BBIO - BridgeBio: Positive Updated Acoramidis Data May Not Imply Further Upside

2023-08-30 16:08:00 ET

Summary

- BridgeBio's shares have soared by over 150% since the positive results of its drug Acoramidis for treating ATTR-CM were released in July.

- The final data from the Phase 3 study of Acoramidis confirmed its positive results, and the company plans to submit a New Drug Application to the FDA by the end of the year.

- BridgeBio's pipeline includes multiple programs targeting various disease areas, but its cash available for development projects is dwindling. The company is under pressure to bring a product to market.

- Although Acoramidis data arguably makes the case it is a more effective drug than Pfizer's Tafamidis, it may be tough for BridgeBio to compete in a commercial setting.

- There is further competition in the form of Alnylam's Patisiran. All things considered, this may not be the right time to be buying BridgeBio stock.

Investment Overview

When I last updated on BridgeBio Pharma ( BBIO ) for Seeking Alpha in February, I suggested that the company "has some very significant price catalysts arriving in 2023 promising substantial upside should they be positive".

That has very much proved to be the case, with shares soaring in value by over 150% since my note, primarily driven by the progress of the company's most important drug Acoramidis, indicated to treat transthyretin amyloidosis cardiomyopathy ("ATTR-CM"), a disease in which build-up of amyloid in the heart's left ventricle - its main blood pumping chamber - prevents its effective functioning, potentially causing heart failure.

After failing the first part of a Phase 3 study in this indication in late 2021 - owing to an unexpectedly strong performance within the placebo arm in the primary endpoint of 6-minute walk test ("6MWT") - BridgeBio's share nose-dived overnight from a value of over $40 per share, to ~$9 per share.

My thesis - shared by many - was that if data from the second part of the study - due in July - were positive, BridgeBio's share price would reclaim much of its lost ground, particularly since, according to the company's research at least, the ATTR-CM market is worth ~$3.6bn today, but if a suitable treatment is commercialised, could grow in size to $10-$20bn within five years, with better testing leading to more patient diagnoses.

When the data arrived in July, it was indeed positive, with management noting a "highly statistically significant improvement in the primary endpoint", which was 6MWT, and an 81% on-treatment survival rate, versus 74% in the placebo arm, resulting in an absolute risk reduction of 6.43% and relative risk reduction of 25%. As soon as the data were released, BridgeBio stock doubled in value, from ~$17 per share, to $35 per share.

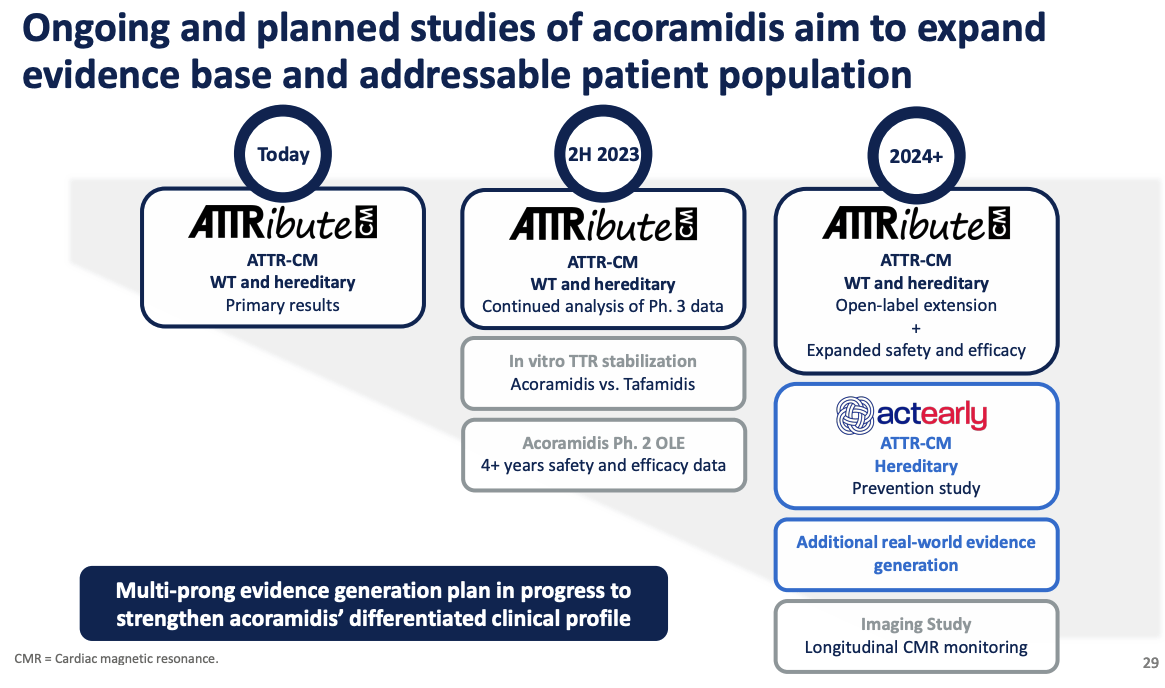

Yesterday, BridgeBio released the final data from the study - dubbed ATTRibute-CM - confirming and even improving on the initially impressive results, and promised to submit its New Drug Application to the Food and Drug Agency ("FDA") before the end of the year.

In this post I'll look at the data in more detail and also discuss the market opportunity, BridgeBio's ability to hit the ground running with a commercial launch, and what the implications may be for the company's share price. Before I do that, however, I'll briefly provide an overview of the company, highlighting its overall pipeline strength

BridgeBio - Broad Overview

BridgeBio is a Palo Alto based biotech founded, according to its Q2 2023 10Q submission (quarterly report), "to discover, create, test and deliver transformative medicines to treat patients who suffer from genetic diseases and cancers with clear genetic drivers". The 10Q goes on to say:

Since inception, BridgeBio has created 15 Investigational New Drug applications, or INDs, and had two products approved by the U.S. Food and Drug Administration. We work across over 20 disease states and have over 15 ongoing clinical trials at various stages of development.

Several of our programs target indications that we believe present the potential for our product candidates, if approved, to target portions of market opportunities of at least $1.0 billion in annual sales.

Bridge Bio's first two approved drugs - NULIBRY - indicated for reducing risk of mortality in patients with molybdenum cofactor deficiency, and Truseltiq - to treat metastatic bile duct cancer - have been respectively out-licensed, and out-licensed and subsequently withdrawn from the market. Neither generated much in the way of revenue, but in its 2022 annual report, management promised that it:

...could deliver up to eight potential Phase 3 readouts over the next five years, of which we expect acoramidis, low-dose infigratinib, encaleret, BBP-418 and BBP-631 to be in markets of one billion dollars or more.

{kind=link}

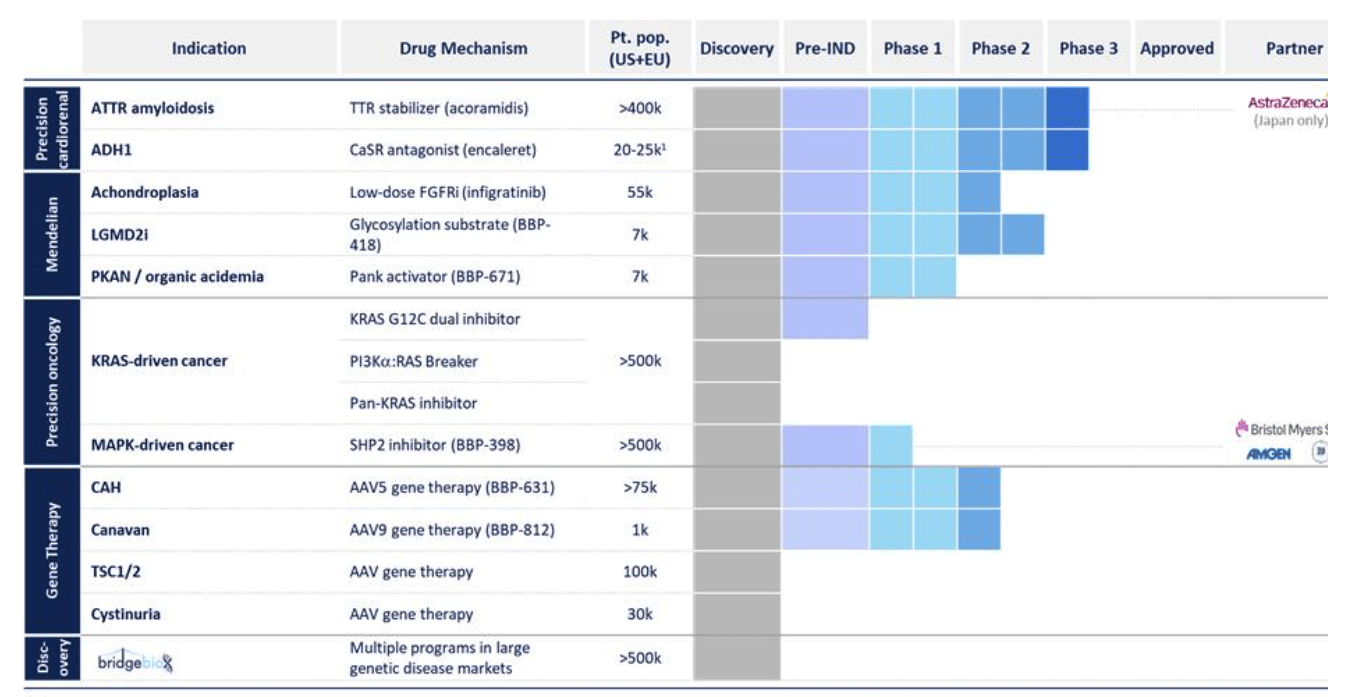

As we can see above, BridgeBio's pipeline is a diverse one, targeting four different disease areas - Precision Cardiorenal, Mendelian, Precision Oncology, and Gene Therapy - plus several other programs focused on "large genetic disease markets".

Essentially, BridgeBio is taking a pragmatic approach to drug development, first identifying areas of high unmet need, such as genetic diseases, which management believes exists "at the intersection of high unmet patient need and tractable biology", and then attempting to develop drugs that fit the remit using its "leadership team of world-renowned drug hunters".

Working through the pipeline, we can see that ATTR-CM has the largest patient population other than KRAS driven cancers - a tricky space in which BridgeBio is at the earliest stages of development - there are already two approved drugs targeting KRAS, Amgen's ( AMGN ) Lumakras, and Mirati Therapeutics ( MRTX ) Krazati, both of which have struggled somewhat in the commercial setting to date.

Since BridgeBio shared the above pipeline status in its 2022 annual report , the company has begun enrolling for children in a registrational Phase 3 study of low-dose infigratinib in achondroplasia and hypochondroplasia (short stature), after Phase 2 study results "demonstrated a significant and robust increase in annualized height velocity ("AHV") with a mean change from baseline of +3.38 cm/year for 12 children at six months.

In limb-girdle muscular dystrophy type 2I/R9 ("LGMD2I/R9"), BridgeBio believes it may be able to use glycosylated ?DG levels as a surrogate endpoint to support a push for accelerated approval for candidate BBP-418, and has dosed a first patient in Phase 3 study, whilst management hopes to share Phase 3 study data for Enacalaret, a calcium-sensing receptor ("CaSR") inhibitor for autosomal dominant hypocalcemia type 1 ("ADH1"), in the first half of next year, and has promised an update on BBP-631 – its AAV5 gene therapy candidate for congenital adrenal hyperplasia ("CAH") by the end of the year (updates taken from company Q2 2023 earnings update ).

BridgeBio has cash available to fund its many development projects - over $380m counting short term investments as of Q2 - although the cash pile is being eroded rapidly - net loss across the first half of 2023 was $258m. In short, BridgeBio is coming under increasing pressure to bring a product to market, otherwise further dilutive at the market fundraisings are likely to be the order of the day.

The company's best chance of doing that surely lies with Acoramidis at the present time - as evidenced by the wild share price swings updates on study progress tend to trigger.

Acoramidis - Overview & Latest Data

In 2019, the FDA approved two drugs developed by Pharma giant Pfizer - Vyndaqel (tafamidis meglumine) and Vyndamax (tafamidis) for ATTR-CM. These drugs come in capsule form, and were the first to be approved to treat the disease. In 2022, they generated ~$2.5bn of revenues. The drugs are oral transthyretin stabilizers that slow the formation of amyloid.

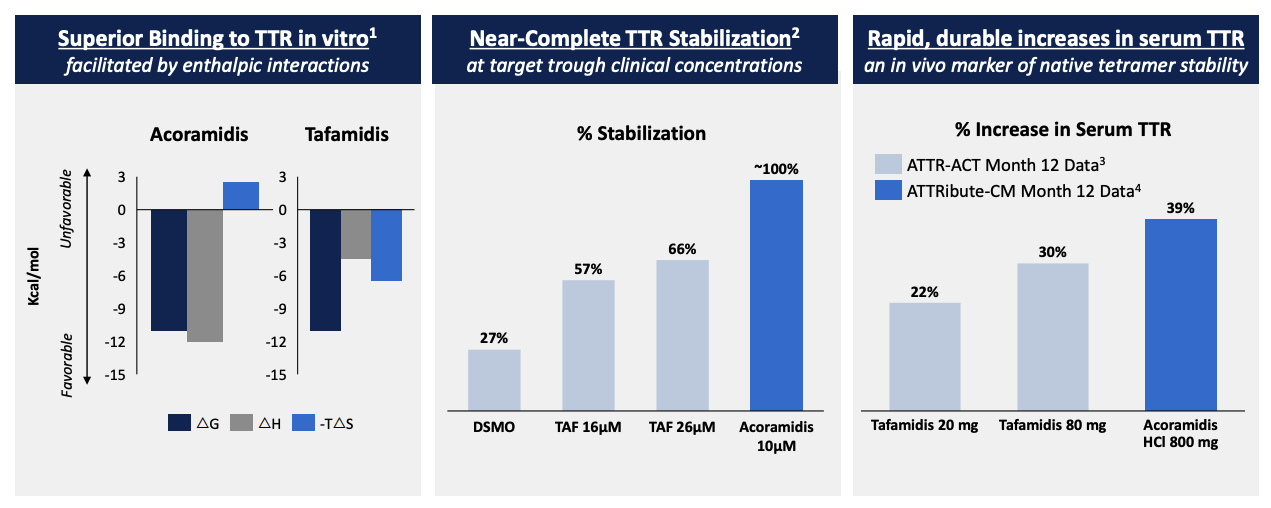

In its presentation of full Phase 3 ATTRibute-CM acoramidis data, BridgeBio says that its candidate is a "next generation stabiliser that employs multiple strategies to maximise potency", which means the drug "sees more target", "binds more target", and "glues the target together stronger".

The company claims data shows superior binding, near-complete TTR stabilisation, and rapid, durable increases in serum TTR, and shares data comparing acoramidis favourably with tafamidis in terms of pan-variant TTR stabilisation.

Acoramidis - more potent TTR stabilisation (results presentation)

{kind=link}

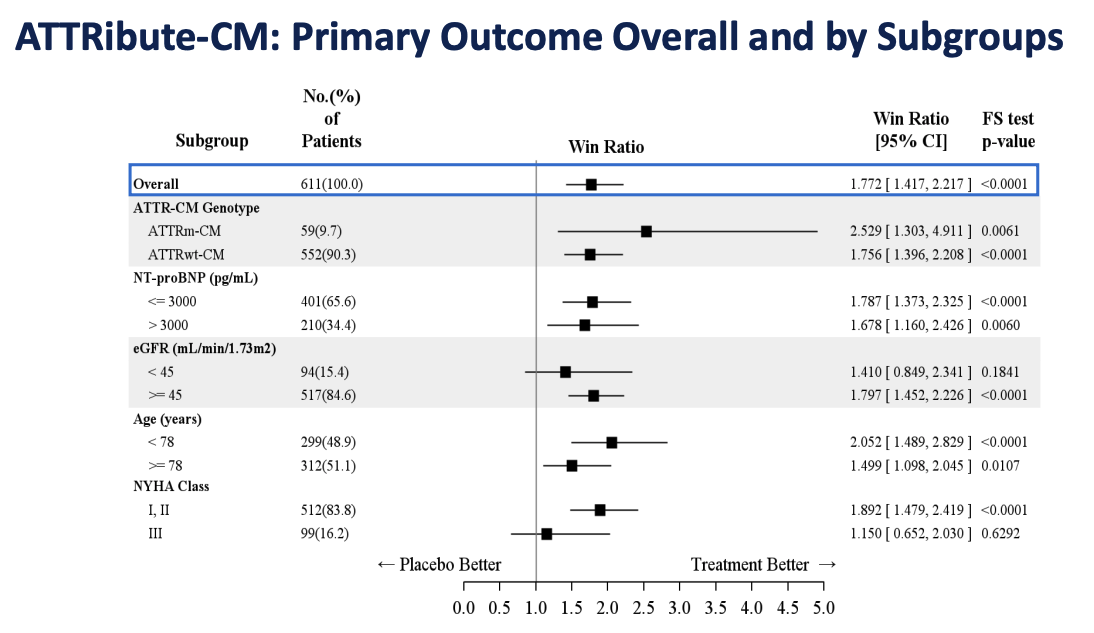

ATTRibute-CM had 421 patients enrolled in the acoramidis arm (receiving a dose of 800mg twice daily), versus 211 in the placebo arm, and the study lasted thirty months. In its detailed results press release BridgeBio announced that:

Absolute values observed across all-cause mortality ((ACM)), cardiovascular mortality ((CVM)) and CVH showed that over 30 months, patients survived more and were hospitalized less than has been seen in prior controlled studies of ATTR-CM to the company’s knowledge

ATTRibute-CM - primary outcome and by subgroups (results presentation)

{kind=link}

As we can see above, Acoramidis was consistently favoured across key subgroups, namely variant and wild-type ATTR patients, and New York Heart Association ("NYHA") Class I, II, and III patients. 40% of acoramidis patients experienced an improvement in 6MWT, versus 24% on placebo, which, again, BridgeBio states is "higher than have been observed in prior controlled studies in ATTR-CM".

The overall safety data did not reveal any issues of major significance, with acoramidis patients experiencing a similar level of treatment related adverse events, a lower percentage of severe adverse events, and a lower rate of discontinuations.

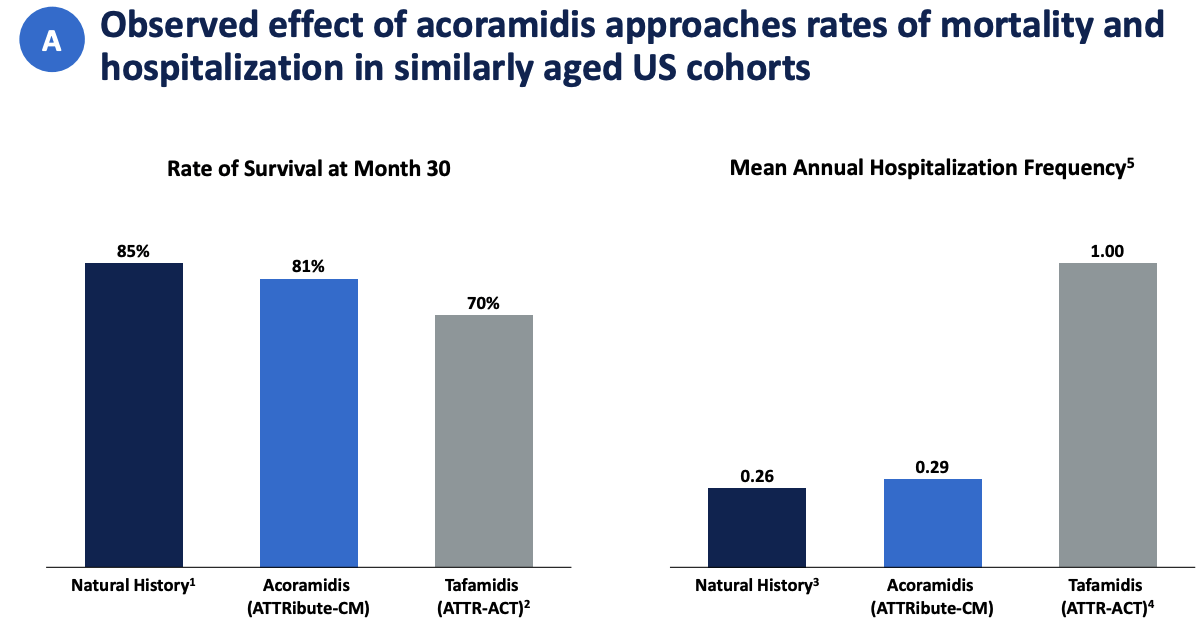

acoramidis versus tafamidis, Medicare populations (results presentation)

{kind=link}

Above we can also see that patients on acoramidis achieved rates of mortality and hospitalisation similar to a broader US Medicare population, and importantly, apparently superior to Tafamidis, with a substantially lower rate of hospitalisations also. The 40% 6MWT improvement was also superior to the 19% achieved by Tafamidis, BridgeBio states, although BridgeBio does frequently make the point that "the values shown are directional and do not report robust comparative analysis."

It is certainly dangerous to cross compare different studies, as no two clinical studies are every quite the same, and medical professionals and analysts have been generally hesitant to declare acoramidis the outright superior drug of the two drugs, given this was not the goal of the study. Nevertheless, there are clearly reasons for BridgeBio shareholders to be positive about these final results.

Path To Commercialisation & Further Competition

Despite the positive ATTRibute-CM results, BridgeBio's path to an approval is not necessarily straightforward - it could be the case that the FDA requests data from further studies, or longer term safety data, before it agrees to even accept an NDA from BridgeBio, let alone approves the drug.

{kind=link}

With Tafamidis already on the market, BridgeBio's data is probably not compelling enough for the FDA to see the need to rush the drug to market, whilst authorities overseas are expected to require more data submissions before accepting a marketing submission.

Meanwhile, if it does eventually reach the market, acoramidis may face another challenger for market share in the form of the RNA-interference specialist Alnylam's candidate Patisiran.

Patisiran has been approved since 2018 under the brand name Onpattro for the treatment of polyneuropathy ("PN") of hereditary transthyretin-mediated amyloidosis (hATTR), but in November last year, the drug met its primary endpoint of 6MWT in a study in ATTR-CM, causing Alnylam's stock price to jump by nearly 50%.

Patisiran apparently missed a composite endpoint of all-cause mortality, frequency of cardiovascular events, and change from baseline in 6-MWT, but nevertheless, the FDA accepted Alnylam's supplementary NDA for the indication in February this year, with a decision date likely on October 8, although the FDA is likely to convene an advisory committee to discuss the application.

On the one hand, Patisiran is already approved commercially in a similar indication, so it is familiar to physicians and proven to work in a commercial setting. On the other, acoramidis appears to have generated the superior study data. Alnylam has the market experience and $2bn of cash available to fund a commercial launch, whilst, as mentioned, BridgeBio's funding is expected to run out in the second half of next year.

Concluding Thoughts - Management May Rue Initial Phase 3 Study Failure As Competition Intensifies

When Alnylam delivered its positive results last November, analysts were quick to suggest patisiran revenues could top $2.5bn per annum. Based on my research, it is harder to find a similar level of enthusiasm for acoramidis in a commercial - although that may be due to skepticism brought about by the original study failure.

In my view, that original study failure may prove to be a continuing thorn in BridgeBio's side, as it dampened expectations around the drug. Although it may not have delayed an NDA submission (although could the company have pushed for accelerated approval if that study had been aced?), it has likely made it much harder for BridgeBio to find a well-resourced partner that could have helped the company fund a commercial launch.

The reality now is that cash-strapped BridgeBio will either have to raise substantially more funding in a dilutive manner, dragging its share price down in the process, or drop some of its other projects simply in order to get an acoramidis approval across the line, leaving little funding for a marketing push.

If data had been ever-so-slightly more impressive - for example, had the all-cause mortality endpoint not been missed, BridgeBio may have been able to position acoramidis as clearly superior to tafamidis, and perhaps patisiran as well, but as things stand, in a three-horse race for market share, it is hard to see BridgeBio coming out on top, and realizing its blockbuster (>$1bn per annum) revenue goal.

Of course, it is not too late to secure a commercial partner, or even a buyout - in 2020, Bristol Myers Squibb paid $13bn to acquire MyoKardia and gain access to its obstructive hypertrophic cardiomyopathy (“HCM”) drug Mavacamten, now marketed and sold as Camzyos, with peak sales expectation of ~$4bn.

It's not inconceivable that BridgeBio could be acquired, although given it has so many other assets of significance, in completely separate fields, arguably management would prefer a commercial partner, even if it was forced to split revenues from the drug 50/50.

A worst case scenario could see the FDA request more data before considering approval, leaving the company struggling for funding with no near-term commercial revenues in sight. Even without any delays, there is not much prospect of the company driving any meaningful revenues until 2025.

As such, if I were an investor considering purchasing BridgeBio stock, I would be in no rush to buy at today's share price of $31 with a market cap valuation of $5bn. Although there are other data updates arriving, from other pipeline assets, acoramidis is clearly the "jewel in the crown" driving the company's valuation.

Given there will now be a long wait - of anything up to two years - for an approval decision on BridgeBio's lead drug, my suspicion is that we may see a downward price correction, and as such, I would wait until the end of 2023 at least before re-evaluating the company's progress, checking to see if management has delivered on its goal of submitting its acoramidis NDA before the end of the year, and looking at the funding position.

For further details see:

BridgeBio: Positive Updated Acoramidis Data May Not Imply Further Upside