BHG - Bright Health Group: Stock Price Has Been Too Heavily Beaten Down

Summary

- The healthcare system in the United States is too disjointed and needs to be integrated.

- BHG adopts a strategic approach to address the challenges faced by the industry.

- Stock should do better as we lapse a weak FY23.

Summary

I recommend to buy Bright Health Group ( BHG ). I believe the stock has been massively sold off to an extend that does not make sense given the business growth prospect and value proposition. Should BHG continue to execute well (i.e., continue to show that they are on the right track to achieving profitability), I believe the market will react positively, thereby pushing the stock price up.

Company overview

BGP provides health care services . Through its digital health records platform, the company is able to bring together patients' clinical, financial, and social information in order to produce superior results.

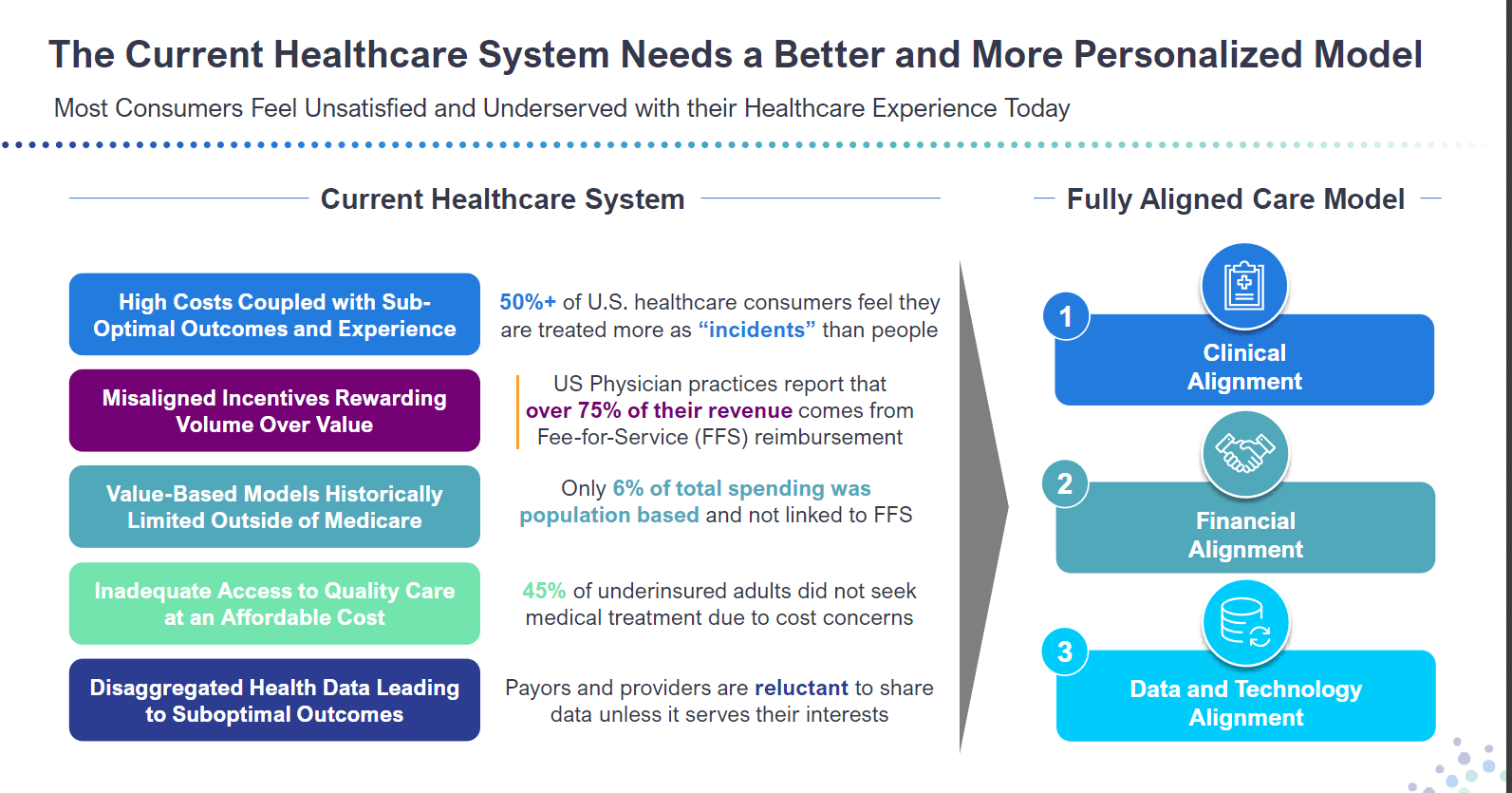

There is a need to integrate the fragmented US healthcare system

American healthcare has historically been geared toward serving large organizations rather than individual patients, with a preference for impersonal, centralized systems. As a consequence of this dynamic, the healthcare system is extremely disjointed, with even the most effective individual providers having trouble thriving in the face of poor coordination and conflicting incentives from other key players. By focusing on keeping costs down, traditional managed care organizations [MCO] have distanced themselves from their network providers and forgotten about the real target of their efforts: the healthcare consumer. In my opinion, the poor customer service, subpar clinical results, and massive financial waste are all results of this narrow perspective. There have been efforts in recent years by traditional MCOs to address these issues, but I believe they have been hampered by their inability to take a consumer-centric approach.

{kind=link}

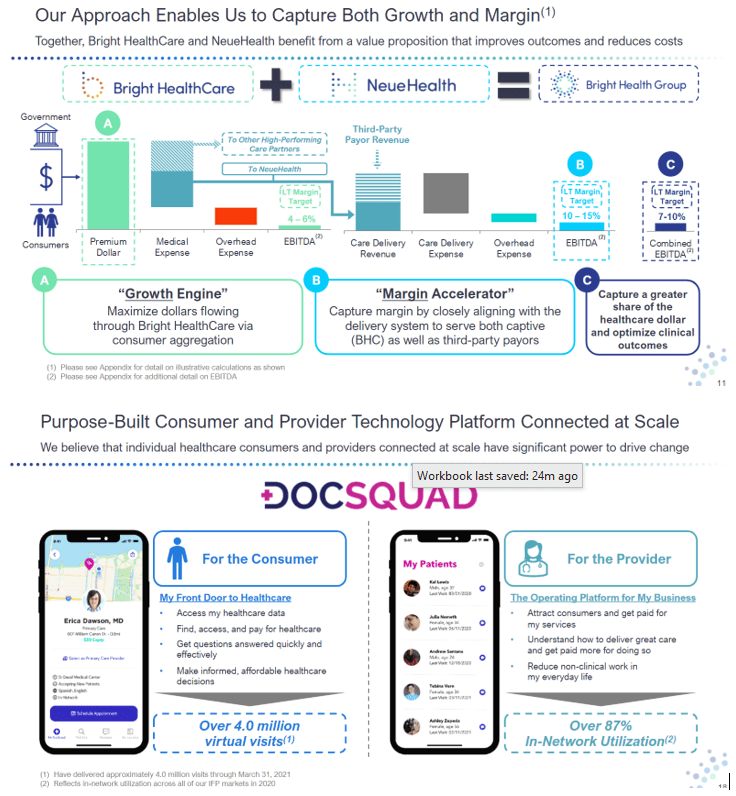

BHG strategic approach (BHG core, NeueHealth, DocSquad)

Strategically, BHG's focus is on aligning with its Care Partners on the medical, finance, and digital fronts. This is done to better serve the needs of patients and enhance the quality of care delivered. Although it is difficult for BHG to compete as a smaller player in a market where size and earnings matter, I do think that starting fresh has given BHG some competitive advantages. For instance, I think BHG is able to attain relatively competitive unit economics especially in comparison to traditional MCO with much bigger patient populations and wider networks by constructing relatively narrow networks with just high-performing physicians. BHG is able to offer competitive pricing and encourage substantial use of in-network providers as a result of this benefit design.

In addition, BHG has also been successful in moving healthcare spending toward value-based arrangements thanks to its efforts to connect with and establish tactical alliances with top physicians. To date, over 70% of Bright HealthCare's membership, or over 275,000 individuals, are participating in a value-based arrangement in the company's four largest states.

My opinion is that BHG can gain even more from the expansion of value-based care thanks to NeueHealth, one of BHG's businesses. By utilizing NeueHealth's IT services, affiliated providers can make the change to a risk-bearing arrangement with greater ease. Bright's NeueHealth division gives the company a foot in the door of the rapidly expanding provider enablement market. Even though this industry is still in its infancy, I believe the BHG's insurance assets and provider assets make a natural pair, and that the provider enablement space is set up for significant growth in the coming years.

These aside, DocSquad, one of BHG's consumer and care provider solutions, also helps to increase patients' participation in their own care while also equipping doctors with resources to improve their knowledge of their patient populations and their readiness to adopt more complex risk-bearing arrangements.

I believe BHG's ability to provide a wide variety of services and solutions, combined with its emphasis on value-based reimbursement, gives it excellent potential for market share growth. Although I recognize the potential value of linking payment to patient outcomes, healthcare is notoriously resistant to innovation. But I think BHG will be able to capitalize on long-term industry trends thanks to its alignment model.

{kind=link}

Win-win scenario

When it comes to healthcare, BHG's aligned model unites the provision with the financing, which is different from the standard connection between payors and providers. With the help of NeueHealth Care Partners, BHG develops its products to provide financial incentives for lowering the overall cost of care, improving clinical outcomes, and providing a better customer service experience. Care management under value-based arrangements is made easier with the help of the tools and expertise provided by NeueHealth Value Services. This allows local care delivery organizations to assume more financial risk and reap greater financial rewards. I believe Bright HealthCare and NeueHealth have excellent synergies that will allow them to shake up the current healthcare system.

Competition

BHG is in the highly competitive fields of both managed care and care delivery. Over a hundred different health plans operate in the United States, most of which are relatively small and regional, with only a select few truly operating on a national scale. I believe BHG will compete for membership with health plans from all levels, and I see Medicare Advantage [MA] as the most appealing growth opportunity in managed care.

The MA industry is cutthroat, with just a handful of companies controlling the vast majority of the market. When compared to Medicaid, Medicare Advantage is the most alluring government healthcare business because of its stable growth and higher profit margins. Given that seniors use more care than younger demographics, I believe that network of clinics and physicians, and ancillary perks are major points of distinction in MA, in addition to price. With thousands of seniors enrolling in Medicare every day and MA quickly becoming the program of choice, it's clear that the future of healthcare for the elderly lies with this innovative product.

Recent commentary from management instils confidence

BHG's updated forecast for FY23 revenue is $3.4-$3.6 billion, up 10-15% from the consensus estimate of $3.1 billion. The ratio of adjusted operating costs to revenue has decreased to 11% to 12%, which is 300 to 400 basis points lower than the prior guidance. The company remains committed to achieving a positive cash flow position and a positive adjusted EBITDA in 2023. Given that the stock price has been severely beaten down over the past two years, I believe that this new set of guidance is something that investors would welcome with open arms.

BHG's decision to phase out its IFP operations beginning in 2023 as part of a strategy shift to emphasize MA is another plus in my book. I think the MA market is more in line with IFP's core focus on value-based care models, which is important given that IFP is a small business with no clear path to profitability in the near future.

The management team was also pleasantly surprised by the higher-than-anticipated 2023 MA membership numbers. They expect growth to be positive in 2023, up from a prediction of flat to slightly down. C-SNP products, the management said, could see incremental growth because the company added over 10,000 members during the year 2022. As BHG continues to expand its presence in MA, the company plans to keep an eye on integration and operational improvements. However, similar to its competitors, I believe that MA rate increases in 2024 will be less favorable than in recent years.

Valuation

I believe the stock has been beaten down to a ridiculous level where any reasonable assumptions made will result in significant upside. Based on my model, using consensus estimates, BHG is worth 80% more than the $0.87 share price today.

I believe as we lapse the optically weak FY23 due to the exit of IFP business, a tough comps due to COVID, and a transitionary cost-alignment period, investors would be able to better value BHG based on its future prospects. This would certainly help with the stock narrative and share price.

Own calculations

Risks

Path to profitability

The biggest threat to the stock, in my opinion, is BHG's potential to reverse its guidance or fail to deliver on its promise of a profitable path. If investors stop believing management, the stock price, which is already low, is likely to plummet.

NeueHealth is part of BHG bullish thesis

Increased competition in the NeueHealth industry poses a risk to BHG's ability to scale its business, which could have a negative effect on the company's long-term growth and margin profile.

Conclusion

BHG's focus is on aligning with its Care Partners on the medical, finance, and digital fronts to better serve the needs of patients and enhance the quality of care delivered. The company has a competitive advantage in that it is able to attain relatively competitive unit economics and offer competitive pricing by constructing relatively narrow networks with just high-performing physicians. BHG also aligns with and forms strategic partnerships with top-tier physicians to shift medical spending toward value-based arrangements. The company's NeueHealth division gives it a foot in the door of the rapidly expanding provider enablement market, and DocSquad, one of BHG's consumer and care provider solutions, helps increase patients' participation in their own care while also equipping doctors with resources to improve their knowledge of their patient populations.

Overall, BHG's ability to provide a wide variety of services and solutions, combined with its emphasis on value-based reimbursement, gives it excellent potential for market share growth in the healthcare industry.

For further details see:

Bright Health Group: Stock Price Has Been Too Heavily Beaten Down