BRLT - Brilliant Earth: Waiting For Gains To Show Up In Earnings

2024-01-11 11:41:35 ET

Summary

- Brilliant Earth's share price has increased by 12% since October 2023, as investor sentiment improved following its Q3 2023 earnings report and its share repurchase program.

- Improved sales growth is expected to reflect in Q4 2023, however, the adjusted EBITDA figure is wanting at a time when the market multiples are already high.

- A spate of showroom openings during the year along with improved analyst expectations for 2024 do give hope, but it's better to wait and watch for the company's outlook.

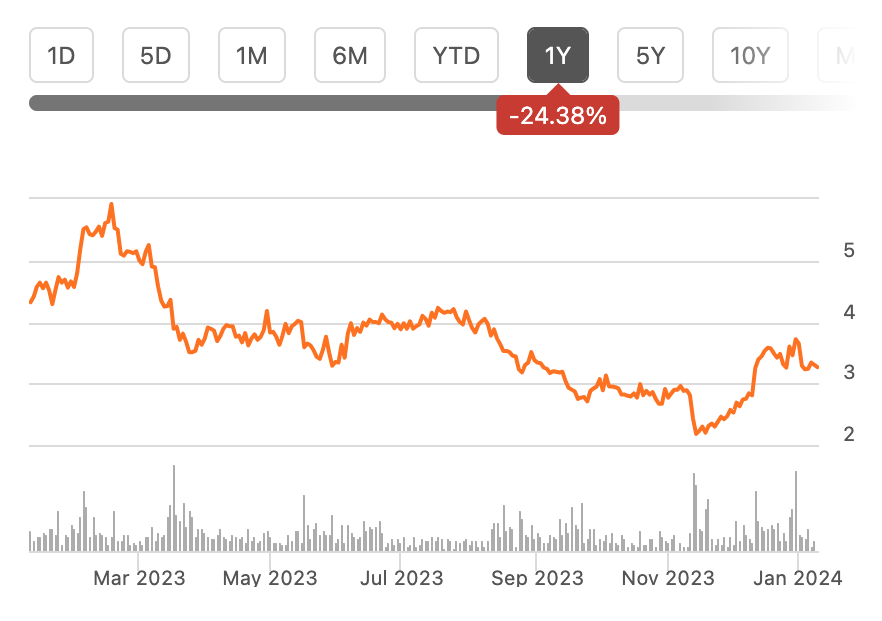

Since I wrote about the jeweler Brilliant Earth ( BRLT ) in October last year, its share price is up by 12%. I had given it a Hold rating at the time, but even then it was evident that the stock was at the cusp of a potential turnaround.

{kind=link}

The turnaround was contingent on a sales growth uptick based on two factors. First, the relatively weak base of the second half of the year (H2 2022) could naturally result in higher growth. Next, the festive season in the final quarter (Q4 2023) held particular potential since the company had invested in new stores and collections during the year. Brilliant Earth had also upgraded its adjusted EBITDA target, which was positive for its price-to-earnings (P/E) ratio if it materialized.

Why did the price rise?

As it happens, improved sales growth became visible in Q3 2023, pulling up the numbers for the first nine months of the year (9m 2023). Presumably on account of softening inflation, it also saw an uptick in gross margin. No sooner did the company release its earnings in November, that the stock price started inching up. Here are the key highlights of the earnings report:

- Net sales grew by 2.5% in Q3 2023 and pulled up the growth for the first nine months (9m 2023) to 0.6% after sales contracted by 0.5% in H1 2023.

- The order volume also grew by 16.7% in Q3 2023 and the increase was 19.2% for 9m 2023, up from 15.9% for H1 2023.

- The adjusted EBITDA margin came in at 6.4%, maintaining the level from H1 2023. This is higher than the 5.7% projected for 2023 at the midpoint of the earlier guidance range.

- The gross margin jumped up to 58.5% in Q3 2023 (Q3 2022: 54.7%), resulting in a 57.1% margin for 9m 2023, which is an increase of 440 basis points from the same time last year.

Brilliant Earth's share repurchase program of $20 million, announced in December, could also have played some part in sustaining higher price levels. I wouldn't stress this factor too much, though, since the proposed repurchase is only around 6.2% of the company’s current market capitalization and will be carried out over the next two years. It could, however, make a marginal difference to the share price.

Mixed prospects for the remainder of 2023

Despite the positive trends in Q3 2023, the path ahead for the company isn’t entirely clear even now, considering that in the latest earnings update, Brilliant Earth downgraded its net sales and adjusted EBITDA forecast.

It now expects net sales to come in the range of $444-450 million, compared to the earlier forecast of $460-490 million. At the midpoint, this is a 5.9% forecast downgrade. While the company will manage to see a 1.6% growth, it's still a significant decline from the 15.7% increase seen in 2022.

The adjusted EBITDA is now expected to be in the range of $22-24 million, compared to the earlier projection of $22-35 million. At the midpoint, this is a downgrade of 19.3%. Needless to say, this represents a far bigger drop in the profit measure of 41% compared to a 27% decline seen earlier. The adjusted EBITDA margin is now expected to be 5.1% compared to 6% earlier, both of which are a decline from the 8.9% in 2022.

While the adjusted EBITDA margin is expected to be exceptionally small at 1.7% in Q4 2023, it isn’t all bad. The net sales growth estimate is 4.5%, which will make it Brilliant Earth’s best quarter for growth in 2023.

Forecast for 2024 and beyond

Analysts expect a further uptick in revenue growth to 5.1% in 2024 and also expect a sharp recovery in the earnings per share [EPS] by 39.4%. For perspective, the GAAP diluted EPS has declined by 80% for 9m 2023 while the adjusted diluted EPS has declined by 27.8% during this time.

The company itself has ambitious long-term targets as well, both in terms of revenue and adjusted EBITDA (see chart below). Positive as they are, it’s unclear whether it can achieve these targets as of now.

Long Term Targets (Source: Brilliant Earth)

Growth driven by expansion

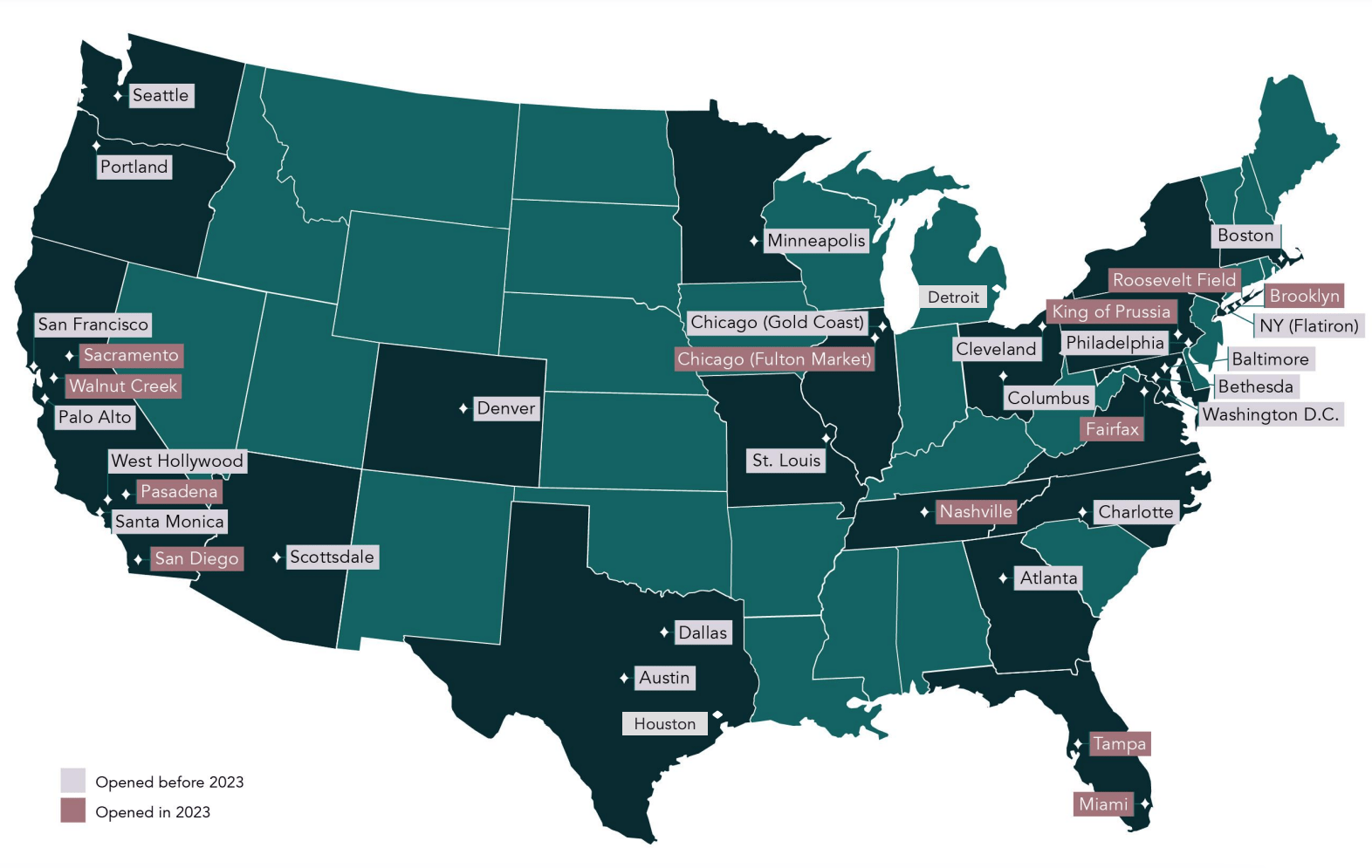

Potentially underpinning the improved expectations for the company are its store openings. In Q3 2023 alone, it opened five new showrooms and up to 9m 2023, it had already opened 37 new showrooms, exceeding its full-year target. The company has also said that some of these are “yielding strong incremental growth”.

{kind=link}

Market multiples are high

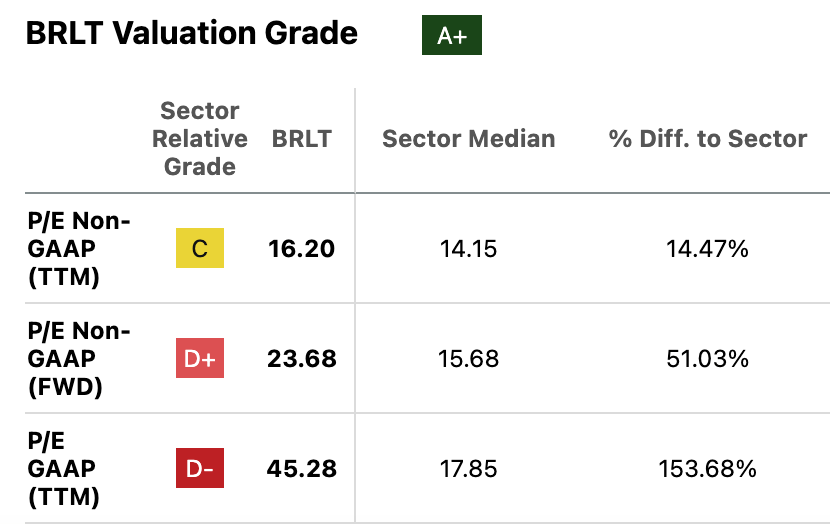

The positive prospects for 2024 result in a forward non-GAAP P/E ratio of 17x, which is still higher than that for the consumer discretionary sector at 15.7x, much like the rest of the P/E ratios (see table below). Notably, the non-GAAP forward P/E is also much higher than the 9.75x ratio for its immediate peer Signet Jewelers ( SIG ) along with the other multiples as well.

{kind=link}

What next?

With this as the background, it’s tough to get behind a Buy rating for Brilliant Earth, even with the recent price rise. Sure, there are signs of improvement. Its revenue growth has turned positive, and Q4 2023 will likely be its best quarter in the year. The sales forecast for 2024 is positive too.

But the earnings picture is wanting. It has seen a big decline in profits this year. While this is understandable going by its investments in store openings this year, the recent downgrade in adjusted EBITDA expectations is disappointing. It’s encouraging, though, that analysts expect an uptick in earnings in 2024, making its forward P/E relatively more attractive.

For now, however, I’d like to wait for the company’s outlook for the year when it releases its full-year 2023 results in March. These can help determine if Brilliant Earth can indeed see a good 2024. By that time, it's also possible that the price will correct from its current highs to make for better-placed market multiples. I’m retaining a Hold rating.

For further details see:

Brilliant Earth: Waiting For Gains To Show Up In Earnings