LND - BrasilAgro: Real Estate Resilience During A Challenging Harvest

2023-10-24 04:28:27 ET

Summary

- BrasilAgro should report a lower yield due to challenging factors in the 2022/23 harvest, but maintains a positive outlook for the future.

- The company's strategy revolves around efficient real estate transactions and profitable agricultural production, with an emphasis on mitigating risk.

- Despite dividend concerns and market fluctuations, BrasilAgro remains an attractive option for income-oriented investors, with the potential for strong returns and appreciation in its stock value.

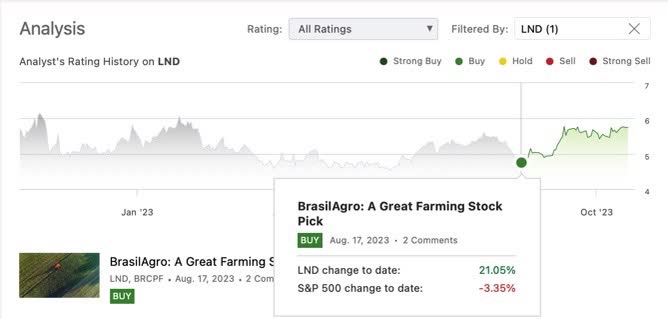

In my previous article about BrasilAgro - Companhia Brasileira de Propiedades ( LND ), I identified the company as an excellent farming choice. This assessment was primarily based on the observation that its stock was trading significantly below its net asset value ((NAV)). The company also boasts a well-rounded business model that includes owned and leased land. It also holds potential for long-term growth by capitalizing on Brazil's thriving agribusiness sector and the possibility of increasing dividend distribution. Since mid-August, the company's shares have experienced a notable increase of approximately 21%.

{kind=link}

In September, the company released its results for the fourth quarter of 2023. The company reported weak results due to a harvest significantly impacted by several external factors. However, the company's ability to sell farms helped mitigate the impact, resulting in results that were not as dismal as initially anticipated.

Despite the potential for a dividend decrease this year and possibly in the next, BrasilAgro has updated its guidance for the 2023/2024 harvest, offering a more optimistic outlook. With this in mind, given that the company continues to trade at heavily discounted valuation multiples, I maintain my buy recommendation for BrasilAgro. It remains a solid choice for income-oriented investors.

A Simple Strategy but Difficult to Execute

The strategy behind BrasilAgro's operations primarily revolves around timing real estate asset transactions (buying or selling) effectively and ensuring the agricultural production on its farms is both efficient and profitable. This approach aims to achieve optimal operational results and maintain the property's value. Additionally, if all goes well, the intention is to sell these properties after five years of increasing crop productivity.

The sale of two farms in April significantly bolstered the results in the fourth quarter of the 2022/23 financial year, aligning with its core focus. In Brazil, these properties represent assets with high current liquidity.

Nonetheless, agriculture comes with its set of challenges. There are both good and bad harvests, and weather and price fluctuations are inherent to the industry. Depending on the behavior of these factors, liquidity can become uncertain. There are opportune moments for selling farms and favorable times for buying, but such opportunities may not always be available.

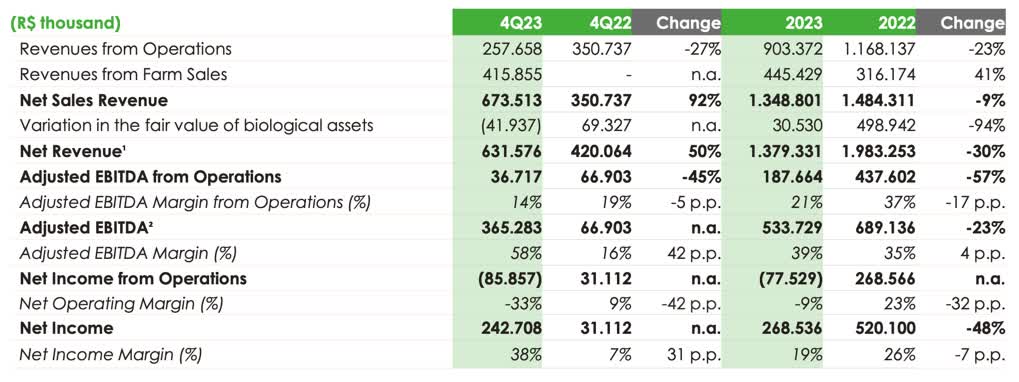

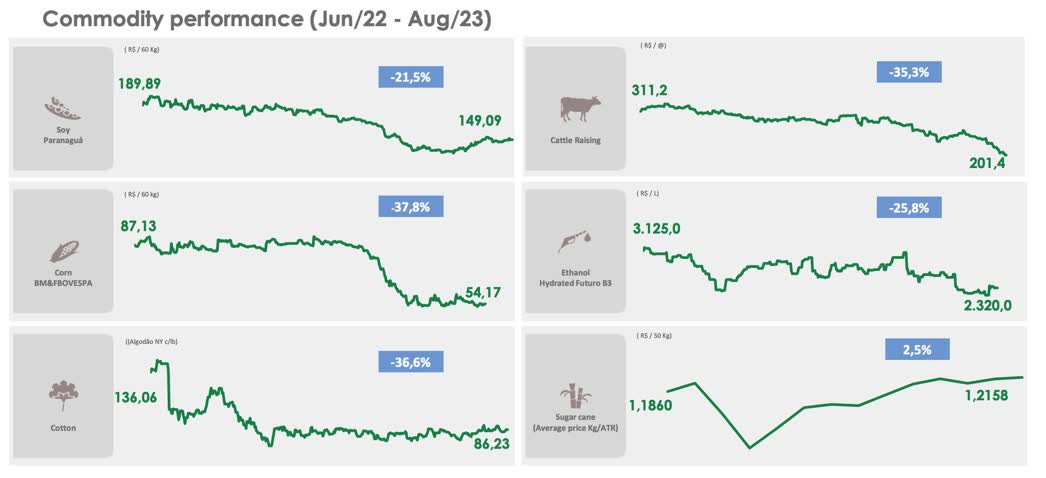

This strategy yielded successful results in the fourth quarter of 2022/23. Even amid the decline in commodity prices, including soybeans and corn, the sale of the two properties led to a remarkable 92% growth in the company's net revenue compared to the same period in 2021/22, reaching R$673.5 million.

{kind=link}

The company's management strongly emphasizes achieving balance and risk diversification. Operationally, BrasilAgro aims to expand its agricultural area by 10% to 15% in each harvest, akin to recent seasons. In the real estate business, the goal is to renew 10% of its portfolio annually.

"When we sell land, we exchange operating income for real estate. However, we must establish the operational side as a recurring source of EBITDA, considering that land is worth 20 to 25 times the multiple it generates," noted CEO André Guillaumon.

How Has the Execution Been Carried Out

BrasilAgro has recently announced its earnings results for the fourth quarter of the 2022/23 harvest, which concluded in June. The company reported a net profit of R$268.5 million, marking a 48% decrease compared to 2022, with a total net margin of 19%. This net profit was primarily attributable to the company's real estate strategy.

In the same comparative analysis, the company's adjusted EBITDA increased from R$66.9 million to R$365.2 million, and the total net revenue surged by 92% to reach R$673.5 million.

The 2022/2023 harvest proved to be among the most challenging for the company. The grain and cotton harvests fell below expectations, totaling 354,000 tons, a 9% decrease compared to the initial company estimate.

Several factors directly influenced the company's results during this harvest, including (1) a decline in agricultural commodity prices, (2) the devaluation of the Brazilian real against the US dollar, (3) climate issues caused by El Niño, (4) the high cost of fertilizers, (5) the high cost of seeds, and (6) the high cost of fuel.

{kind=link}

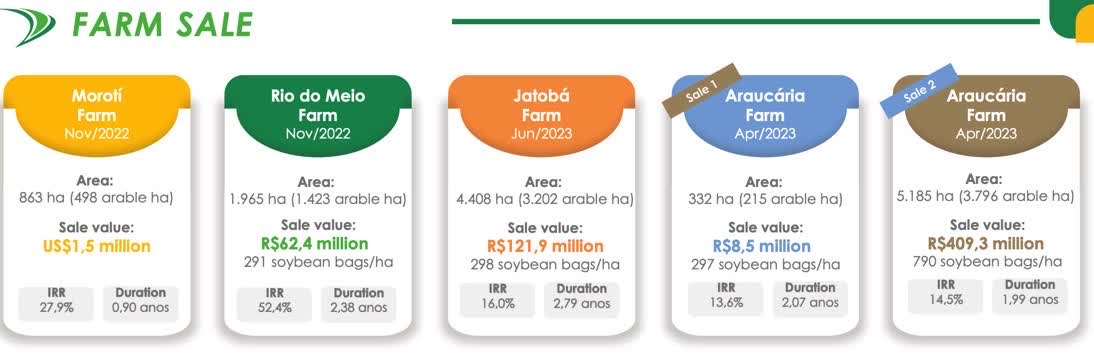

In contrast, during the 2022/2023 harvest, the company successfully sold over 12,000 hectares, of which 9,100 hectares were utilized, generating R$610 million in revenue. Notably, these sales' IRRs (Internal Rate of Return) were quite compelling, ranging from 13.6% for Fazenda Araucária to an impressive 52.4% for Fazenda Rio do Meio.

{kind=link}

Over the past five years, the average value of farm sales stands at R$269.2 million, with unleveraged IRR spanning from 13.6% to 56.5%. This data underscores how BrasilAgro has consistently managed to create value from its real estate activities.

As of the end of June, BrasilAgro's net worth reached R$2.197 billion, and the market value of its properties was estimated, according to the company, at R$3.1 billion. The company had 19 farms in operation, with 16 of them located in Brazil (spanning six states), one in Paraguay, and two in Bolivia. The total land area of these properties amounted to 273,500 hectares, comprising 213,300 hectares owned and 60,200 hectares leased.

The most recent acquisition, made during the 2022/23 financial year, is a 10,800-hectare property in the state of Mato Grosso, Brazil. Approximately 6,000 hectares were leased from a Comodoro and Mato Grosso property during the year. These areas are more mature in production and aimed at maximizing operational results.

What to Expect from the 2023/2024 Harvest

For the 2023/24 harvest, with soybean and corn planting already underway, the company projects that its total planted area will reach 185,700 hectares, compared to 168,900 in 2021/22 and 168,700 in 2022/23. The sites directly operated by BrasilAgro will account for 53% of the total, leased areas managed by the company will contribute 39%, and areas owned by third parties and operated by BrasilAgro will constitute 8%.

In the crop breakdown, soybeans take the lead with a 40% share of the area, followed by corn (14%), sugarcane (14%), cotton (4%), and beans (4%). Livestock activities account for approximately 8%. Despite declining grain prices, the company anticipates growth in production volumes for all crops. For soybeans, an expected increase of 21% is projected, reaching 248,500 tons. As for second-crop corn, 102,600 tons are expected, representing a 47% increase.

As part of BrasilAgro's strategy to mitigate real estate, production, and market risks, hedging is another crucial aspect to consider. As of June 30, nearly 25% of the expected soybean production for 2023/24 had its price locked at an average of US$ 12.91 per bushel, compared to an average of R$ 14.50 in 2022/23. For cotton, the hedged percentage exceeded 28%, and for corn (total), it reached 6%.

Dividends: Decreasing, Yet Expected to Remain Strong

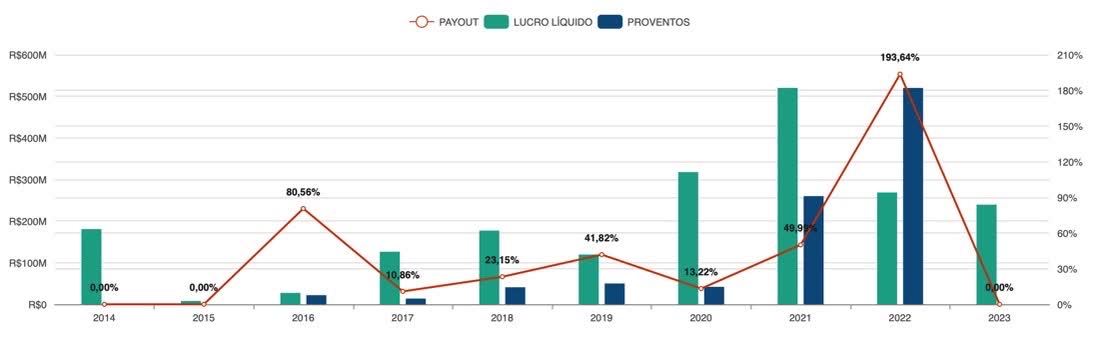

BrasilAgro's agricultural sales have delivered a positive surprise, enabling the company to propose a dividend of R$320 million, equivalent to a yield of approximately 12.8%. This dividend payment will be subject to approval at the Shareholders' Meeting scheduled for October 24, 2023. This is a positive proposal, highlighting BrasilAgro's strong financial position, which allowed for a payout of over 100% in the previous year.

BrasilAgro's payout (orange), net profit (green), and dividends (blue). (Status Invest)

{kind=link}

BrasilAgro has updated its guidance for the 23/24 harvest, reiterating its optimistic outlook for expanding the production area. However, as highlighted by the company's management in recent reports, there may be a shift in its strategy, likely involving a reduction in farm sales in the short term. This adjustment could overshadow the expectations of dividend payments and eliminate an essential trigger for the company's shares.

Assuming that BrasilAgro reports a net profit representing a 13% decrease in 2023 (estimated at approximately $86 million, in line with the S&P Global consensus) compared to the previous year and taking into account the company's average payout ratio of 59% over the past decade, it remains well-positioned to offer a dividend yield exceeding 8%, which is approximately $0.51 per share.

Establishing a 5% return on investment ((ROI)), the current price target for BrasilAgro should be around $10.2.

Company's data, compiled by the author.

The Bottom Line

BrasilAgro continues to be an appealing option for dividend-seeking investors. However, since its business is highly dependent on timing the sale of farms about the seasonality of more or less robust harvests, there is a certain degree of risk in sustaining the company's net profit at very high levels.

While the recent quarterly results may have appeared weak, the modest impact on EBITDA was primarily attributed to lower commodity prices and the company's intentional strategy of postponing farm sales. Regrettably, this decision led to unfavorable outcomes as prices continued to decline, coupled with increased costs for agricultural inputs and freight during the 2022/2023 harvest.

The company has updated the market value of its portfolio, indicating a Net Present Value ((NAV)) per share of R$37.20 ($7.39 considering 1 BRL = 0.20 USD). This suggests a potential appreciation of 28% compared to current market prices, assuming historical discounts are considered.

Based on the company's guidance, there's a higher likelihood that the 2023/2024 harvest will return to the productivity levels observed in previous years. BrasilAgro has already hedged 25% of its soybeans and 6% of its corn and is awaiting improvements in grain prices before securing further hedges. Furthermore, the significant reduction in the prices of specific fertilizers by more than 50% should offer some relief to margins, even in the face of lower commodity prices.

Despite the less robust dividends this year, the outlook for BrasilAgro appears favorable for the coming years. Given the substantial discount in its current valuation compared to its Net Asset Value ((NAV)) and in my dividend valuation model, I maintain a bullish stance on the company's prospects.

For further details see:

BrasilAgro: Real Estate Resilience During A Challenging Harvest