BRZE - Braze: Remarkable Growth But Fairly Valued

2023-12-23 00:29:37 ET

Summary

- Braze is a CRM solution that helps businesses analyze customer spending patterns and implement effective marketing strategies.

- Braze has experienced consistent revenue growth since its IPO, with an expanding customer base and increased utilization by existing customers.

- While Braze's value proposition is strong, I perceive other high-growth opportunities in the market that present more favorable valuations at present.

Intro

??Braze (BRZE) serves as a customer relationship management ((CRM)) solution, focusing on scrutinizing customer spending patterns and experimenting with fresh marketing strategies. Following its IPO on November 17, 2021 , starting at $65 per share, the stock soared to $96.65 the subsequent day, but has steadily declined since then, hitting a low of $22.53 on November 7, 2022.

Braze has showcased an extraordinary revenue surge, escalating by an impressive 350% from 2019 to the trailing twelve months ((TTM)) and marking an additional growth of nearly 85% since its 2021 IPO. Despite this remarkable advancement, the current stock price stands at $54.09, reflecting a decrease of 17% from its IPO. However, this price point appears to mirror a fair valuation. Therefore, my current recommendation for investors is to maintain a HOLD stance.

How Braze Works

As previously stated, Braze functions as a CRM tool, enabling users to:

-

Identify target customers by leveraging available data.

-

Develop novel marketing campaigns.

-

Perform A/B testing for campaign optimization.

-

Forecast customer responses to the devised campaigns.

-

Produce comprehensive reports derived from campaign outcomes.

Braze In App Looks (Screenshot of Braze App)

{kind=link}

Here are some standout features offered by Braze:

Blue : Seamlessly link Braze to internal data warehouses (like AWS, Azure, GCP-think Big Data) and generate detailed reports.

Red : Craft engaging campaigns and interact with users through functionalities like push notifications.

Green : Tailor campaigns to specific target audiences based on preferences and behaviors.

Orange : Gauge the potential reach of your campaigns, providing insights into their anticipated impact.

Braze's primary value lies in precisely targeting a wider customer base. Through Braze, companies can better engage their target audience by designing tailored campaigns and testing them on a smaller scale before launching to a larger audience. This approach streamlines effectiveness while concurrently reducing costs. Essentially, Braze facilitates reaching the right audience in the right way, all the while saving money. To avoid cluttering this article, here is a link to some specific examples showcasing what users can do using Braze.

After reviewing analyses from other analysts, I hold a contrasting perspective on the notion that economic downturns and budget reductions automatically lead to decreased usage of Braze. Let me explain why:

Firstly, the use of software like Braze isn't tied to advertising budgets but rather falls under the software budget category. This distinction is crucial as it separates Braze's utilization from direct advertising expenses.

More significantly, Braze isn't just a marketing tool-it's a money-saving mechanism. Efficiency is key here. Braze empowers companies to optimize their expenditures by pinpointing specific audience targets, enabling Braze users to efficiently connect with more of their own customers. Interestingly, during periods of economic recession, Braze becomes even more advantageous. It acts as a tailwind by conserving customers' funds that might have been squandered inefficiently otherwise.

Revenue and Business Trend

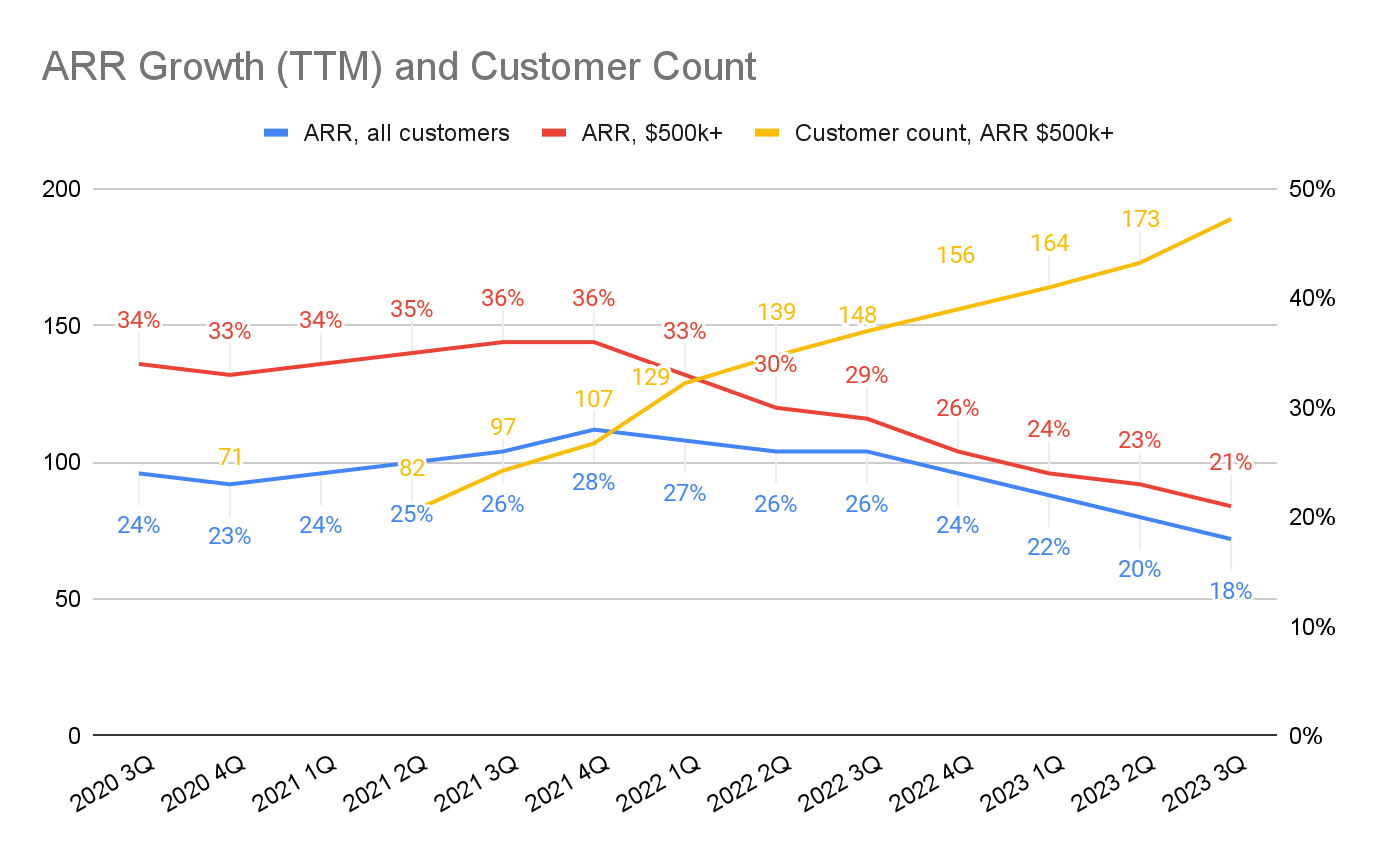

Braze Annual Recurring Revenue Growth and Customer Count (Company SEC Filings)

{kind=link}

Since its IPO, the company has consistently witnessed growth in its top line figures every quarter. This uptick is credited to an expanding customer base and increased utilization of the software by existing customers. What's particularly noteworthy is the amplified spending among larger clients over the trailing twelve months ((TTM)) in comparison to the overall customer cohort.

Although there might be concerns among investors regarding the decline in Annual Recurring Revenue ((ARR)) growth, this decrease is likely influenced by the substantial growth in total revenues. With larger revenues, the same value of increase leads to a lower percentage change.

Moreover, it's essential to recognize the stickiness inherent in enterprise software like Braze. Integrating one's data infrastructure with Braze involves considerable effort, making the software challenging to replace. If a company were to cease using Braze, they'd need to redo the same extensive integration work, which serves as a significant deterrent to switching platforms.

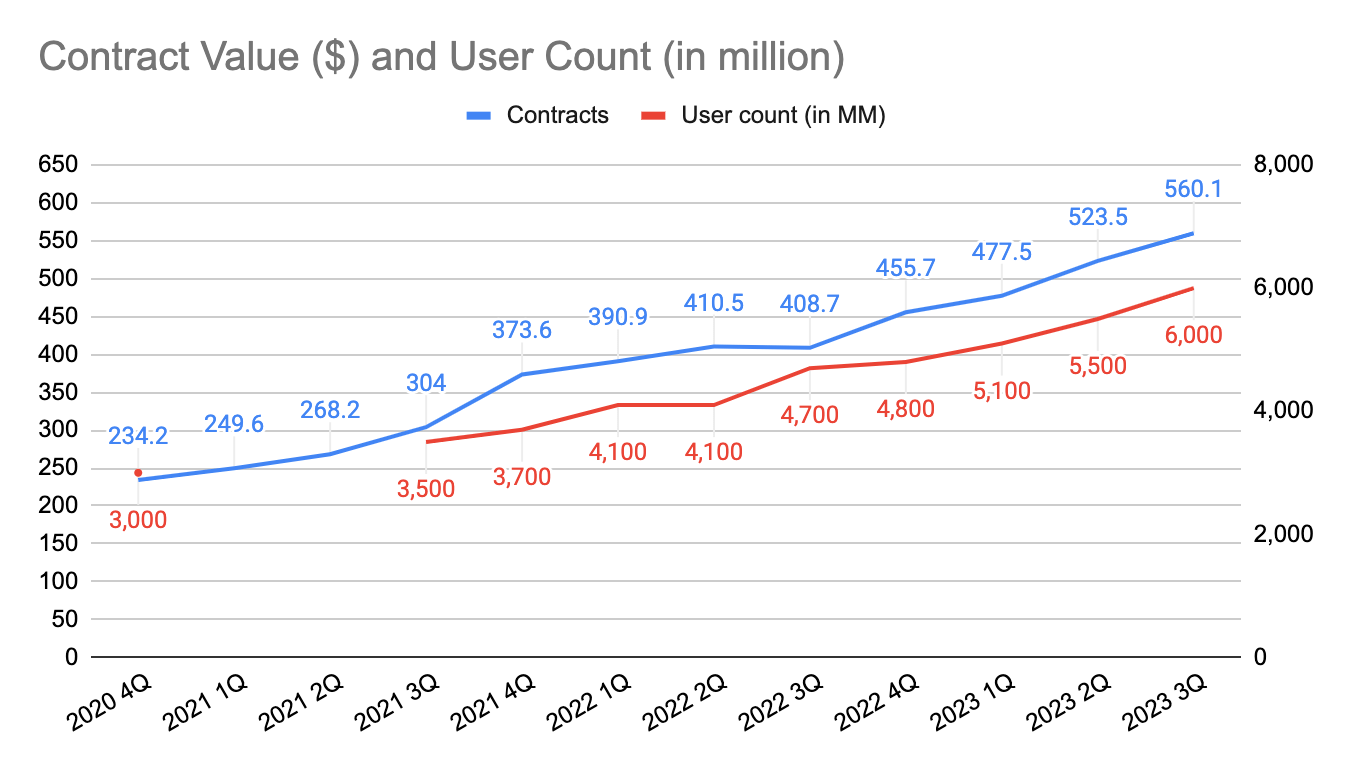

Braze Contract Values and User Count (Company SEC Filings)

{kind=link}

Please be aware that certain data points are absent due to the recent IPO, resulting in sporadic information availability.

Recognizing Braze as a mutually beneficial solution, customers are increasingly investing in future payments to the platform, expanding their ability to connect with a broader user base . From 4Q2020, there has been a twofold surge in user count, accompanied by a remarkable 139% rise in contract values. These figures indicate robust annual growth rates of 29% and 37%, respectively.

Braze Revenue by Quarter and Year (Company SEC Filings)

Historically, Q4 has consistently shown the most modest growth within the company, a pattern commonly observed among other software firms. This trend primarily stems from year-end budget limitations in many companies, hindering new software sign-ups. However, despite this industry norm, Braze has sustained its revenue growth momentum. Since 2020, the company has experienced remarkable expansion, and this upward trajectory shows no signs of slowing down at present.

Looking ahead, the company is poised to secure significant victories within the customer engagement industry, currently valued at $19.3 billion and projected to reach $32.2 billion by 2027 , equivalent to a CAGR of 10.8%. This surge will be fueled by the escalating usage of eCommerce platforms and the increasing adoption of customer engagement solutions aimed at curbing customer churn rates.

Extrapolating on the current rate of growth in existing customer usage, industry growth and new customer wins, I foresee the company expanding at a substantial rate of approximately 25-30% for the next 3-4 years. In comparison, the trailing twelve months ((TTM)) revenue growth stands at 34%. Moreover, the year-over-year (YoY) growth from 2020 to 2022 showcases an impressive trend of 49%, 58%, and 56%, respectively. Extrapolating from this pace, I estimate that by 2026, the company's revenues will likely hover around $1 billion annually at its midpoint.

Road to Profitability

Operating Cash Flow

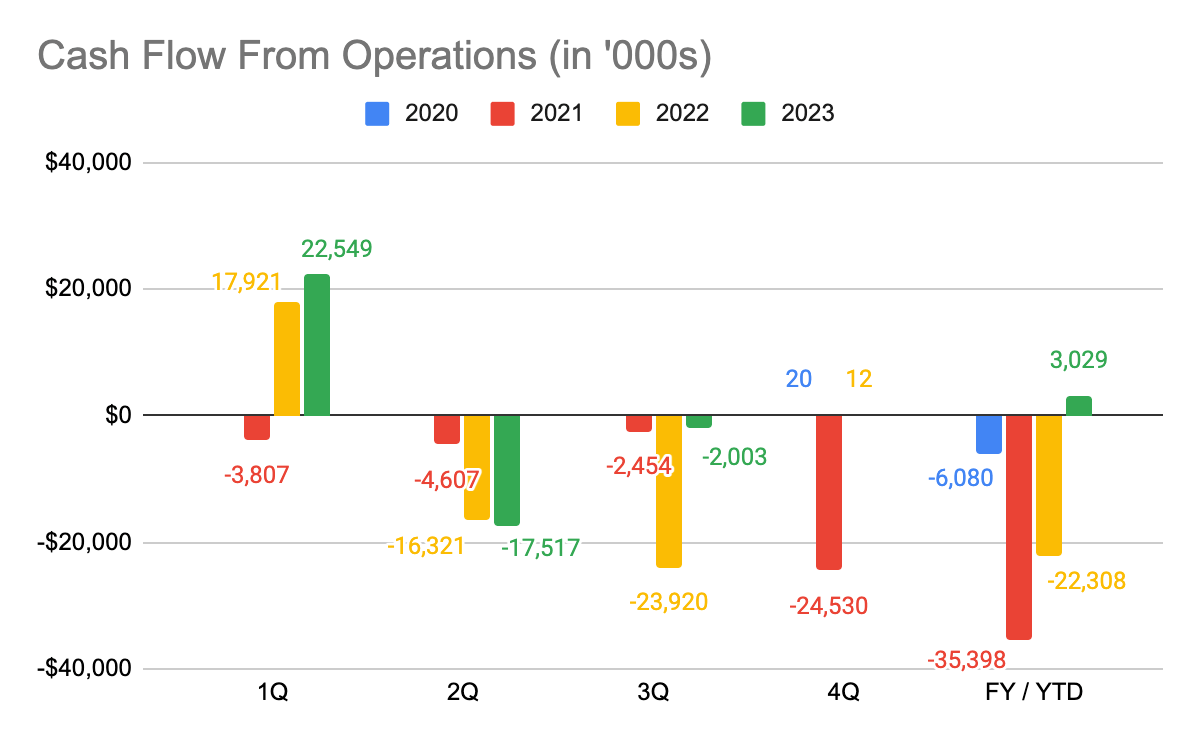

Since its IPO, the company has faced cash losses, although these have notably diminished owing to significant growth in overall revenue. A closer examination of operating cash performance reveals a recurring pattern: the highest cash generation occurs in 1Q, followed by cash burn throughout the rest of the year. This pattern is quite common in B2B tech firms, where revenue is generated each quarter but payment often occurs annually at the start of the year.

Conversely, costs associated with the company's software are incurred continuously throughout the year. Consequently, the operating cash flow appears to follow a seasonal trend due to this disparity between revenue generation and payment cycles.

Braze Cash Flow from Operations (Company SEC Filings)

{kind=link}

With expanding revenues, cash flow from operations is poised to increase accordingly. Given the current trajectory, investors might anticipate the company to achieve positive cash flow from operations around 2025-2026. This aligns with my projection of the company transitioning from a growth-focused phase to a profit-oriented phase during that period.

Can Gross Profits Improve?

The upward trend in gross profit margins indicates improving scale economics. This positive trajectory is expected to persist, considering the company operates on an established app with a solid cost foundation. This foundation includes various expenses like computing and storage costs from providers like AWS, Azure, and GCP, hosting expenditures, direct labor costs, and more.

GP Margins by Year and Quarter (Company SEC Filings)

In growth-oriented companies, priority often lies in executing new ideas and modules rather than strict cost efficiency. This emphasis sometimes leads to technical debt, unnecessary complexities, and inefficiencies in processes. However, as the company shifts focus towards optimizing infrastructure, reducing technical debt, and improving software utilization, these initiatives are poised to enhance gross profit margins. With these optimizations, I anticipate a rise in gross margins, potentially reaching the industry's peak performance rates of 77-80%. Nevertheless, further expansion might face constraints once variable costs come into play and start constraining gross margin expansions.

Are Operating Expenses Too High?

There's a prevalent anxiety, especially within the tech realm, surrounding the consistent rise in operating expenses each quarter. This concern, however, may not be as alarming as it seems at first glance. The critical point of concern typically emerges when surging operating costs fail to align with revenue growth. Fortunately, this particular worry may not hold true in this case. Despite a significant surge in hiring during the final quarter of 2021, the company has managed to reverse the trajectory of its operating costs relative to its revenues.

Braze Operating Costs as a % of Revenue (Company SEC Filings)

This reduction, contrary to the expected escalation, reflects a promising trend, indicating a potential for improved cost efficiency and operational optimization. This could signify a strategic phase where initial investments in personnel and infrastructure are beginning to yield positive results, potentially bolstering the company's financial performance in the long run.

In my opinion, looking ahead, I envision a continuous decrease in operating costs compared to revenue while the company thrives in its growth phase. I believe that only when the company's growth momentum subsides will they pivot towards a profit-driven strategy, initiating stringent cost-cutting measures. For investors, this implies that traditional valuation methods like the price-to-earnings ratio or discounted cash flow might not effectively gauge the company's worth. However, valuation based on the company's growth trajectory and revenue scale remains a viable approach.

Could The Company Achieve Profitability?

Absolutely. Compared to other sectors, the tech industry holds a distinct advantage in cost reduction, particularly in terms of workforce. Drawing from my background as a data and automation specialist in tech, I've led projects that automated tasks, slashing over 2000 work hours-equivalent to eliminating 12.5 positions-within a quarter. This isn't an isolated case; take X, formerly Twitter's 80% reduction in headcount earlier this year, which had no lasting impact on their operational performance. The app and essential business operations continued seamlessly without the excess workforce.

Moreover, the company currently holds substantial reserves, boasting over $467 million in cash and marketable securities, alongside a rapidly growing contract value. This financial position offers them ample room to sustain their growth trajectory without an immediate need to prioritize profitability. However, the potential for the company to shift towards a profitable mode remains a strategic option for the future.

Valuation

Regarding valuation, the company has seen a substantial decrease in its value post-IPO. This decrease provides a more attractive entry point for investors compared to its initial valuation. However, it's crucial to assess the company's valuation not just in relation to its past performance but also in absolute terms when weighed against alternative investment opportunities.

That being said, the current valuation of the company stands at:

| Shares Outstanding |

| 99,842,434 |

| Stock Price (as of Dec 22, 2023) |

| 54.09 |

| Market Cap |

| 5,400,477,255 |

| Market Cap (in '000s) |

| 5,400,477 |

| Less: Cash & Equivalents (in '000s) |

| 63,843 |

| Less: Marketable Securities (in '000s) |

| 407,500 |

| Add: Debt (in '000s) |

| 0 |

| Enterprise Value (in '000s) |

| 4,929,134 |

| Revenue, TTM (in '000s) |

| 439,518 |

| EV/Revenue |

| 11.21 |

Source: Company SEC Filings, author calculations.

The currently elevated EV/Revenue multiple stems from the company's projected revenue growth in the coming years. In my valuation assessment, I consider an average annual revenue growth between 25% and 30% for the next three years, gradually tapering thereafter as the company shifts gear towards profitability. This estimation positions the 2026 Revenue around $911 million. Utilizing the comparable median EV/Revenue multiple of 7.4 5 , this projection equates to an EV of approximately $6.8 billion, suggesting an anticipated annual return of ~11.2%, excluding the potential effects of dilution.

When compared to a few other B2B software companies today:

| BRZE |

| SMAR |

| GTLB |

| DDOG |

| SNOW |

| TTM Revenue (in Millions) |

| 439.52 |

| 913.73 |

| 539.03 |

| 2,008.11 |

| 2620.80 |

| TTM Growth % |

| 34.3% |

| 28.3% |

| 34.1% |

| 31.1% |

| 24.6% |

| EV (in Billions) |

| 4.92 |

| 5.83 |

| 8.76 |

| 38.83 |

| 61.33 |

| EV / Revenue |

| 11.2 |

| 6.5 |

| 16.5 |

| 19.0 |

| 23.1 |

| EV/Rev Multiple to BRZE |

| 1x |

| .57x |

| 1.47x |

| 1.70x |

| 2.06x |

Source: Company SEC filings, Seeking Alpha data and author calculation.

When juxtaposed with Smartsheet ( SMAR ), Braze commands a higher valuation owing to its higher growth rate. This elevated valuation implies broader opportunities for scaling operations, subsequently boosting revenues. However, when compared to GitLab ( GTLB ), Datadog ( DDOG ), and Snowflake ( SNOW ), Braze carries a lower valuation due to its smaller scale. Larger companies often present more opportunities for operational efficiencies, hence justifying higher valuations, provided these efficiencies are realized. Considering these factors, Braze appears to hold a fairly equitable valuation when evaluated alongside other B2B sales-focused software companies.

Risks

-

Multiple Stock Classes: The presence of multiple stock classes poses a challenge. Currently, Class B shares hold 10 voting rights, overshadowing Class A's single voting right. However, by January 2026, Class B will convert to Class A, equating their voting powers. Until this conversion, management retains substantial influence, limiting shareholders' sway over pivotal decisions.

-

Dilution Concerns: In line with industry norms, the company issues shares to attract and incentivize talent. Since their IPO, shareholder stakes have been diluted by approximately 5%. If this trend persists, existing shareholders may possess a smaller portion of the company over time.

-

Past Performance ? Future Growth: Although the company's robust trajectory, marked by escalating contract values, suggests continued success, past performance isn't a guaranteed indicator of future outcomes. Customer preferences can shift, potentially leading to customer losses as they opt for alternative software solutions. This shift could impact the company's growth prospects.

Conclusion

Braze stands as a thriving B2B tech enterprise, facilitating enhanced operational efficiency for companies. Their product's value reflects in the escalating contract values, growing customer base, and increasing revenues. While the company continues to utilize cash, there's a noticeable decline in their burn rate. Backed by a robust cash reserve, Braze is poised to sustain its growth trajectory for the coming years.

In conclusion, I hold an optimistic view that the company will transition into profitability sooner rather than later. Considering both growth rates and scale, I find Braze to be reasonably valued against its peers. However, the current valuation appears rather steep. I deeply appreciate their product and the value it offers to customers. Nonetheless, I perceive other high-growth opportunities in the market that present more favorable valuations at present.

For further details see:

Braze: Remarkable Growth, But Fairly Valued