BAK - Braskem: Glad I Sold After A 27.8% Negative RoR

2023-11-08 21:00:18 ET

Summary

- I sold my position in Braskem after the involvement of Novonor and Petrobras in a recent deal.

- My strategy of selling and rotating at the right time has protected my profits and capital in the past.

- The article will provide an update on the negative return on investment for Braskem and discuss the implications for the investment thesis.

- I currently give the company no more than a "HOLD".

Dear readers/followers,

I'm going to be providing you with an update on Braskem ( BAK ) here. I've been covering the company for a few years at this point - being mostly positive with successful RoR, but went "HOLD" and sold my position after the involvement of Novonor and Petrobras in a recent deal. While the company certainly did not meet my initial long-term expectations, this is a good example of protecting your profits, your capital, and your returns by selling and rotating at the right time.

Does this sort of strategy always work?

No, not always - I would be hard-pressed to claim that it even works "Most" times, but I will say that it has prevented me from owning overvalued businesses, and for myself, a majority of the time, been able to avoid major losses by doing this.

So, in this article, I'm going to update you on the negative RoR we've been seeing for the company, and what this means for the thesis here. Take a look.

Seeking Alpha Braskem RoR (Seeking Alpha)

Does this mean that we should "BUY"? now?

Let's take a look.

Braskem - Selling was definitely the right choice

My bullish stance on Braskem lasted for quite a while, and when selling, I had a positive RoR. I already made it clear in my last article that I sold 50% of my holding at what turned out to be in retrospect a great price (Source: Braskem Article ).

The historical appeal to this company was the combination of a very sector-outperforming yield backed by very solid if volatile assets of the company. However, other players have seen the appeal of these assets as well - the latest of which has come into play is the Abu Dhabi National Oil Company. While certainly not the first player to try and put a price tag on Braskem's assets - not even the first in the last 5-6 years - it remains a question whether this deal could see any sort of traction. And based on what the share price has done since I sold the rest of my stake in the company, this is not a strategy I regret.

Because of the tag-along rights held by Petrobras ( PBR ), any player seeking to either put a price on or fully M&A Braskem is going to have trouble. The tag-along rights give Petrobras the right to participate in any sale of Braskem, and this detail has stopped at least one deal in the track. With the offer received to sell at R$37B, which represented (at one time, not anymore) , the rationale for this movement was solid - and I have no doubt that value in the company could have been unlocked.

But anyone doing deals in Brazil or in South America in general needs to be aware of the veritable regulatory quagmire that is one of the reasons deals in this geography involving outside parties often do not go through. A good example of this is the Brazilian Audit Court delaying any potential sale of Braskem due to the environmental involvement in the Alagoas environmental disaster, which means that any deal would likely have to provision for this.

I frankly wouldn't characterize the company's volatile M&A history as the problem - it's the Maceió liabilities that are the issues in this case.

Since my last article a few months back, some moving parts have changed in the deal. First of all, Apollo Global is out and it was this asset manager that ADNOC had joined in order to get 100% of Braskem. So that deal is off - according both to the Brazilian government and Petrobras wanting Apollo out of the deal ( Source ). Another thing that apparently was a core concern for Apollo global leaving, was the veto that Petrobras has. ( Source )

Instead, we now have a situation where ADNOC intends to buy the former Odebrecht stake, now Novonor, and establish a JV with Petrobras , which in turn would remain a near-majority partner at a 50% each in terms of stake. This is of course one way to go. The Brazilian state-owned company currently owns 36.1% of Braskem, with 47% of the capital with voting rights. The former Odebrecht has 50.1% of common shares and 38.3% of the company’s total capital.

This change simplifies the transaction quite a bit, because only ADNOC is left, and this source of JV is something that Petrobras actually preferred. Because Petrobras isn't handing over majority control, this is an easier sell in terms of not handing over strategic national assets to a foreign power - which ADNOC, as a state-owned company out of Abu Dhabi, certainly is.

Part of the recent decline in share price is certainly the ongoing uncertainty with regards to the deal, and Apollo exiting the deal, as we might see from the timing decline since September of this year.

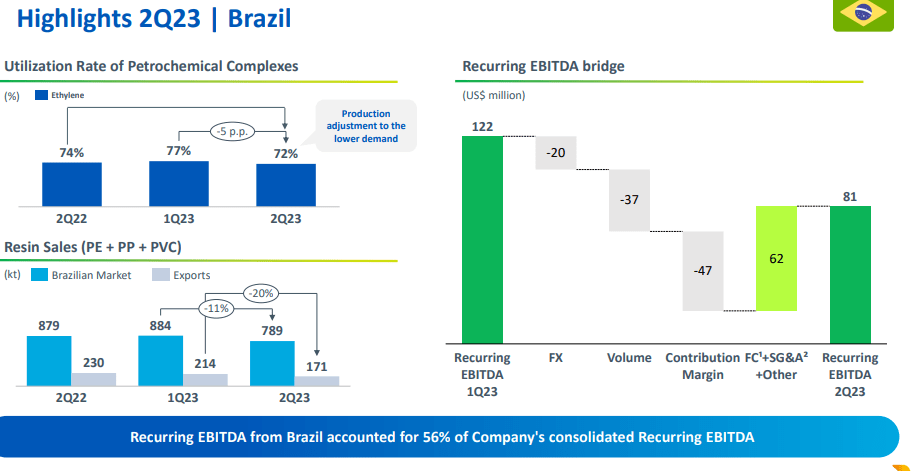

As I pointed out in my last article on Braskem, we're already at the beginning of a downcycle for energy, chemicals, and oil - but this does not take away what Braskem has been able to collect and prepare for during the upcycle. With a recurring EBITDA of over $135M, increases in utilization rates in assets, increases in sales volume, and other good KPIs, with a solid debt maturity profile of 13 years and a strong liquidity position, Braskem has a lot going for it.

The results, with decreases in sales volume in chemicals and resins and decreasing spreads, is more a function of a macro than anything else. Utilization and sales remained at impressive levels despite these levels.

{kind=link}

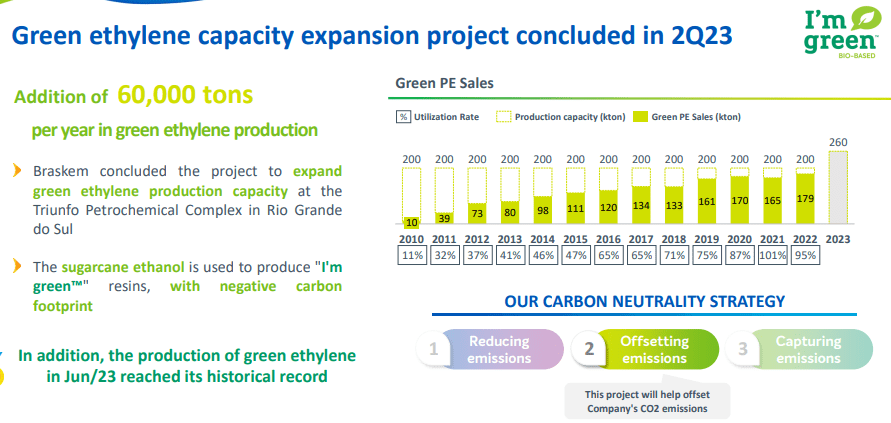

The company is also using its considerable cash and liquidity to expand its capacity, adding a net capacity of 60,000 tons of green ethylene per year. This needs to be seen in context, meaning just how good and how much the utilization rates have actually improved in less than 15 years.

{kind=link}

if something positive can be said for one of the more serious environmental and geological events in recent history in Brazil, it's that Braskem has really pushed forward in terms of its reparations and compensation proposals. The company has submitted 99% of all active proposals, with an acceptance rate of 99.4% and 90% paid. This gives, I would say, a very good visibility of the future cost of the risk here. The relocation program is at 99% execution until June this year. Still, R$6.5B in provisions still remain.

3Q23 production and sales numbers, which are numbers that we actually have, mirror the continued downturn in global demand for chemicals. The industrial slowdown is ongoing. The company also saw some production volume declines in both Mexico and Brazil due to external factors (Source: 3Q23 Braskem ).

Unfortunately, the utilization rate in key segments is down, now below the 70% level compared to 79% in 3Q22. This is the company adjusting its petrochemical crackers to the global demand, as well as some unscheduled outages due to power outages in certain regions, as well as some operational instabilities. Whenever you invest in geographies like these, these are risks that you need to be aware of - things that can indeed happen.

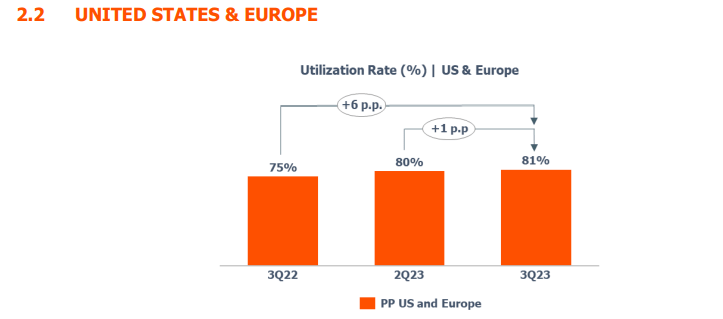

Green Ethylene is thankfully increasing, with the ramp-up of production as well as expansion, with demand not being as bad as in other parts of the business. The US and EU segments saw similar trends, an actual increase in 3Q23 utilization in the company's PP plants - though some reason for the increase was also lower utilization in the last quarter due to maintenance.

{kind=link}

Sales performance somewhat reversed, at least in resin, due to good seasonality and in core markets such as Brazil. Trends were good across multiple consumer goods sectors, civil construction, sanitation, and others.

I don't expect further improvements in utilization rates unless it's for the segments that have seen a decline here. Spreads will remain the same - not much the company can do to influence macro. But Braskem does not need to influence macro - it just needs to ride the wave of petrochemical demand and cycles for it to continue at a relatively attractive trend.

Volatility continues to be Braskem's main issue. As I see it, Braskem is only interesting as an investment if you can procure shares at a very attractive valuation in the right portion of the cycle, to take advantage of upswings and yields. This is not a company I would aim at holding for 10-25 years - as I made clear in my last article, by selling the company's shares first around the time of that piece, and the remainder before it crashed further when it became clear that the deal rationale was worsening.

Let's update my valuation here.

Braskem's Valuation - we're cycling down, and earnings are going negative.

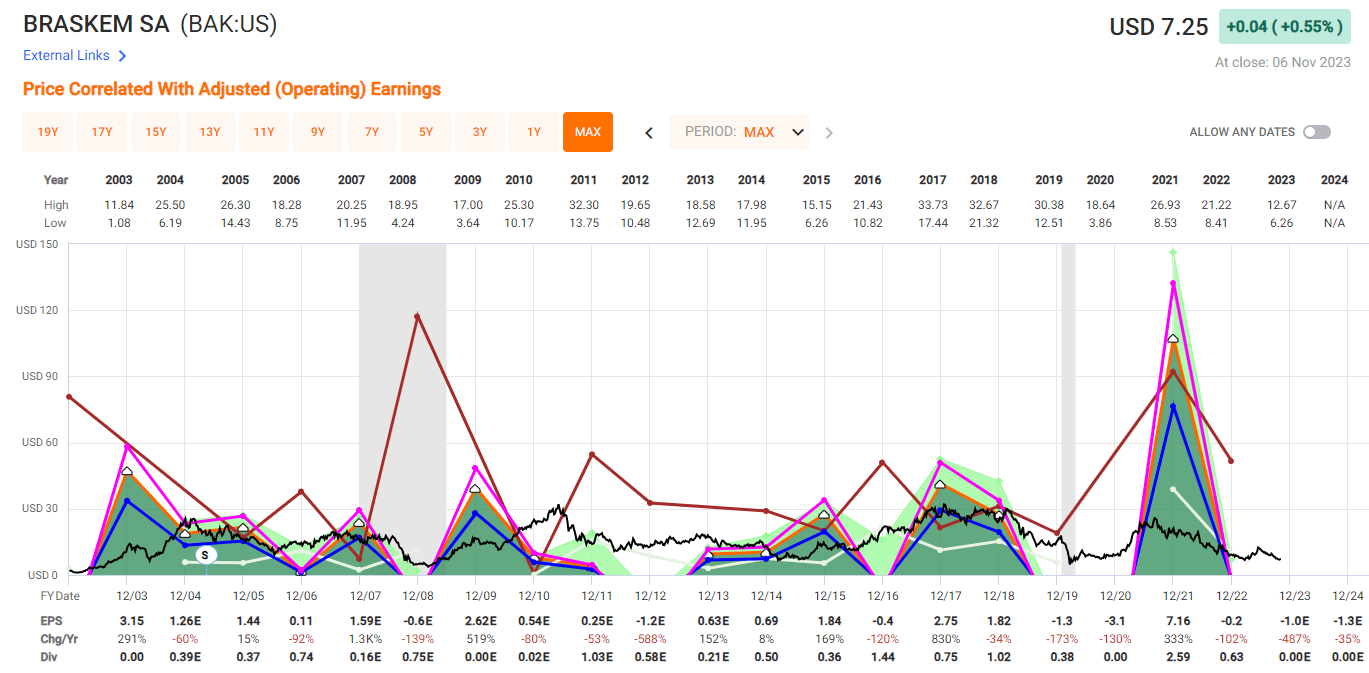

{kind=link}

As you can see above, I hope it illustrates my rationale for being careful with this company. While $7.25/share isn't a bad price for this company, and based on my previous PT could be considered a "BUY", this is not a stance I hold with an expected earnings downtrend resulting in a negative adjusted EPS and a zero dividend for the 2023E Fiscal.

I'm changing my PT to $7.1/share here.

The reason? Simple - current fundamentals and outlook in an undervalued market. Negative 11.93% EPS yield, a negative P/E given the current earnings estimates, and a current set of estimates - likely ones given FX, given demand, and given macro - that are likely to remain negative in 2024E as well. I am not the only analyst forecasting this - S&P Global forecasts are for the negatives to continue into 2024E as well, and not go back into positive until 2025E (Source: Braskem Forecasts, S&P Global).

The current average for the expectations, translated in FX to the BAK ticker, is around $6.36 from a low of around $4 to a high of around $14/share. Only 2 analysts are currently at a "BUY", with most either at "HOLD" or "SELL". Based on the company's trends and forecasts, I would not go higher than a $7.1/share, which represents around 1.8x to BV and around 0.2x to forward sales. More than that, given what else is available on the market, is not something I'd accept here.

My thesis, as of November 2023, is as follows.

Thesis

- Braskem is an attractive company from a fundamental viewpoint, and it does have the potential of granting you some massive returns if bought at the trough and held to an upcycle. The recent 2021 is an excellent example.

- Based on this, it's a speculative "BUY" when it's cheap. But I want to, in this case, buy it at a $7.1/share PT for the downcycle given the current deal uncertainty we're facing. This price represents the highest I would be willing to pay here.

- Due to the complications from the M&A coupled with current trends in petrochemicals, I expect the company to actually move slightly to the negative in 2023. There are better alternatives available than Braskem here.

- I give the company a PT of $7.1/share, and maintain a "HOLD". I don't believe Petrobras is likely to accept a sale of Braskem easily, and if it does (which seems likely here), the eventual shareholder outcome and upside is unclear.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italics).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I still consider the company to be a conservative "HOLD", due to neither being cheap nor having a good upside in the medium term. The dividend is also very unsafe at this time, and the prospects here with the potential deal are uncertain.

For further details see:

Braskem: Glad I Sold After A 27.8% Negative RoR