BRID - Bridgford Foods: A Strong Balance Sheet Should Help It Navigate Current Headwinds

2023-05-15 13:00:21 ET

Summary

- Net sales have increased at a relatively fast pace over the years.

- Margins are under pressure due to high inflation rates and increased production and transportation costs.

- The company's balance sheet is very robust thanks to low debt and high cash and equivalents and inventories.

- Buybacks will likely be kept on hold for the foreseeable future due to negative cash from operations.

- The recent price decline represents a good opportunity to acquire shares at reasonable prices.

Investment thesis

We, as investors, are used to seeing companies that in order to grow make intensive use of debt to perform acquisitions and expand their operations, but Bridgford Foods ( BRID ) has achieved very acceptable growth rates over the past few years with almost non-existent debt on its balance sheet as it expands its offerings through new product launches.

Despite this, gross profit and EBITDA margins have deteriorated in recent years, and this weakening has accelerated in the past few quarters as a result of inflationary pressures, higher labor costs, increased transportation costs, and declining purchasing power among consumers. These headwinds frustrated investors and caused a significant drop in the share price as the company pays no dividends and share buybacks have been on hold since 2016.

Still, I strongly believe that these headwinds are temporary as they are directly linked to the current macroeconomic landscape and that the company is prepared to withstand them, and even a potential recession, for a very, very long time thanks to its very strong balance sheet as inventories and cash and equivalents are currently very high. Furthermore, the company has recently modernized one of its two factories located in Chicago and sold the other, which should significantly improve profit margins once the current headwinds subside. For these reasons, I consider that the recent share price decline represents a good opportunity for acquiring shares at reasonable prices as the upside potential is high.

A brief overview of the company

Bridgford Foods is a manufacturer and distributor of snacks and frozen foods, including biscuits, bread dough items, roll dough items, dry sausage products, and beef jerky that operates for retailers and food service companies. The company was founded in 1932 and its market cap currently stands at ~$112 million, employing around 700 workers.

The company operates under two business segments: Frozen Food Products and Snack Food Products. Under the Snack Food Products segment, which provided 79% of the company's net sales in fiscal 2022, the company sells around 160 different products through customer-owned distribution centers and a direct-store-delivery network serving approximately 20,000 supermarkets, mass merchandise, and convenience retail stores located in 50 states. These products include, among others, pepperoni, beef jerky, summer sausages, salami, and other meat snacks. And under the Frozen Foods Products segment, which provided 21% of total net sales in fiscal 2022, the company sells 130 unique frozen food products through approximately 800 wholesalers, cooperatives, and distributors, as well as restaurants, the food operations of health care providers, schools, hotels, resorts, corporations, and other traditional and non-traditional food service outlets.

Currently, shares are trading at $12.43, which represents a 67.29% decline from all-time highs of $38.00 in July 2019. This represents a very significant drop after a ~150% surge from July 2018 to July 2019, caused mainly by margin pressures as net sales are stabilizing at high figures.

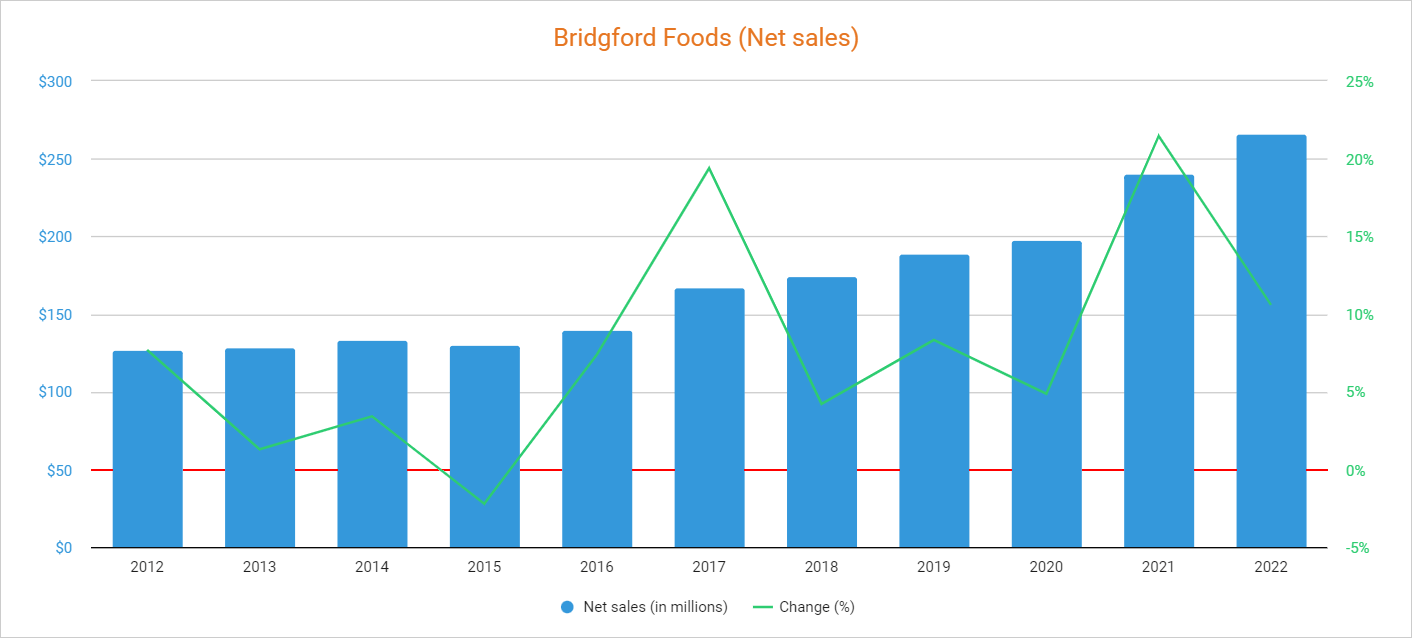

Net sales have increased over the years but are showing signs of stabilization

The company has achieved very acceptable net sales growth over the years, and it has achieved this without using debt to make major acquisitions, which says a lot about the company's ability to expand sales from its own product portfolio. In this regard, net sales increased by 109% from fiscal 2012 to fiscal 2022 but declined by 3.84% year over year during the first quarter of fiscal 2023. Even so, we must not forget that fiscal 2021 and 2022 were strong years as net sales increased by 21.45% and 10.59%, respectively. Therefore, in my opinion, a weak retracement is not a cause for alarm.

{kind=link}

Although the balance sheet is currently very robust, no acquisitions are expected to take place as the company has no M&A strategy and relies on new product launches and expansion of its customer base to increase sales, but the recent decline in the share price coupled with ever-growing net sales has caused a steep decline in the P/S ratio to 0.428, which means the company currently generates net sales of $2.34 for each dollar held in shares by investors, annually.

This ratio is 42.63% lower than the average of the past 10 years and represents a 76.41% decline from the peak of 1.814 reached in 2019. This shows a relatively high degree of pessimism among investors as they are placing less value on the company's sales due to signs of sales stabilization after a boost in recent years and an ongoing margin contraction as a consequence of inflationary pressures and increased transportation costs. Furthermore, there is a growing concern about a potential recession due to recent interest rate hikes carried out in order to put an end to high inflation rates in the economy. Still, the management has not stood idly by and has already taken steps to improve profit margins in the long run.

Margin deterioration is a concern, but the management has already taken action

The company's gross profit and EBITDA margins have shown continued deterioration over the years, and this is a true cause of concern. During the first quarter of fiscal 2023, the company reported a gross profit margin of 27.69% and an EBITDA margin of 4.71%, and cash from operations has reached negative levels as the company has increased its inventories and cash and equivalents.

In this regard, the company's trailing twelve months' cash from operations stands at -$9.12 million, and although inventories also decreased by $0.4 million during this time, accounts receivable increased by $6.1 million while accounts payable declined by $5 million, which means cash from operations should be higher in the coming quarters. As for the first quarter of fiscal 2023, cash from operations remained negative at -$2.6 million, inventories declined by $1.7 million, and accounts receivable decreased by $1.8 million, but accounts payable also declined by $4.6 million. This means that profitability issues remain a concern and that they will need to be addressed sooner or later. The problem is that, as a result of negative cash from operations, cash and equivalents decreased by $3.3 million during the quarter, which means high inflation rates (and a slight decline in volumes) are currently putting pressure on the company's balance sheet. Luckily, the balance sheet remains robust, which will most likely give the company enough margin to withstand current (and potential) headwinds. Also, capital expenditures decreased as the company finished modernization investments in its remaining Chicago manufacturing facility, which should provide significant margin expansion once current headwinds ease.

In this regard, the company sold its Chicago, Illinois 156,000 square feet manufacturing facility in July 2022 following the modernization of its other 177,000 square feet factory also located in Chicago in order to offset part of the impact from current inflationary headwinds and improve profit margins in the long run, which should give results in the form of stronger profit margins as soon as current inflationary pressures subside.

The balance sheet is very robust

The company's balance sheet is very strong thanks to a virtually non-existent long-term debt as cash and equivalents of $12.99 million and inventories of $38.82 million are significantly higher than the long-term debt of $4.67 million.

The company has managed to empty part of its inventories in the last two quarters ($1.5 million in the fourth quarter of fiscal 2022 and $1.7 million during the first quarter of fiscal 2023), which has allowed it to cushion much of the impact derived from high inflation rates. In this sense, high inventories and cash and equivalents will allow the company to continue navigating the ongoing headwinds for a very long time, but some margin improvement will be eventually necessary for the company to return to profitability as the balance sheet could continue to deteriorate if margins continue at current levels, and for this to happen high inflation rates will need to be relaxed. The problem is that the solution to inflationary pressures is not easy since ongoing interest rate hikes could drive the economy into a recession that could put even more pressure on profit margins and, therefore, continue to damage the balance sheet until the economy stabilizes.

That is why volatility will likely continue for a few more quarters and why the stock price has fallen so significantly. And although I consider this a good opportunity to acquire shares at reasonable prices due to low P/S ratios, a strong balance sheet, and strong investments in factory modernization, it will be necessary to have an exit plan as the company pays no dividends and share buybacks will likely remain on hold for more years.

Share buybacks are on hold

Until 2016, the company rewarded shareholders through share buybacks, which had the goal of reducing the total number of shares outstanding and effectively passively enlarged the holdings of investors as each share represented an increasing size of the company. This was a reasonable incentive to hold the company's shares since as the company grew, per-share metrics improved even faster as they are now calculated among fewer shares.

Had it not been for the contraction in margins that the company has suffered in recent years, it would likely have continued making share buybacks. But even tighter margins due to current headwinds suggest that no share buybacks will take place in the foreseeable future.

Risks worth mentioning

Overall, I consider Bridgford Foods' risk profile to be very low thanks to virtually non-existent debt and a robust balance sheet, but there are still certain risks that I would like to highlight.

- Declining purchasing power among consumers as a consequence of inflationary pressures could cause a growing preference for private-label brands as consumers often become more price sensitive when economic conditions weaken. In this sense, the company can supply private brands, but profit margins from store brands tend to be lower than that of branded products. Nevertheless, a potential recession could also accelerate consumer adoption of private labels.

- With the sale of the Chicago factory taking place in July 2022, the impact that this event will have on profit margins is not yet known as high inflation rates were already impacting the company's operations by the time of the sale.

- Share buybacks could remain on hold for a long time as inflationary headwinds continue to take place and the company faces a potential recession in the medium term.

- The share price could continue to fall before a potential turnaround as we are currently navigating very volatile times due to high inflation rates, supply chain issues, and a potential recession due to interest rate hikes.

Conclusion

Certainly, the current situation at Bridgford Foods' operations is not easy as the company's profit margins remain depressed as a result of a series of headwinds, including high inflation rates and higher production and transportation costs, which are taking the cash from operations to negative territory. This has caused concerns among investors as these headwinds are coming at a time when a potential recession could take place due to interest rate hikes.

Still, the management has already taken action by selling one manufacturing facility in Chicago and upgrading another in order to improve profit margins, and the balance sheet is very strong as cash and equivalents and inventories are much higher than long-term debt, which means the company has a lot of time before its balance sheet is seriously damaged. Furthermore, net sales are stabilizing at very high levels, so it seems that the company's problems are directly linked to the current macroeconomic context and, therefore, ongoing headwinds are of a temporary nature. For these reasons, I believe this represents a good opportunity to acquire shares and get potential high returns in the form of capital gains as the company pays no dividends and share buybacks are on hold.

For further details see:

Bridgford Foods: A Strong Balance Sheet Should Help It Navigate Current Headwinds