BWB - Bridgewater Bancshares: An Excellent Prospect In The Banking Sector

2023-08-31 21:37:52 ET

Summary

- Bridgewater Bancshares is a strong buy candidate despite weakness in revenue and earnings, with robust deposits and cheap shares.

- The company has a growing loan portfolio, with a focus on commercial and industrial loans and little office exposure.

- The value of deposits has increased, and the company has successfully reduced exposure to uninsured deposits.

Ever since the banking crisis earlier this year, I have been looking for players in the space that are worthy of the ‘strong buy’ rating. Most of the companies that I have covered in recent months seemed to fall under either the ‘hold’ category or the ‘buy’ category. But in Bridgewater Bancshares ( BWB ), I do feel confident that I have found that's super special and rare ‘strong buy’ candidate. Although the company is experiencing a bit of weakness from a revenue and earnings perspective so far this year, its deposits are robust and shares are cheap. Debt, while elevated, is not at dangerous levels and the institution has significantly reduced its exposure to uninsured deposits. Add all of these factors together, and I think we have a great prospect for long term, value-oriented investors to consider.

A great prospect

Operationally speaking, Bridgewater Bancshares is a financial holding company that's based out of Minnesota that operates both a bank and a captive insurance entity. Through its 7 branches, the company provides its customers with a wide array of services. These include, but are not limited to, loans that can be utilized for the purchase of residential properties, non-owner-occupied single-family properties, multifamily properties, construction projects, land development, and more.

Management's focus in recent years has been on growing its exposure to the commercial and industrial spaces. They have done this by offering up a variety of loan types to its customers, such as term equipment loans, revolving lines of credit, etc.... I mentioned earlier in this paragraph a captive insurance company under its umbrella as well. But this is not what you might think it is. That business does not engage with outside customers. Instead, it merely provides insurance coverage to its parent company in order for said business to more appropriately manage its risks.

{kind=link}

Author - SEC EDGAR Data

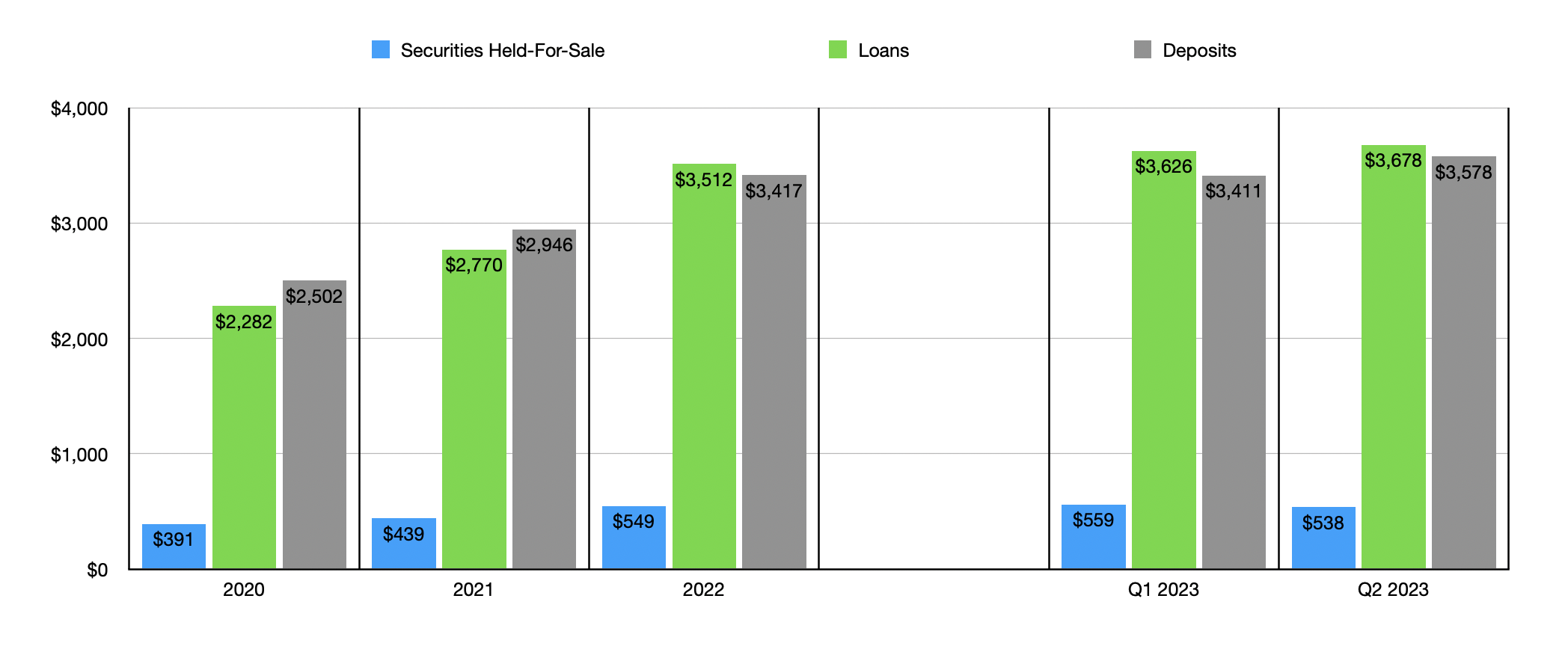

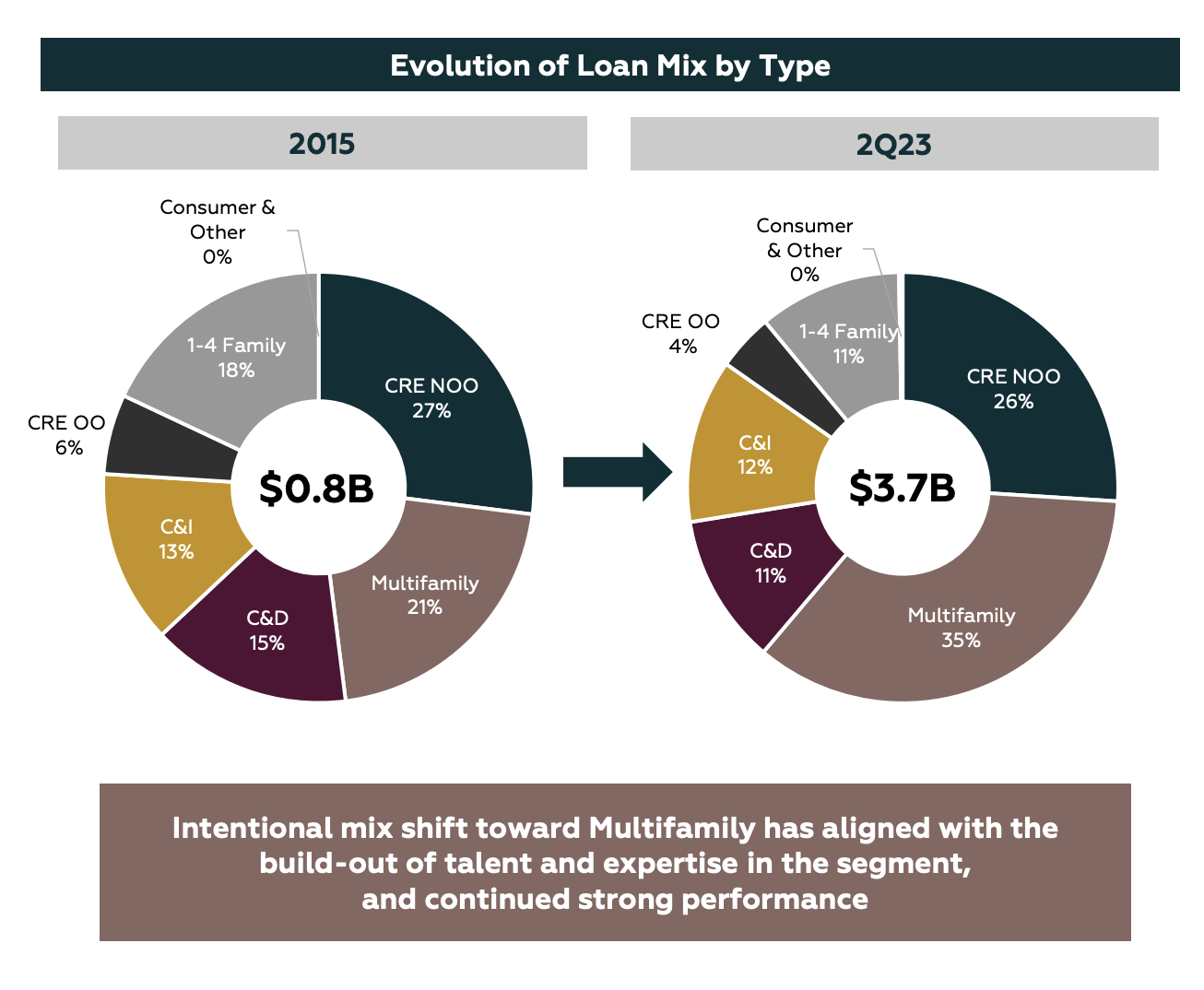

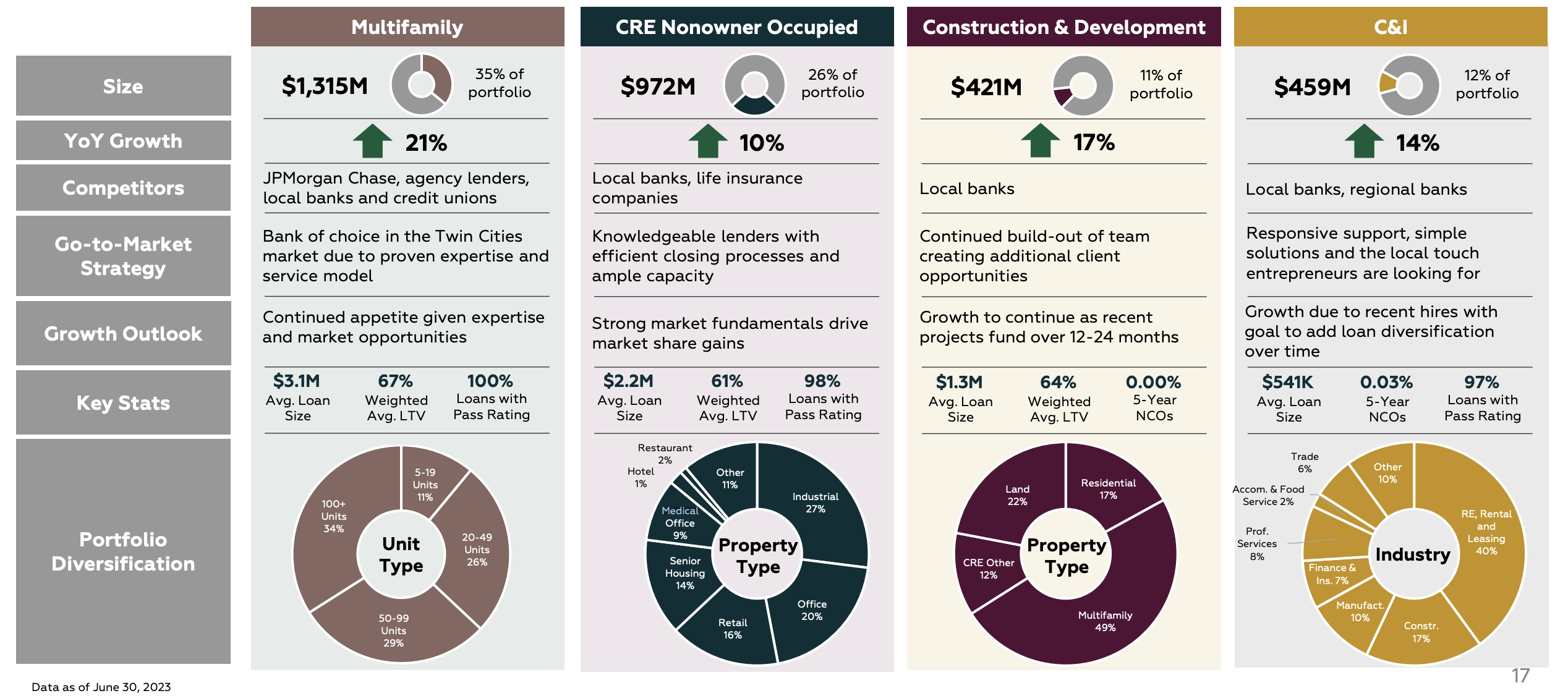

In recent years, the firm has seen the value of its loans increase. Its loan portfolio grew from $2.28 billion in 2020 to $3.51 billion in 2022. We saw a further increase to $3.68 billion by the end of the second quarter of this year. At present, 35% of the company's loans, by value, fall under the multifamily category. This is followed by the 26% attributable to the non-owner occupied commercial real estate market. And in third place, we have commercial and industrial loans at 12%. The one area that investors seem to be worried about most when it comes to loan exposure involves office properties. And with a high amount of its portfolio and commercial real estate, I can understand the need to have a deeper look on this front. The good news is that about 20% of the value of the company's non owner occupied commercial real estate, or about 5.3% of the firm’s overall loan portfolio, is in the form of office properties. This does exclude another 2.4% that's attributable to medical office assets.

{kind=link}

Bridgewater Bancshares

{kind=link}

Bridgewater Bancshares

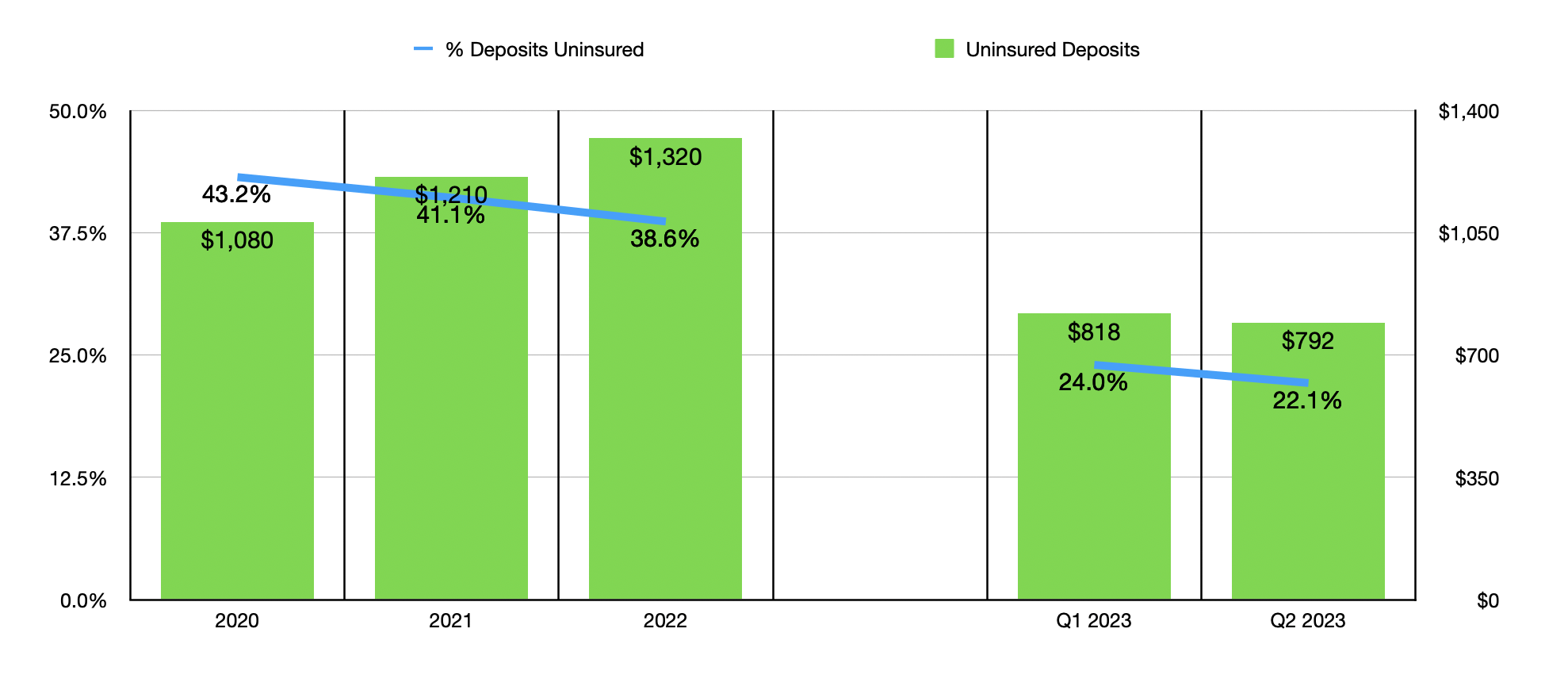

The value of the company's loan portfolio has only been able to increase thanks to a growing deposit base. From 2020 to 2022 , deposits shot up from $2.50 billion to $3.42 billion. During the banking crisis, the company saw almost no decline in the value of its deposits. From the final quarter of last year to the end of the first quarter of this year, it saw deposits drop only $5.4 million. This was followed up by a $166.8 million increase in deposits by the end of the second quarter. Along the way, management has also been successful in decreasing exposure to uninsured deposits. At the end of 2020, 43.2% of the company's deposits were uninsured. This number declined to 38.6% by the end of last year. As of the second quarter of this year , this number has dropped further to 22.1%. The lower this number is, the better. But my cut off point between a healthy firm with little risk and one that's riskier is 30%.

{kind=link}

Author - SEC EDGAR Data

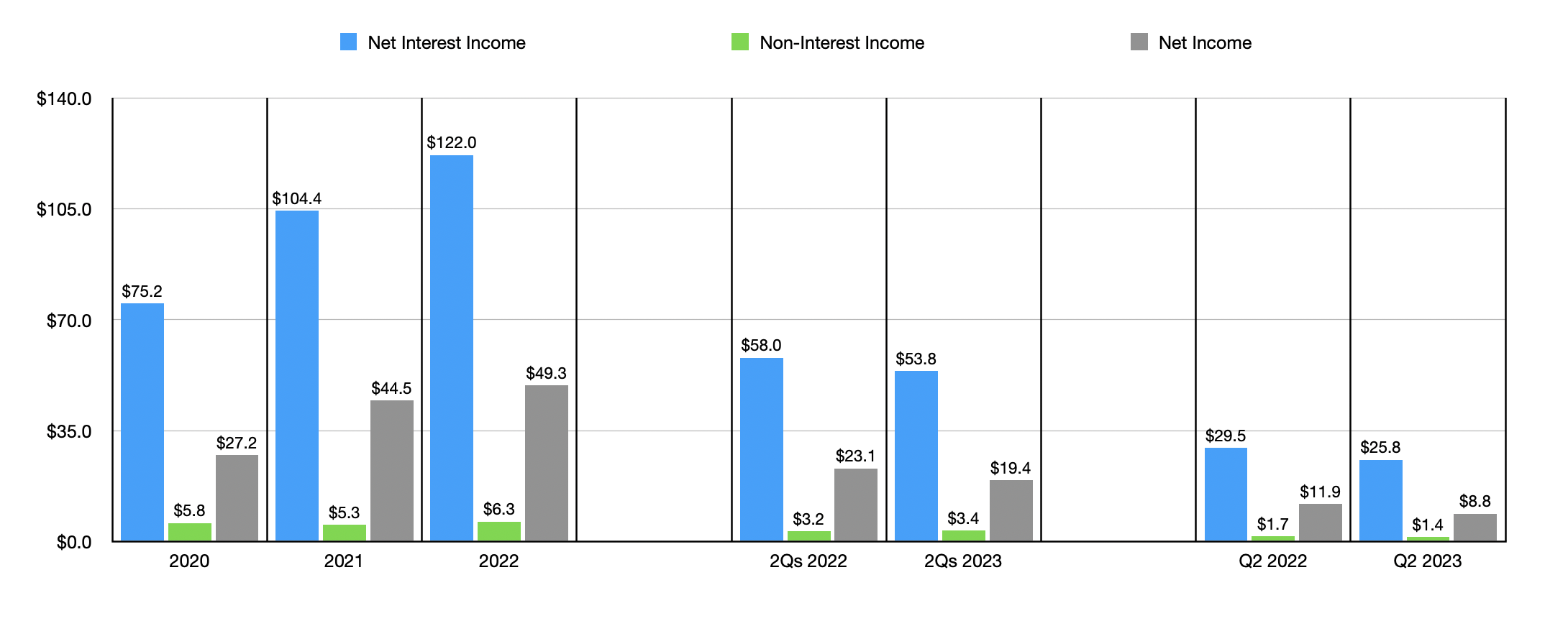

Over the three years ending in 2022, financial performance for the business had been quite impressive. Net interest income, for instance, grew from $75.2 million to $122 million. Non-interest income inched up from $5.8 million to $6.3 million. These increases allowed the company to grow its bottom line substantially. Net income nearly doubled from $27.2 million in 2020 to $49.3 million last year. The picture has not been quite as appealing when we look at the current fiscal year. As you can see in the chart below, net interest income and net profits as a whole weakened both in the first half of the 2023 fiscal year in its entirety relative to the same time last year, and in the most recent quarter alone.

{kind=link}

Author - SEC EDGAR Data

Even though the value of loans on the company's books increased and the value of deposits grew also, profitability took a hit because of higher interest expense. The biggest problem involved interest that the company had to pay on its deposits, which, in the first half of this year, totaled $39.4 million compared to the $6.6 million reported one year earlier. In addition to having to pay higher interest rates on regular deposits in order to keep depositor funds in the institution, the company also saw funds flow into savings and money market funds that tend to be less profitable than interest bearing transaction deposits. And it also saw a surge in brokered deposits, alongside a rise in the yield that the company paid on those assets from 0.90% to 3.53%.

It is unclear how long these circumstances will last. But very likely, interest rates will start declining sometime next year. That should take the pain off the company. Another thing that might help is debt reduction. At the end of the most recent quarter, the company had gross debt of $549.8 million. That's almost double the $289.8 million reported for the first quarter of this year and it is significantly higher than the $189.7 million reported at the end of 2022. The company does have plenty of liquidity on hand in order to address this debt. So this is not something I am terribly concerned about. But paying it down might help decrease costs.

{kind=link}

Author - SEC EDGAR Data

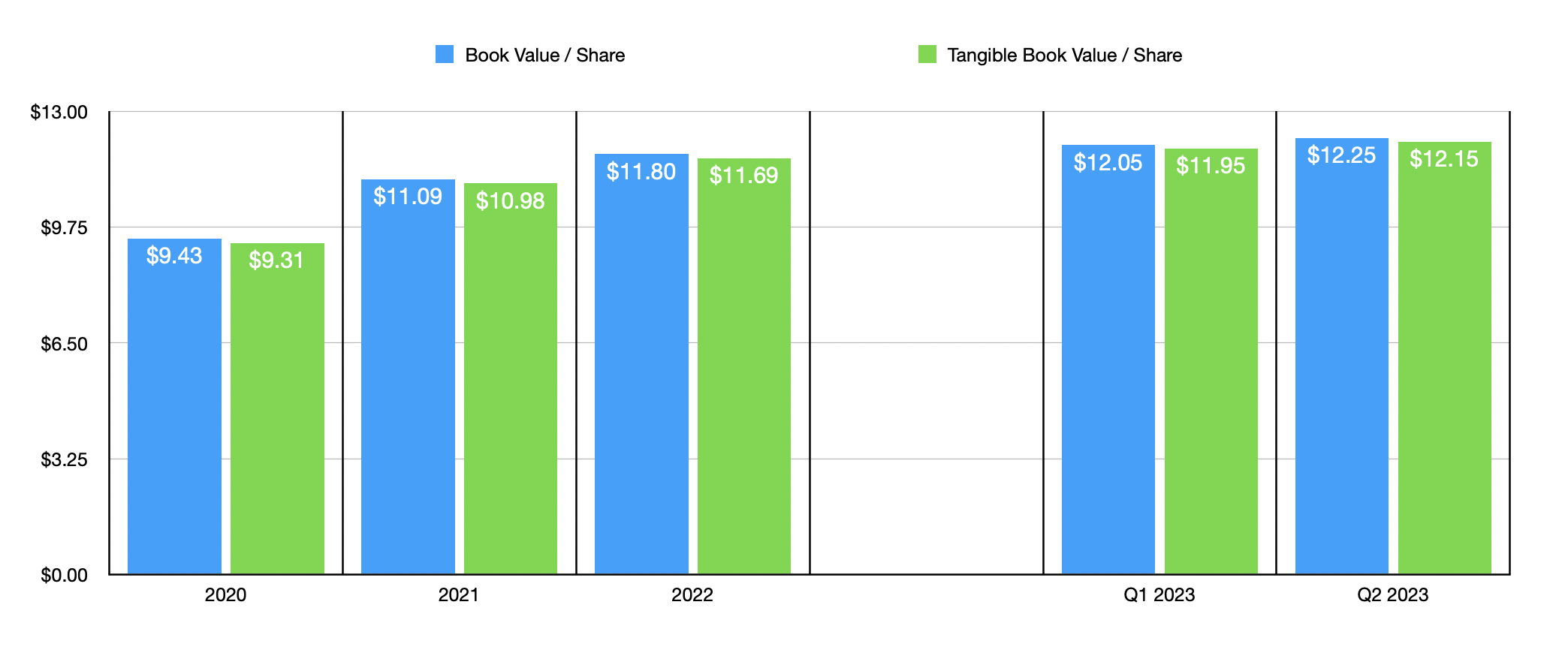

Another thing that's noteworthy is that, in recent years, management has been successful in growing the company's book value per share and tangible book value per share. Book value per share went from $9.43 at the end of 2020 to $12.25 in the most recent quarter of this year. Tangible book value per share followed a very similar trajectory from $9.31 to $12.15. Given the $10.25 that shares are currently trading at, this means that the company is going for 15.6% less than its tangible book value per share. And if we use financial results from 2022, the business is trading at a price to earnings multiple of only 5.8.

Takeaway

From the data that I see, I must admit that I am impressed. Right now, shares of the company look very attractive and the business seems to be rather solid. I would like to see debt come down, but where it is does not constitute a deal breaker. I find it perplexing that, given the health of the company, shares are still down 29.5% compared to where they ended February of this year at. Admittedly, this is a massive improvement over the 46.3% that shares dropped from that point until they bottomed out earlier this year. But I would not expect a recovery to have taken as long as it has. Given these factors, I do believe that a ‘strong buy’ rating is appropriate for Bridgewater Bancshares at this time.

For further details see:

Bridgewater Bancshares: An Excellent Prospect In The Banking Sector