BAK - Braskem: 22% RoR Since March Still A 'Buy' After Q1 2023

2023-05-24 07:45:07 ET

Summary

- Investing in Brazilian stocks is rarely a non-volatile or even somewhat stable venture. So too is the case with investing in Braskem S.A.

- I do have a position in the company, and I believe the time is still ripe to "BUY" more, but it does come at a fair bit of volatility risk.

- Since my last article, the company has outperformed. I'm updating my thesis here, and am showing you why I believe in further upside for the company.

Dear readers/followers,

When reviewing Braskem ( BAK ) the last time, I made a point of a positive stance, and this stance has proven to be the right choice for investors - by which I mean that the investment has more than doubled the S&P500 in the same timeframe. We got the company at a cheap price - at least for that specific article.

Braskem article RoR (Seeking Alpha)

The time has come to update the thesis after that article, to see where the company seems likely to go. We have 1Q23, and we do have some pretty significant news from the high-level for this company - in the form of a potential takeover offer. As of the 15th of May, we have information that says Petrobras ( PBR ), is in talks/considerations of acquiring control over Braskem through a buyout of its partner. The talks seem to be in the initial stages - so let's see what we have going for us here, and whether we perhaps should take advantage of the momentary upswing to take some profits.

Braskem 1Q23 results - good, and overshadowed by takeover talks

So, overall 1Q23 results were pretty good. Braskem managed to maintain a strong liquidity position, where the next 6 years of maturities are covered by the company's current cash alone. Fundamentals for this company are of importance, and debt/liquidity are important, with 14-year average maturity being good. At the corporate level, the company has a debt/leverage ratio of 3.86x, which is neither the best nor the worst. This comes to a debt/EBITDA of around 12x, and this puts the company at some very pressured interest coverage ratios, resulting in some low scores for Piotroski-F and Altman, giving the company the picture of being in distress.

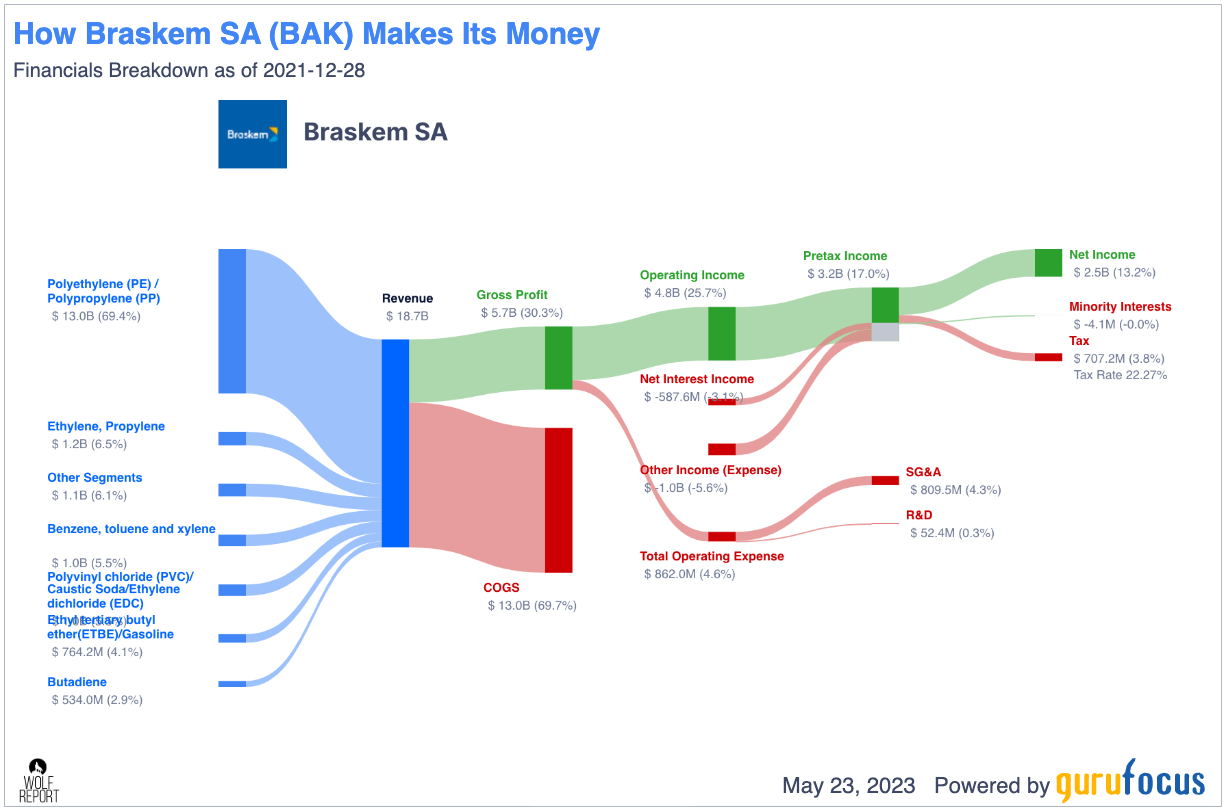

I would not call the company one in "distress". This is why looking at several perspectives is important. Braskem is a solid Chemical company that comes with very attractive segments and generates a double-digit, 13%+ net income and a 30%+ gross margin.

{kind=link}

This is not the best, but it's far from the worst in the industry - though it should be noted that the figures above, because figures aren't published yet, are not representing the impaired year of 2022, when numbers went significantly lower, at least for the moment.

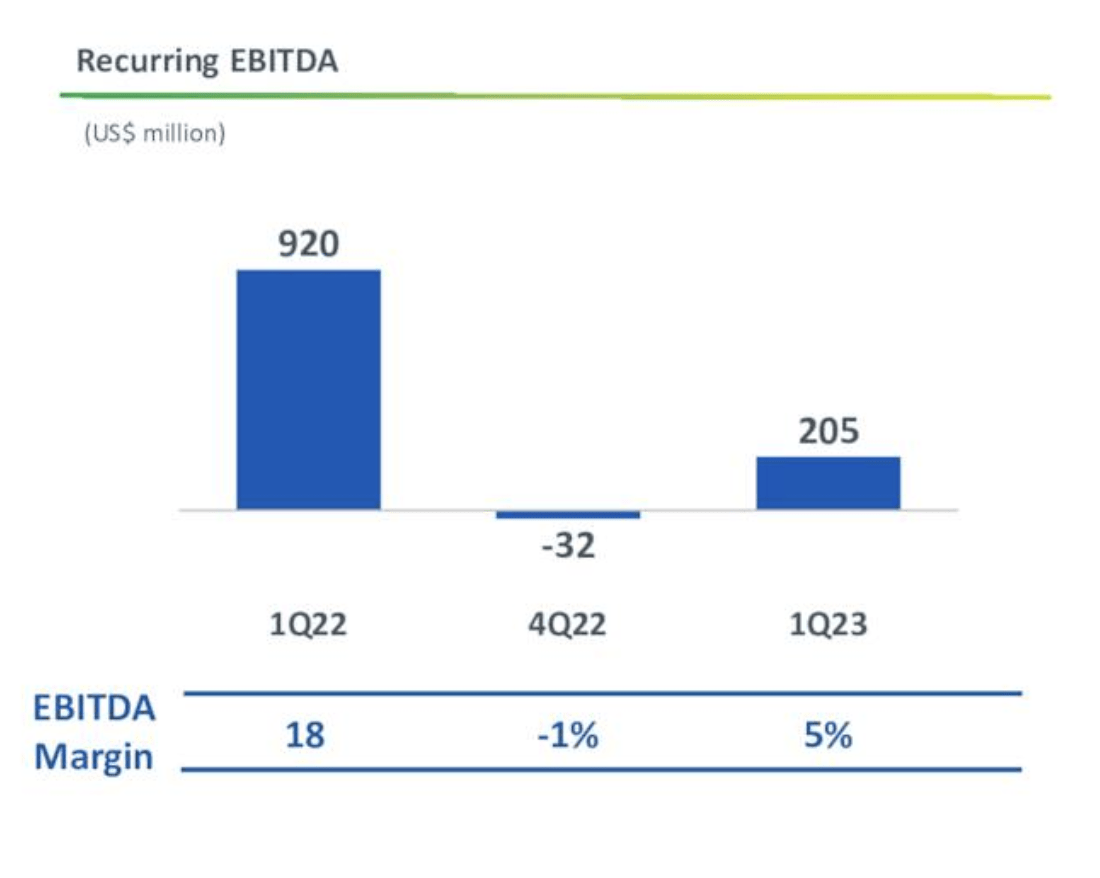

However, 1Q23 is showing some positive signals of recovery here. Braskem has increased the utilization rates of its assets across all regions on a QoQ basis, and this means higher sales volume. The company also isn't even close to unprofitable, coming in dozens of millions in net income for the quarter despite the difficulties we currently see. Company recurring EBITDA is recovering due to good demand recovery, with increased sales volumes in all segments.

{kind=link}

Spreads are higher, especially for the international market, which has had positive effects on margins in Brazil, Mexico, and other areas, Utilization is back above 75% - below high levels of 2021 where we could see over 85%, but back to 77% for the quarter. The increase in recurring EBITDA which has resulted in the positive growth is mostly due to the increased margin for the company's sales. Utilization in Europe is even higher, breaching 80% for both US and EU/EES

Alagoas remains a ball-and-chain around the company's ankle, but I've reviewed it previously and won't go deeply into it here, beyond saying that as of 1Q23, the company's mobility actions are in progress, with 3 of the 11 planned projects already in construction. The company has provisioned R$6.1B as of 1Q23, with total disbursements so far being at R$7.5B for the time being, and the relocation programs to residents are 99% executed as of March 2023, when the report was published.

The cost of debt, which might have been high on a comparative basis once upon a time, is starting to look fairly standard with the interest rate environment we are currently in. Braskem has an average cost of debt of 5.8%, and based on ROIC net of WACC, is actually still positive despite the recent pressures - at least, taken outside of the context of the current year.

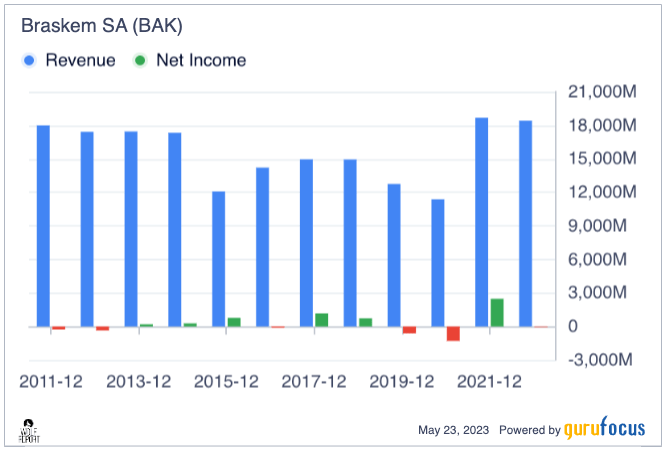

Braskem is neither the most stable nor the most solid/fundamentally qualitative chemical company. That is why my position is comparatively minor. I like the clarity of EU/US companies in this segment, which come at far less revenue/profit volatility. A quick glance historically tells us that the company's current situation is in no way unique.

Braskem Revenue/Net (GuruFocus)

{kind=link}

The company has no positive insider trends. Jim Simons, responsible for Renaissance Technologies LLC and managing a portfolio value of $75B, is a frequent buyer of Braskem shares. However, he also employs investment strategies that I do not, so one famous investor following and buying Braskem doesn't mean it's the right stock for you.

My investment case for Braskem is relatively simple. I see it as a volatile play on the recovery of the global petrochemical cycle . Due to significant underbuilding of PE/PP/PVC in the coming years, and postponements due to ESG, and due to COVID, the demand will, as forecasts currently show, outstrip capacity as early as 2024.

This will in turn allow companies like Braskem to dictate pricing. Just as my investments in the fertilizer industry over the past couple of years have vastly outperformed indices, I see a turning point in the supply/demand cycle that will turn positive for chemical companies either next year or at the very least in 2025.

Once this happens, Braskem will, as the thesis goes, trade higher and see a significant upside. That is what I am counting on. I have followed industry trends and do not see indications of capacity catching up. The current interest rate environment means that companies are sitting on their hands rather than investing large sums of money/capital into new projects. This can also be confirmed if you look at building companies, or the businesses supplying machinery and supplies.

Based on this, I see a non-trivial upside for Braskem in the next few years, and as things are looking now, the situation will be as critical on the excess demand side as it was on the excess supply side 2-3 years ago.

Let's look at the company valuation and see where this puts us.

Braskem Valuation - An upside does exist

Due to its significant volatility, Braskem isn't the easiest company to forecast and work with compared to almost any other chemical company in the segment. It gives all the appearance of being a textbook value trap, at least at this time - but this is too simplified a view. DCF valuations are not useful for a company with this amount of earnings and other volatility.

The business remains troubled, but if you take the time and look through what the company actually owns and operates, and the capacity it brings to market, it's hard to argue against the fact (as I see it) that there is an upside to be had here.

Despite appreciating 20%+ since my last article and now trading around $9.37, and the company's average valuation target actually seeing a decline since my last article when it was closer to $14/share, the company still has upside to the current average PT of $10-16.75 from 6 analysts, coming to an overall average of $12.4, or an upside of over 32% here. 4 out of 6 analysts following the company have either a "BUY" or an "outperform" rating on the company.

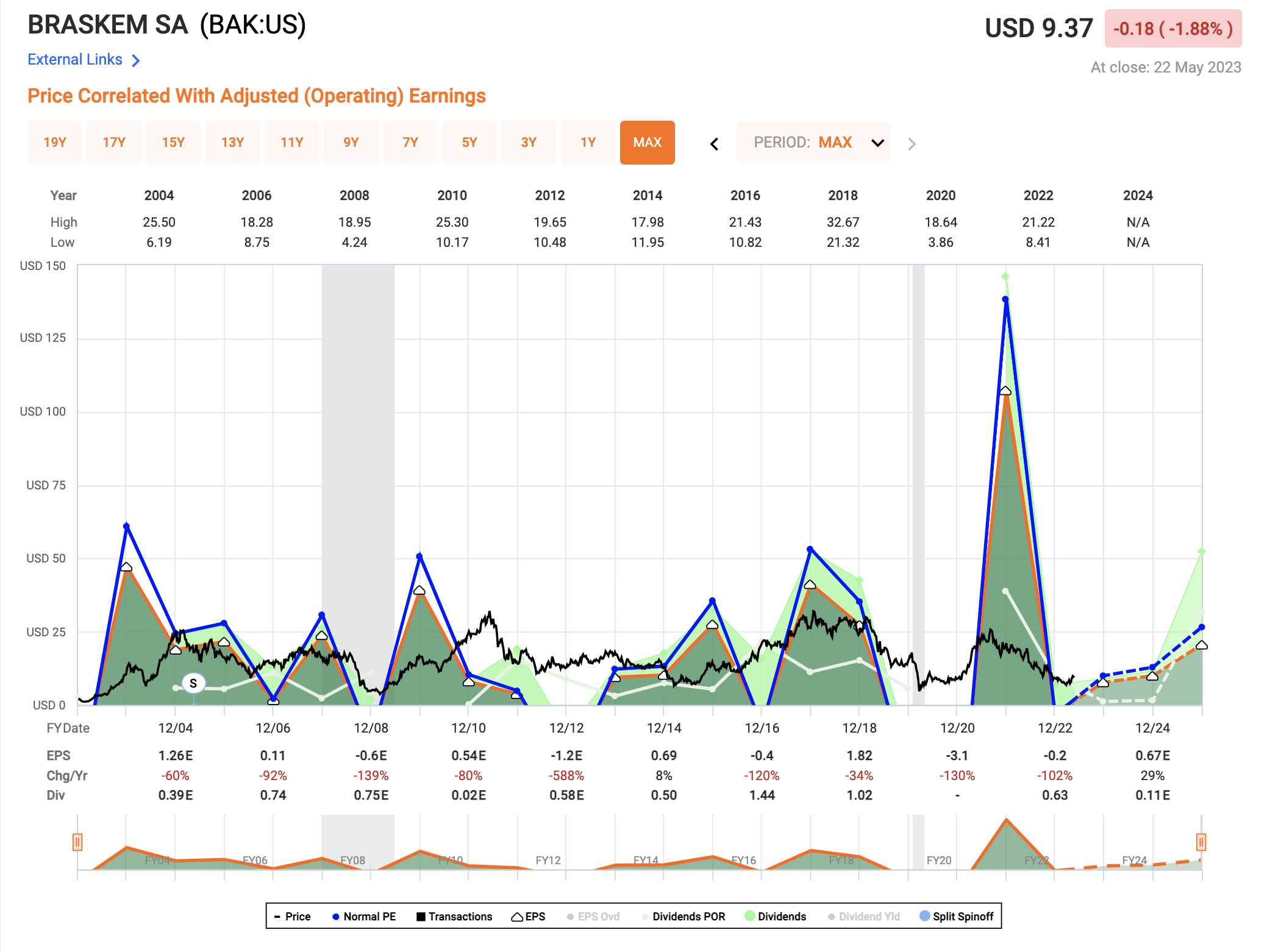

Forecasting how high or how low the company may go as a result of earnings is very difficult, illustrated by the following EPS trends here.

Braskem valuation (F.A.S.T graphs)

{kind=link}

The company can go as high as $30/share or above, but can also drop as low as below $5/share. Where it currently stands does not necessarily imply how high it may go in the future.

When I last reviewed the company, I applied a 10-20% discount to the company's NAV and forecasts based on spread trends, the company's somewhat worse fundamentals, and what peers we do have, reaching a PT of around $12/share. I'm still at that price target because I do not change my price targets lightly - and I would like to say that this price target, for the time being, has been the right choice. If I see further improvement in utilization rates and other fundamental indicators, I may raise it to $14-$15/share. In the event of full demand normalization and the scenario I described above, I would put the company worth $25/share, easily. But that is not where we are at this time, and I don't think we're likely to see this clearly for at least the next 6 months or so.

At this time, I remain cautiously optimistic about the prospect of this company, and I don't mind calling it a "Speculative BUY" here. As you can see, sometimes speculative "BUYs" can surprise you with how quickly they move up, though in this case, it was somewhat due to rumors of a takeover.

With regard to the takeover rumors, I would not move one way or the other based on them. I would not buy more Braskem simply because of them, nor would I sell at this price for the rumor's sake alone. I view the company as a longer-term play, a normalization of the entire petrochemical PP/PE/PVC cycle. This is a longer-term play, and this sort of rollercoaster demands that you sit still even when things change - if you're looking for that longer-term RoR, that is.

For that reason, this is my updated thesis on Braskem as of May 2023.

Thesis

- Braskem is an attractive company from a fundamental viewpoint, and it does have the potential of granting you some massive returns if bought at the trough and held to an upcycle. The recent 2021 is an excellent example.

- Based on this, it's a speculative "BUY" when it's cheap. While it can go lower from $10-12/share, I would say that at less than 0.6x revenues and lower-priced than almost every peer, I see it as a " Buy ".

- The company is undervalued here - though I want to really emphasize the speculative nature of the investment, and my initial position will likely be low to reflect this.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italics).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

While the company does fulfill all of my valuation-related criteria, it does not fulfill the dividend and conservatively-run criteria and therefore is a bit of a wildcard.

This one is for the most risk-tolerant investors. I have only a small position in the business.

For further details see:

Braskem: 22% RoR Since March, Still A 'Buy' After Q1 2023