question on the prognostic value of NfL, whether or not assessed in combination with other biomarkers, the most important question remains whether NurOwn can lead to a clinical benefit in patients with ALS.

Results of NurOwn’s Phase 3 trial in ALS did show an improvement in the overall treated patient population compared to placebo, but not one that led to statistical significance . NurOwn also demonstrated meaningful improvement compared to placebo in a pre-specified subgroup of patients with early and less advanced disease.

NurOwn treatment effect, subgroup analysis (Biotech Showcase presentation)

Subgroup analysis, slide 2 (Biotech Showcase presentation)

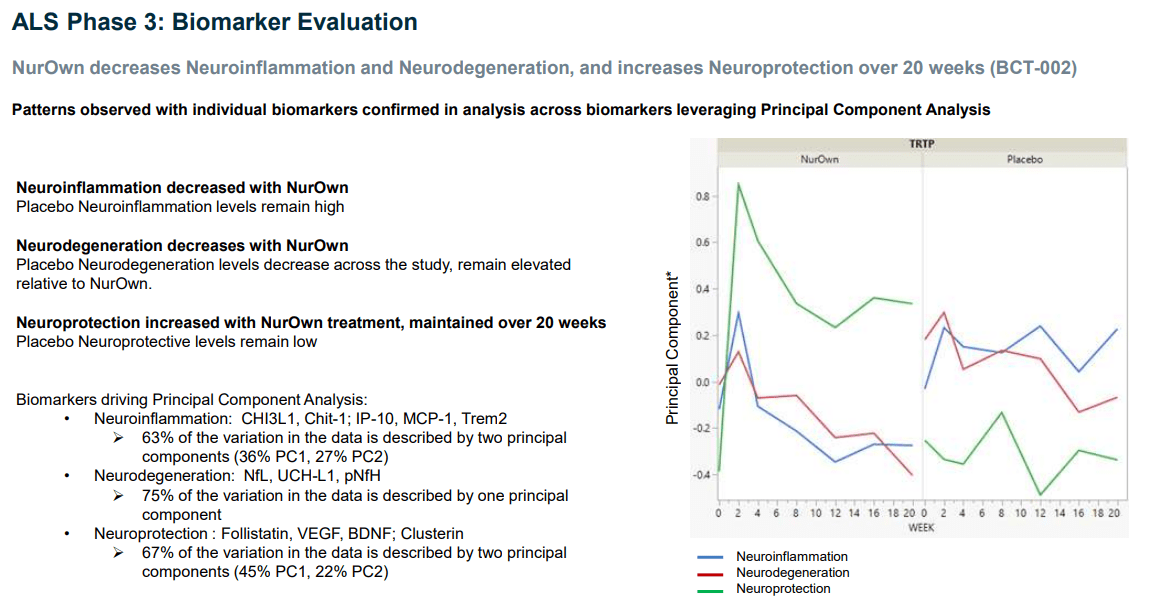

The changes seen in biomarkers following NurOwn treatment are moreover statistically linked to clinical outcomes from the trial, and the same biomarker responses and patterns were observed in participants with less advanced ALS, and advanced ALS.

{kind=link}

Biomarker evaluation (Biotech Showcase presentation)

Finally, BrainStorm has also shown that patients with the A/C Genotype treated with NurOwn had a significantly higher response compared to placebo (A/C Genotype, 65% NurOwn vs. 29% Placebo, p=.011).

Thoughts on valuation

BrainStorm’s stock currently has a market cap of about $90 million. Merely looking at ALS, I had previously considered that peak sales could reach $300 million by 2028, on the basis of market revenue forecasts of $885 million yearly.

I am changing that position in light of Amylyx’s Relyvrio’s pricing of $158,000 per year, much higher than the fair price that had been considered to be in between $9,100 and $31,700 per year. There are about 30,000 patients in the US suffering from ALS. With a moderately assessed peak market penetration of 20% at a price of $100,000, peak sales could reach $600 million. And BrainStorm may not have to wait until 2028 to reach peak sales potential.

For reference, in an article on Amylyx, Seeking Alpha analyst Stephen Ayers had suggested peak annual revenue for could be in between $632 million and $1.58 billion, depending on the level of market penetration achieved, and I believe he mistakenly considered the number of ALS patients in the US to be 20,000 instead of 30,000 . For further reference, Amylyx’s market cap is currently trading at about $2 billion, after having been approved in Canada and the US last year.

I think competition from the side of Biogen’s Tofersen would be fairly limited, as that drug candidate only addresses a small subpopulation of all ALS patients, namely those with a SOD1-gene mutation, which is an ultra-rare and aggressive form of ALS.

Moreover, NurOwn’s side effects are mild and temporary , and the drug may hence have a better safety profile than Relyvrio or Tofersen .

Financials

BrainStorm has just reported its results for the past quarter on March 30, 2023. Its cash position as of December 31, 2022 was $3 million, compared to its previously known cash position of $7.4 million as of the end of September 2022, and $22 million a year earlier. Brainstorm has 36.5 million common shares outstanding, and fully diluted, has a share count of 39.9 million shares. If the company has not already tapped into its ATM over the past three months, which I consider unlikely, then it would be running out of cash at this time. Questions on this return on investor calls, and during the previous quarterly call, BrainStorm’s CEO mentioned :

We have an ATM of $100 million that we can tap into opportunistically. In addition, quite a few of our major shareholders are considering supporting the company at this time. They felt it might be a good time to even out their investments while supporting the company's potential pathway to approval. [...] The best strategy for financial means where the main focus of the company is and that is to arrive at an agreement with the FDA to allow an AdCom. Once we have figured this out, our burn rate will be in my belief a non-issue.

The at-the-market financing facility is with Raymond James, and Brainstorm can pick up to $100 million tapping into it. If dilution were to occur in the near future, if it hasn't occurred yet, all will depend on the amount of financing picked up. The cash burn is about $6 million per quarter, so there is real risk of additional dilution and share price pressure.

Risks

As mentioned in my previous coverage, I reiterate to readers that things may not turn out the way investors hope them to. If at any stage, the AdCom meeting or PDUFA may not turn out positive for BrainStorm, shares of BrainStorm may still fall considerably. The risk here involves primarily regulatory dependency and efficacy issues.

Conclusion

BrainStorm announced on March 27, 2023 that it has secured an FDA advisory committee vote for treatment candidate NurOwn for the treatment of ALS. That AdCom vote is unexpected, as the FDA could have easily explained in the type A meeting of January 11, 2023 why it had rejected BrainStorm’s BLA.

Recent developments in the approval of drugs for ALS and Alzheimer’s may indicate the FDA’s willingness to accept surrogate endpoints for approval, and more specifically NfL data as a surrogate endpoint. NurOwn’s results on biomarker NfL have actually been remarkable good, outperforming Biogen’s/Ionis’ Tofersen, which has its PDUFA date on April 25, 2023 and has just received an AdCom vote which was unanimously in favor of using NfL as a biomarker predictive of clinical benefit.

As BrainStorm has amended its biologic license application using the file-over-protest route, a possible PDUFA date may come sooner than expected, as the FDA’s advisory committee may already convene in a matter of days or weeks.

BrainStorm’s stock has known two major sell-off events both in 2020 and 2023, which create an investment opportunity. Trading at a market cap of about $90 million, with peak sales potential of around $600 million, I believe there may be a good opportunity for investors at this time. Though BrainStorm’s need for cash is dire, it can tap into its at-the-market facility, and may have already done so over the past months.

For all the above, whereas in my previous coverage I had rated the company as a Buy, I am currently rating it as a Strong Buy.

For further details see:

BrainStorm: Upcoming AdCom Meeting For NurOwn For ALS Could Be Start Of Major Turnaround