BHF - Brighthouse Financial: Dull At Present But Rebound Potential Still Evident

2023-03-28 04:33:53 ET

Summary

- Brighthouse Financial, Inc. maintained a decent performance amidst market volatility.

- Its solid financial positioning can help the company withstand more disruptions and rebound.

- Macroeconomic headwinds are evident, but the company can get through them.

- The stock price had a sharp plunge last month but appeared reasonable.

Brighthouse Financial, Inc. (BHF) continues to cope with macroeconomic headwinds. It maintained stable revenue growth amidst the rising prices and lower demand. However, cost pressures and lower investment yields offset revenue growth, leading to hammered margins. As inflation and interest rates remain elevated, its near-term performance may stay at the current level. But if the inflation decrease continues, operational. improvements may be expected. On a lighter note, its financial positioning stays in impeccable shape. It allows the company to cover its current capacity and capital returns. It has adequate means to withstand more headwinds and rebound.

Meanwhile, the stock price remains at the bottom, one month after its sharp plunge. It appears reasonable as recessionary fears persist. Its products, mainly fixed index annuities, do not perform well in a high-inflation environment. Despite this, it opens an opportunity for investors to buy BHF stock at a discount. It may bounce back once the market stabilizes, and the way I see it, BHF remains a durable and resilient company.

Company Performance

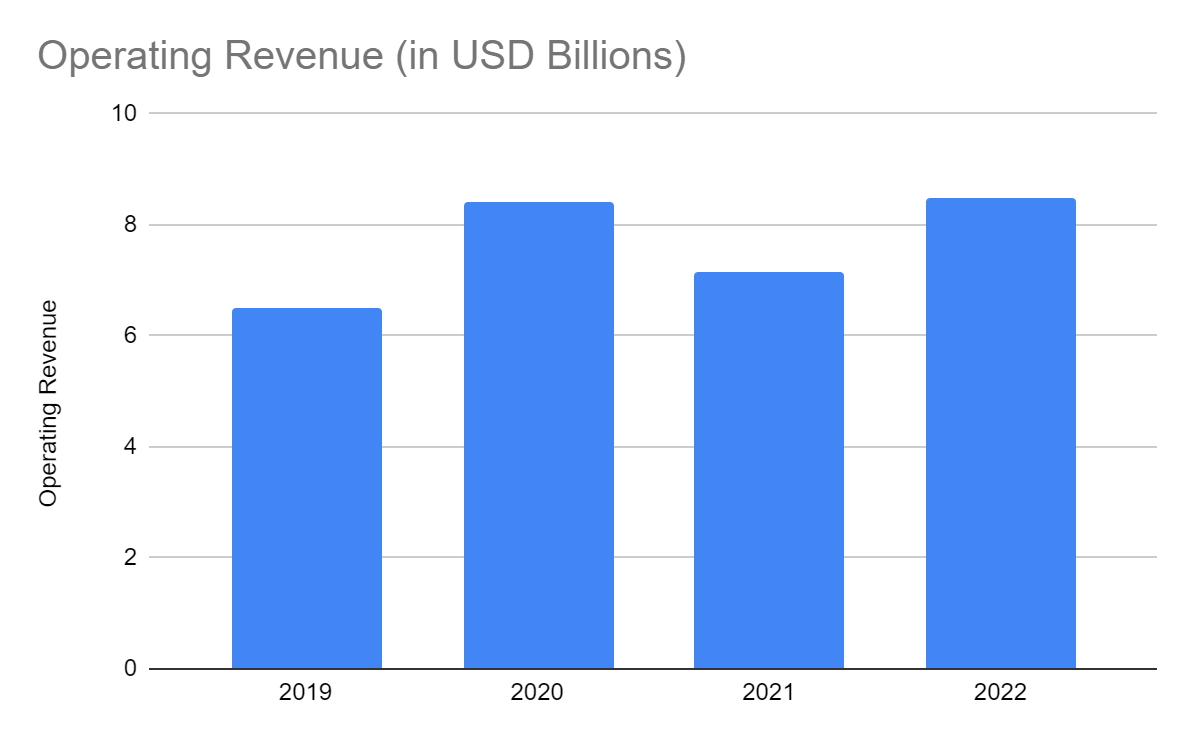

Since its spinoff, Brighthouse Financial, Inc. has expanded and fueled its domestic market presence. In only a few years, it has become one of the largest companies in the US life insurance and annuities market. Indeed, the pandemic highlighted the essence of life insurance and annuities. Its toll raised the financial awareness and literacy of many Americans. It was not easy, though, since joblessness made it difficult for many to purchase policies. We can see its solid rebound in the first half of 2022, with cumulative revenue of $6.5 billion. It was already higher than the whole-year sales in 2019. Also, it was 80% of the 2020 sales and 91% of the 2021 sales.

Moreover, its operating revenue in 2022 amounted to $8.47 billion , the highest value since it went public. It was a 19% year-over-year increase. We can attribute it to the increased influx of policyholders in 1Q and 2Q 2022. Its strategic pricing also helped it amidst inflation.

Operating Revenue (MarketWatch)

{kind=link}

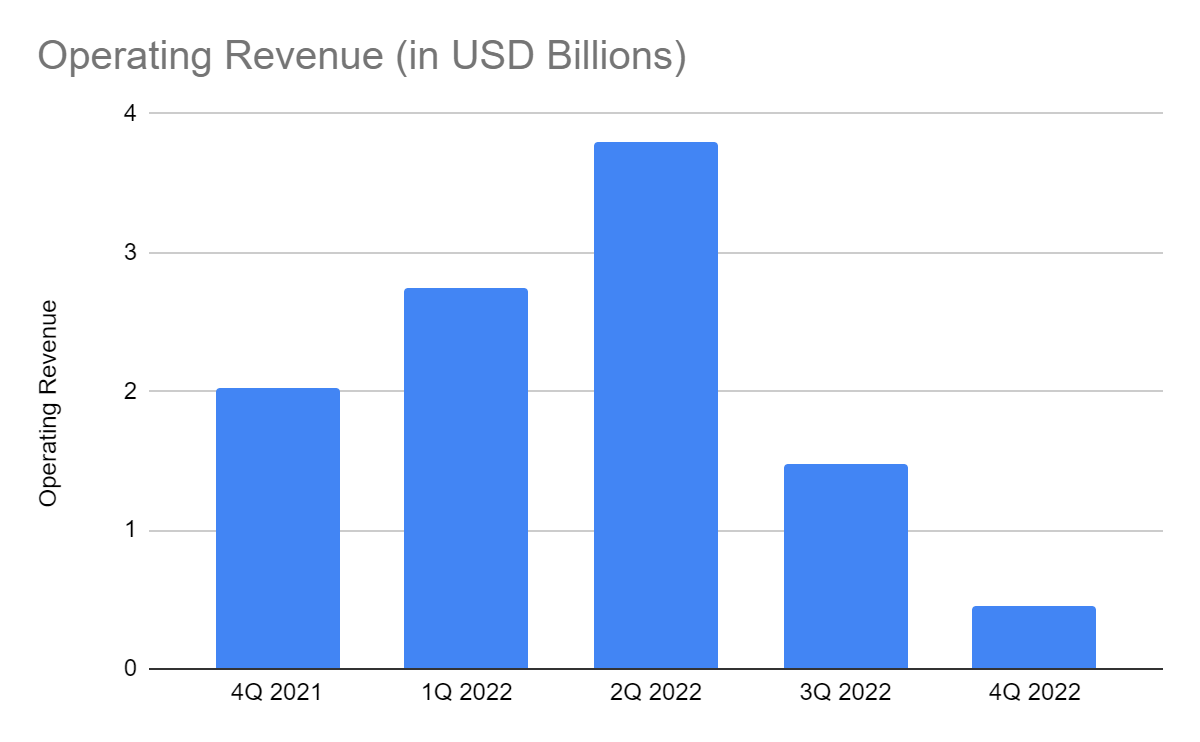

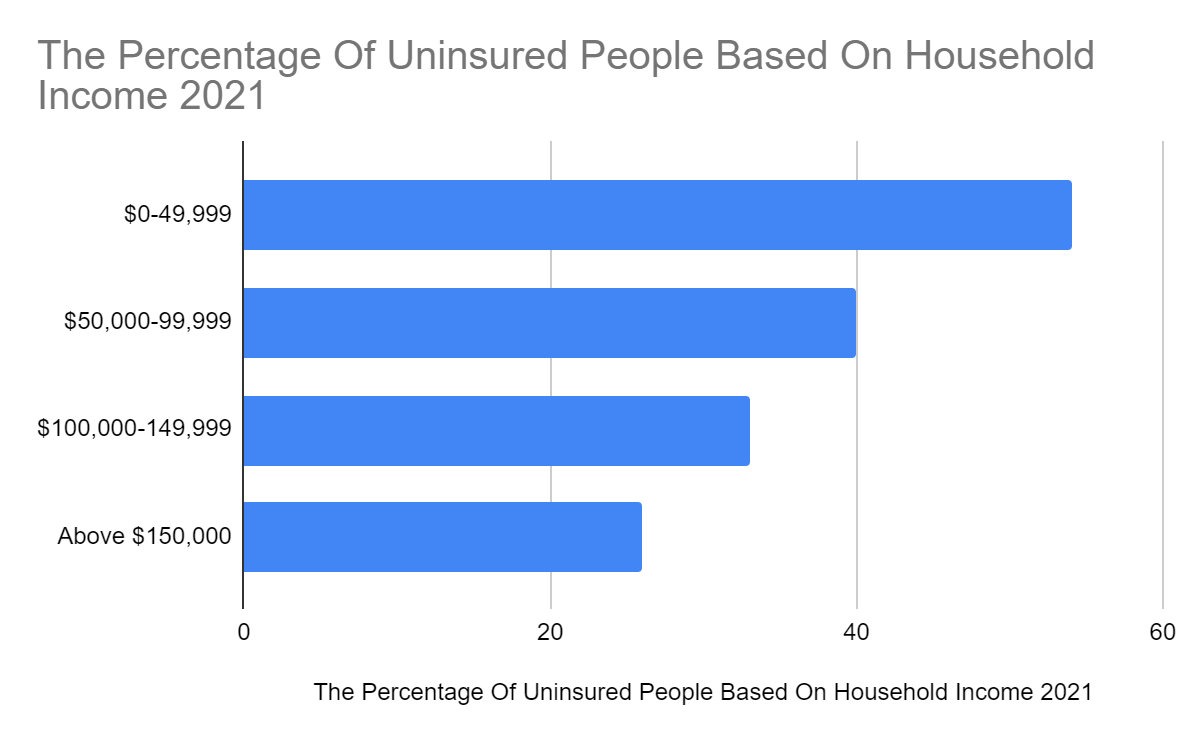

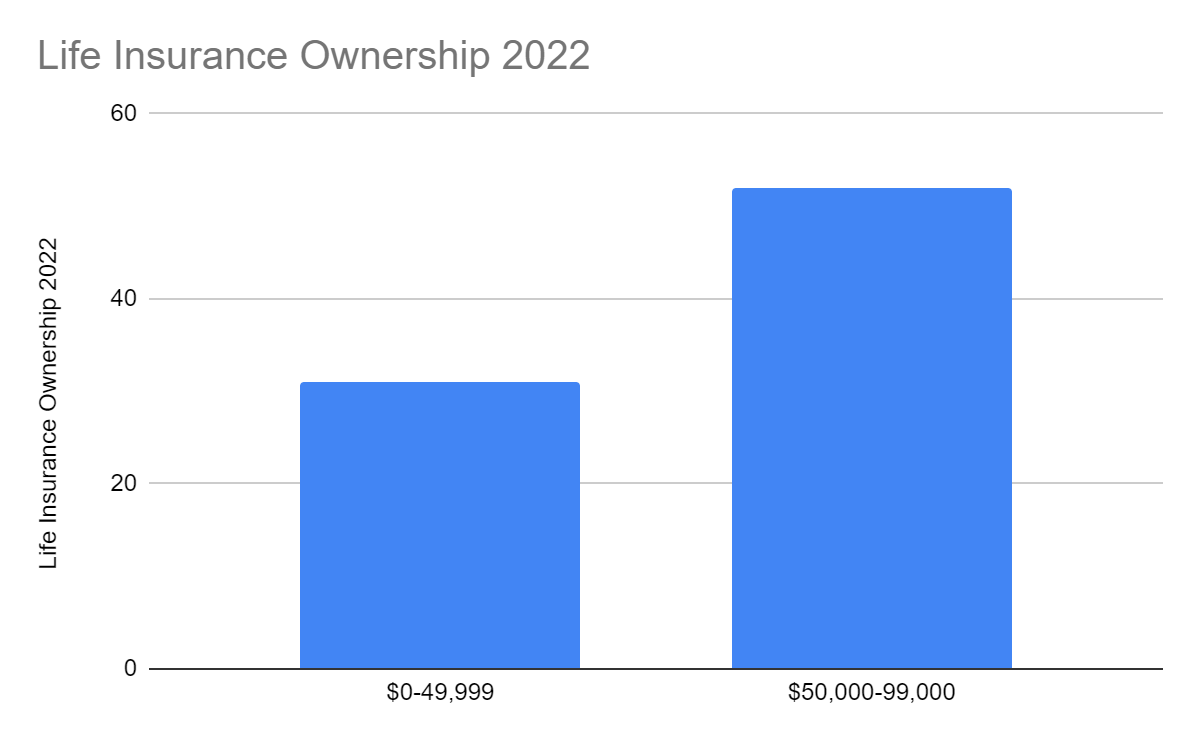

However, we can see its impact in the second half as revenues kept decreasing. In 4Q, the operating revenue hit rock bottom at only $450 million, a 122% year-over-year decrease. With that, it already came to a point where repricing could no longer offset volume drop. It was consistent with a survey in 2022 where the majority of the respondents said prices were a primary concern for buying life insurance . Also, life insurance ownership dropped from 2021 to 2022. Ownership among those earning below $50,000 was only 31% in 2022 versus 46% in 2021. Likewise, ownership among those earning between $50,000 and $99,999 decreased from 60% to 52%. Its investment products also impacted its performance. More often than not, fixed annuities indexes are prone to lower yields and valuation losses in a high-inflation environment. The same scenario could be seen in the company, leading to a weaker performance of its run-off segment.

Operating Revenue (MarketWatch)

{kind=link}

The Percentage Of Uninsured Americans Based On Household Income 2021 (Insurist)

{kind=link}

Life Insurance Ownership 2022 (Annuity.org)

{kind=link}

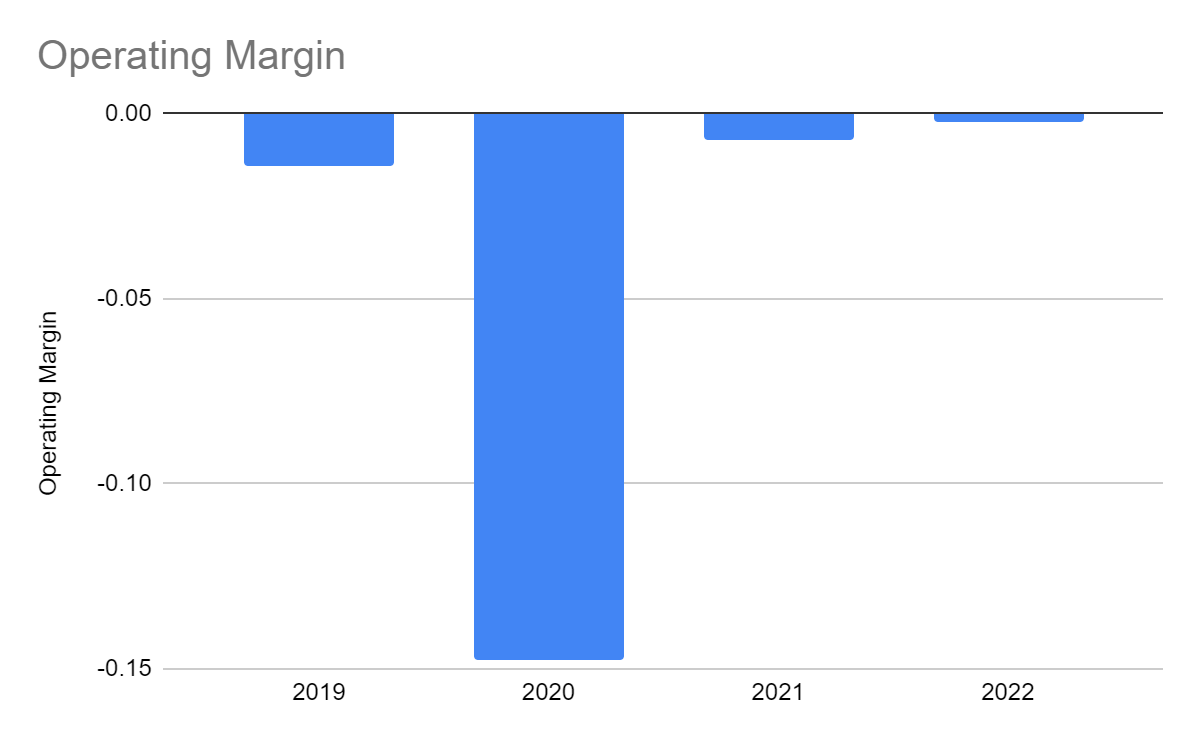

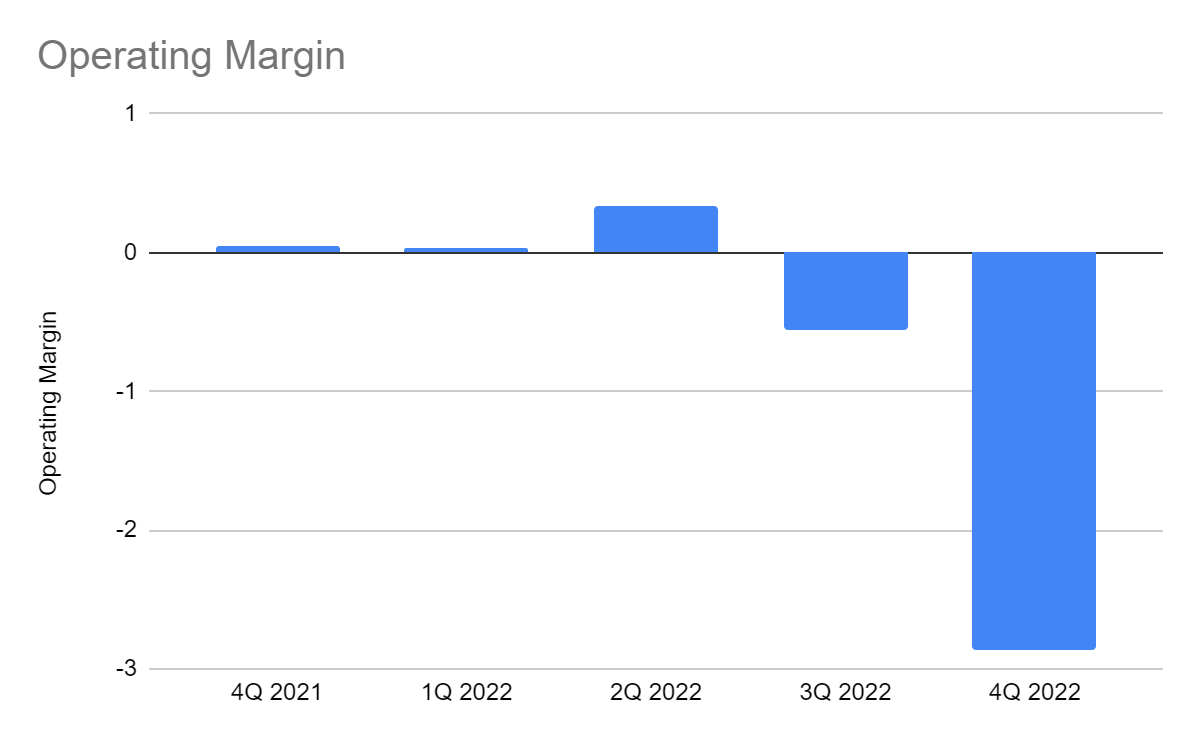

Meanwhile, cost pressures hammered the company. Higher claims were higher, which we could attribute to various factors. First, lower policy retention due to inflation led to many policyholders pulling out their life insurance and annuity policy contracts. In 2022, it has 2.5 million policies in force versus 2.7 million in 2021. Second, Hurricane Ian could be another driving force since North Carolina was one of the greatly affected areas. It was not directly stated, but it could be logical. Non-insurance expenses also rose substantially. The combined increase in claims and expenses offset revenues. As such the operating margin was only -0.2%. Even so, it was better than the -0.7% operating margin in 2021. We can say that its improved performance in 1Q and 2Q 2022 was integral to it. But in 4Q, the operating margin was -287%.

Operating Margin (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

This year, its near-term performance may stay hammered. Recession fears are still intense, which may negatively affect consumer behavior in the industry. But hope can be seen on the horizon as inflation eases. There may be continued improvements in the second half or in 2024. We will discuss it further in the next section.

Why Brighthouse Financial, Inc. May Stay Afloat And Bounce Back

Most companies are prone to higher risks associated with macroeconomic volatility. Regardless of size, businesses may be crushed into pieces in an instant. So beware. At this point, we may be thinking twice about investing or keeping our current shares in Brighthouse Financial, Inc. But right now, some crucial factors might be considered. We must know how long inflationary headwinds will last and how long BHF can keep up with them. Despite the bleak near-term macroeconomic forecast, I am optimistic about it. As of this writing, the US inflation rate is only 6%, 34% lower than the 2022 peak. With that, the conservative action of the Fed is paying off. It already raised interest rates by another 25 bps last meeting. Given the current pattern, we may expect interest rate increments to slow down in the second half. Meanwhile, inflation may continue to decrease. The efforts may not materialize soon, but the long-run impact may be worthwhile. To that end, the purchasing power of consumers may increase. And since the rising prices are the primary concern of policyholders, it will be favorable for Brighthouse Financial. Even better, its investment yields may improve. Both of these may lead to increased revenues.

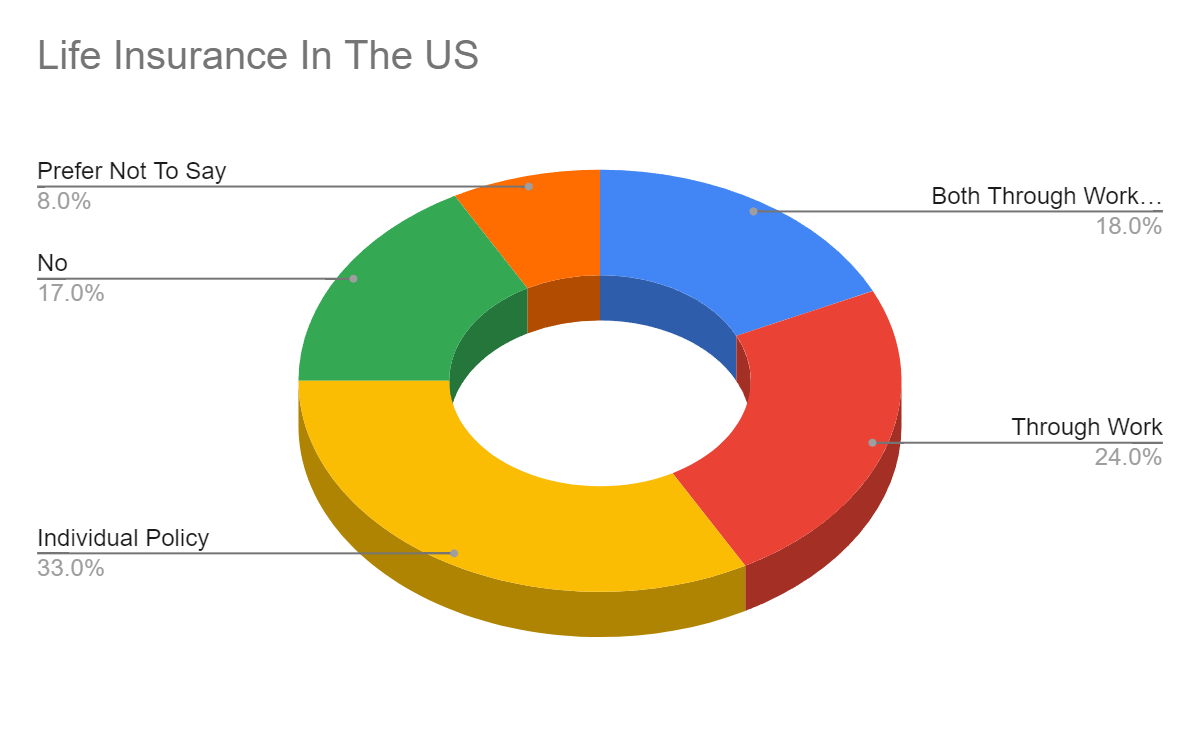

Moreover, the insurance and annuity market penetration is still lower than desired levels. In the chart below, we can see that policy ownership in the US is over 70%. But that is combined with policies provided by their employers. The average individual policy ownership is only 33%, which is consistent with the survey we discussed in the previous section. As such, there may be more potential clients BHF may cater to. Once inflation becomes more stable and manageable, the company can have more flexible pricing. It can capture more demand.

Life Insurance In The US (Annuity.Org)

{kind=link}

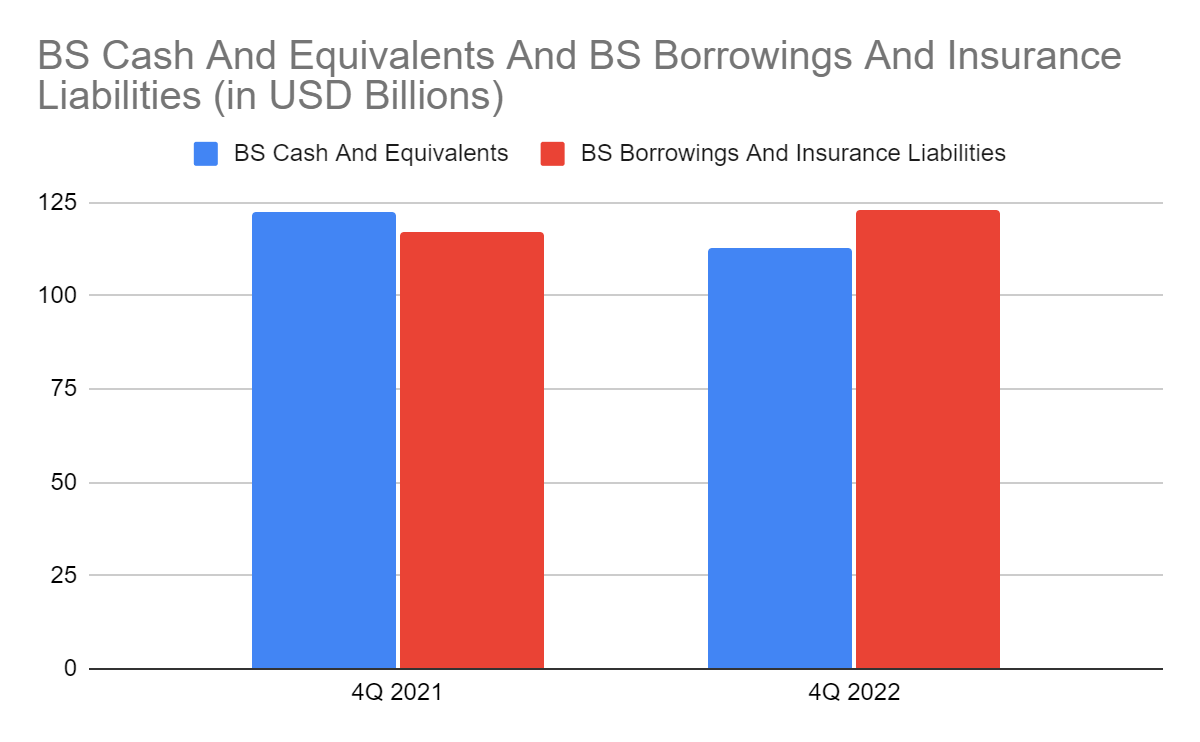

But what made this company trustworthy is its sound financial positioning. It has adequate cash reserves to cover its current operating capacity, outstanding borrowings, and capital returns. The combined value of cash investments of $112.7 billion comprises 49% of the total assets, making it a very liquid company. The company may not be viable now, but it is still sustainable.

BS Cash And Investments And Borrowings And Insurance Liabilities (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of Brighthouse Financial, Inc. has been in a downtrend since the start of the year. It became more prominent after the sharp decrease last month. At $41.4, it is already 24% lower than last year's value. For more than a year, it stayed between the upper 40s to mid-50s. But it opens another opportunity for investors to get their shares at a discount. Its book value may be lower than in the preceding years. Yet, the PB Ratio of 0.63x shows that the stock price is still attractive relative to fundamentals. The current decrease may be logical since it must reflect the intrinsic value of the company. Also, earnings and FCF are negative values, leading to a weaker outlook. But with the current liquidity of the company, it can sustain capital returns and share repurchases. It can withstand more headwinds and bounce back once macroeconomic indicators stabilize. Even better, its PS Ratio is only 0.33x. It means that the stock is trading less than three times the sales. If we compare it to the average since it went public, the ratio will be 0.41x. If we use the average ratio to find the target price, it will increase to $50.74. There may be a 22% upside in the next 12-18 months. Hence, investors may take this opportunity to buy shares at a lower price.

Bottomline

The operations of Brighthouse Financial, Inc. may be challenged right now. But its current market positioning and strategic pricing shows it can stay afloat amidst headwinds. Its financial positioning allows it to sustain its current capacity, capital returns, and long-run rebound. Also, the stock price appears low with potential undervaluation. The recommendation is that Brighthouse Financial, Inc. is a buy.

For further details see:

Brighthouse Financial: Dull At Present But Rebound Potential Still Evident