BAK - Braskem: Fade The M&A Optimism

2023-05-24 16:27:20 ET

Summary

- Adnoc has made a bid for Braskem for a sizeable premium to its pre-announcement trading price.

- As attractive as the deal economics might seem, there are too many hurdles to overcome.

- With the stock still embedding deal optimism despite the deteriorating fundamentals, I would steer clear.

Braskem's ( BAK ) stock popped earlier this month following a material fact disclosure that its controlling shareholder Novonor (formerly Odebrecht) had received a non-binding proposal from the state-owned Abu Dhabi National Oil Company (Adnoc) to acquire a 100% stake in the company. It remains early days, though, and given Braskem's history of on-again/off-again acquisition attempts, I would avoid buying into the news pending more concrete details. Given Novonor's control (>50% of the voting capital of BAK), its reluctance to engage with Adnoc/Apollo, despite the big deal premium, makes a change of control outcome unlikely at this point. Further complicating matters are strategic changes at BAK's other significant shareholder, Petrobras ( PBR ), post-announcement of a new CEO, as well as uncertainties around minority shareholders' tag-along rights. So at this stage, it seems premature to underwrite a transaction premium. Instead, investors should focus on the earnings outlook, which remains weak against a cyclical downswing and deteriorating policy backdrop post-election.

A Braskem Sale is Back on the Table

Earlier this month, Adnoc presented an offer to controlling shareholder Novonor (~38% stake and >50% voting interest) to buy a 100% stake in Braskem for up to R$37.5bn. The headline R$47/share offer price would imply a 145% premium to the pre-announcement trading price of BRL19.2/share if confirmed. This isn't the first time a foreign strategic player has made an acquisition attempt - recall that in 2018, LyondellBasell ( LYB ) also launched an unsuccessful bid for Braskem (at a sizeable premium to today's market cap).

Per Novonor, the BRL47/share deal price is split across several tranches - a BRL20/share upfront cash payment, followed by BRL20/share and BRL7/share in 4% yielding perpetual debentures and warrants, respectively. Thus far, Petrobras and Novonor (combined >80% control) have refused to engage, citing that more than half of the offer is in the form of deferred payment structures, and thus, the net present value could meaningfully deviate from the BRL47/share headline offer. As a result, the stock has moved further below the BRL47/share offer price, though at BRL23/share, Braskem still trades at a >20% premium to pre-announcement levels.

The Case for Strategic Value Remains Valid, but Deal Hurdles are Significant

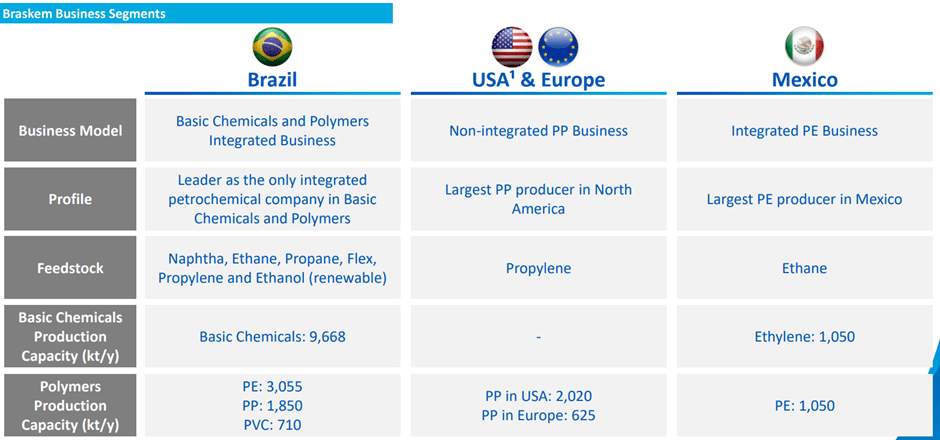

Braskem's strategic value has never been in doubt. The company remains the dominant player in Brazil, with >90% of the existing ethylene capacity. Perhaps more interestingly, Braskem also has a firm foothold in the global 'green ethylene' expansion (addressable market of $10bn by 2025 and $15bn by 2030), supported by its favorable cost structure and access to bioethanol. In an emerging market with an extensive chemical demand growth runway and where competitive dynamics have been relatively benign (limited new ethylene capacity additions over the last decades), Braskem also has compelling core earnings visibility. Outside of Brazil, the company maintains a strong presence, with a portfolio of international assets spanning Mexico (Idesa gas cracker) and the US and Europe (polypropylene), all of which have sustained strong capacity utilization through the cycles. Thus, Braskem's assets and know-how offer a relatively inexpensive way for major foreign strategic players to grow in chemicals and access new markets.

{kind=link}

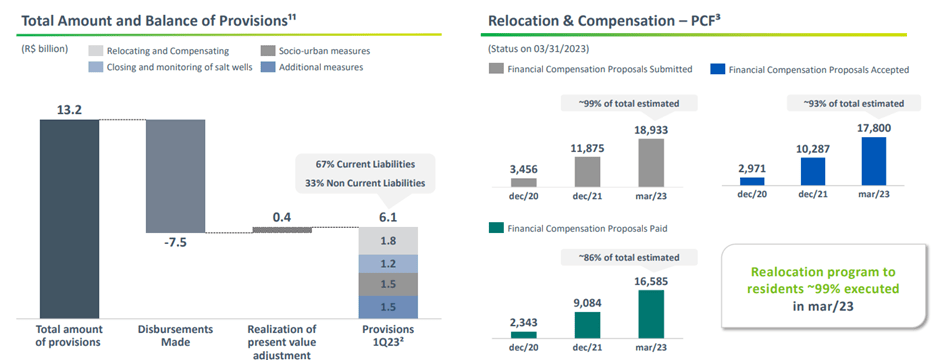

Yet, Braskem's market valuation has always been at the lower end of its peers - for a good reason. As LyondellBasell found in its 2018/2019 acquisition attempt, the roadblocks are significant. For one, the offer price has to clear not just Novonor and Petrobras but also the banks, since controlling shareholder Novonor's Braskem stake is pledged as collateral to creditors and cannot be sold without their approval. Also concerning is the Alagoas overhang (a result of environmental damage caused by Braskem's mining facility in the region), which has driven a steady increase in liabilities in recent years. As of Q1 2023, the provisions on the balance sheet amounted to BRL6bn, though there could be more escalations on the horizon, particularly with a recent ruling by the Alagoas State court blocking >BRL1.1bn of Braskem cash (equivalent to a high-single-digit percentage of the company's market cap). Few potential buyers would be comfortable taking on these liabilities.

{kind=link}

Minority shareholders should be particularly wary. While the latest rumors around a competing Petrobras offer (via an option to exercise its preemptive acquisition right) seemingly improve the risk/reward of a merger arbitrage trade, it isn't clear if minority shareholders will have tag-along rights. Even in the Adnoc acquisition scenario, Novonor's voting control (and economic control, together with Petrobras) means minorities have little say in the process. The Lula administration hasn't been market-friendly either, so a sub-optimal outcome for shareholders is a real possibility.

Fade the M&A Optimism

Adnoc's non-binding proposal for a 100% stake in Braskem (delivered to controlling shareholder Novonor) has put the stock in play. The only certainty, for now, is more volatility, however, given Braskem's history of on-again/off-again buyout plays in recent years. The market seems skeptical as well, with the stock price still well below the up to BRL47/share offer price and retreating further following Novonor's reluctance to engage with Adnoc/Apollo. The uncertainties around key shareholder Petrobras' strategy post-election and the appointment of a new CEO further weigh on a change of control outcome. The implications of a deal for minorities are also uncertain, particularly around their tag-along rights in different transaction scenarios. With the stock still well above pre-announcement levels, the valuation likely still embeds some deal premium following the disclosure, which exposes investors to the downside should the market re-focus on Braskem's deteriorating fundamentals.

For further details see:

Braskem: Fade The M&A Optimism