BBIO - BridgeBio: If Acoramidis Completes Comeback This Highly Prized Biotech's Share Price Should Soar

Summary

- BridgeBio has some very significant price catalysts arriving in 2023 promising substantial upside should they be positive.

- Most important is Phase 3 interim data from Part B of a pivotal study of Acoramidis - indicated for ATTR.

- A $3bn market today, ATTR is expected to be worth >$10bn in annual revenues by the mid-2030s.

- Acoramidis unexpectedly failed to outperform placebo in a 6-minute walk test study in Part A of the trial - although the placebo arm performed unexpectedly well.

- This can be remedied when Part B data arrives in July which has an endpoint of all cause mortality. The failure of Part A is still baked into the share price, so success ought to result in a soaring share price.

Investment Overview - A Highly Valued Company Recovering From A Major Trial Setback

At first glance, Palo Alto, California based biotech / drug developer BridgeBio ( BBIO ) Pharma may not seem like the most attractive of investment opportunities.

At the time of writing the company has a market cap valuation of $1.7bn, yet revenues earned from its 2 commercialised products to date - NULIBRY (fosdenopterin), approved to reduce risk of mortality in patients with molybdenum cofactor deficiency - and TRUSELTIQ, an orally administered, ATP competitive, FGFR1 tyrosine kinase inhibitor approved to treat metastatic bile duct cancer - earned only $1.5m across the first 9m of 2023, while BridgeBio made a net loss of $344m over the same period.

Both NULIBRY and TRUSELTIQ have now been fully licensed to partners - Origin Sentynl in the case of NULIBRY, in exchange for a $10m upfront payment plus ~$5m of sales milestone payments and royalties on net sales, and Helsinn in the case of Truseltiq, with profits and losses shared on a 50:50 basis, although in August last year Helsinn informed BridgeBio it would terminate the deal, meaning neither company is actively marketing and selling the niche drug.

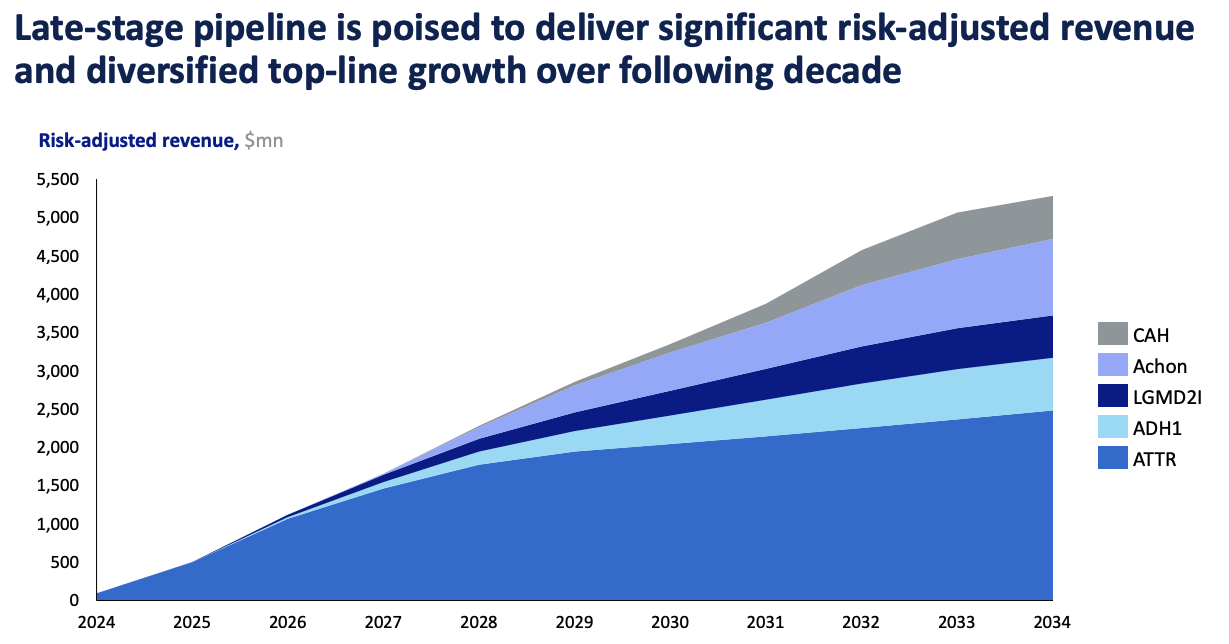

In January 2022 BridgeBio initiated a restructuring designed to reduce costs and reduce the workforce - usually a sign of a struggling company - but with that said, after a difficult end to 2021 and a struggle through 2022, which saw the company's share price decline by 85% from ~$49, to ~$8, 2023 promises to have some exciting catalysts in store - whilst management has promised >$2bn per annum in revenue generation by 2027, and $5bn per annum by 2034.

{kind=link}

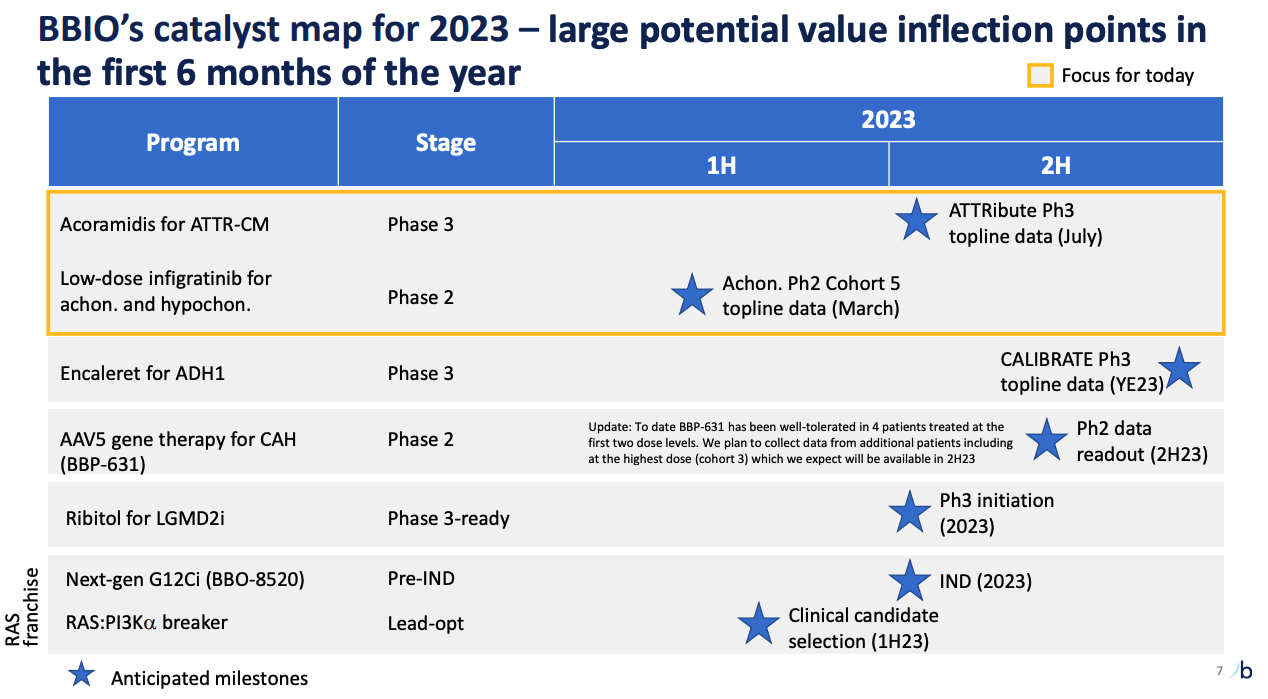

BridgeBio 2023 catalyst map (BridgeBio JPM Healthcare Conference presentation)

The biggest contributor to these revenue targets will come from the disease indication transthyretin amyloidosis ("ATTR"), a protein disorder caused by a faulty TTR gene that results in a stiffened left heart ventricle that struggles to pump blood around the body. If left untreated, ATTR can be fatal.

As we can see above BridgeBio's Acoramidis will read out Phase 3 interim data in the second half of this year. The company believes the ATTR market is worth $3bn today, but will be worth $10-$15bn by next decade owing to better diagnostic tools, and better available treatments.

Acoramidis has already failed Part A of this Phase 3 study , however, after data showed the placebo arm of the trial performing unexpectedly well. Acoramidis failed to outperform placebo in the key primary endpoint of 6-minute walk test ("6MWT"), which was described as "baffling" by the biotech's CEO Neil Kumar, Ph.D.

That was in December 2021 and it is the most striking reason for the declines in BridgeBio's share price, although other data, such as a 27% reduction in risk of death compared to placebo - persuaded the Independent Data Monitoring Committee and Bridge Bio itself to continue into the part B phase of the pivotal study.

{kind=link}

BridgeBio revenues sources looking ahead (JP Morgan Healthcare Presentation)

As we can see above the remaining $2 - $3bn of revenues BridgeBio expects to generate by the middle of next decade are derived from 4 separate fields.

- Firstly, autosomal dominant hypocalcemia type 1 (ADH1) - topline Phase 3 data is expected from BridgeBio's lead candidate, Encaleret, a small molecule antagonist of the calcium sensing receptor by the end of 2023.

- Secondly, limb girdle muscular dystrophy (LGMD) - lead asset Ribitol, a glycosylation substrate pro-drug formerly known as BBP-418) will enter a Phase 3 study this year.

- Thirdly, - Achondroplasia, a genetic disease affecting the fibroblast growth factor receptor ("FGFR"), in which BridgeBio is attempting to secure approval for low-dose infigratinib (Truseltiq is a high dose formulation of infigratinib)

- And finally, Congenital Adrenal Hyperplasia - with a Phase 2 readout of gene therapy BBP-631 due this year.

With $558m in cash BridgeBio says it has a funding runway that will last until 2024, although I would not be surprised to see the company raise on a promising data readout in 2023, to ensure there is sufficient funding in place to fund a commercial product launch.

Naturally, if all of these programs were to succeed and BridgeBio met its revenue targets, the company's current market cap would significantly undervalue the company.

Alexion - another rare disease specialist generated $6bn of revenues in 2020, the year before it was acquired by Anglo / Swedish Pharma AstraZeneca ( AZN ) in a ~$39bn deal.

Nevertheless, with its lead asset a doubt after failing the first stage of its first pivotal trial, and other assets needing to overcome significant hurdles both clinically and commercially before they can meet management's expectations, it is understandable that the market is fearful of sending BridgeBio stock any higher at the present time.

The key catalyst here would appear to be Acoramidis and we will have a tantalising Phase 2 readout this quarter or next from a Phase 2 study, plus the Phase 3 topline data expected in July.

A such, this could be a good time to consider picking up some BridgeBio stock, which remains priced as if Acoramidis is not going be approved by the FDA, or at least not deliver data sufficient to challenge currently approved therapies such as Vyndamax, a $2bn per annum selling drug belonging to Pharma giant Pfizer ( PFE ), and Onpattro, developed by RNA-interference specialist Alnylam ( ALNY ) earning $558m in FY22.

Another development of note at the company is its KRAS targeting precision oncology franchise. KRAS is a much sought after drug target that was once thought undruggable, before both Amgen ( AMGN ), with Lumakras, and Mirati Therapeutics ( MRTX ) secured approvals for Lumakras and Krazati, respectively. Both these drugs are approved for Non Small Cell Lung Cancer ("NSCLC") and are forecast to make peak sales >$1bn per annum (so called "blockbuster" sales) although neither has got off to a strong commercial start.

In this post I'll provide a quick overview of BridgeBio the company, assess the prospects for Acoramidis' approval in more detail, and consider the rest of the pipeline, whilst highlighting some risks.

BridgeBio Overview

BridgeBio joined the Nasdaq back in 2019 via one of the largest biotech IPOs of the year, which raised >$300m via the issuance of 20.5m shares priced at $17 per share. According to a statement in the company's Q322 10Q submission:

Since inception, BridgeBio has created 15 Investigational New Drug applications, or INDs, and had two products approved by the U.S. Food and Drug Administration. We work across over 20 disease states and have over 15 ongoing clinical trials at various stages of development.

All of BridgeBio's programs are focused on treating patients suffering from "genetic diseases and cancers with clear genetic drivers" and there are 4 main franchises of sorts: Precision Cardiorenal - which includes Acoramidis and Encaleret - Mendelian (diseases arising from a single defective gene), which includes low and high dose Infigratinib, and Ribitol - Precision Oncology, which includes the KRAS franchise, TRUSELTIQ and Infigratinib indicated for various solid tumor cancers - and Gene Therapy, which includes the CAH candidate BBP-631.

Bridge Bio has an experienced management team led by CEO and President Neil Kumar, Ph.D. Kumar was educated at Stanford and was interim Vice President of Business Development at MyoKardia from 2012 to 2014. He has also served as a principal at Third Rock Ventures - a well-known biotech venture capital business - and as an associate principal at strategists McKinsey & Company.

Co-founder Charles Homcy has also worked at Third Rock ventures and was once a director at Sickle Cell Disease specialist Global Blood Therapeutics (GBT), recently acquired by Pfizer in a $5.4bn deal. Founder and Chairman of Oncology Frank McCormick was formerly at Onyx Pharma, acquired by Amgen in 2013 in a ~$10bn deal, and Chairman of R&D Richard Scheller was formerly Chief Science Officer and Head of Therapeutics at 23andMe, and before that Executive Vice President of Research and Early Development and a member of the Executive Committee at Genentech.

Given the blend of Big Pharma experience, venture capital financing, and past M&A activity, it would probably not be too far-fetched to suggest that management may view a takeover of BridgeBio as an optimal outcome, which may explain why it has made its revenue generating ambitions so clear - so that prospective buyers can trace a clear path to a return on their investment and leadership in complex fields such as liver disease, gene therapy, and Precision Oncology.

Paths to Approval - Acoramidis Can't Afford To Fail Again

For all its experience, however, management must prove that its drugs work and are approvable, which is likely why the Phase 3 Acoramidis data released in December 2021 dealt such a blow to the company's share price. This was a company in a hurry that was not expecting such a reverse.

Prior to announcing the data, management had also completed a deal to raise $750m in debt financing. The fact that it was non-dilutive was a positive for investors, although BridgeBio has 3 separate major deals which amount to nearly $1.7bn of debt held by the company, but the money was surely earmarked for a commercial push.

In its ATTRibute-CM study, according to a December 2021 press release :

The mean observed decline in 6MWD at Month 12 in participants receiving acoramidis or placebo with baseline eGFR ? 30 mL/min/1.73m 2 were 9 meters and 7 meters, respectively. Decline observed in both arms of ATTRibute-CM was similar to expected functional decline in healthy elderly adults.

The declines were also substantially less than the >40 meter annual declines observed in previous untreated arms reviewed by the company. The decline in the ATTRibute-CM placebo group was more than 70% lower than the decline observed in the ATTR-ACT treatment group.

In other words, had the placebo group behaved as prior groups had, it seems that Acoramidis would have shown a statistically significant result and shares would not have collapsed in value the way they did. After describing himself as - justifiably, it seems - "baffled" by the placebo showing, CEO Kumar continued:

The drug does appear to be pharmacologically active and well-tolerated, and we observed improvement on quality of life with promising trends on adverse events leading to death. The drug seems to be doing what we are asking of it. If we observe enough clinical outcome events at Month 30, I am still hopeful that we will demonstrate the benefit of acoramidis treatment.

The study has not moved into Part B which evaluates a "hierarchical comparison including all-cause mortality and cardiovascular hospitalisations: at 30 months in a patient population of 632. Based on secondary endpoints met in the December 2021 dataset there are reasons for qualified optimism.

- Acoramidis improved Kansas City Cardiomyopathy Questionnaire Overall Summary Score relative to placebo (nominal p < 0.05, mixed model repeated measures without imputation)

- Acoramidis improved NT-proBNP relative to placebo. Median percent change from baseline at Month 12 in acoramidis-treated and placebo-treated participants were +0.6% and +24.3%, respectively (nominal p < 0.05 based on absolute changes from baseline between groups)

- Acoramidis increased serum TTR levels relative to placebo. Mean percent change from baseline at Month 12 in acoramidis-treated and placebo-treated participants were +38.5% and -0.7%, respectively (nominal p < 0.01 based on absolute changes from baseline between groups)

There has not been much in the way of fresh data to consider since, although BridgeBio did report data from a Phase 2 open-label extension ("OLE") study of Acoramidis in patients with ATTR cardiomyopathy (ATTR-CM). 31 of 47 patients remained in the study after 36 months, and BridgeBio reported that "near-complete TTR stabilization as measured by established ex vivo assays and increased serum TTR levels" was observed.

To summarise, BridgeBio cannot afford to fail again when its Phase 3 interim data arrives in July. It is hard to see the FDA tolerating another missed endpoint when there are 2 approved therapies on the market, and several other medication prescribed off-label.

On the other hand, if you take all datasets as a whole, had it not been for the anomalous placebo arm in 6MWD, the market and analyst expectation would likely be much more in favour of approval. With management promising $2bn in revenues by 2026, the pressure is really on the company to deliver. A positive set of data will almost certainly revitalise the share price, whilst a negative readout is going to shave more value off the market cap.

Encaleret Leads Charge Of ex-ATTR assets

In December last year BridgeBio issued a press release stating it had moved its asset Encaleret into a Phase 3 pivotal study in ADH1. This follows a successful Phase 2 in which the drug demonstrated:

At week 24 of outpatient treatment, 92% of participants receiving encaleret achieved normal blood calcium levels in the absence of SoC, and 77% of participants had achieved normal 24-hr urinary calcium excretion

The Phase 3 study will enroll ~45 participants with biochemical evidence of hyperparathyroidism, and genetic confirmation of ADH1. This is the next most important data readout in a catalyst rich 2023, in my opinion, which management rates as a $1bn market opportunity, implying sales could be measured in the triple-digit millions.

Even if there are only ~25k carriers of gain-of-function variants of the calcium sensing receptor (CaSR), the underlying cause of ADH1, management estimates, compared to an estimated ~400k patient market for ATTR-CM, success with Encaleret would provide further validation of BridgeBio's approach and its technology, and management's ability to guide assets through the clinical study and FDA approval process.

In terms of market opportunity, Bridge Bio's next most important asset after Acoramidis is low-dose Infinigratinib in achondroplasia, which represents a 55k patient market, management believes. Achondroplasia is a disease that restricts bone growth - people with the disease have an average height of ~137 centimetres.

This is $2.5bn market, management believes, and although Vosoritide - developed by BioMarin ( BMRN ) and marketed as Voxzogo, achieving >$100m sales in the first three quarters of 2022 - represents tricky competition, believes it has the edge of the competition in terms of driving bone growth, although this proof has not yet been established in the clinic.

Cohort 4 of the Phase 2 study showed a statistically significant increase in the important biomarker Collagen X, and now management is expecting Cohort 5 results - due this year - to show:

Efficacy across 3 measures: change from baseline AHV, responder rate, and % of children getting to 7 cm/yr.

There are several other highlights in BridgeBio's pipeline besides. Ribitol ready for Phase 3 in a disease in limb girdle muscular dystrophy that has no approved therapies - a 7k patient market. The Phase 1 trial initiation of Bristol Myers Squibb ( BMY ) partnered BBP-398, targeting SHP2, which like KRAS, is a drug targeted that has the market excited. This deal could be worth >$900m in upfront payments and milestones.

The KRAS assets themselves are scarcely mentioned in BridgeBio's January presentation to the JP Morgan Healthcare conference - perhaps due to lack of success of Lumakras and Krazat in the commercial setting, although Lumakras racked up nearly $300m of sales in FY22. Besides, these are preclinical assets, so investors will need to be patient regarding this franchise.

Conclusion - A Strong Player In Rare Diseases In a Hurry To Show Promise - The P3 Acoramidis Is Key (although there is some downside protection)

To summarise my take on BridgeBio it is a company set up by industry veterans who typically also have a background in venture capital.

What that means is that BridgeBio has set itself some aggressive targets when it comes to revenue generation, and it has also borrowed - and spent - heavily in order to develop its pipeline.

The failure of Acoramidis in the first part of its Phase 3 clearly shocked the company and spooked the markets, but that opportunity is still very much in the balance - based on the other endpoints of the ATTRibute-CM study, the chances of the drug's success in its Part B are arguably greater than 50/50, although even if endpoints are met, convincing the FDA to approve the drug represents a tricky task.

With its market cap of $1.7bn BridgeBio shares are still not cheap and should Acoramidis fail I am not sure a conservative estimate of BridgeBio's remaining pipeline opportunities - in the near term at least - would exceed $1bn in peak revenues. That may be enough to mitigate the downside risk of an Acoramidis Phase 3 miss, however.

The company would be forced to curb its spending once again and losses could drag the market cap valuation <$1bn, whilst mounting debts would become an uncomfortable topic of discussion. There may, however, be three other Phase 3 stage assets to fall back on, including the gene therapy targeting hyperplasia, which I have scarcely mentioned, and which uses an older approach than more modern, CRISPR based gene therapies, although it has been validated by the likes of bluebird bio (BLUE).

The case for upside is easier to make, since we can look back to BridgeBio's share price prior to the 6MWD test fail - ~$50 per share. That implies there is >100% upside potential in play on positive news.

BridgeBio may have been launched and grown as a potential acquisition target so there is that additional upside catalyst in play and management's past experience is strong enough that a setback when the interim data arrives in July may not necessarily be a terminal setback, as it would be for a single-asset company.

As such, I would give BridgeBio a tentative "BUY" recommendation due to the large number of catalysts falling due in 2023, including the key Acoramidis interims. This ought to be a pivotal year for the company's pipeline assets and I am "just about) expecting management to pull through.

The downside will be ugly if Acoramidis falls through, but the company will at least live to fight another day, and there is an intriguing early stage pipeline to fall back on long term, even if finances are an ongoing concern.

For further details see:

BridgeBio: If Acoramidis Completes Comeback, This Highly Prized Biotech's Share Price Should Soar