VTOL - Bristow Group: Decent Quarter And Strong Outlook - Buy

2023-11-07 09:21:59 ET

Summary

- Leading aviation services provider Bristow Group Inc. reported vastly improved quarterly results mostly due to higher fleet utilization in the offshore energy services segment.

- The company raised full-year expectations and affirmed projections for substantially increased profitability next year.

- Starting in 2025, Bristow will also reap the benefits from material investments in new government SAR contracts which should provide healthy margins and cash flows well into the next decade.

- Given the company's constructive outlook and undemanding valuation based on my profitability expectations for 2025, I am reiterating my "Buy" rating on the shares with a price target of $35.

Note:

I have covered Bristow Group Inc. ( VTOL ) previously, so investors should view this as an update to my earlier articles on the company.

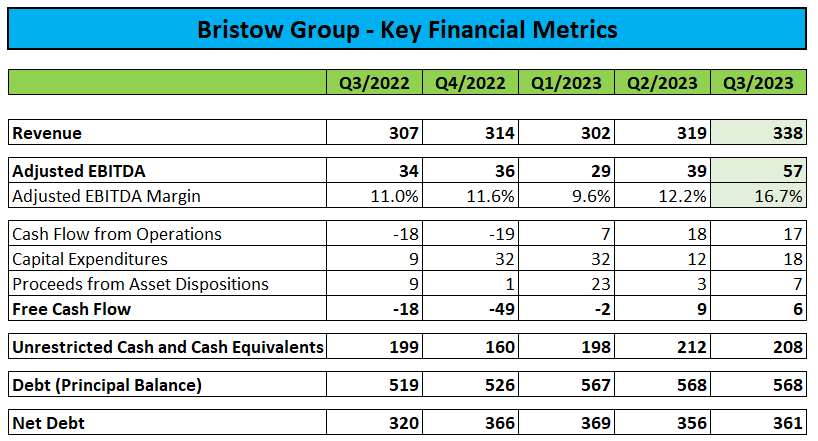

Earlier this week, leading offshore helicopter services provider Bristow Group or "Bristow" reported strong third quarter results as the ongoing recovery of the offshore oil and gas markets resulted in higher fleet utilization.

Consequently, revenues and Adjusted EBITDA reached new multi-year highs:

Regulatory Filings and Company Presentations

{kind=link}

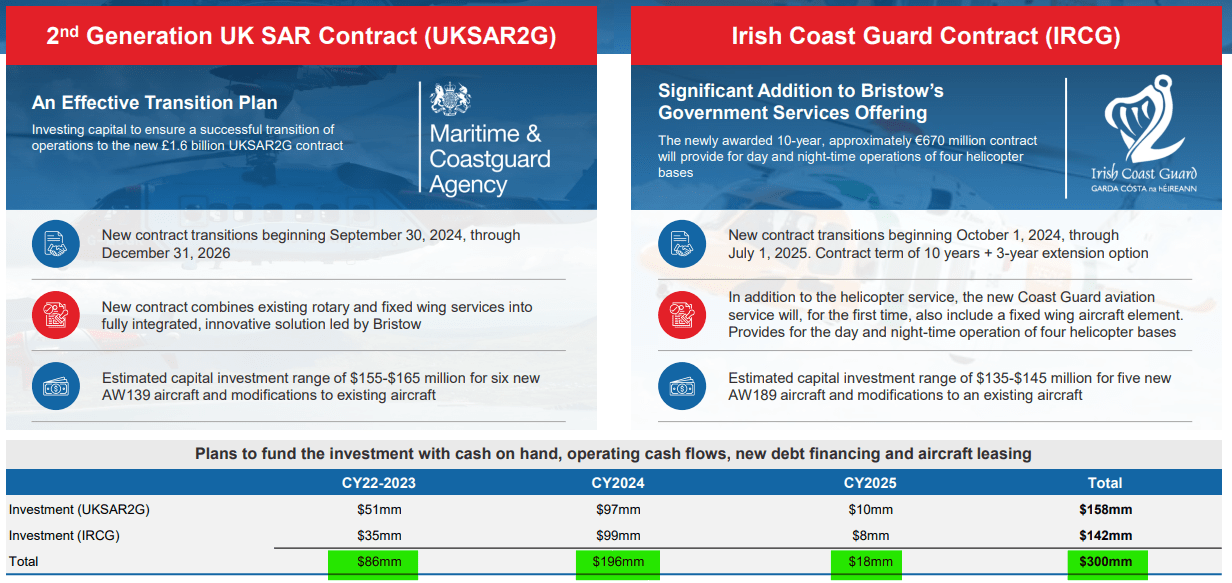

Elevated SAR Capex To Impact Near-Term Cash Flows

However, free cash flow generation continues to be impacted by elevated capex commitments related to the company's recent government search-and-rescue ("SAR") contract wins in the United Kingdom and Ireland:

{kind=link}

In aggregate, Bristow expects to incur $300 million in capital expenditures in with almost $200 million anticipated for next year, as outlined by management on the conference call (emphasis added by author):

As we have noted in our earnings presentation, we have a capital investment of approximately $300 million related to the successful award of contracts with the U.K. and Irish Coast Guard. Much of this capital investment is expected to happen in 2024, as we will be adding 11 new helicopters to our fleet . Our search and rescue contracts are long-term in nature, typically 10 years with attractive returns. So once we were through with the investment period, we have a long-term cash yield as noted on slide 16 of our presentation.

We plan to fund this investment with cash on hand, operating cash flows, new debt financing of a similar structure to what we currently have with NatWest and/or aircraft leasing. Due to the nature of these long-term cash generative contracts, we have access to competitive financing and sufficient flexibility in how we structure it. As we've stated before, we believe this business model will continue to generate strong cash flows.

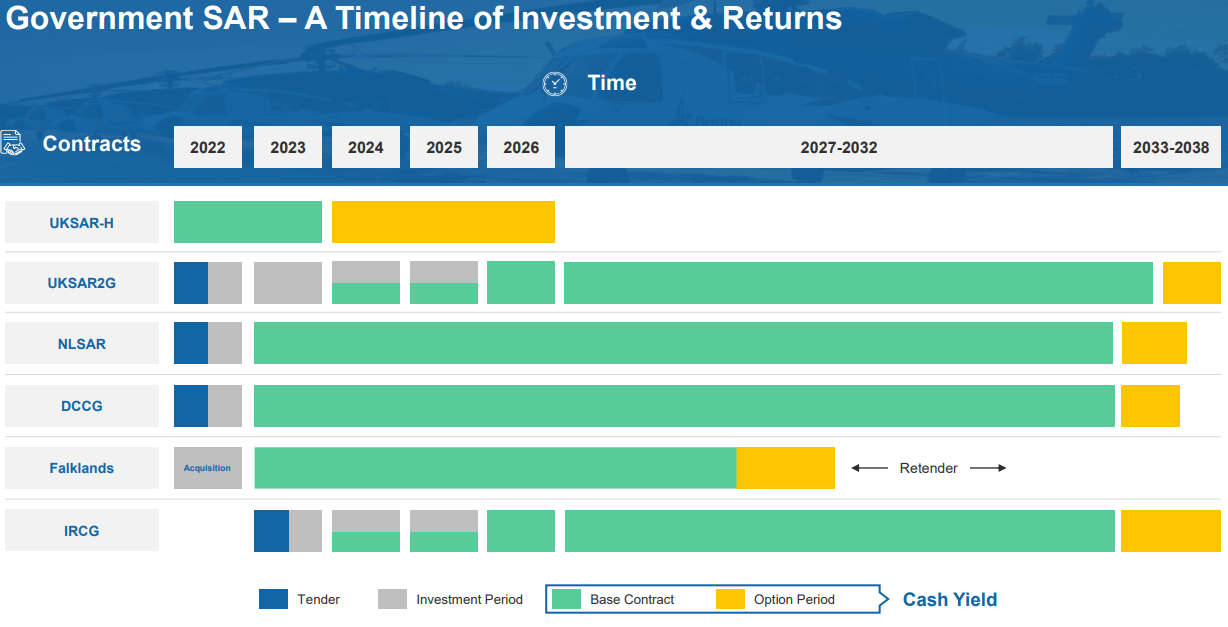

With the lion's share of these investments expected to be behind the company in 2025, the company's SAR business should provide Bristow with solid cash flows for many years to come:

{kind=link}

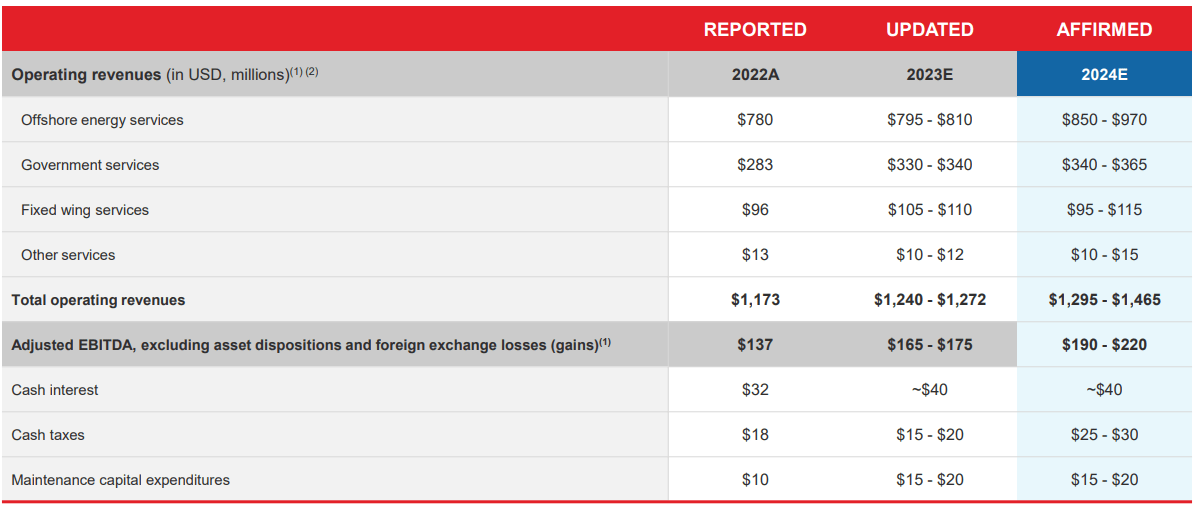

Full-Year Projections Raised

As a result of the strong offshore energy and, to a lesser extent, fixed wing services performance, the company now expects full-year Adjusted EBITDA in a range of $165 million to $175 million, up from previous projections of $150 million to $170 million.

In addition, management reaffirmed expectations for meaningful top- and bottom line growth to continue next year:

{kind=link}

On the conference call, management pointed to unfavorable foreign exchange movements as the main reason behind the decision not to raise 2024 guidance at this point.

In addition, Bristow continues to experience major supply chain issues related to the company's fleet of Sikorsky S92 helicopters. As Sikorsky remains behind its obligations under the respective power-by-the-hour service agreement, the resulting lack of serviceable S92s has caused the company to miss out on additional contract opportunities in the U.S. Gulf of Mexico and the North Sea.

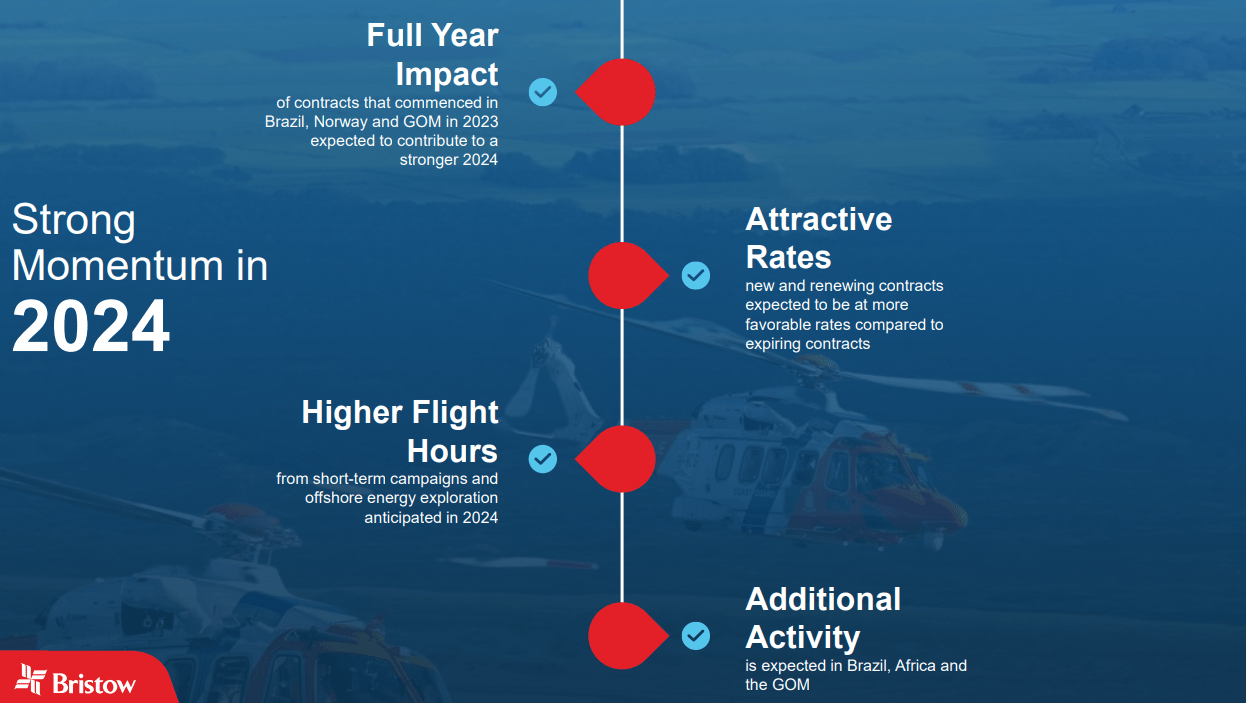

Further Improvement Expected in 2024 And Beyond

With no material contributions from the new SAR contracts expected for next year, Bristow's projected 2024 growth will be derived from its larger offshore energy services segment which is benefiting from the ongoing recovery in offshore oil and gas exploration activity:

{kind=link}

With the new SAR contracts finally coming into play and more legacy offshore energy-related contracts transitioning to prevailing market prices, 2025 should see a further, substantial improvement in profitability:

Company Projections / Author's Estimates

Valuation And Price Target

With the government services segment providing an increasingly stable baseline, assigning a multiple of 7x EV/Adjusted EBITDA seems warranted thus resulting in a $35 price target for the shares.

Author's Estimates

Upcoming PHI Group IPO A Potential Catalyst

Lastly, investors should note that closest peer PHI Group, Inc. ( PHIG ) recently filed for a $100 million initial public offering with Barclays and Goldman Sachs acting as lead underwriters. Shares are expected to be listed on the NYSE under the ticker "ROTR."

Clearly, the upcoming PHI Group IPO has the potential to also draw some attention to Bristow Group's thinly-traded shares.

Bottom Line

Bristow Group reported materially improved quarterly results and raised its full year outlook mostly as a result of improving fleet utilization in the company's offshore energy services segment, a trend that is widely expected to persist for the next couple of years.

Please note that without foreign currency headwinds and major supply chain issues related to the company's fleet of Sikorsky S92 helicopters, the company's outlook would have been even better.

Starting in 2025, Bristow will also reap the benefits from its material investments in new large-scale government SAR contracts which should provide the company with healthy margins and cash flows well into the next decade.

Given the company's strong prospects and undemanding valuation based on my profitability expectations for 2025, I am reiterating my " Buy " rating on the shares while introducing a price target of $35.

Key Risk Factors:

Offshore energy services stocks are heavily correlated to oil prices so any sustained down-move in the commodity would almost certainly result in the company's shares taking a hit.

In addition, the company has considerable foreign exchange exposure, particularly the British pound. And material weakening of the pound against the dollar would negatively impact the company's top- and bottom line.

For further details see:

Bristow Group: Decent Quarter And Strong Outlook - Buy