BRZE - Braze: Improving Financials But Concerning Operational Costs

2023-12-16 02:19:45 ET

Summary

- Braze beats EPS and revenue expectations in Q3 2024, improving its forecast for FY 2024.

- Concerns remain about the company's high negative operating margin and operational challenges.

- The high short interest and lack of profitability caution against an overly bullish outlook.

Braze, Inc. (BRZE) released its Q3 2024 , beating EPS and revenue expectations and improving its top and bottom line results YoY. In my previous article, my concern was the company's lack of profitability. It has improved its EPS guidance for FY2024 by roughly $0.10, which is impressive. However, the forecasted loss is still between $0.26 and $0.27. One of the significant concerns remains the company's high negative operating margin. Losses from operations have increased over the last nine months, which I believe is due to the complexity of managing and operating its diverse multi-channel marketing solutions. Furthermore, we should be cautious of the high short interest signalling negative market sentiment at 9.34%. Therefore, I maintain a wait-and-see hold rating.

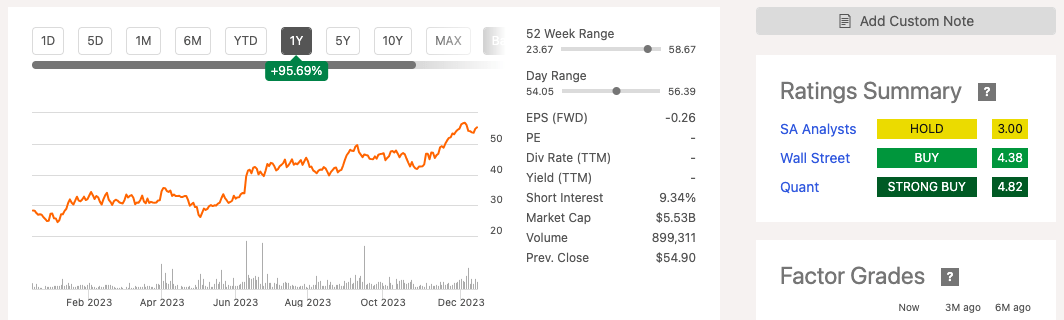

One year stock trend (SeekingAlpha.com)

{kind=link}

Q3 2024 company updates and concerns

In a previous article , I provided an overview of Braze, a company that has demonstrated improvements in its financial performance, particularly in top and bottom-line figures. However, there are certain concerns that warrant caution from investors. Braze stands out from its competitors by utilising a diverse cross-channel marketing approach, which is highly appealing to customers. However, this broad scope of services presents operational challenges that are impacting the company's income potential.

Braze solutions and customers (Braze.com)

{kind=link}

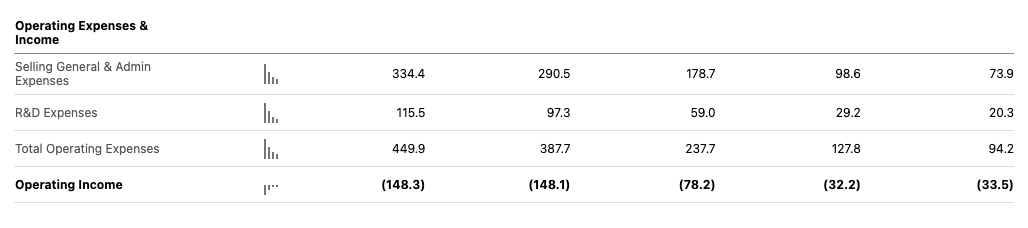

As Braze expands its solutions and customer base, it faces mounting operational complexities and escalating costs. These expenses have grown, currently reflecting total operating expenses of $449.9 million TTM. Despite attempts to streamline processes and reduce costs, the company's operational income remains worrisome.

Annual operational income (SeekingAlpha.com)

{kind=link}

Moreover, managing multiple marketing channels at scale risks stretching resources and hampering innovation. This could significantly slow Braze's responsiveness to market demands and stifle its ability to introduce cutting-edge features in a quick paced and competitive environment. Complicating matters further, Braze operates in an industry heavily reliant on customer budgets. During economic uncertainty, advertising budgets are often cut, posing a risk to Braze's anticipated growth.

Financial updates

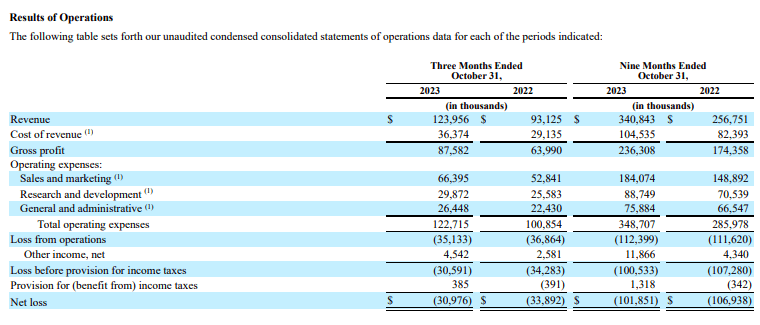

The company reported strong Q3 2024 earnings, beating EPS and revenue expectations and improving its forecast for FY 2024. The revised projections suggest a Q4 revenue of $124 million to $125 million and fiscal 2024 revenue ranging from $465 million to $466 million. Additionally, their fiscal Q4 non-GAAP diluted net loss is expected to be between $0.04 and $0.05, resulting in a full-year fiscal 2024 net loss of $0.26 to $0.27. Notably, these losses have improved significantly compared to the earlier forecast on September 7th, where the projected net loss for fiscal 2024 was $0.37 to $0.39. The company's net losses have shown a considerable improvement, narrowing down to a negative $30.9 million. However, we can see that over the last nine months, loss from operations increased YoY.

Q3 2023 versus Q3 2022 (Sec.gov)

{kind=link}

The company has a positive levered free cash flow of $70.87 million TTM. This has been upward trending and good to see as the company can reward investors, reinvest into the business and pay off debts. If we look at the company's liquidity it has a healthy quick ratio of 2.19 indicating that it can cover its short term liabilities.

Valuation

Given the current market performance and recent Q3 2024 results, Braze's trajectory seems bullish, reflecting in the stock's significant uptrend of 95.69% over the past year and a commendable 21.24% increase in the last three months. The stock is still trading below its average target price of $68.47 , indicating that it may be undervalued.

Target price increase post Q3 2023 (Marketscreener.com)

However, despite these positive trends, my concerns linger. The increased price targets from various analysts post-Q3 could be overly optimistic, especially considering the continuous decline in operational income, dampening profitability and worsening over the recent years. Additionally, the high short interest of 9.34% raises red flags regarding negative market sentiment. Furthermore, the company has yet to deliver positive EPS results and will not do so this year. While Braze's improved EPS guidance is a positive sign, the underlying operational challenges in a competitive market and sentiment caution me against an overly bullish outlook.

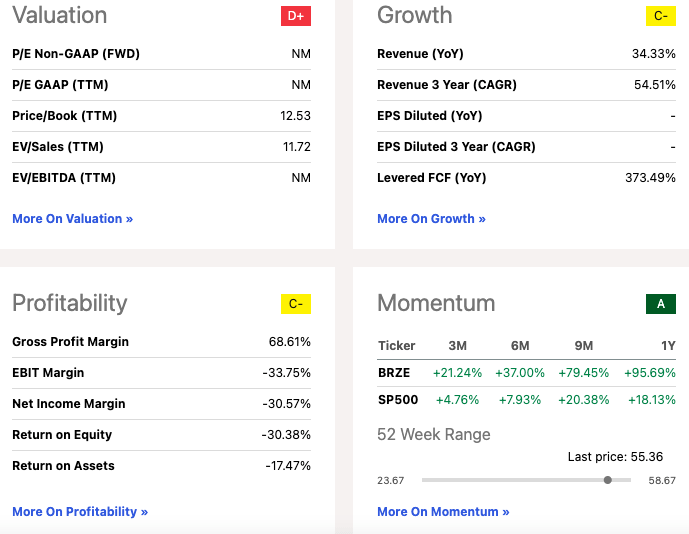

Quant grading (SeekingAlpha.com)

{kind=link}

Risks

There are some risks that investors should be aware of. Firstly, Braze is still a loss-making company. There are alternatives in the same market that are profitable. Furthermore, the company's growth depends on market conditions as these will determine the type of advertising budgets their customers will have. In downturn markets, budgets are more likely to be cut and would, therefore, negatively impact the growth performance. Another concern is the competitive landscape and sales strategy. Braze competes against diverse strategies and product offerings. Falling behind in innovation or failing to differentiate themselves could lead to losing market share against competitors adapting swiftly. Lastly, there's a risk related to customer relationships. Braze heavily relies on retaining customers, and any misstep in delivering results or over-dependence on a few large clients could impact its financial performance.

Final thoughts

Q3 2024 witnessed Braze topping EPS and revenue forecasts, hinting at an upward trajectory in their financials. Yet, my concerns persist. While their EPS guidance improvement is noteworthy, the estimated loss between $0.26 and $0.27 and the continuing negative operating margin at 28% are concerning. Braze's efforts to expand its solutions and client base have improved the top line; however, ideally, I would like to see an improvement in operation costs before taking a bullish stance. Therefore, I maintain a wait-and-see hold rating.

For further details see:

Braze: Improving Financials But Concerning Operational Costs