BFAM - Bright Horizons' Strategic Expansion: Not Enough To Offset Traditional Offerings' Struggles

2023-04-27 14:07:05 ET

Summary

- Bright Horizons has been expanding into new markets and diversifying its products, but this may not be sufficient to offset the struggles faced in its core traditional offerings.

- The company's attempt to manage a growing portfolio of services raises concerns about its ability to maintain focus and effectively manage its operations.

- The company's profitability metrics show a lower gross profit margin, EBIT margin, and net income margin than some of its peers, indicating it's less efficient at utilizing resources than peers.

Thesis

While Bright Horizons Family Solutions ( BFAM ) has been able to increase revenue through expansion into new markets, such as Australia, many factors have been working against it that could prevent it from achieving its projected double-digit growth over the next several years. These include inflation, economic headwinds, foreign exchange issues, a shortage of qualified staff, and higher labor costs in some countries. Furthermore, when ARPA funding ends in September 2023 this will likely have an impact on their overall growth. In light of all these challenges faced by BFAM, this article evaluates whether or not they can overcome them to reach their goals.

What Does the Company Do?

At first glance, Bright Horizons Family Solutions appears as a straightforward company that many of us can identify with. Essentially, it serves as a comprehensive provider of childcare and educational services, catering to both employers and families. As I delved deeper into BFAM's operations , I discovered that it functions across three primary segments: Full Service Center-Based Child Care, Back-Up Care, and Educational Advisory and Other Services.

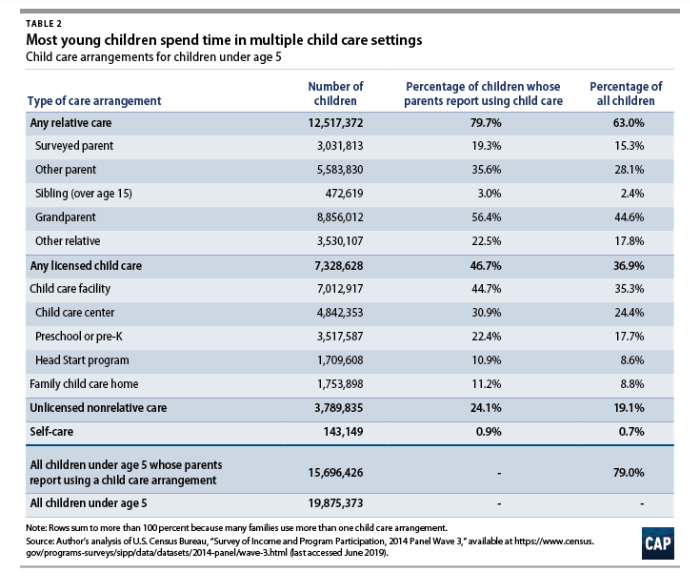

I am particularly intrigued by their first segment, which focuses on delivering traditional childcare and early education services, such as preschool and elementary programs. With 80% of children under the age of 5 spending at least some time with a relative during the week, 47% in licensed childcare, and 24% in unlicensed, non-relative childcare settings, I see the appeal of their offerings for families in search of quality care and education for their young ones.

The Center for American Progress

{kind=link}

Moreover, its Back-Up Care encompasses services like center-based back-up childcare, in-home care for children and adult/elder dependents, school-age camps, virtual tutoring, and even self-sourced reimbursed care. This enables employees to strike a balance between their work and family lives, potentially translating into increased job satisfaction and retention. This is particularly noteworthy since, as per a survey , around 73% of employees in the United States will require some form of back-up child and/or adult care.

Lastly, the Educational Advisory and Other Services segment offers a diverse range of solutions, including tuition assistance, student loan repayment programs, workforce education, and college admissions advisory services. In essence, they are assisting employees in advancing their education and managing student debt, given that the Federal Reserve reported that there's:

$1.75 trillion in total student loan debt (including federal and private loans).

Hence, such offerings could prove to be a significant perk in attracting and retaining talent.

Childcare and Early Education Providers Industry Outlook

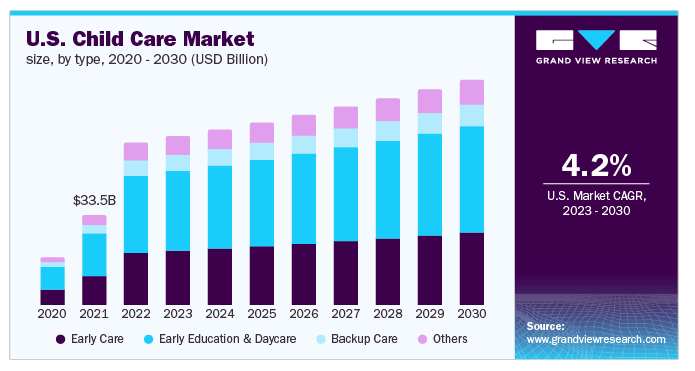

Grand View Research's projection of growth between 2023-2030 indicates that childcare and education services demand will contribute to its expansion with a compound annual growth rate ((CAGR)) of 4.18%.

{kind=link}

This projected expansion brings up many pertinent questions regarding access and affordability of these services as well as any regional disparities within the nation. One reason behind the surge in demand for child care services is due to the rising number of single mother households across America.

{kind=link}

Research estimates there were around 15.62 million single mother households in the US last year - an increase from previous years. Therefore, I believe it is evident that families attempting to juggle work and parenting responsibilities alone are more likely to turn to childcare facilities for their young children; something which bodes well for Bright Horizons.

Moreover, demand for child care services differs across the United States - creating significant growth opportunities for the company. For example, the South has an elevated concentration of single parent families which increases demand for child care services even further in this region. While the federal government provides some financial support for childcare programs, accessing quality care still remains challenging due to barriers such as prohibitively expensive cost of those programs (the average annual childcare expense being $14,760).

{kind=link}

Furthermore, in other regions there is a severe lack of child-friendly environments, resulting in the term "daycare deserts."

{kind=link}

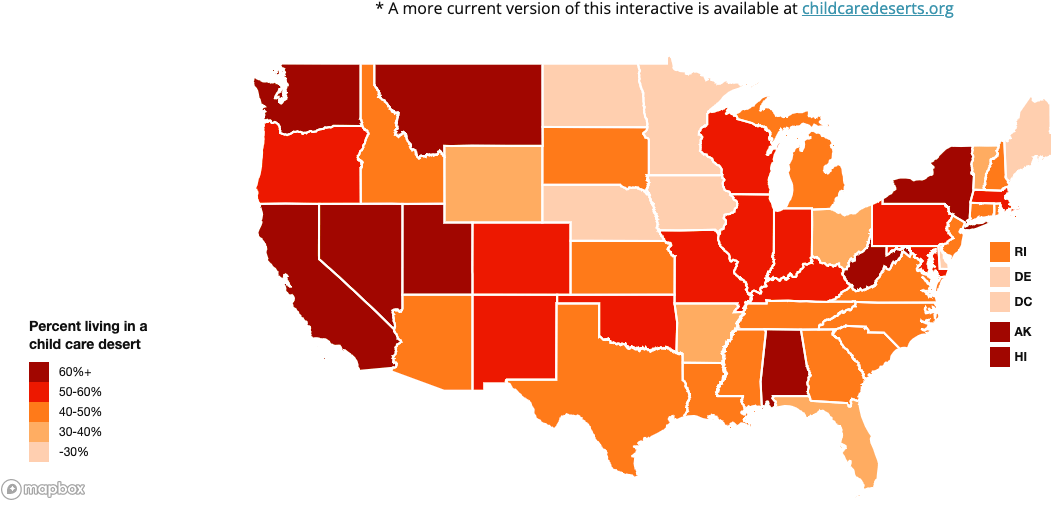

Estimates show that 51% of US population live in areas without access to childcare; thus reinforcing Bright Horizons as an ideal company capable of addressing such disparities.

{kind=link}

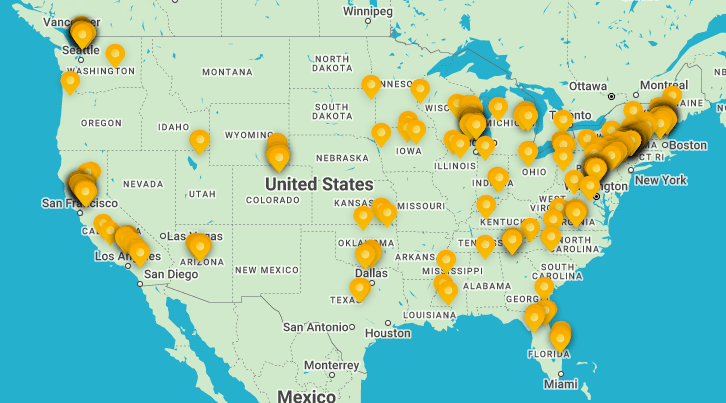

The above map marks Bright Horizons' current locations in the US . As you can see there's ample room for growth in multiple states, particularly in Nevada and Utah which registers above 60% living in a "daycare desert" on the previous heat map. Also, I noticed a particularly huge gap in the Carolinas as well as most of Texas, with all three of those states in the 40+ percentile.

How Does Bright Horizons Stack Up?

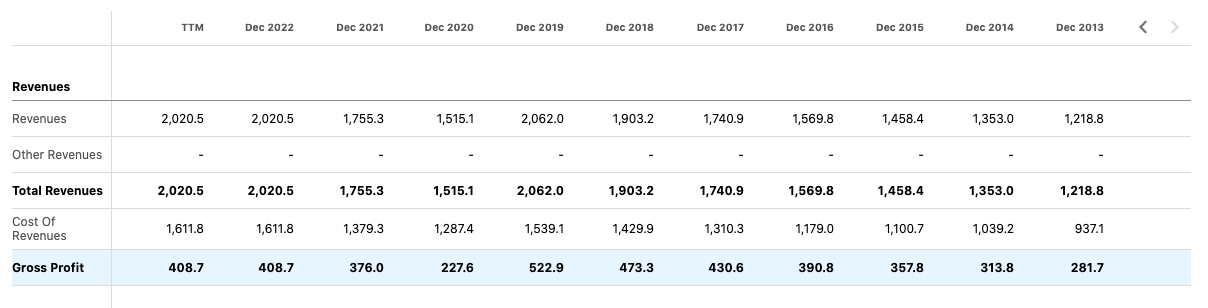

As I checked out the company's income statement , I wanted to highlight several key takeaways that I think should be considered. First of all, total revenues for the latest period TTM total $2,020.5 million, showing (relatively) steady revenue growth since 2013's $1,218.8 million figure; this tells me that BFAM has managed consistent revenue increases year over year, indicating an impressive compound annual growth rate of 5.7% that exceeds the aforementioned 4.18% industry outlook.

{kind=link}

Moving on to gross profit, BFAM demonstrates an upward trend, growing from $281.7 million in December 2013 to $408.7 million (see above) in December 2022. Nonetheless, this growth has been somewhat volatile, with significant fluctuations over the years.

{kind=link}

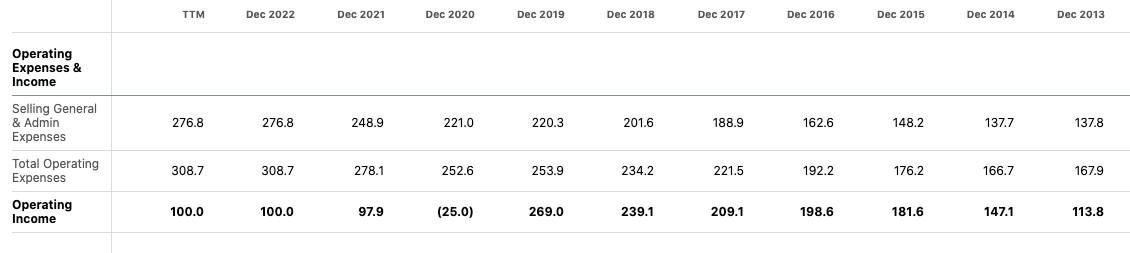

Moreover, operating income did experience an upward trend, increasing from $113.8 million in December 2013 to $269 million in December 2019. However, I wanted to point out that this upward trend rebooted, or restarted, in December 2021 as a result of the pandemic where there was a negative operating income of $25.0 million reported in December 2020.

{kind=link}

And finally, regarding BFAM's interest expenses, it looks like they've remained relatively stable over the years, ranging between $34.7 million and $47.5 million; however, there is a slight decrease in interest expenses from $45.2 million in December 2019 to $39.5 million in December 2022 which I interpret as a positive sign for the company, as it implies a more manageable debt burden.

Peer Evaluation

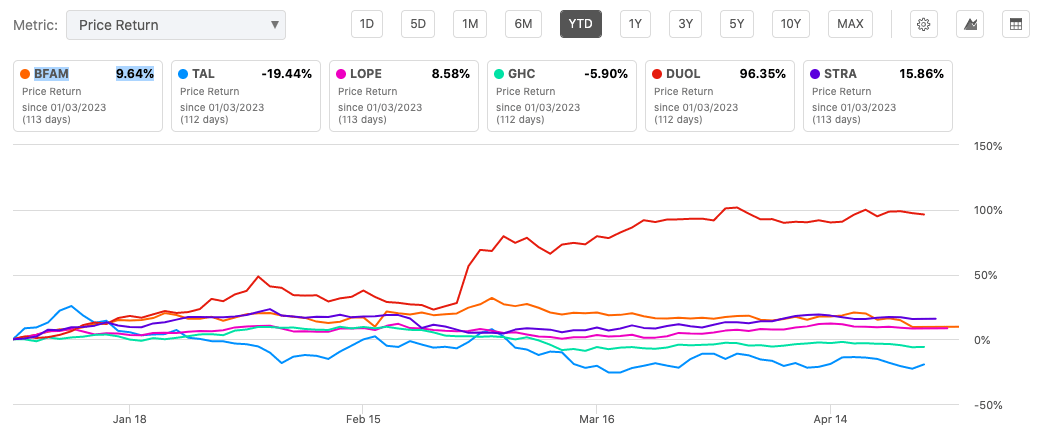

Relative to its peers, BFAM's YTD price return gets the bronze medal, yet it, along with STRA, gets blown away by DUOL's nearly 100% return .

{kind=link}

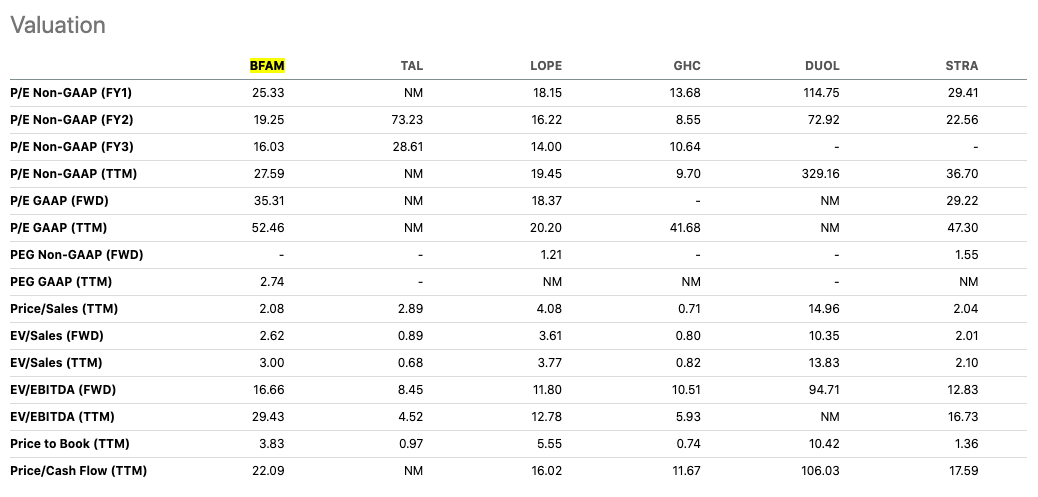

Moreover, it also appears that BFAM may be slightly overvalued compared to its peers by drawing this conclusion from the following observations:

{kind=link}

Looking at BFAM's forward P/E ratio of 25.33, you'll notice that it's higher than most of its peers (LOPE, GHC, and STRA). Meanwhile, the P/E ratio for DUOL is considerably higher, but that's due to the fact that DUOL's valuation may not be directly comparable due to its extremely high revenue growth rate. Furthermore, BFAM's price/sales ((TTM)) ratio of 2.08 is also higher than some of its peers (LOPE and STRA).

{kind=link}

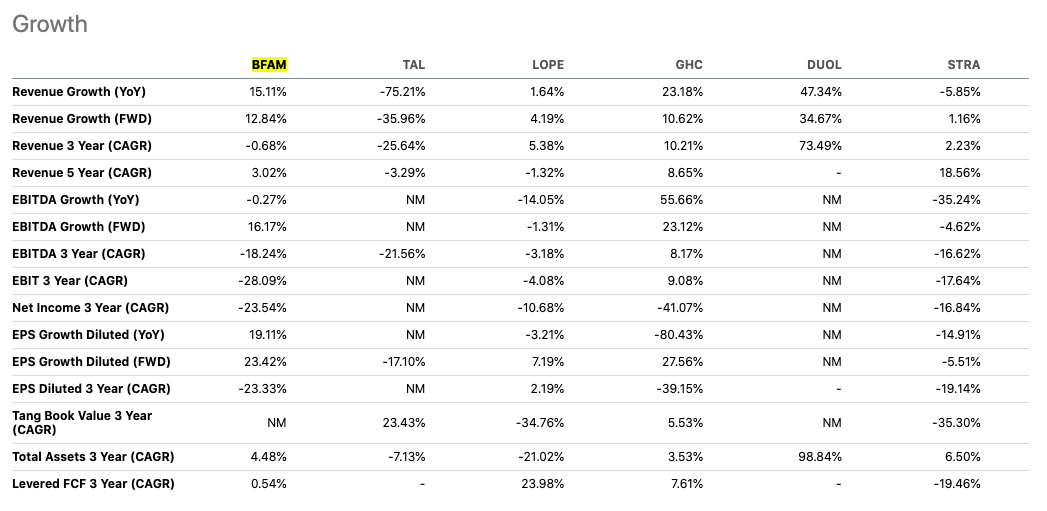

Moving on to growth metrics , while BFAM has positive revenue growth, you'll see that it's lower than a couple of its peers, such as GHC and DUOL. Additionally, its EBITDA and EPS growth rates are lower than LOPE and GHC.

{kind=link}

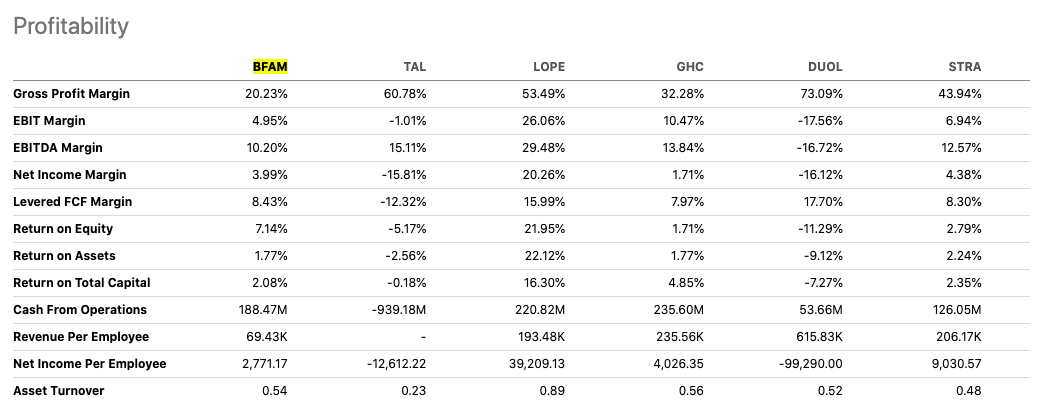

And, last but not least, BFAM's profitability metrics show a lower gross profit margin, EBIT margin, and net income margin than some of its peers, such as TAL, LOPE, and STRA. Additionally, its return on equity and return on assets are lower than LOPE and STRA as well, indicating to me that it's less efficient at utilizing resources to generate returns.

Q4 2022 Bullish Bullet Points Recap

- 2022 was a good year for BFAM , as their revenues surged 15% and earnings expanded an astounding 31%. Much of that money went toward tech infrastructure upgrades as well as buying other companies to open new markets or diversify products - like Steve & Kate's Camps and pet care services .

- Last quarter saw their revenue surge 14%; full-service child care performed especially well, increasing 15% year over year while Back-Up Care also experienced strong results with 15% revenue increases for this quarter alone. CEO Stephen Kramer noted :

Reflecting on 2022, I believe it was a pivotal year for Back-Up Care. After onboarding more than 200 clients and rebuilding traditional use across 2020 and 2021, we surpassed pre-pandemic use midway through 2022. And we saw further acceleration of use growth in Q4 across all traditional use types. With now more than 1,100 Back-Up clients, a broader set of use cases and a more streamlined reservation system, I couldn't be more excited about the opportunity to grow Back-Up Care in double-digits over the next several years.

- And, looking ahead, BFAM projects double-digit growth over the coming years, and they hope for revenues to come in between $2.3 and $2.4 billion and adjusted earnings of $2.80 to $3 per share for 2023.

Q4 2022 Bearish Bullet Points Recap

- For starters, the company is dealing with a shortage of qualified staff , and the higher labor costs in the UK and Netherlands haven't been helping. Inflation and economic headwinds have been making it tough for parents in the UK, and that hiccup has been slowing down their expansion into Australia.

- They still managed to increase their revenue by 14% in Q4 2022, but foreign exchange issues took away 4% of that growth. When the ARPA funding program ends in September 2023 , they're expecting it to have a $0.40 impact on their overall growth. CEO Stephen Kramer commented :

So I think this will be an interesting year as it relates to continuing to track enrollment and staffing and then ultimately, seeing what the impact of a sunsetting ARPA program is going to do to the sector at large.

- And finally, on top of that, BFAM is going to have to deal with higher interest expenses and tax rates in 2023, which could make it even harder for them to keep growing. So, while they're aiming for double-digit growth in the next few years, it's still up in the air whether they can overcome these challenges to hit their targets.

Final Takeaway

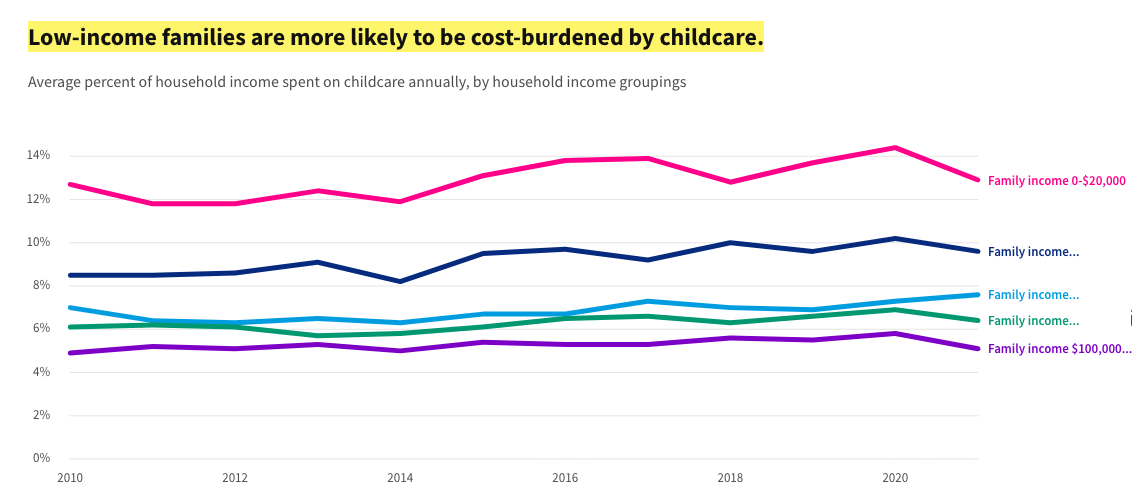

Bright Horizons is grappling with mounting provider fees, escalating labor costs, and acute staffing limitations , all of which are exacerbated by fierce competition from the other roughly 600,000 childcare providers in the US alone. Moreover, regarding the recession every seems to be talking about, those low-income families who'll ride out that storm will likely be cost-burdened by childcare , which means that they might be scrambling towards other, less costly, alternatives.

{kind=link}

Moreover, on the international front , it appears that Bright Horizons is also battling strong headwinds. So with revenue growth forecasts not quite meeting expectations, due in part to the adverse effects of the American Rescue Plan Act (ARPA) and enrollment constraints, the company's overseas performance, in my opinion, leaves much to be desired. I think for most discerning investors, this is another big red flag.

And finally, I think that the company's attempt to diversify and branch out into non-traditional services may not be sufficient to offset the struggles faced in its core traditional offerings. For the most part, this strategic expansion, though admirable, raises concerns about the company's ability to maintain focus and effectively manage its growing portfolio of services. In other words, I prefer businesses that demonstrate a solid grasp on their primary operations before venturing into new territories in order to bank on expanding their growth. With all of these factors considered, I believe Bright Horizons may face considerable difficulty in achieving its revenue targets and delivering substantial growth in the short term. As a result, I rank the company as a sell.

For further details see:

Bright Horizons' Strategic Expansion: Not Enough To Offset Traditional Offerings' Struggles