BRDCF - Bridgestone Starts Seeing Destocking Trends Near Year's End

2023-04-21 07:43:53 ET

Summary

- Bridgestone's weak Q4 demand for general tires in US and Europe signals that dealers aren't confident about continued pent-up demand for automotive mobility.

- We think the yen could come back online and that will hurt Bridgestone's relative appeal to more Japan-focused stocks, as well as its absolute earnings power.

- There is a strong long-term thesis around electrification that we think investors should keep in mind, especially considering the current Bridgestone PE.

- However, with the price still at average levels within its typical range, we don't see it as an attractive proposition at this point in time.

Bridgestone Corporation ( OTCPK:BRDCY ) is one of the leading tire brands in the world and a Japanese stalwart. In its latest results we see softening demand despite continued new vehicle sales, which signals that probably in addition to destocking trends, tire dealers aren't confident in mobility, replacement rates and continued demand for automotive that for the moment is supported by pent-up demand. There are long-term trends around electrification: cars will get heavier as we electrify vehicles and wear out tires quicker. While a solid thesis for the long term, Bridgestone is at average levels in USD terms considering the softening outlook as well as a potential rally in the yen are all negative incremental forces for the company. We think a 5% medium-term pullback is warranted, where it should trade below it's typical average.

FY Comments

Almost 50% of Bridgestone's business is in the US. With the Fed hiking rates, the USD rallied relative to the JPY this year and this had a pretty major positive currency effect on Bridgestone's JPY denominated results. With the plurality of income coming from USD, a stronger USD is relatively better for Bridgestone than a stronger Yen.

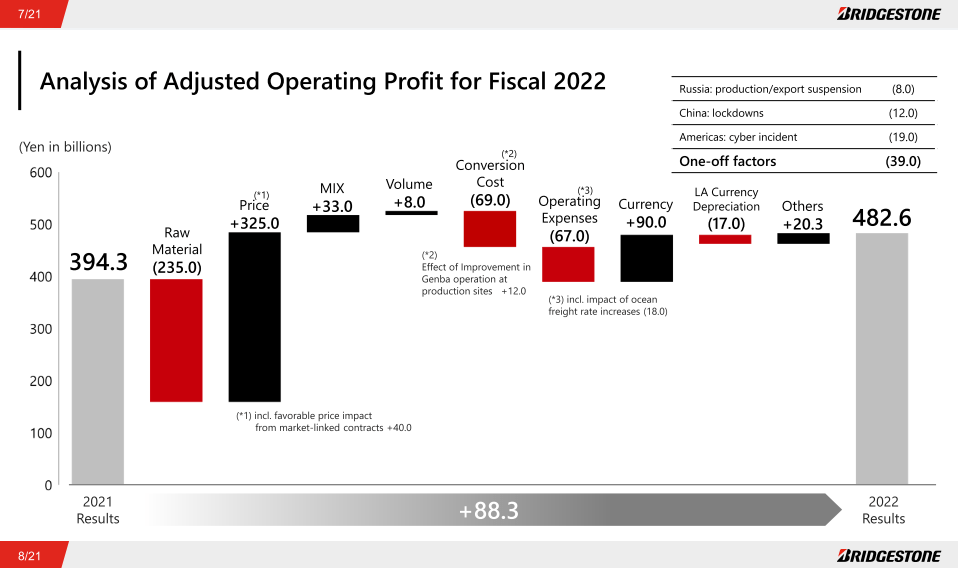

Operating Profit Waterfall (FY 2022 Pres)

{kind=link}

Otherwise, with the return of automotive volumes after the end of semiconductor shortages, tire sales to new vehicles actually made a recovery in the latter half of the year supporting volume demand. This also meant that a lot of tire inventory was liquidated upfront putting pressure on price to cost ratios, with inflation throughout 2022 really making itself known towards the end of the year's unit economics.

All of the cost effects were still offset with pricing initiatives, which preserved profits, but conditions seem to be deteriorating now and potentially deflationary effects could kick in.

Dealers are apparently slowing demand meaningfully in Q4 in restocking. While this may have to do with a general destocking trend going on across most industries that were concerned with shoring up their supply, it also comes from recessionary pressures cropping up in Europe and the US in particular. Volumes to Russia, which is part of the EMEA business, obviously collapsed with the Russian export suspension. The impact was about 2% headwind to operating profit, with lockdowns in China being 3%.

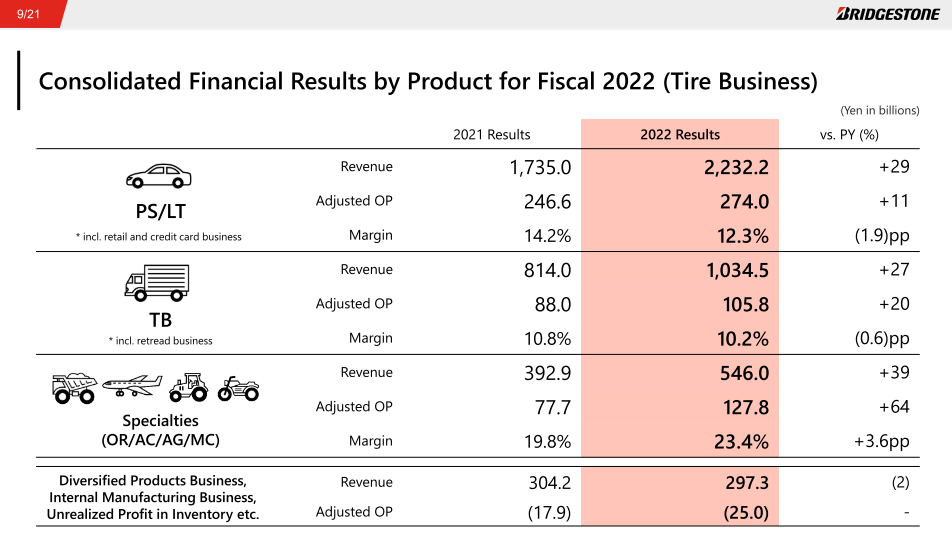

Bucking this weaker demand trend were premium and specialty tires, as well as premium passenger and light vehicle truck tires, which saw relatively healthy Q4 demand, where in premium tires Bridgestone won share throughout the year and specialty tires saw continued strength due to activity in industrial markets like mining, and a recovery in aviation tire demand which has been a drag for years now with lower air mobility.

Just the tire market (FY 2022 Pres)

{kind=link}

Premium tires for trucks and buses and passenger cars remained strong in North America, and this will likely continue to be a resilient segment that should also hold price. Although management believes that recoveries in tire markets generally should become visible as soon as in Q2, which we are not so sure about.

Outlook

We think there are two principal problems for Bridgestone on a go-forward basis. Appreciation of the Yen won't be such a great thing for the company, and with cracks showing in the financial system as well as evidence of recessionary pressures, the lessened need for further rate hikes in competing economies is likely to turn demand back to the Yen whose yields hadn't risen at all, but may start after other countries start to roll back their rate hiking. With the plurality of Bridgestone's income being in USD, even Bridgestone's converted price is helped by a stronger rather than weaker dollar with JPY to USD denominated revenue being 1:2. Recessionary pressures are the other issue, and while OE demand remains good due to the end of semiconductor shortages, the destocking may signal that dealers are not optimistic about how many more cars will be on the market, or at least mobile on roads, as the recession takes greater hold. The Q2 recovery in tire markets could be optimistic, especially if the recession proves to be long and drawn out, albeit perhaps not so deep.

Investors should be optimistic about the long-term tire thesis, which we believe is relatively strong and a stealthy way to play cousin to a direct EV bet. With heavier BEV cars wearing tires faster, the velocity of tire demand could improve dramatically. At around 10x PE, that is quite an attractive proposition since long term earnings growth prospects are likely greater than the market's earnings.

However, we think that raw material prices, in particular commodity prices, may not budge as much as price could if destocking continues and tire demand grows weaker. While premium and specialty tires' pricing power will mean that average prices should stay high enough to avoid very meaningful profit erosion from the price side, the bulk of tire demand can't be expected to be good as we get an interest rate and financial system-led recession, and further pricing benefits should not be extrapolated.

Bridgestone is a little in the way of current trends, with the Yen being the most likely problem and deflation being the least, but still all possible headwinds with almost no case for any more improvement from an excellent FY showing. Better to avoid it, especially as in USD terms the stock price is actually trading around average levels in its typical range. Downside, or at least limited upside, is quite reasonable to expect at this point.

For further details see:

Bridgestone Starts Seeing Destocking Trends Near Year's End