BWB - Bridgewater Bancshares: Fundamentally Sound On Troubled Waters But Overvalued

Summary

- Bridgewater Bancshares, Inc. sees sustained revenue growth but squeezed margins.

- Its financial positioning remains robust, but it must watch out for its borrowings.

- The recent stock price downtrend opens a potential entry point for investors.

Bridgewater Bancshares, Inc. ( BWB ) shows decent results amidst market volatility. Interest rate hikes pushed revenues up but squeezed margins. Even so, its viability stays high to sustain its operations. Also, its liquidity position stays sound. But it has to watch out for its loan-deposit ratio and borrowings. It is a crucial factor to consider as interest rates continue to increase. Cash levels have remained adequate in the last year. More importantly, asset quality is superb, with lower non-performing assets.

Meanwhile, the stock price had a noticeable YTD downtrend. It is slightly divorced from fundamentals. The pessimism appears reasonable, given the higher risks and lower-than-expected 4Q earnings . As such, investors must watch out for the potential overvaluation of the stock.

Company Performance

Bridgewater Bancshares, Inc. operates in a highly cyclical industry. Despite this, it remains successful in sustaining growth while remaining viable. In fact, the past two years have become a stepping stone toward its expansion. Today, it shows its robust performance while cautiously navigating the rugged market. It does not entirely benefit from interest rate hikes, but opportunities are present.

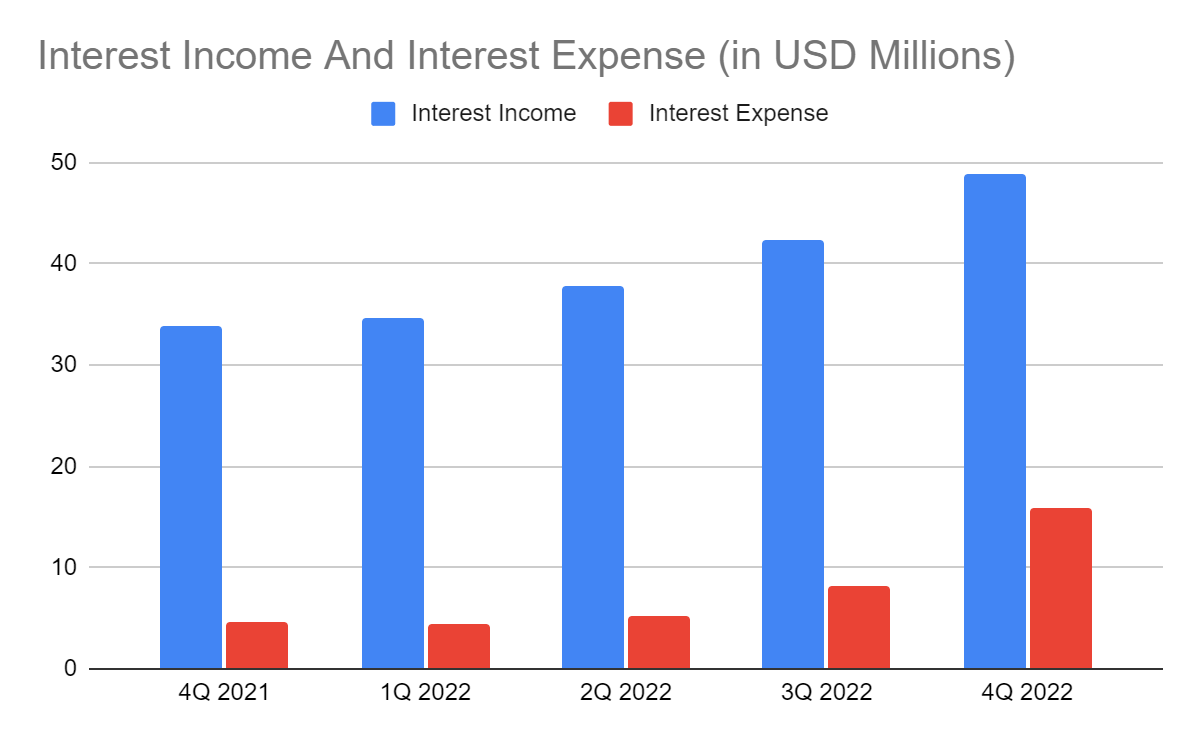

The core operating revenue in 4Q 2022 amounted to $48.9 million , a 44% year-over-year growth. It consists of interest income from loans, investments, and other interest-bearing assets. So, BWB's earning assets have been well-diversified and efficiently managed. But we can attribute this robust growth to several factors. First, its loan portfolio was managed with more prudence. Thanks to its solid brand presence and customer relationships, these helped it secure high-quality deals. Also, a considerable portion of its loan portfolio is real estate loans. This segment can be risky yet rosy. Note that construction already increased by 17% in mid-4Q 2022. But given the cooling property sales, we must anticipate a potential slowdown.

I will discuss more of this part in the next section. What was most striking was the company's conservative approach to loans. It focused more on ensuring high credit-quality transactions. And although it compromised loan deal volumes, it could help limit loan delinquencies. Overall, loan demand has declined in line with interest rate hikes. Originations and advances have slowed down by 13%. But thanks to its disciplined loan pricing, which goes along with market volatility, it also led to a reduction in payoffs by 37%. As such, loans are still higher than in the comparative quarter.

Interest Income And Interest Expense (MarketWatch)

{kind=link}

Another aspect to consider is BWB's prudent diversification of investment securities. A substantial portion of investments is government-backed securities. Since these are more suitable in a high-interest environment, yields are more stable. Investment income in 4Q was more than twice its value last year. With a full-year value of $16.41 million , yields rose from 2.1% to 3%. This year, interest rate hikes may continue to stabilize inflation further. But increments may continue to slow down, which started with only a 25 bps increment . With that, it may be wise to increase its concentration on government securities.

However, interest rate hikes also raised interest expenses. The current amount of $15.97 is already 300% higher than in 4Q 2021. So, it quickly offset the increase in interest income. Also, it now comprises 33% of interest income, squeezing the net interest income margin. We can attribute it to deposit growth outpacing loan growth. Note that growth is not linear, given the increased deposits and interest rate hikes. It may become more challenging this year as costs increase further. Although it has means for lending and investments, deposits yield faster than them.

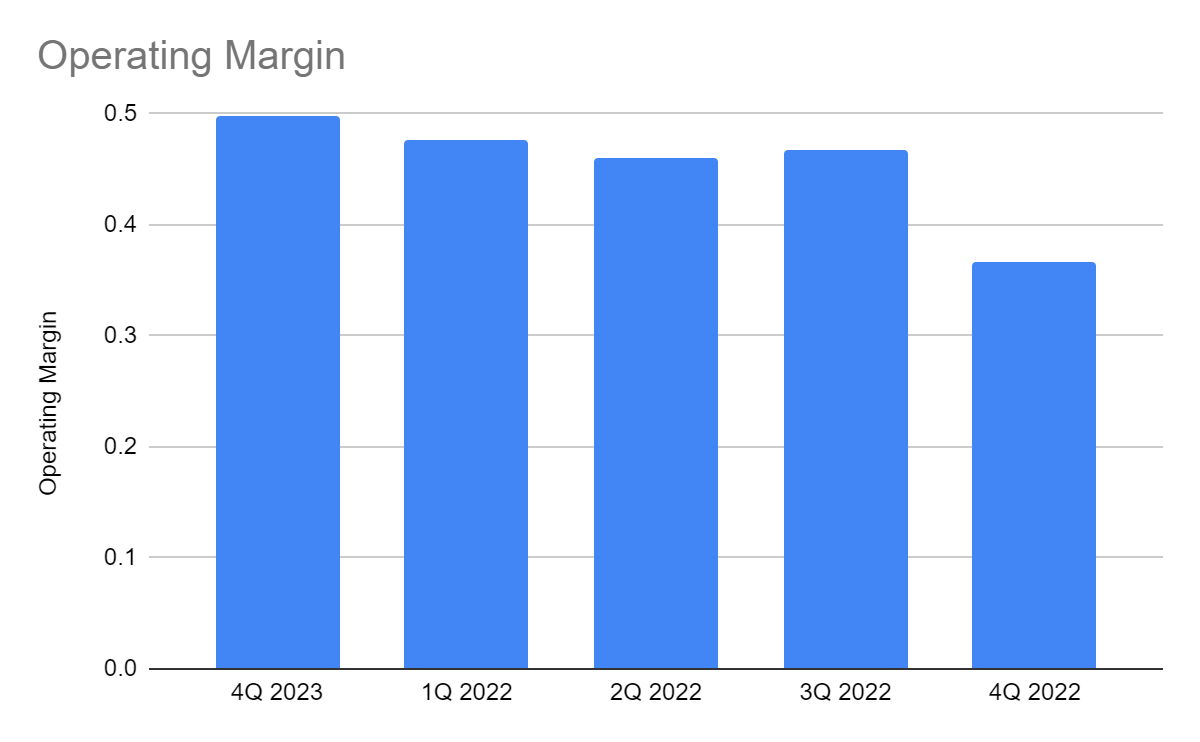

Thankfully, its non-interest segments are more stable today as inflation continues to relax. With higher-quality transactions, non-interest income continues to increase. Non-interest expenses are also increasing but still manageable. The increase in labor expenses has slowed down. Unfortunately, the massive increase in interest expense could not be offset. The operating margin dropped from 50% to 37%. On a lighter note, the company's viability could sustain its operations. The actual value was still higher by more than $1 million. So, amidst the mixed operating results, Bridgewater stock maintains a robust performance.

Operating Margin (MarketWatch)

{kind=link}

How Bridgewater Bancshares May Remain Stable This Year

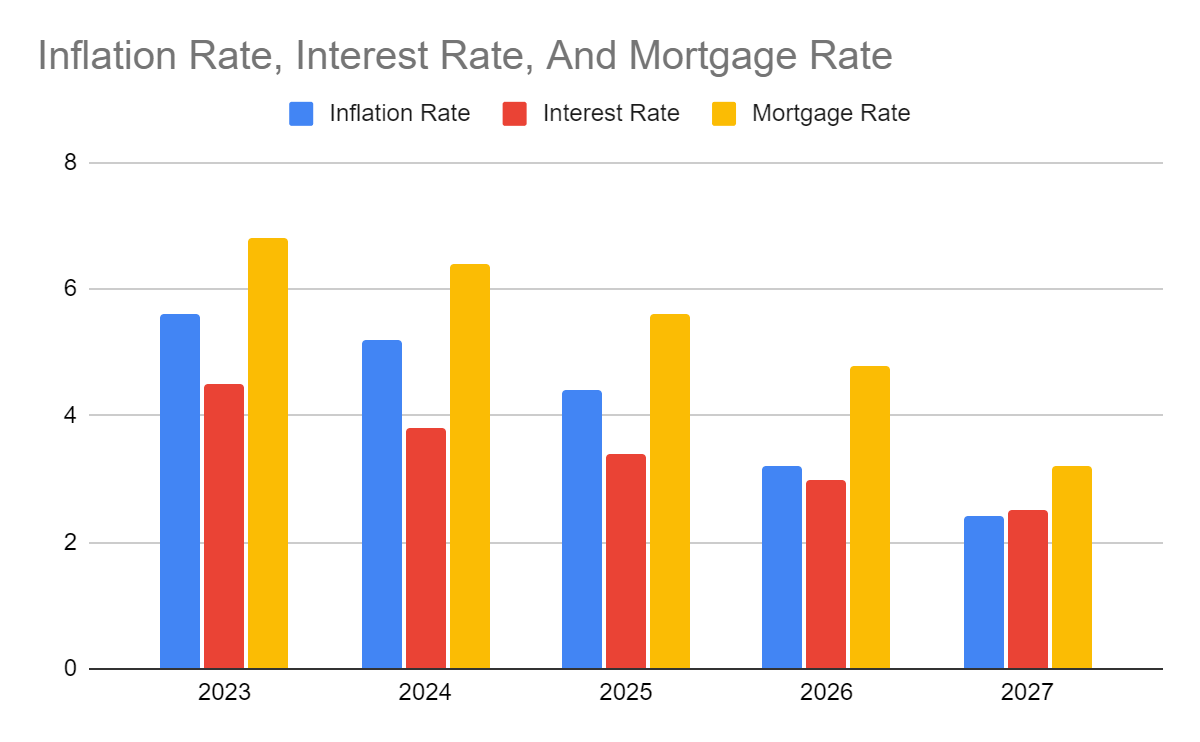

Bridgewater had a fruitful 2022 but must prepare for an economic slowdown. With the lower loan originations and advances, BWB must beware of interest rate hikes. It must also keep a keen eye on higher costs of deposits and borrowings. Despite this, interest rate increases may be more manageable than expected. Note that inflation has started to relax in 3Q 2022. From its 9.1% peak , it is now 6.4%, or a 29% difference. With that, I expect interest rate increments to cool down this year. In fact, the Fed has raised its benchmark rate by 25 bps only recently after the 75 bps increment for four consecutive quarters. Interest rates may stabilize if inflation continues to decrease. In turn, it may be easier for the company to manage its loans, deposits, investments, and borrowings.

Inflation Rate, Interest Rate, And Mortgage Rate (Author Estimation)

{kind=link}

Also, home sales and mortgage rates are cooling down. This aspect is crucial since real estate loans comprise the majority of the total loans. But I don't expect a sharp crash in the real estate market:

- The property value may stay valuable as shortages remain high. House inventories are still low, which we can point to builders not ramping up over the past decade.

- Unlike in the Real Estate Bubble, no unethical practices and speculative mania exist.

- The unemployment rate is still low.

All these aspects show that the market remains stable. Also, there may be an economic slowdown but not a deep recession. So while I expect BWB to be less robust this year, revenues and margins may remain manageable.

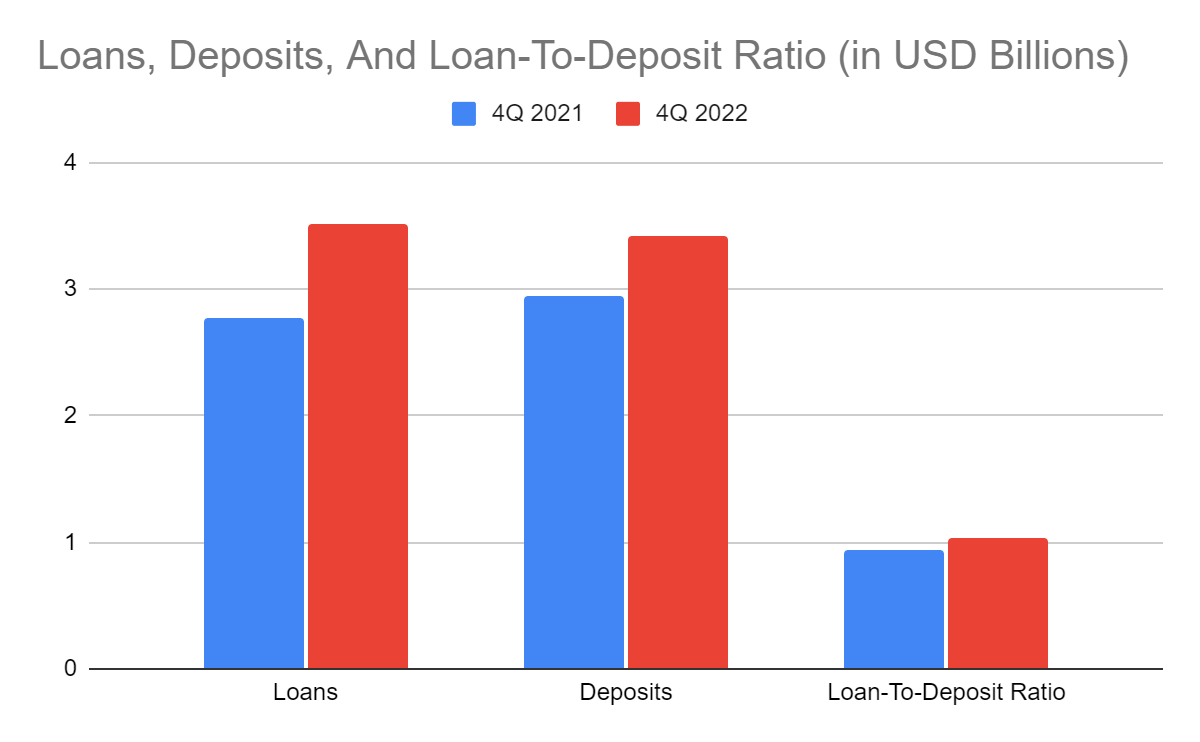

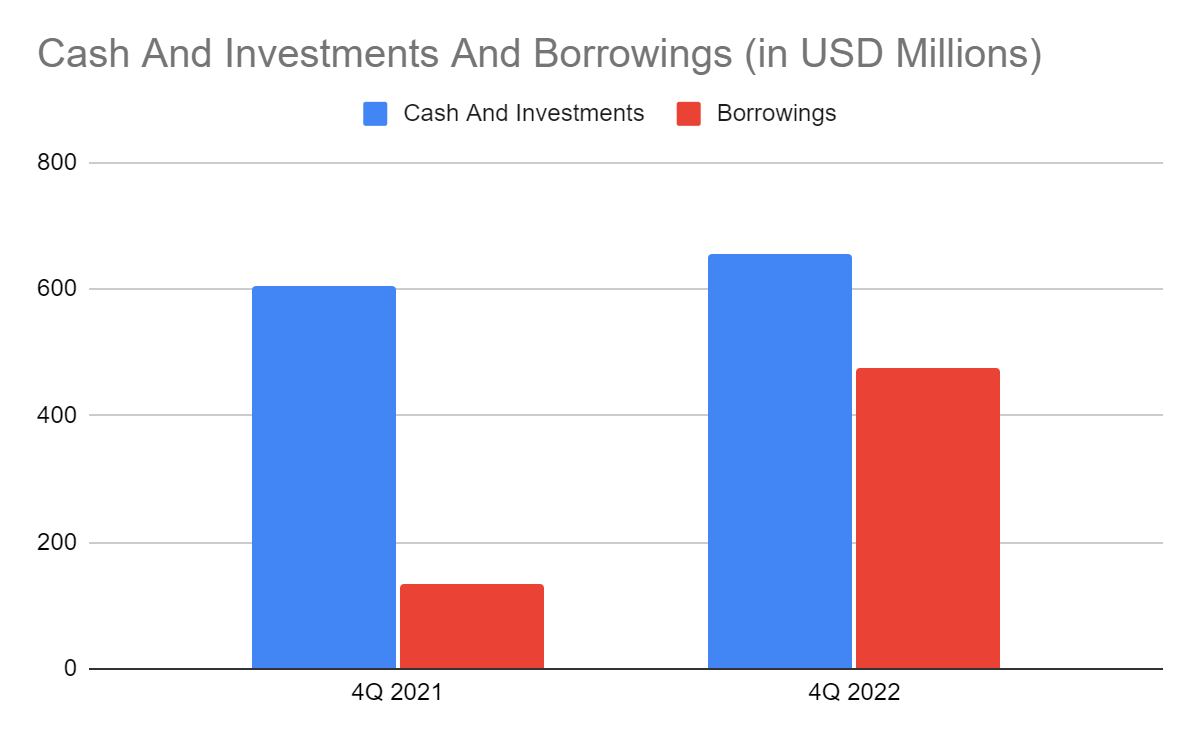

Meanwhile, Bridgewater Bancshares, Inc. shows decent liquidity levels. Loan growth stays solid as lower payoffs offset lower originations and advances. Loan pricing is strategic to sustain interest income. My only concern is the high loan-to-deposit ratio of 103%. It can limit its reserves if there are defaults or delinquencies. Fortunately, it stays conservative with its allowances for credit losses of 1.37%. It can also attract more customers through deposits to improve liquidity. It may not be that simple, but it is feasible since interest rate increases may cool down this year. Moreover, cash and investments continue to increase. Their combined value comprises 16% of the total assets, making it a fairly liquid company. Also, they can cover borrowings. But it must be careful since borrowings tripled in only a year. Overall, BWB shows a decent financial positioning.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

{kind=link}

Cash And Investments And Borrowings (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of Bridgewater Bancshares, Inc. has been in a downtrend since 4Q 2022. But it became sharper after the release of the 4Q report. At $14.95, it has been cut by 14% from last year's value. It may be reasonable since analysts' estimates are pessimistic about its earnings. If we multiply the PE multiple of 8.79x and the estimated EPS of $1.52, the target price will be $13.36. On the contrary, the book value of the company shows potential undervaluation. Its book value keeps increasing, giving a BVPS of 11.7 and a PB Ratio of 1.4x. If we multiply the current BVPS and the 2019-2022 PB Ratio average of 1.41x, the target price will be $16.53. To assess the stock price better, we will use the discounted cash flow ("DCF") Model.

FCFF $32,000,000

Cash $87,000,000

Borrowings $476,000,000

Perpetual Growth Rate 4.8%

WACC 8.2%

Common Shares Outstanding 27,752,000

Stock Price $14.95

Derived Value $12.19

The derived value shows that the stock price has potential overvaluation. The Bridgewater Bancshares, Inc. stock price is still higher than the intrinsic value of the company. There may be a 19% downside in the next 12-18 months.

Bottom Line

Bridgewater Bancshares, Inc. sustains its larger capacity despite the squeezed margins. It has a decent financial positioning, driven by impressive earning asset quality. Bridgewater Bancshares, Inc.'s liquidity shows it can withstand market headwinds while covering its core operations. However, the Bridgewater Bancshares, Inc. stock price appears overvalued and does not reflect its intrinsic value. The recommendation, for now, is that Bridgewater Bancshares, Inc. stock is a hold.

For further details see:

Bridgewater Bancshares: Fundamentally Sound On Troubled Waters But Overvalued