BRCC - BRC Inc.: Take A Pass On This Unprofitable Stock

2023-03-18 02:26:25 ET

Summary

- BRC has been gradually improving the top line, and should continue to do so moderately in 2023.

- Where the major challenge for the company lies is in regard to its bottom line, which has struggled significantly throughout 2022, and I expect it to continue in 2023.

- With no certainty as to the performance of the company in 2023, I would look elsewhere for stocks that have a much better chance of doing well.

BRC Inc. (BRCC) has been hit hard during 2022, especially on the bottom line, where it continues to struggle to find a way to profitability.

The firm has been doing okay with revenue, and should continue to grow in 2023, but has been doing so at the expense of its bottom line, which has been under pressure for a while now.

In 2023 BRCC failed to adjust its prices to be more in alignment with market prices, and it paid the price on margins. It has since boosted prices and expects that to flow through to its P&L throughout 2023.

Management also said the bulk of expenditures on bolstering its sales channels is largely over, and that should also improve the bottom line of the company as it seeks to expand its customer base.

In this article, we'll look at some of the numbers, the growth strategy of the company, and why I'm somewhat skeptical it'll be able to deliver on its plan, based upon how deep of a hole it has dug itself into.

{kind=link}

Some of the numbers

Revenue in the fourth quarter of 2022 was $93.6 million, compared to revenue of $71.8 million in the fourth quarter of 2021, up 30 percent year-over-year. Full year revenue for 2022 came in at $301.3 million, compared to revenue of $233.1 million for full year 2021 , a gain of 29 percent.

While the company guided for revenue to be in the range of $400.00 million to $440.00 million for full year 2023, it's still significantly below consensus of $491.18 million.

Adjusted EBITDA in the fourth quarter of 2022 was -$(34.00) million, compared to -$(145k) last year in the fourth quarter. The decline was attributed to expenditures associated with growing and scaling its various sales channels.

Gross margin came under significant pressure in the reporting period, coming in at 31.5 percent, down 290 basis points from gross margin of 34.3 percent in the fourth quarter of 2021. It was worse for full year 2022, where gross margin was 32.9 percent, a drop of 556 basis points from gross margin of 38.5 percent in full year 2021. The reasons for the faltering gross margin was from the impact of higher inflation and costs associated with the start-up of its RTD production. Management said the impact from the start-up of production in the fourth quarter was 190 basis points, and for full year 2022 the impact was 170 basis points. With inflation expected to remain elevated for some time into the future, this is a problem that BRCC must solve in order to improve its bottom line.

The company spent approximately $37.5 million in cash in the fourth quarter to build up inventory in preparation to take on new customers. Last year it was limited in that regard because of low inventory issues, which resulted in the company primarily catering to its existing customer base rather than work in a meaningful way on adding new customers. That's something investors need to watch in order to see if they are able to effectively execute on the strategy.

Net loss for full year 2022 was -$(338.00) million, or -$(1.62) per diluted share.

At the end of calendar 2022 the company had cash and cash equivalents of $39.00 million, compared to cash and cash equivalents of $18.33 million at the end of calendar 2021.

Company had debt of $49.2 million at the end of 2022, compared to debt of $34.7 million at the end of calendar 2021.

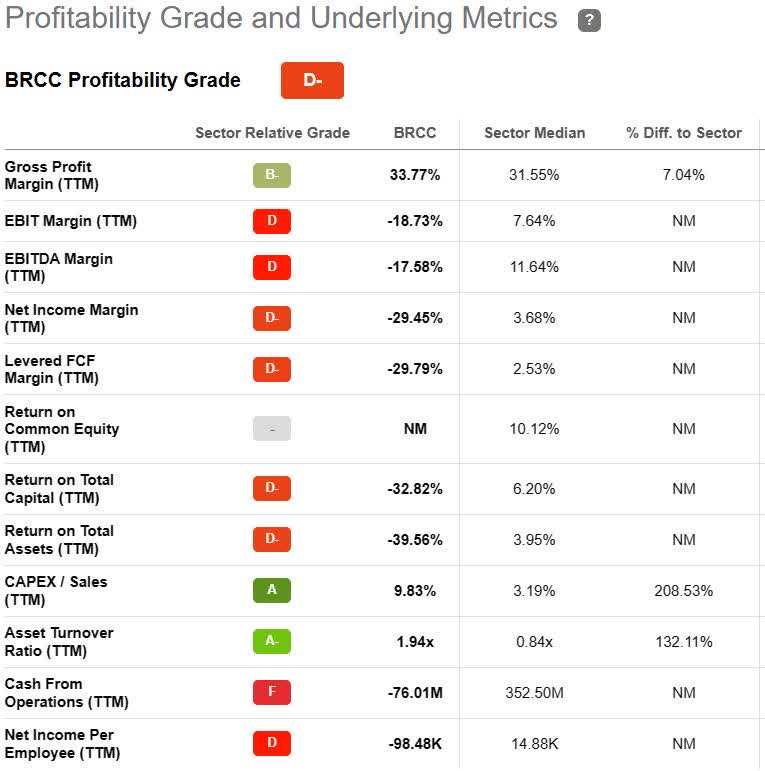

Profitability

While the company has started to grow some, it has done so at a huge cost, with almost every metric that matters, outside of gross profit margin, underperforming the sector median.

Among the most important and one of the worst of the profitability numbers was net income margin, which on a TTM basis was -29.45 percent, compared with net income margin of 3.68 percent sector median.

EBITDA margin ((TTM)) was also very weak, coming in at -29.79 percent, compared to the sector median of 11.64 percent.

Return on total capital ((TTM)) was -32.82 percent, compared to the sector median of 6.20 percent.

Return on total assets ((TTM)) was -39.56 percent, compared to the sector median of 3.95 percent.

Cash from operations ((TTM)) was -$(76.01) million, compared to the sector median of $352.50 million.

{kind=link}

Other than revenue growth, there wasn't much to like about the latest quarter and yearly performance, and even there it appears the company will have to continue to spend at high levels in order to maintain sales growth. Management did note that as a result of pricing adjustments, that should flow through its P&L during 2023. If it's able to execute, it could be a positive catalyst for the company, although I think it'll be a moderate one based upon the work it needs to do in order to turn profitable.

Gross margin guidance for full year 2023 was for it to be in a range of 36 percent to 37.5 percent. Even though that's an improvement over gross margin of 32.9 percent in full year 2022, it still is under the gross margin of 38.5 percent in 2021, showing how deep a hole management has dug itself.

As for adjusted EBITDA, the company guides for that to be in a range of $5 million to $20 million for full year 2023. Those numbers are predicated upon the company's sales channels performing as expected, in light of the significant expenditures to expand and improve them in 2022. In my opinion, if the company falters here, its share price is going to take another hit. If the company doesn't deliver in 2023, I don't see what it can do to improve its bottom line going forward, especially if it has to spend more to grow the top line.

Conclusion

As I'm writing this article, BRCC stock hit its 52-week low of $5.435 per share, and I'm not sure it'll be able to hold much above that going forward. About the only positive I see there is there is less risk at its current share price than there was last year.

Management was very clear on what it believes was the problem on the bottom-line last year, and with prices more in align with market prices, and most of its spending to improve its sales channels over, the ball is totally in the court of the company concerning executing on its strategy.

When all is said and done, it's still a question of demand, and there's a lot of uncertainty as to whether or not the company has a core customer base that it can count on for consistent and sustainable sales.

And even if it does continue to grow the top line, the bottom-line numbers are so bad it's going to have to vastly improve in order to turn sentiment around on the company.

Until it does prove it, I consider BRCC more of a trading stock than anything else, and I think it's going to be volatile throughout 2023, until or if it confirms it's going in the right direction by the results it produces.

There are so many better stocks to take positions in at this time that I don't see why any investor should take on the uncertainty and risk represented by the past performance of BRCC.

For further details see:

BRC, Inc.: Take A Pass On This Unprofitable Stock