BV - BrightView's Fiscal Q3 Earnings: A Pruned Outlook

2023-08-08 09:15:00 ET

Summary

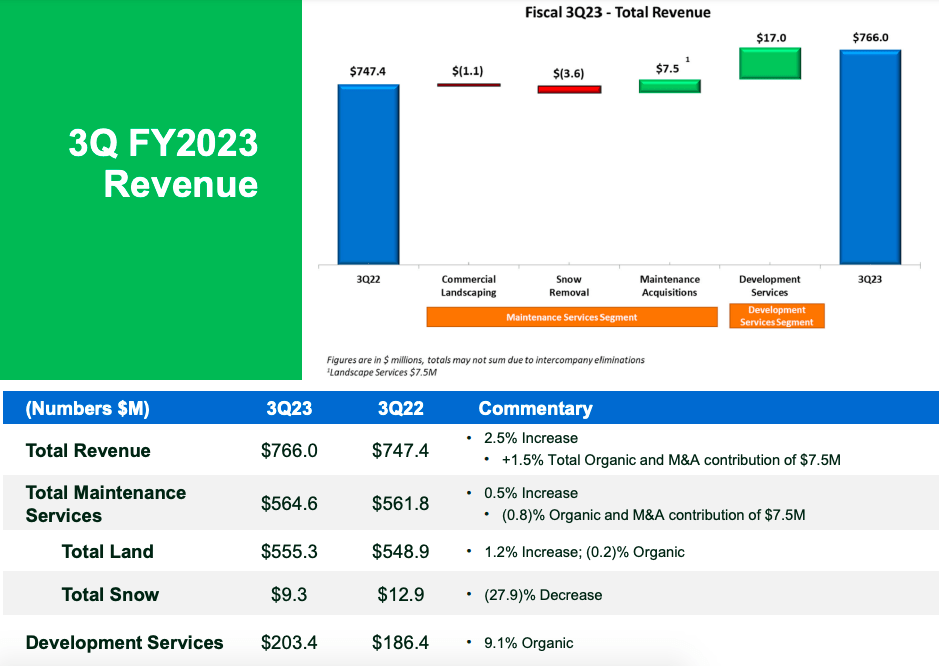

- BrightView Holdings, Inc. reported a 2.5% increase in revenue in its fiscal Q3 2023 earnings report, reaching $766 million.

- The company's growth trajectory shows promising signs of improved profitability and cash generation, driven by high quality contracts and disciplined pricing strategies.

- However, challenges remain, including the need for sustainable growth, successful implementation of Project Accelerate, and the search for a new CEO. Investors should maintain a holding pattern.

Thesis

BrightView Holdings, Inc. (NYSE: BV ), in its fiscal Q3 2023 earnings report, displayed a revenue increase of 2.5%, reaching $766 million. Despite beating Non-GAAP EPS estimates by $0.06 with an EPS of $0.44, the revenue fell short by $11.15 million. The company's growth trajectory, driven by high-quality contracts and disciplined pricing strategies, showed promising signs of improved profitability and cash generation.

However, this analysis argues that challenges remain, including the need for sustainable growth, successful implementation of Project Accelerate, and the search for a new CEO to steer the company towards value creation and better performance in subsequent quarters. This prompts a recommendation for investors to maintain a holding pattern until there's more clarity on those initiatives.

Company Overview

BrightView Holdings, Inc., headquartered in Blue Bell, Pennsylvania, and founded in 1939, operates in the U.S. commercial landscaping industry and is segmented into two main areas: Maintenance Services and Development Services. Maintenance Services provides an array of recurring services to a broad clientele, including 9,500 office parks, 7,500 residential communities, and 550 educational institutions, covering tasks from mowing to specialized golf course maintenance.

The Development Services segment focuses on landscape architecture and new projects, strengthening BrightView's standing as a full-service provider that also serves as an official field consultant to various baseball leagues.

BrightView Holdings Fiscal Q3 Earnings Highlights

In its recent quarter , BrightView's financial report showed a revenue uptick of 2.5%, accumulating $766 million.

{kind=link}

The company's growth trajectory, emanating from both land and development segments, displayed a pattern of pursuing more lucrative contracts and adopting disciplined pricing strategies. In particular, the maintenance segment saw an expansion in margins. Whether this trend could lay the foundation for sustainable profitability and an improvement in cash generation, if it persists, remains to be seen.

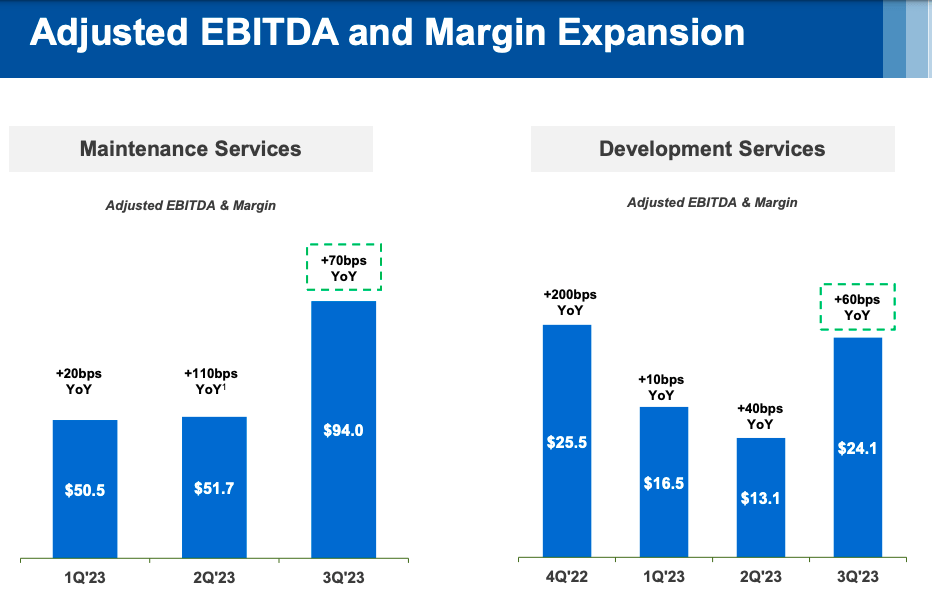

BrightView's third-quarter report also put a spotlight on its ability to grow margins, with an increase of 70 basis points year-over-year in the maintenance sector and 60 basis points in development.

{kind=link}

According to management, this appears to align with the company's meticulous approach to high-quality contracts and precision in pricing strategies, seemingly translating to profitability which they noted several times on the conference call.

There's also an undertone of anticipation surrounding the expansion of Project Accelerate, which the company foresees as a potential catalyst to reach or even surpass the targeted $20 million in annual cost savings. In a nutshell, and for the most part, the "project" is a company-wide program created to reduce overhead costs; however, as of now, the details are slim and more information is expected to be provided on the subsequent earnings call.

{kind=link}

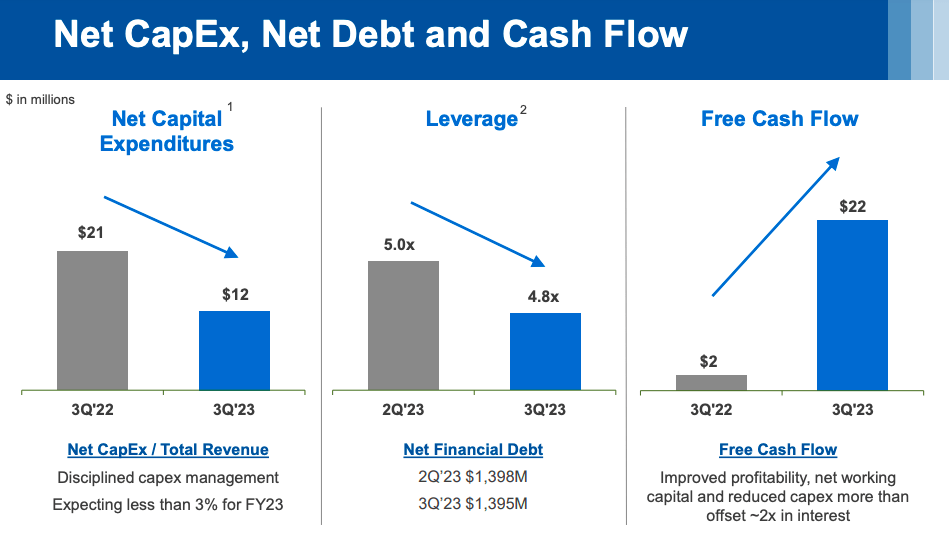

Another noteworthy aspect of BrightView's financial picture this quarter is the enhanced free cash flow, totaling $22 million. This appears to be a product of the ongoing decisions to reduce capital expenditures, coupled with an improvement in profitability.

Lastly, BrightView's search for a new CEO is ongoing and represents a statement about the company's future trajectory. It goes without saying that the search for a leader who can articulate a clear and focused growth strategy is underlined by an expectation to foster value creation as the integration of fresh leadership, and the inherent capabilities of the existing executive team could collectively contribute to a new chapter in BrightView's performance in subsequent quarters.

Performance

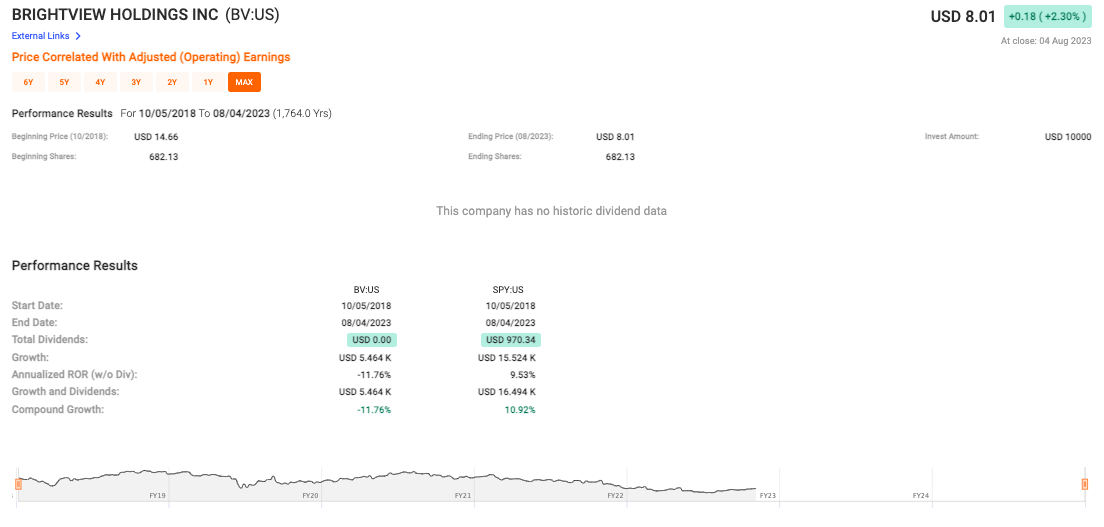

Unfortunately, BrightView's five-year performance is anything but bright and reveals a troubling trend with the share price plummeting from USD 14.66 to USD 8.01, translating into a negative annualized rate of return ((ROR)) of -11.76%. This drastic reduction in share price, in my opinion, is a red flag for investors.

{kind=link}

Comparing BV's performance to that of the S&P 500 Index (SP500) further emphasizes the company's struggles. While the S&P experienced an annualized ROR of 9.53% and compound growth of 10.92%, BrightView lagged far behind. Ultimately, this divergence underscores the firm's failure to capture market trends and suggests systemic problems within the company.

Valuation

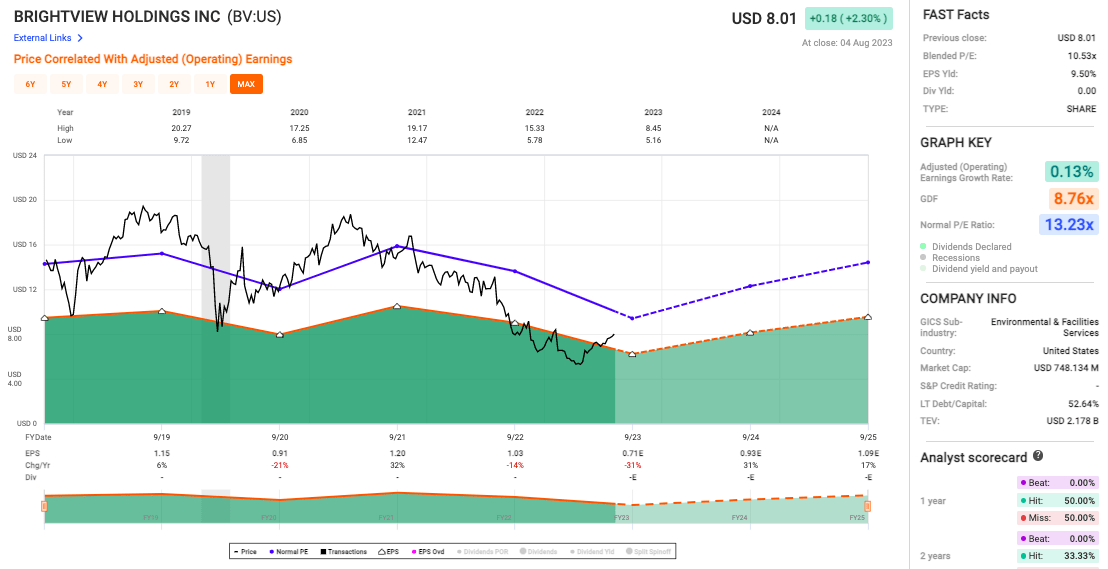

With a blended P/E of 10.53x (see chart below), BrightView appears to be undervalued when compared to the normal P/E Ratio of 13.23x. On the surface, this suggests a potential upside opportunity; however, a mere 0.13% adjusted operating earnings growth rate is definitely sluggish and raises concerns over the company's ability to significantly grow profits in the near term which may explain the lower P/E ratio.

{kind=link}

And while the EPS Yield of 9.50% may appear attractive, given the company's negligible earnings growth, I believe it warrants further caution.

Risks & Headwinds

I think that one of the nuances worth dissecting is the nature of revenue growth. On the surface, a 2.5% increase in revenue might seem relatively modest, especially in light of some of the previously highlighted overarching positive financial performances the company exhibited. But beneath that top-line number, there's a story of strategy in play. The company's pivot towards a focus on high-quality contract opportunities, arguably a prudent move for sustainable growth and risk management, may have acted as a double-edged sword. While it likely bolstered the quality and stability of revenues, this shift might also have constrained the more aggressive expansion that other growth-driven strategies might have afforded.

Adjusting Expectations

The recent adjustment in full-year revenue guidance could be interpreted in a few ways. At its core, this revised guidance seems to underscore a commitment to driving profitability, perhaps signaling a belief that chasing pure top-line growth without ensuring bottom-line returns might be a Pyrrhic victory. However, for market participants whose primary lens is top-line growth, this recalibration might introduce a note of caution. The key question then becomes: Is this revised guidance a mere blip or a precursor to a broader strategic reorientation?

The Weight of Project Accelerate

Lastly, like many businesses in transformational phases, the company is placing considerable emphasis on its new initiatives, particularly Project Accelerate. These strategies' success or lack thereof could significantly shape future trajectories. Initiatives like these are not just operational overhauls; they often encapsulate a company's vision for its future. While the optimism surrounding such projects can energize a corporate culture and potentially act as a market differentiator, their failure might not just affect immediate financial results, it could ripple into investor sentiment and confidence in leadership. As noted earlier, we're probably going to have to wait until next quarter to learn more on how the project is shaping up.

Final Takeaway

Based on the information provided, I would rate BrightView Holdings stock as a "hold." While the company shows positive signs in its recent quarter, with an uptick in revenue and an increase in margins, there are underlying concerns such as a troubling five-year performance trend and negligible earnings growth. The potential success of initiatives like Project Accelerate and the integration of new leadership could lead to future gains, but until there's more clarity on these fronts, a cautious approach seems warranted.

For further details see:

BrightView's Fiscal Q3 Earnings: A Pruned Outlook