BWAY - BrainsWay Is Reviving From A Deep Depression

2024-01-08 23:32:32 ET

Summary

- BrainsWay has achieved a successful turnaround with positive adjusted EBITDA and cash flow in Q3/23.

- The company offers advanced TMS therapy devices and has numerous patents.

- There are plenty of growth drivers from reimbursement, new conditions, and international expansion.

- With little in the way of recurring revenues, BWAY is dependent on device sales, which might not increase in a linear fashion and have the ability to disappoint.

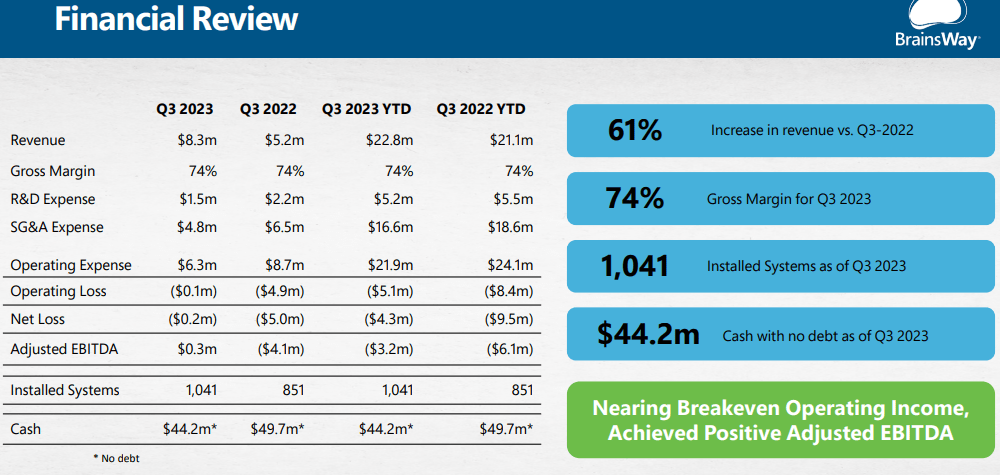

BrainsWay ( BWAY ) has produced a successful turnaround of their business with Q3/23 being the first quarter in which adjusted EBITDA as well as cash flow were positive, based on a 61% revenue growth and an OpEx decline in dollar terms. We think this turnaround has plenty of legs.

A quick recap

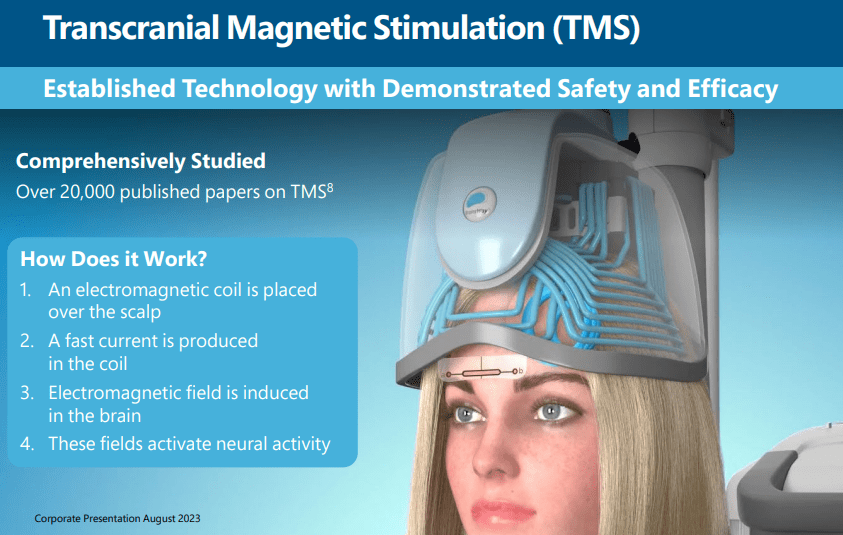

BrainsWay offers TMS or transcranial magnetic stimulation therapy devices:

{kind=link}

TMS is an established technology and BrainsWay claims to have the most advanced version:

{kind=link}

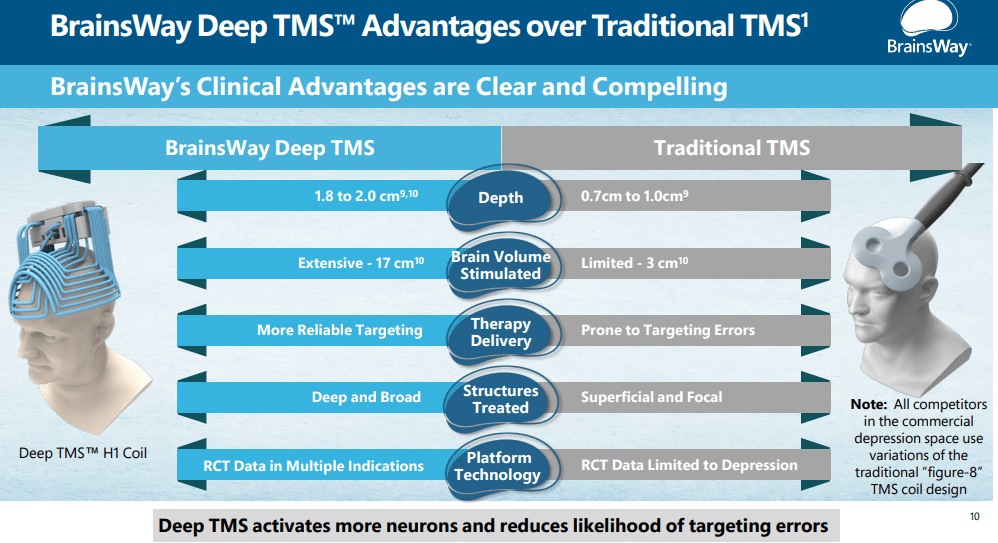

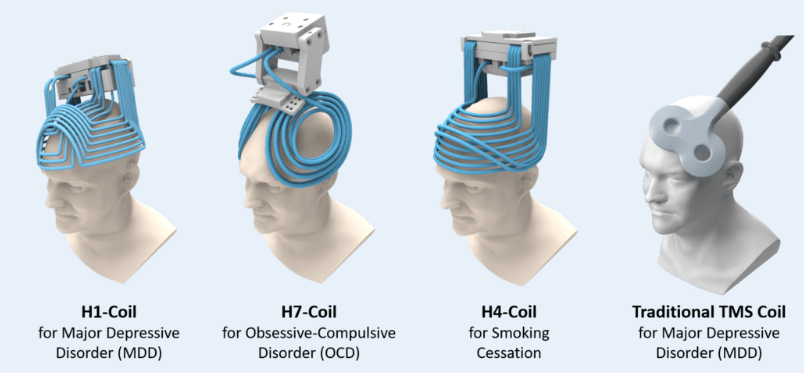

The company website also explains the advantages of deep versus traditional TMS and the company argues it's the only company offering deep TMS therapy. The company offers different coils for different applications:

{kind=link}

The company has numerous patents (30+ in the US, 50+ in the rest of the world). There is plenty of evidence TMS in general, and BrainsWay's version in particular, works (for further information see the company website , the IR presentation or the 10-K).

They called for additional research proposals on the effectiveness of Deep TMS and received 30 applications by the July 1 deadline, they are going to select 10 of these to advance research further.

Market

From Grandview Research :

Grandview Research

This is a handy graph as BrainsWay is supposedly the only company offering Deep TMS therapy and it has at least a third of the overall market.

Competition

There is serious competition in the form of Neuronetics with its NeuroStar . The company generates more than twice the revenues compared to BrainsWay, but also produces larger losses (and $37M in operational cash outflows in the last 12 months).

Its NeuroStar is only cleared for depression . The recent spurt in BrainsWay's stock price has enabled it to jump Neuronetics on a 3-year return basis, no doubt Neuronetics still large losses have something to do with this:

But as fellow SA contributor Stephen Ayers explained , there is additional competition from the likes of:

- Magstim's 3D Navigation System offers precise targeting.

- Magventure's NeuroStar has the advantage of greatly reducing treatment times for MDD.

- New drugs like ketamine can produce rapid relief for treatment-resistant depression.

- ECT (electroconvulsive treatment).

- VNS (vagal nerve stimulation).

- DBS ( deep brain stimulation) from the likes of Medtronic ( MDT ) and Boston Scientific ( BSX ).

Here is what the 20-F says about ECT:

While ECT has high proven efficacy (70-75%) for patients with MDD, ECT's potential for serious side effects, as well as negative stereotypes surrounding the treatment, often cause patients to be reluctant to undergo ECT. ECT affects the entire brain, including parts that do not need treatment, and may cause permanent cognitive damage, including memory loss. ECT may have significant and relatively severe side effects, the most common of which are cognitive and memory loss, changes in blood pressure, muscle pains, nausea, changes in mood, headaches, and pain or discomfort.

And about VNS and DBS:

VNS and DBS are invasive therapies that can have serious side effects. Both involve implanted devices, which require surgery. In DBS, two electrodes are surgically implanted in the brain and a pulse generator is implanted into the patient's chest. The electrodes produce electrical impulses that can regulate the electrical activity of the brain. In VNS, a pulse generator is implanted on the upper left side of the chest to stimulate the vagus nerve. VNS and DBS include surgical-related risks, such as infection or local damage to the recurrent laryngeal nerve, which may lead to permanent voice alteration.

It's difficult to arrive at any definite conclusions here as each solution has its advantages and disadvantages.

Other limitations

There are some practical limitations to BrainsWay's Deep TMS systems:

- They require multiple 20-minute sessions 5x a week for MDD (and up to 24 maintenance sessions 2x a week) and regimens for smoking cessation and OCD are only slightly less (smoking cessation) or more (OCD) onerous.

- The costs can add up for patients with insufficient coverage ($200-$300 per session).

Business model

The company sells its TMS systems directly to hospitals, medical centers, and clinics in various countries through exclusive distribution agreements in countries like Japan, South Korea, Thailand, Taiwan, the Philippines, and the United Arab Emirates.

Under these agreements, the distributor typically receives an exclusive right to commercialize the TMS in the relevant territory.

Apart from direct (or indirect) sales, TMS systems can also be leased, typically for a 48-60 month period at a fixed annual fee for unlimited use. There are hints of some recurring revenue opportunities ( 20-F ):

We also utilize and/or are planning to utilize other commercial models, including those based on a pay per use model, with certain customers in certain territories. Additional potential revenues may be derived from extended warranty fees paid for the system for service coverage beyond the standard included warranty period, and from variable or usage fees based on the number of treatments performed with the system. We are also able to leverage our platform technology, which includes the ability to treat multiple indications using different H-Coil helmets, to facilitate transactions utilizing combined pricing models often involving a single system with one or more add-on helmets. These flexible offerings are designed to facilitate market penetration by addressing the differing clinical needs and risk tolerance among our customer base.

BrainsWay generates recurring revenues through leasing, extended warranty and maintenance fees, and usage fees but we haven't seen these split out and (apart from leasing fees) these are not significant.

Given that revenue from leases is spread out over 4-5 years it looks like there is a significant shift in the business model ongoing away from leasing and towards the sales model:

BWAW 20-F

We think the business model is a limitation, a much better one would be a business model based on pay-per-use. Now growth is dependent on selling ever more systems although additional coils and service revenues do help.

Growth

We see three main growth vectors:

- Selling more systems to new and existing customers

- Increasing utilization

- Approval for additional conditions

- International growth

They are selling more systems to new and existing customers, they have shipped 53 systems in Q2 (30 of which were recognized in the quarter) and a net 56 in Q3 (46 of which were purchased and 10 leased).

The company now has a total installed base of 1041 systems (versus 851 at the end of Q3/22). The company focuses on larger clients with a large existing US customer who ordered 30 systems , and another one who ordered 10 systems this year.

In Q3 there were additional large orders:

- A new partner , a prominent mental health clinical treatment provider in the Northeast US ordering 10 systems

- Another 10 were ordered by Katie's Way Plus, a mental health services provider serving active-duty military members, veterans, and their families.

- Q4 saw another expansion with a big client.

Demand for OCD treatment continues to grow with the company shipping 48 OCD (obsessive-compulsive disorder) coils as add-on helmets (up from 34 in Q2). Nearly half of its installed base now includes OCD treatment capability.

Reimbursement helps, there are three applicable CTP codes and the one for OCD (Obsessive Compulsive Disorder) is especially helpful. There was also further good news on this front:

- Aetna now reimburses TMS treatment for MDD under behavioral health nurse practitioners

- BlueShield Michigan reduced the number of antidepressant medication attempts from 4 to 2 before approving TMS treatment.

- Blue Cross Blue Shield of Louisiana reduced the patient eligibility requirements for TMS treatment from four failed medication trials to two.

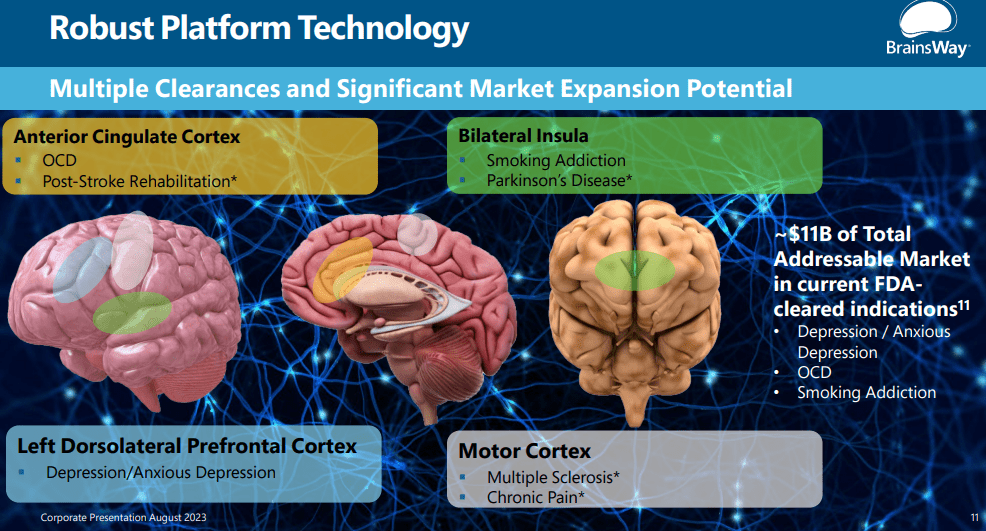

The devices have been FDA-approved for four conditions (OCD, depression, smoking addiction, and anxious depression) and management argued during the Q3CC :

Just to remind everyone that in Europe, we have cleared for 10 indications, not only three like in the US

We take it that in the US they took depression and anxious depression as a single condition.

New indications

There are future possible indications:

{kind=link}

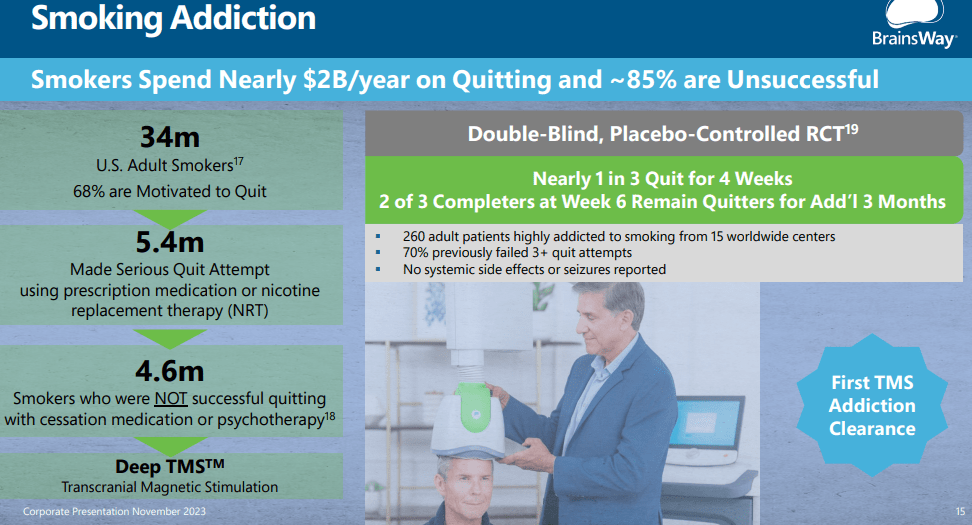

The most immediate opportunity is smoking addiction , for which the TMS has already been approved:

{kind=link}

Needless to say, this is a large opportunity, the company is looking for a distribution partner for the smoking cessation indication, and some progress was gained with respect to reimbursement in the form of a positive recommendation issued by the Clinical TMS Society.

Then there is the accelerated TMS treatment , involving five treatments a day for six days for MDD patients. Management argues that preliminary trial data is very favorable in terms of safety and efficacy.

Their first rotational field system (or multichannel system) will be placed in the present quarter, like some other technology it's licensed from Yeda and the company is required to pay royalties (5% maximum), from the 20-F:

where two coils perpendicular to each other are connected to two channels and operated with a phase delay, thus inducing a rotating electric field in the brain. This enables stimulation of neurons in various orientations, in contrast to currently available TMS devices which stimulate only neurons parallel to the induced field.

It could work for neurological conditions like Alzheimer's, but it's very early days here.

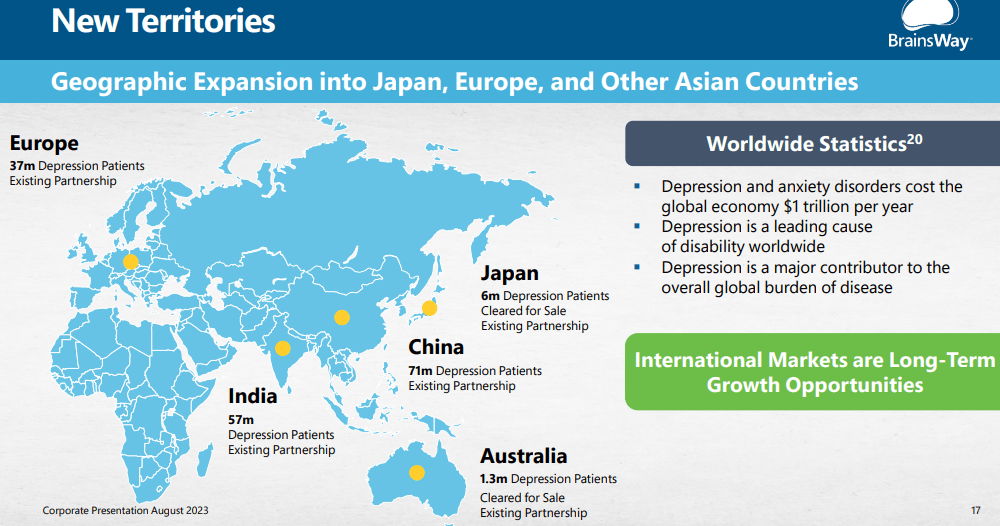

International growth

The large majority of revenues (70%+) comes from the US but there are significant opportunities abroad as its successful Q2 Indian order for 25 systems illustrates:

{kind=link}

And this is just the worldwide opportunity for depression. Apart from the large orders from India, there has been additional success in Asia in Q3 with orders from Taiwan , where there are now 16 systems.

Some 25% of revenues in FY22 came from outside the US where it mainly uses the sales (rather than lease) model:

Approximately 25%, 12% and 13% of our revenues for the fiscal years ended December 31, 2022, 2021 and 2020, respectively, were generated outside of the United States. A significant part of our sales outside the United States are made indirectly with local distributors and agents. Most of our sales outside the United States are made only via the purchase model, although we lease some of our Deep TMS systems in France and Israel. Our primary focus is on selling to hospitals, medical centers and clinics dealing with the treatment of psychiatric neurological and addiction illnesses and disorders.

Evolve Psychiatry sheds some light on approved conditions in Europe :

In Europe, Deep TMS has received the CE certification mark for various conditions, including PTSD, Alzheimer's disease, autism, bipolar disorder, Multiple Sclerosis, and Parkinson's disease. It has also received the CE certification mark for post-stroke rehabilitation, chronic pain, and smoking cessation therapy.

That's a much wider approval compared to the three US-approved conditions (MDD, OCD, and Smoking Cessation) and Europe provides ample room to grow and they are looking for a distributor.

Yet somewhat surprisingly, management indicated Asia Pacific (Japan, China, and India as well as Taiwan and South Korea ) as its greatest international opportunity where their installed base increased to 16 on good momentum.

Finances

There was a considerable retreat last year on a tough macro environment for smaller customers after which they redirected to pursuing bigger customers. Now, the company is growing again (on a sequential basis 18% in Q2 and 6% in Q3).

{kind=link}

The margins in the graph below are in GAAP:

Gross margin largely depends on US versus international mix (margins are somewhat higher in the US) and direct sales versus lease. The company has embarked on cost-cutting which has reduced OpEx spending quite a bit even in dollar terms:

Considerable reductions were achieved in all three categories (S&M, G&A and R&D), combined with 61% revenue growth in Q3 which produced tremendous operating leverage.

Cash flow (as well as adjusted EBITDA) has turned positive in Q3 for the first time and the company ended Q3 with $44.2M in cash and no debt.

The company is targeting breakeven operating income and positive adjusted EBITDA in Q4.

Valuation

The share count is quite well behaved which is no surprise as the company still has $44.3M in cash. There were 1.36M options exercisable and 769 RSUs at the end of FY22 (the latest data) so we take the fully diluted share count as 18.7M, which at $6.5 per share gives a market cap of $140.25M and an EV of $96M.

At an estimated $30.5M in FY23 revenues, the shares sell at 3.15x EV/S. Analysts have surprisingly dim projections for 2024, expecting revenues to grow to just $35M with the company still making losses (EPS will only rise 3 cents to -$0.12).

It's surprising as management noted a favorable demand backdrop both in the US and overseas.

Risks and reservations

There are several risks and reservations we have:

- The business model is dependent on device sales and generates little in the way of recurring revenues. While the 61% Q3 growth is impressive, it's not the first quarter generating $8M+ in sales, so perhaps this is what produced those lowball analyst 2024 projections.

- Ever-increasing device sales aren't given in the face of an increased installed base, significant competition, and end-user inconvenience and cost.

- Economic headwinds that make life difficult for small practices like in 2022 and can affect Healthcare CapEx sales in general.

And then there is this (20-F):

Patents covering some of our core technology have expired or will expire within the next five years. In particular, the earliest of our U.S. patents on Deep TMS is set to expire in 2024.

In fact, some patents (Family A, coverage for the H-Coil for MDD, OCD, and smoking cessation) already expired abroad and are set to expire in the US in 2026, but the 20-F, so we assume that this doesn't generate a major headwind but based on the provided information we can't be 100% sure.

Conclusion

The company has a lot going for it:

- Competitive devices.

- A large and growing market opportunity with growing reimbursement, number of conditions, and geographical expansion.

- Growth has returned and the company is on the verge of turning its finances around.

- The shares are still reasonably priced even after a considerable rally.

However, there are some risks and concerns relating to its dependence on device sales, lack of recurring revenue, significant competition, and user acceptance.

The upshot : What is beyond dispute is the turnaround in the company's finances and still reasonable valuation. Growth also looks set to continue as the company still has plenty of markets to go after, adding new customers, selling more systems to existing ones, new indications, and international sales.

However, high revenue growth cannot be taken for granted given the dependence on device sales, increasing competition, and some limitations that have to do with user inconveniences.

So while we think the present uptrend could continue, this is highly dependent on quarterly results not disappointing which requires progressively large equipment sales, something that hasn't happened in the past.

Given the substantial rally that has already happened, we think there are better chances elsewhere.

For further details see:

BrainsWay Is Reviving From A Deep Depression