BAK - Braskem: It's Time To Be Careful After The M&A (Rating Downgrade)

2023-08-04 03:26:01 ET

Summary

- Braskem's M&A deal has raised questions about the future of the company and its appeal to shareholders.

- The involvement of Novonor and Petrobras in the deal adds uncertainty and regulatory challenges.

- The company's valuation is low for a reason, with political and shareholder risks contributing to its volatility.

Dear readers/followers,

I've previously been a bullish analyst on Braskem ( BAK ), seeing the company as undervalued, if significantly volatile of a play to at least look at. I also have a small investment in the business which I now have held for a number of months, and this investment is in a positive RoR situation here.

However, since my last article, we have some significant news to take into consideration with regard to if we want to keep owning our shares, or if it's time to divest this investment and rotate the capital into something more attractive. Remember, the market is full of opportunities for investing and making money. Being "loyal" to a company or an investment here, as some investors are or have been wanting to do (including me at times), makes no sense in this context.

So let's see why Braskem may be a company to start avoiding until we get more overall clarity.

Braskem - The M&A, while positive, has muddled what to expect from the business

After a significant, sudden short-term burst in share price, where I sold 50% of my holding at a rotation RoR of over 25%, we've started to get some more clarity as to what this development could mean to current shareholders of Braskem.

Braskem's appeal was the combination of extremely high yield at the price of volatility but backed by very strong assets. The current offer by the Abu Dhabi National Oil Company may put the foundations of this investment thesis into question.

It's important to point out that this is hardly the first time someone has put a price tag on Braskem and shown interest in purchasing the company. LyondellBasell (LYB), another company I own, tried the same strategy back in -18 but failed. Based on this volatility - which is also the reason I sold at the news - I would be careful about any takeaways where you make Braskem either attractive or not attractive on this piece of news alone.

As I mentioned in my first article on Braskem, the company is actually majority-controlled by Novonor. Because Novonor isn't actually all that interested in the deal in its current form, this means any positive outcome seems dubious at this point - and Novonor is not the only interested transactional party here. Despite not being a majority shareholder, Petrobras ( PBR ) is part of this deal, and any confirmation from even them seems dubious here. Why? BEcause despite not being a majority shareholder, Petrobras has the right to purchase the stake from Novonor. Why?

Because the company has so-called tag-along rights. This entitles Petrobras to participate in the sale, and also due to other legalities, has the right to purchase the entire stake and become the majority shareholder.

For that reason, I'm sticking to the basics. Braskem has received an offer to sell at upwards of R$37B. This represents a significant transaction premium to the share price both at the time and at current levels. The rationale for any sort of deal for the company here is solid. Value could be unlocked, and shareholders could indeed walk away happy. That Braskem has synergistic and portfolio-related value has never been in question.

The questions and problems have been regulatory and specific in nature. So, are they now appearing once again. The latest slamming piece of news came in the form of the Brazilian Audit Court will delay any sale in the company due to its involvement in the Alagoas state environmental disaster, which has been one of the more prominent pieces of my coverage of the company. Any deal would likely require above-and-beyond provisioning for such payouts, requiring new calculations for the salt extraction project. A herculean task, and not easily finished. This is also the reason why Braskem has scared off other potential suitors to the company. The exposure to these liabilities is non-trivial and likely will need to be completely settled before any M&A is allowed to go through. The notion that this in any way is currently "done" is not likely either.

I frankly wouldn't characterize the company's volatile M&A history as the problem - it's the Maceió liabilities that are the issues in this case. And I do not see a way to make this easily calculable under current circumstances, which puts the entire deal rationale into question.

Don't get me wrong. I'd love to sell my Braskem stock to Abu Dhabi National at a significant premium. I just don't think they'll get to buy it as easily as they think.

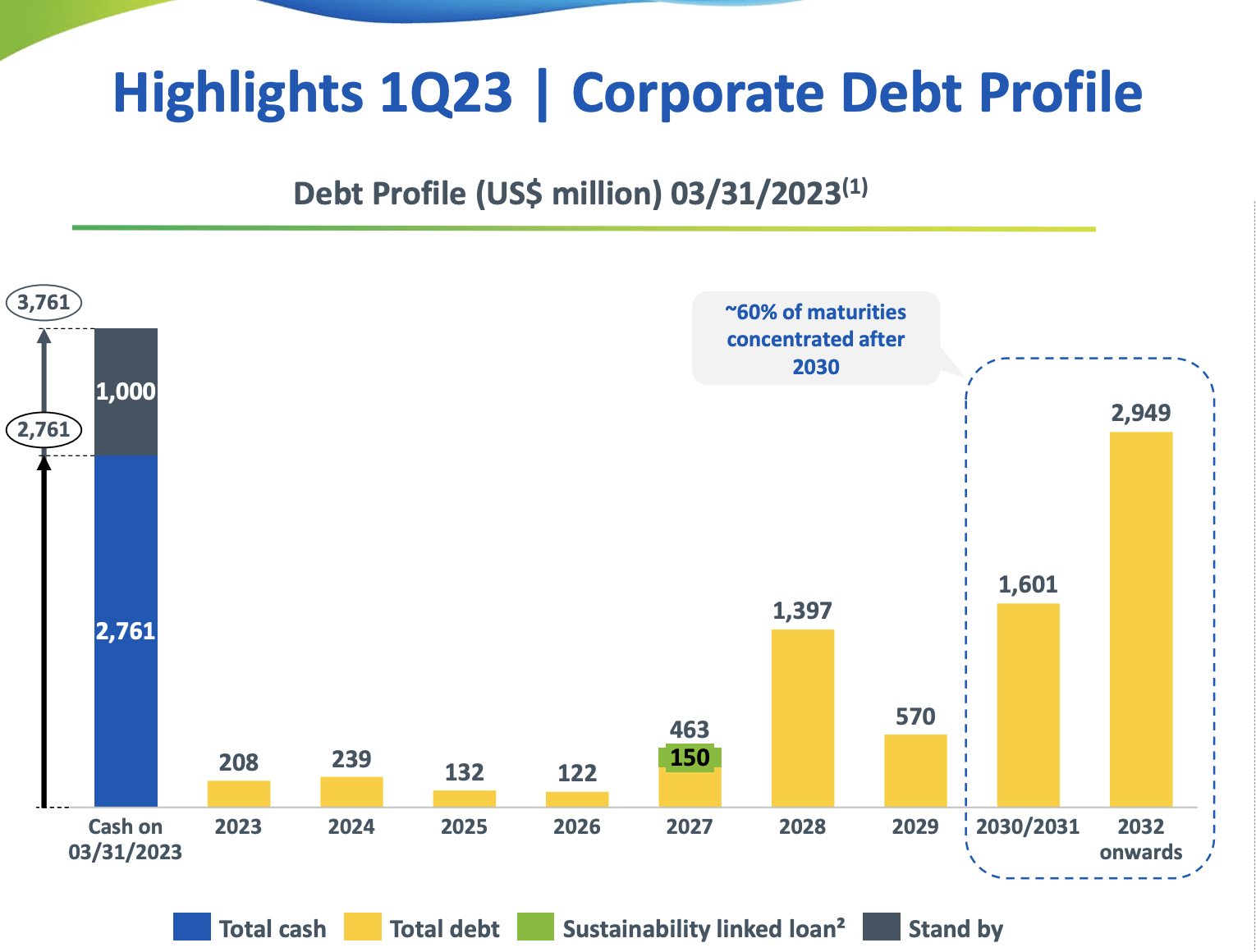

For that reason, focus on the actual Braskem future instead, and this future is looking somewhat dubious. Regardless of near-term Braskem results, the company's correlation is to commodities such as oil and other chemicals. The company's current positives, including a very solid liquidity position, good debt maturity, and leverage of 3.86x on the corporate side, aren't impacted by this.

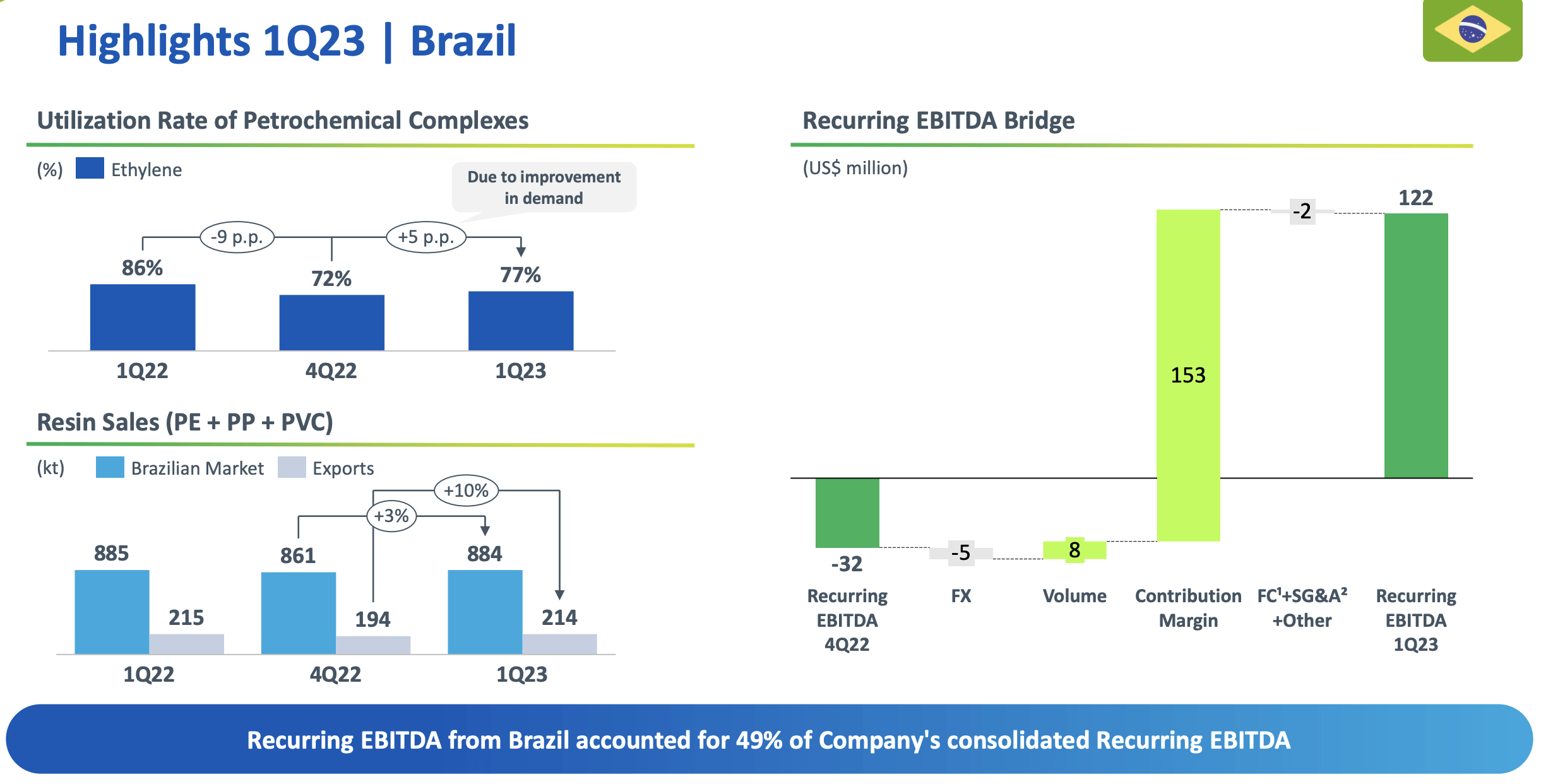

Demand is likely to continue to improve, cementing some of the trends we've seen over the past few quarters.

{kind=link}

The same improvements are, by the way, true for Europe. Average utilization was up to above 80% again for PP in Europe, and sales were up 1% as well. This includes the USA as well. What continues to weigh heavily on the company is the Alagoas event. The interest paid this last quarter may look grim - but R$1B+ is a typical concentration of semiannual interest payments. The company's debt profile remains an overall positive one.

{kind=link}

The company is moving forward with several initiatives set to improve both cash flow and costs, with many of them already seeing positive impacts on the company's annual EBITDA. This includes optimizations of global commercial management, fixed cost management, and digital integrations, improving working capital management, CapEx, and non-recurring monetizations.

I have an overall positive view of the entire Global PE and PP as well as the PVC industry. This has to do with the fact that there has been a significant underinvestment in new capacity on a global scale, which has left demand higher than potential supply, in the event of even close to the trends we're expecting here. It's understandable why 2023E is expected to be less than ideal - we're still in a situation where supply is much higher than demand, with many expecting a recession. But when this cycles around, there will be insufficient capacity to meet the petrochemical/chemical demand that Braskem works with.

I expect this to be a huge part of the deal rationale for the M&A. I expect the utilization rate for the company's assets to improve in both USA and Europe (brazil is already high) for 2Q, I also expect sales volume increases across the board due to higher product availability. Spreads will remain the same - not much the company can do to influence macro. But Braskem does not need to influence macro - it just needs to ride the wave of petrochemical demand and cycles for it to continue at a relatively attractive trend.

The problem is volatility here. As I see it, Braskem is only interesting as an investment if you can procure shares at a very attractive valuation in the right portion of the cycle, to take advantage of upswings and yields. This is not a company I would aim at holding for 10-25 years.

The valuation is the problem.

Braskem - The valuation is low for a reason

Braskem has "always" been volatile. And there are several reasons why the company typically is very cheap. Any peer that you decide to compare Braskem to comes not with close-to complications, political risks, asset risks, and shareholder risks. The fact that Petrobras is a minority stakeholder who, at will given their governmental status, can take over, is a non-trivial risk and fact that needs to be considered. The fact is, Petrobras could make a competing offer via its option of being the first rightful party to acquire the company. To say that Brazil is politically volatile is an understatement, and the current regime in power is hardly known to be friendly toward the forces of capitalism.

I have been reviewing all my Brazilian holdings exactly due to this. Even with the valuation trends that I am showing you here, and regardless of how things go in 2Q, the company's risk ratio has increased. It's no longer even as comparatively stable as I once considered it.

Remember, buying the company at most times , has guaranteed you sub-par returns.

{kind=link}

You have to be willing to "trade", if you're entering this investment. Recognize significant troughs, likely to be followed by significant highs when the cycle shifts.

There is no accuracy to be found here. FactSet analysts have a hit ratio on a 10-year basis with a 10% MoE of exactly 0%.

The company either beats or misses the overall targets which means that any safety here can usually be considered an illusion. We can consider trends positive, and we can state that the company seems likely to perform well in a good market situation, but as to timing and levels of highs and lows, that's a different story.

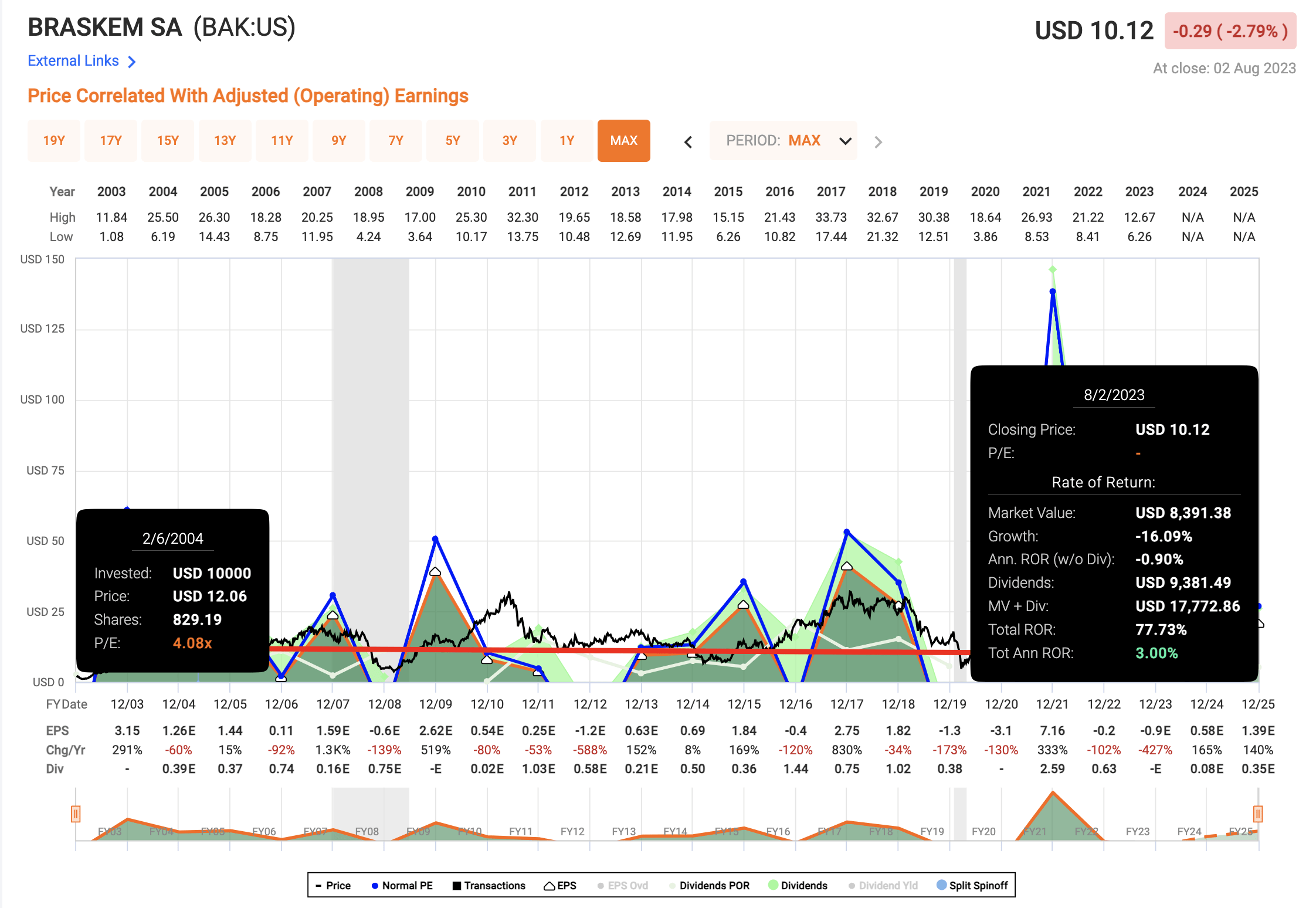

My small position came at a very attractive cost basis. I sold 50% at the highs. my previous PT for the business was around $12/share. That's why I sold when it started going above this.

This current M&A uncertainty is not necessarily a net positive to me, and has the potential of throwing a wrench into the medium-term potential returns. We need to remember that Petrobras has stated with clarity, that it does not believe sales discussions of Braskem are over ( Source ). And Petrobras does "hold the keys" to Braskem, so to speak.

An increase in overall risk and volatility in an already volatile business is not something I view as appealing. While working concrete price targets in this business is extremely hard, I believe the combination of:

- A 2023 trough in petrochemical spreads and demand/supply.

- Continued M&A uncertainty, made worse by the current political situation in Brazil.

will actually lower the share price below $10/share once again.

So for the short term, I'm lowering my PT to below $10/share, and going "HOLD" here.

Thesis

- Braskem is an attractive company from a fundamental viewpoint, and it does have the potential of granting you some massive returns if bought at the trough and held to an upcycle. The recent 2021 is an excellent example.

- Based on this, it's a speculative "BUY" when it's cheap. While it can go lower from $10-12/share.

- Due to the complications from the M&A coupled with current trends in petrochemicals, I expect the company to actually move slightly to the negative in 2023. There are better alternatives available than Braskem here.

- I give the company a PT of $10/share, and move to a "HOLD". I don't believe Petrobras is likely to accept a sale of Braskem easily.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italics).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I now consider the company to be a conservative hold, due to neither being cheap nor having a good upside in the medium term.

For further details see:

Braskem: It's Time To Be Careful After The M&A (Rating Downgrade)