BV - BrightView Holdings: Business Stability Outweighs The Near-Term Headwinds

2023-04-04 22:59:59 ET

Summary

- BrightView has a mature business model and stable growth path because of the non-discretionary demand for recurring services.

- In Q1, the company recorded growth in annual contracts and snow volume realization.

- However, its operating profit faces headwinds from variability in the snow business, high inflation rates, and a spike in fuel prices.

- The stock is reasonably valued versus its peers.

BV Is On A Slow Growth Path

BrightView Holdings ( BV ) runs a landscape architecture and installation business, which is mature with a stable outlook. Because the landscaping industry is fragmented, it can offer opportunities for consolidation and market share gains. But its snow removal business suffers from seasonality and changing cost dynamics. Due to the warmer start in 2023, the company's snow business faces some imminent challenges. The flow-through was lower than expected due to below-average snowfall in the Northeast and the Mid-Atlantic. On top of that, its operating margin has come under the threat of rising input costs and inflation. I expect the topline and profit to shrink in Q2.

However, the long-term business trajectory does not appear to be under any threat, given the continued momentum in economic growth and manageable inflation. Robust liquidity outweighs the concerns associated with negative cash flows. BV stock appears reasonably valued versus its peers, especially after falling by 32% in the past six months. Investors should consider "hold" at this price level with a slight negative bias in the near term.

Business And The End Market Views

{kind=link}

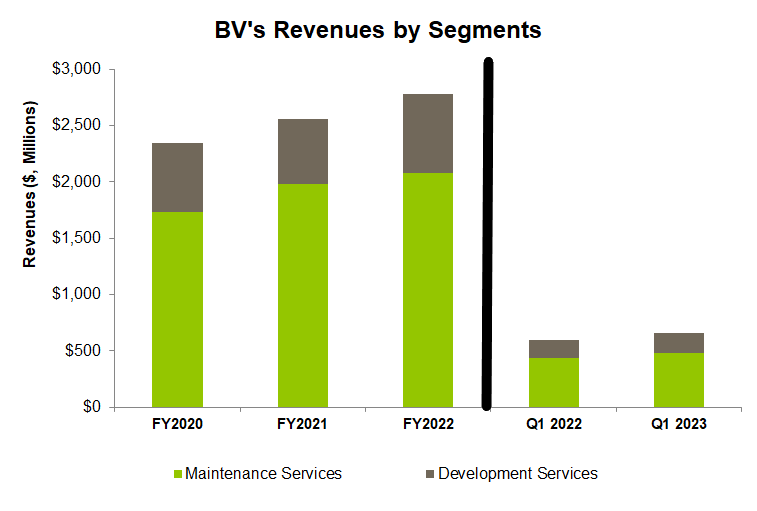

After Q1 2023 (ending December 31, 2022), BrightView's management conceded that it would need to throw more punches at the operating margin now that the topline has gained momentum. Despite low snowfall, it believes it can deliver growth and expansion through the land and development businesses. It has developed a robust backlog in the Development segment, resulting in ~6% organic growth in Q1. On top of that, pricing traction resulted in EBITDA topping the high-end of the previous guidance.

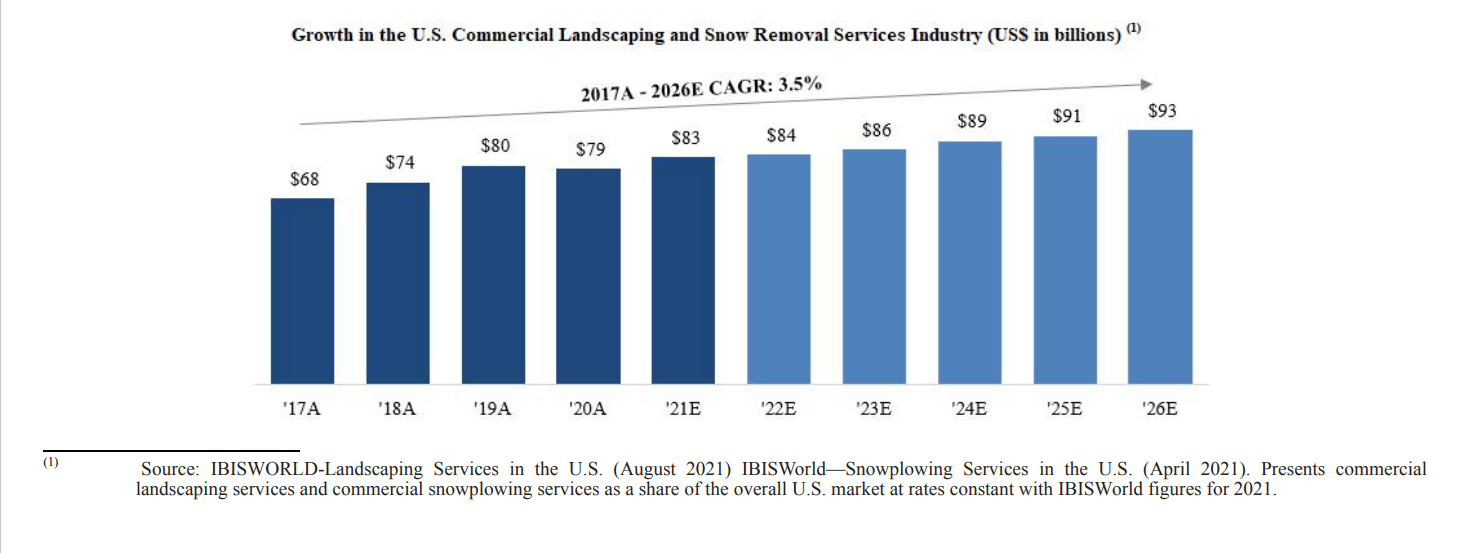

According to the company's estimates (as noted in the FY2022 10-K), commercial landscape maintenance, including snow removal, is an $83 billion industry. It is expected to grow at a 3.5% CAGR from 2017-2026. Its Development Services segment offers complex and specialized offerings, including landscape architecture and installation, irrigation and tree installation, pool and water features, and sports field services. Because of the non-discretionary need for these recurring services, it has generally exhibited stable and predictable growth.

But the path has several roadblocks and challenges. Over the past two years, its profitability has been adversely impacted by variability in the snow business, high inflation rates, and a spike in fuel prices. Even though it made an effort to correct the snow business margin, the flow-through was lower than expected due to below-average snowfall in the Northeast and the Mid-Atlantic.

Snowfall And Margin

{kind=link}

Investors may need to remember that BV's end markets are characterized as evergreen and seasonal. While the evergreen operations require year-round landscape maintenance, its snow removal services are a seasonal market. This is a counter-seasonal source of revenues because it allows for better utilize its crews and equipment during the winter months. Property managers also can optimize costs using the same service provider for snow removal and landscape maintenance services.

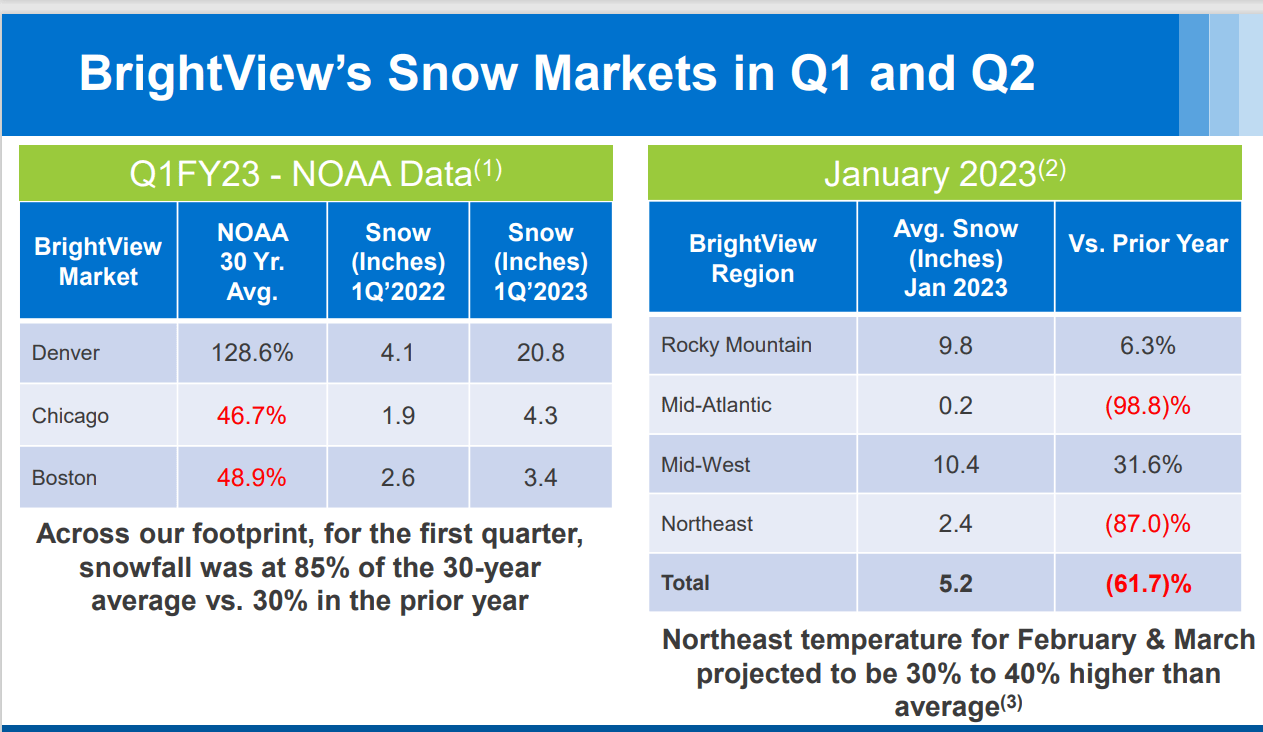

In Q1, there was wide variability in snowfall data. Denver saw above historical averages, while Chicago and Boston were significantly below average. Year-over-year, the US snowfall was higher in Q1 2023. But, two of the company's most significant snowfall revenue drivers, Northeast and Mid-Atlantic, were below-par, which pulled down the margin. So, even though the topline remained steady, the overall performance suffered.

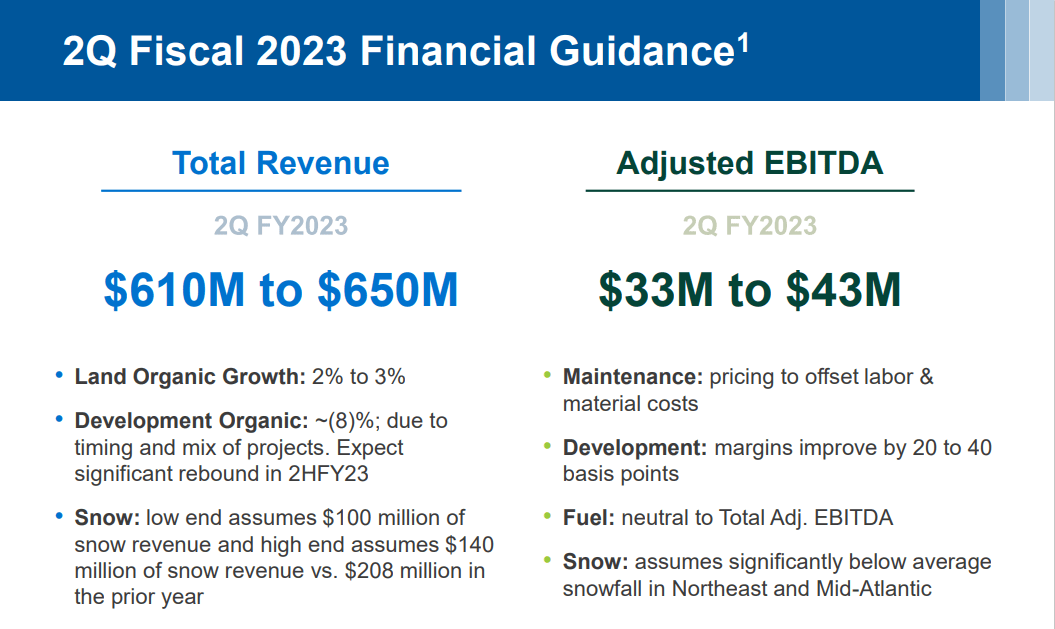

The year 2023 did not begin well for the company. The East Coast, which amounts to 60% of its snowfall business, saw lower snowfall this year. The higher temperatures indicate that snow levels will likely remain low. As a result, the management expects revenues to decline by ~4% in Q2 2023. The adjusted EBITDA can take a more severe 42% cut in Q2 compared to Q1.

Challenges, Strategies, And Outlook

{kind=link}

However, the shortfall in the snowfall market will not dent BV's long-term growth trajectory. The project size averages ~$1.2 million, per its estimates. Even with a lower snowfall footprint in Q1 2023, it still recorded a 6% growth in annual contracts and 44% in snow volume realization versus a year ago.

The most common challenge for the company is to increase market share in a highly fragmented industry. It currently holds only a small market share. The number of operators in this market is large. Approximately three-fourths of the market participants are sole proprietors. The other challenge is the effect of seasonality. Typically, its revenues and net income are higher in the spring and summer seasons (i.e., Q3 and Q4), while the snow removal services dominate revenues and margins in Q1 and Q2. So, given the current trend, the company's operating performance in Q2 will likely deteriorate, as reflected in the company's estimates.

{kind=link}

The third challenge for the company is to contain the rising operating costs. Over the past year, the input costs of raw materials related to fuel, fertilizer, chemicals, road salt, and mulch have gone north. To offset this, the company has adopted a strategy of self-performing snow management. Here, it employs direct labor without subcontractors. The strategy would enable it to secure higher margins by eliminating the middleman. The pricing efforts to offset increases in labor and material costs would be neutral. I think, due to the snowfall deficit, the benefit from these actions will be modest in FY2023 but will gain traction over time.

Economy And Inflation

{kind=link}

Over the past four quarters, the US GDP increased by 1.8% on average. During this period, the US consumer price index (or CPI), a measure of the inflationary situation, increased by 1.9%. However, since the beginning of 2020, the US GDP growth rate has outpaced CPI. So, the economy, at least until the recent past, does pose any concerning sign for BV's near-term outlook.

The Landscaping Market Outlook

{kind=link}

On the other hand, the landscaping markets will unlikely see any slowdown. So, the Development Services segment margin can improve by ~40 to 60 basis points. In Q2, margins can expand by 20 to 40 basis points due to disciplined cost management. The topline growth rate can accelerate in 2H 2023. According to the management's estimates, organic growth can reach ~10% in 2H 2023, resulting in "mid to high single-digit" organic growth in FY2023.

The Acquisition Benefits

BV has a robust M&A pipeline. The management has identified $700 million of an inorganic growth market, which can help its expansion strategy and deliver strong free cash flow. In January, it acquired Smith's Tree Care in Virginia. In the same month, it acquired Island Plant Company – a commercial landscaping provider on the island of Maui and Hawaii. These acquisitions bode well for BV following the expansion and integration of Minnesota and Boise. The company is focused on strategic transactions at attractive valuations to increase shareholders' values.

Cash Flows And Balance Sheet

In Q1 2023, BV continued to generate negative cash flow from operations compared to a year ago. Although the company's revenues grew versus the previous year, a high working capital requirement led by a decrease in other operating assets and a reduction in accounts payable kept the cash flow in the negative territory. Its free cash flows also remained negative and deteriorated during this period.

With additional borrowing availability under the Credit Agreement, BV's liquidity was $325 million as of December 31, 2022. Its leverage (debt-to-equity) of 1.18x is higher than its peers' average ([[SP]], [[HCCI]], and [[CENT]]). However, it has no significant maturity until 2029. Plus, it has also hedged $1 billion of its current debt, which would save $10 million in interest expense annually.

Analyst Rating And Relative Valuation

{kind=link}

According to data provided by Seeking Alpha, only one sell-side analyst rated BV a "buy" in the past 90 days, while four analysts rated it a "hold." One of the analysts rated it a "sell." The consensus target price is $8.7, suggesting a 54% upside at the current price.

{kind=link}

BV's forward EV/EBITDA multiple contraction is less steep than its peers. This typically results in a lower EV/EBITDA multiple. The company's EV/EBITDA multiple (7.4x) is lower than its peers' (SP, HCCI, and CENT) average (9.6x). So, the stock appears to be reasonably valued at this level.

What's The Take On BV?

{kind=link}

BV is managing a steady business through troubling water. Its commercial landscape maintenance, including snow removal, is a multi-billion-dollar industry, expected to grow moderately steadily from 2026, per its estimates. Because the evergreen operations require year-round landscape maintenance and the average contract size is reasonably large, its cash flows are predictable. However, the snow business is highly seasonal. Due to the warmer start in 2023, the company faces some imminent challenges. So, the stock hugely underperformed the SPDR S&P 500 Trust ETF ( SPY ) in the past year.

BV has ample liquidity. Although leverage is high, with no significant maturity before 2027, I do not see any near-term financial risks. Cash flows being negative can be concerning, though. I think the stock is apt for a "hold" at this price level.

For further details see:

BrightView Holdings: Business Stability Outweighs The Near-Term Headwinds