BHF - Brighthouse: Positioned For 2024 Capital Improvement

2024-01-15 01:01:18 ET

Summary

- Brighthouse Financial shares have underperformed this past year due to capital performance and business complexity.

- The company reported adjusted earnings of $4.18 per share in Q3, up 3% from last year.

- Concerns about capital performance have weighed on the share price, but improvements are expected in 2024 given a reinsurance transaction and market movements.

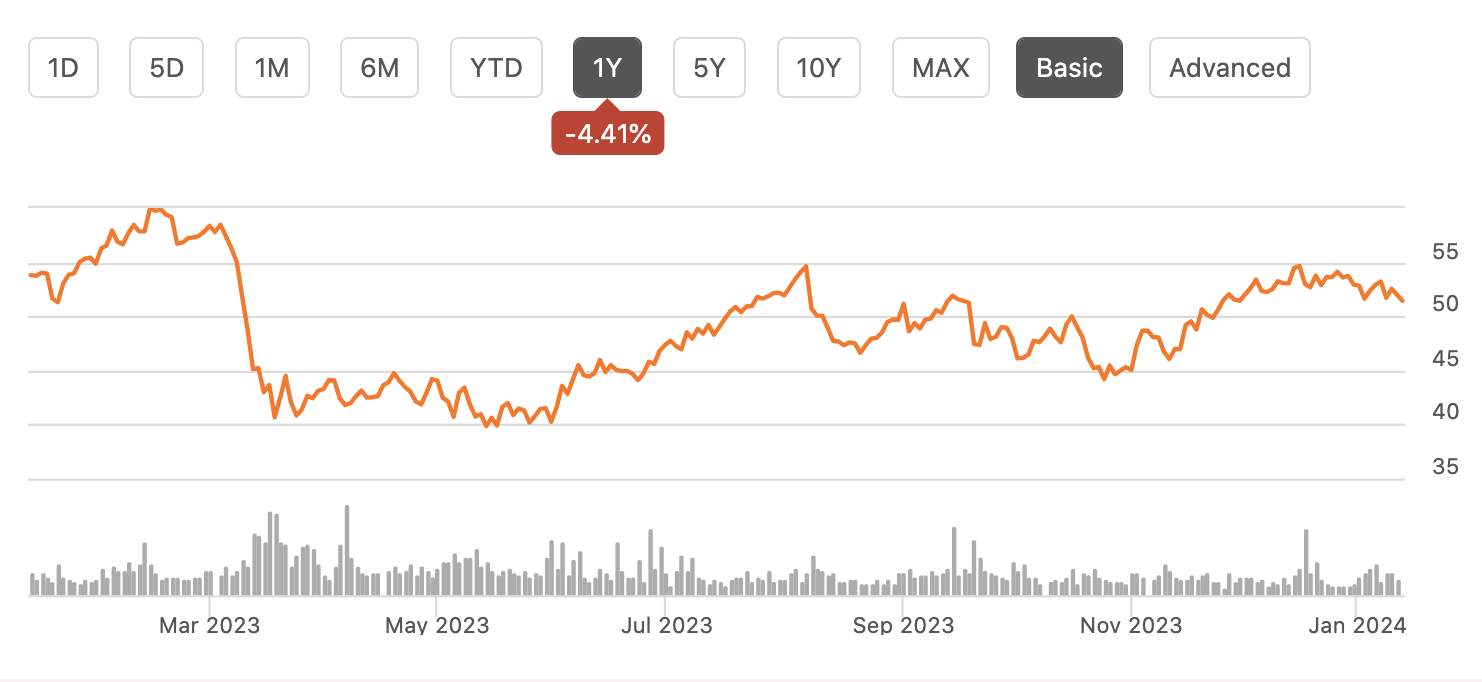

Shares of Brighthouse Financial ( BHF ) have been a meaningful underperformer this year, as its capital performance and business complexity have led its discounted valuation to persist. Since I recommended purchasing them in October , Brighthouse shares have risen by over 8%, though this has lagged the S&P 500’s 11+% gain. While not a bad return, this underperformance is likely partly driven by concerns about its capital performance in Q3. However, I expect the company to report stronger results in 2024 and reiterate long-term guidance, allowing shares to move to the upper $50’s.

{kind=link}

In the company’s third quarter , it earned $4.89 per share, though adjusting for a favorable actuarial adjustment and mark-to-market movement, adjusted earnings were $4.18, up about 3% from last year. Brighthouse remains highly profitable, and there were certainly some strong points in recent results. While annuity sales fell by 30% from last year at $2.6 billion, this was up 5% sequentially. Net flows were -$1.3 billion, accelerating from the -$900 million in Q2, as its legacy variable annuity ((VA)) business continues to wind down.

Account values were down $5.3 billion at $132.1 billion sequentially but still up over 7% from a year ago. Adjusted annuity earnings rose by about 13% to $291 million. I also was very encouraged to see that its run-off unit turned a $1 million profit from a $144 million loss last year as it benefits from higher net investment income.

As explained in October, BHF is winding down its legacy VA business and shifting new sales into less risky annuity products. With each quarter, its VA business naturally falls as it makes payments, and its new business grows. Having this unit run at breakeven and provide stable results will help investors focus on new business. Its core “Shield Level” annuity sales rose by 15% sequentially and accounts for about 70% of sales.

One headwind for results is that Q3 net investment income was about $30 million below its run-rate expectations given a modest 1.6% return in its alternative investments. Management also expects lower alternative returns in Q4. This is one area we are likely to see improvement as the focus turns to 2024. Alternative returns typically lag equity market returns by about a quarter—the weak equity market in Q3/early Q4 is why Q4 alternative returns will be lower. However, with the market rallying back strongly at the end of 2023, this should propel alternative returns higher in H1 2024. Similarly, BHF earns management fees on some account values; with markets rising, we should see BHF’s assets under management grow in 2024 relative to 2023, providing an additional boost to results this year.

While there are these positives, there has been one negative—BHF’s capital position. Risk based capital was at 400-420% with $7.3 billion of statutory capital in Q3. While above 400% is a solid level of capital, its capital position was down from $7.6 billion in Q2 when its RBC was ratio was in the 430-450% range. Interest rate volatility and revaluation of its deferred tax assets (DTA) drove the decline. Only $100 million of its DTA is included in capital, though it still expects to fully utilize it. The full value is $1.5 billion.

A key reason to own Brighthouse is its share repurchases. In fact, management recently announced an open-ended $750 million share repurchase program. During Q3, it repurchased $64 million in stock with another $27 million bought in the first month of Q4. There have been $290 million in buybacks over the past year. It is essential for BHF to maintain strong capital, so it can dividend cash from the insurance operating company to the holding company, which is the entity that makes repurchases. Importantly, the holding company has liquid assets of $900 million, a healthy buffer to maintain operations even if there were less dividends from the operating company.

This lower Q3 RBC has weighed on BHF’s share price performance, as investors likely worry that buybacks will be slowed further. However, I am expecting to see a material improvement in 2024, which should help to allay these concerns. First, BHF has engaged in a reinsurance transaction should also boost RBC by $200 million in Q4.

Additionally, BHF’s variable annuities carry significant long-term sensitivity to stock market levels and bond yields. To manage this, BHF has large hedge positions via derivatives. These hedges have worked well. In Q3, the company enjoyed $1.1 billion of market risk benefits and $900 million of derivative losses for a net $200 million favorable impact. Over the past six quarter, BHF has seen about $800 million in net gains from its hedging activity.

Over the long-term, these hedges and market movements should broadly offset. Validating this, the company shifted its actuarial assumption in Q3 to a 3.75% long-term 10-year treasury yield from 3.5% previously. This created a favorable $51 million impact to its GAAP financials. Considering it has a $220 billion balance sheet, this impact is negligible, which speaks to how fully it has hedged risks that it can control.

However, its statutory capital and risk-measurement can move in the near-term with markets, particularly during periods of volatility, as seen in Q3. However, according to management, in 2024, it will recoup the negative impact that higher rates had on its VA book. Additionally, we have seen treasury yields move down from their highs, which should be a favorable tailwind. This mean reversion factor in statutory capital calculations should mean Q4 RBC is at least comparable to Q3, and we then see increases in H1 2024. As RBC rises back toward 450%, there should be greater comfort that BHF can continue to do $250-350 million in share repurchases per year.

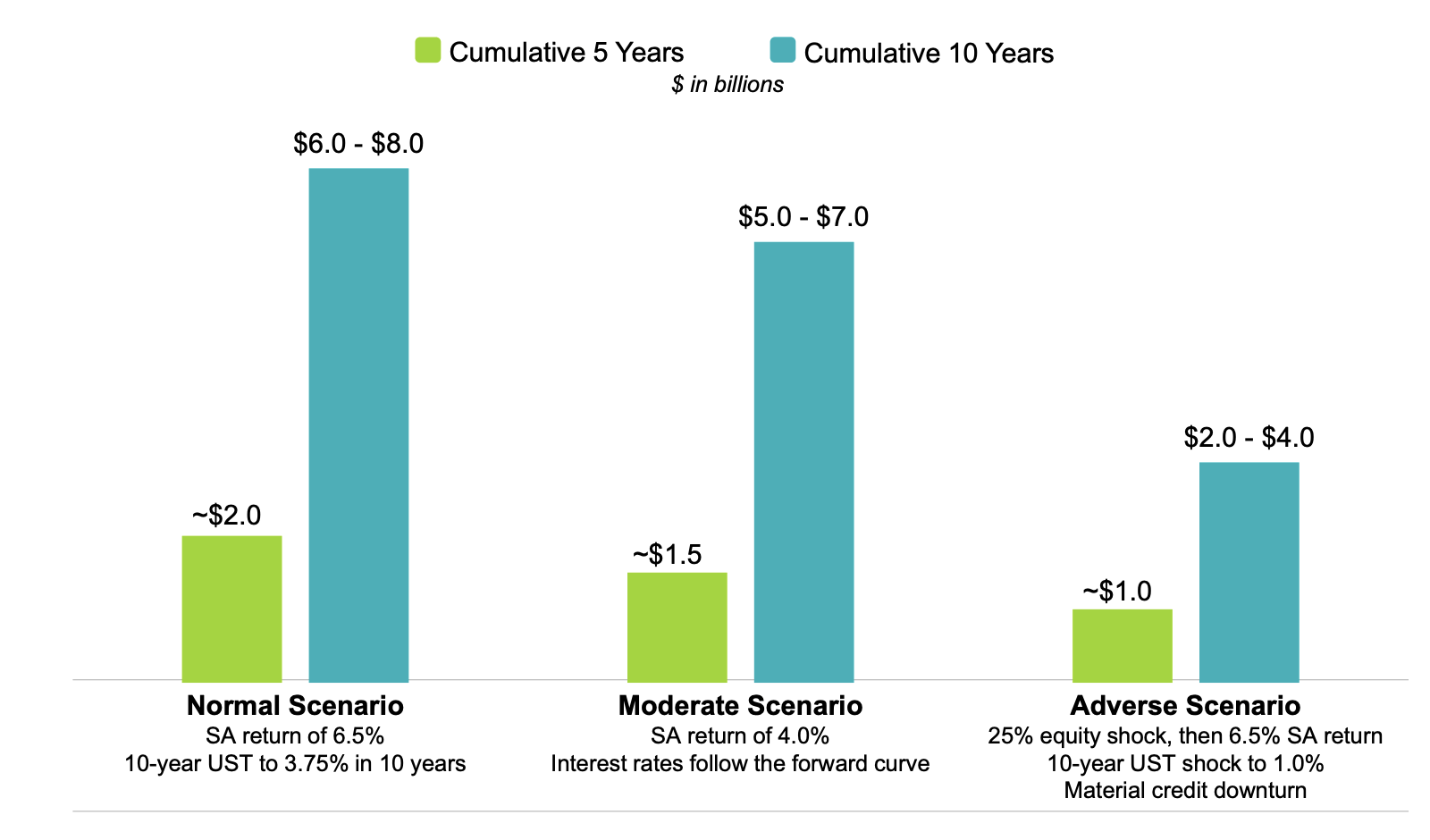

In September , management laid out its statutory free cash flow assumptions, and I expect to hear these targets reiterated. Since then, the S&P 500 has returned over 5%, and the 10-year treasury yield is over 3.9%. This is supportive of BHF operating within the normal to moderate scenarios, with the adverse scenario appearing less likely. In either scenario, BHF is positioned to repurchase at least 40% of shares at its current price over the next five years. As RBC recovers, I expect investors to grow more confident in these targets being achieved.

{kind=link}

Given its business, prolonged declines in equities and yields are a risk, but even then, it can continue ~$150-$200 million per year in repurchases, particularly given holding company liquidity. With equities having rallied and a soft-landing appearing more likely, this risk also appears less concerning. There is also the risk of a self-inflicted loss; however, BHF has a strong balance sheet. It has a $120 billion investment portfolio. $86 billion is in fixed maturity securities with 97% of those investment grade. It continues to pivot this portfolio to a more conservative posture with new money going into investment grade. While this could limit upside, it should make results less volatile.

BHF has 11% of its portfolio or $13 billion in commercial mortgages. The loan to value is 61%, and less than $4 billion are in office. Only 6% of its commercial holdings mature next year. While I continue to closely monitor this allocation, these factors leave me comfortable with BHF’s exposure.

BHF has a $146.61 in book value excluding AOCI. It has about $400 million year in free cash flow capacity, or about a 12% free cash flow yield. Its discounted valuation is due to the volatility and complexity of results. Shares have recently been weighed down by capital degradation, but BHF should see meaningful recovery in RBC in H1 2024. As management communicates that and reports that in H1 earnings releases, I expect shares to more fully value the company’s cash flow. In its moderate scenario, even assuming a 5x terminal free cash flow yield, shares are worth about $63, discounted back at a 10% rate. Given the market will likely continue to see some downside risk, I do not expect this to be fully achieved in 2024, but shares can move to the upper $50s as RBC rises and buybacks continue. I remain a buyer of BHF stock.

For further details see:

Brighthouse: Positioned For 2024 Capital Improvement