BTI - British American Altria And Philip Morris - Which One Stands Out As The Weakest?

2023-12-01 15:53:02 ET

Summary

- Reframing from "What to buy?" to "What to sell?" I take an alternative look at Altria Group, Philip Morris International, and British American Tobacco.

- I will show which of the three companies has the least strong brand portfolio, the most opaque future prospects, and the weakest profitability.

- I will discuss the quality of the companies' balance sheets, also considering the value of the more or less hidden assets on the balance sheets of Altria and British American.

- Finally, I will explain which of the three stocks I'd sell if I were in the position of an investor who has decided to reduce the number of his holdings.

Introduction

Isn't it easy to find arguments in favor of a certain stock? There are of course many reasons why an investor might decide to buy a particular stock, but a high dividend yield is definitely one of the more obvious reasons, apart from a growth-laden narrative (e.g. artificial intelligence, GLP-1 receptor agonists).

From this perspective, the tobacco sector offers us some pretty obvious opportunities, at least so it seems. With current dividend yields of 9.4% and 9.1% respectively, Altria Group, Inc. ( MO ) and British American Tobacco p.l.c. ( BTI , BTAFF ) are the most obvious examples, but Philip Morris International ( PM ) is certainly no mean feat either with a yield of 5.5%.

While I believe that dividend (growth) investing is a strategy with many advantages, also from a psychological perspective, it would be rather foolish to pick such stocks just because of their high dividend yields. Granted, PM, MO and BTI are all what I would call blue-chip companies and they all have a very long operating history, but it is still important to take a closer look, yet without falling prey to analysis paralysis.

In this article, I will take a fresh look at the "Big 3". I put myself in the shoes of an investor who has decided to reduce the number of his holdings and - as the owner of BTI, MO, and PM - sell a tobacco stock. Therefore, I have taken a rather conservative, maybe even skeptical stance. I will detail which of the three companies has the weakest brand portfolio, the riskiest balance sheet and the weakest profitability, while deliberately ignoring valuation. All too often, a mediocre stock is bought because it is cheap. This may be a viable strategy for some investors, but the conventional, long-term investor is best served by buying great companies at a fair price.

A Look At The Companies' Portfolios Reveals A Clear Laggard

All three companies are predominantly active in the premium cigarettes segment. For example, almost 90% of cigarettes sold by Altria (the company only operates in the U.S.) are Marlboro cigarettes, while the discount segment only accounted for 6% of cigarette volume in 2022. Philip Morris International's cigarette portfolio is much more diversified, but Marlboro still accounts for almost 40% of sales in 2022. At BTI, what it refers to as its "strategic brands" (Dunhill, Kent, Lucky Strike, Pall Mall, Rothmans, Newport, Natural American Spirit and Camel), accounted for 66% of 2022 cigarette volume.

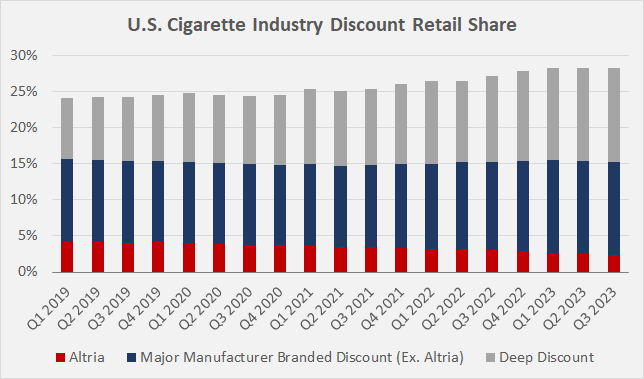

Thanks to their focus on premium cigarettes, all three companies have strong pricing power, which (in addition to efficiency improvements) is an important driving factor in their continued profit growth despite declining volumes. However, in times of high inflation, consumers tend to trade down, which limits Big Tobacco's scope for price increases. Figure 1 shows the continued weakness of Altria's discount segment, but also that of other major manufacturers operating in the U.S. such as British American and Imperial Brands ( IMBBY , IMBBF , see my comparative analysis with BTI).

{kind=link}

Figure 1: U.S. cigarette industry discount retail share on a quarterly basis (own work, based on Altria Group, Inc. filings)

In my view, the data shows not only that the major manufacturers are rather weak in the discount segment, but also that in particular Altria's value proposition is getting worse. However, this is not necessarily due to poor execution. Smaller competitors, such as Vector Group ( VGR ), benefit from a cost advantage under the Master Settlement Agreement, whose payments depend on the volume of cigarettes sold each year (e.g. p. 4, VGR 2022 10-K ).

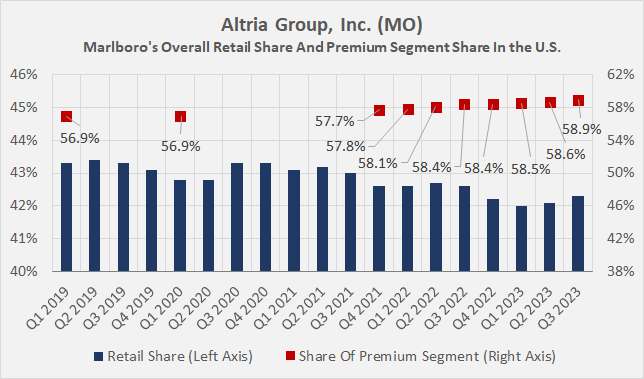

While this sounds worrying, I don't think the growing competition from discount brands should be overstated. In this context, it was encouraging to see, for example, PMI reporting 2% volume growth for Marlboro in 2022 (p. 3, PM 2022 10-K ) and Altria continuing to report an increase in Marlboro's market share in the U.S. premium segment (red squares, Figure 2). Also, it looks like the market share of deep discount brand is leveling off as inflation moderates.

{kind=link}

Figure 2: Marlboro’s overall retail share and share of the premium segment in the U.S. (own work, based on Altria Group, Inc. filings)

Taken together, I think it is fair to conclude that Altria and British American operate a quasi duopoly in premium cigarettes in the U.S., while British American, Philip Morris, and to a lesser extent Imperial Brands and Japan Tobacco ( JAPAF , JAPAY ) form an oligopoly in the rest of the world. I expect the major players to continue to exert their strong pricing power, but I think the continued decline in Altria's market share (blue bars in Figure 2) is at least a little worrying and worth keeping an eye on. Its main competitor in the U.S., BTI, continues to see market share gains (+10bps in 2022, +60bps in 2021 and +45bps in 2020).

Altria's comparatively weak position is also important from the perspective of smoke-free products. Altria is largely focused on acquisitive diversification (e.g., the disastrous acquisition of its stake in Juul Labs), while PMI's continued heavy investment in R&D (I discussed its comparatively high capital expenditure in another article ) has resulted in its market-leading heated tobacco platform IQOS. Due to the termination of its marketing agreement with Altria in October 2022 ( see this article ), PMI will be able to market IQOS itself in the U.S. from May 2024. It will likely utilize the distribution capabilities it gained through the acquisition of Swedish Match, which is also the manufacturer of the market-leading oral nicotine pouch brand Zyn (slide 7 of this presentation ). British American is the company behind Vuse-branded e-vapor products, and I think it's fair to say that the company is very successful in this area ( discussed here ). Its efforts in heated tobacco are less successful, and it lacks the strong presence in oral nicotine products that PMI gained through its very smart (and reasonably priced) acquisition of Swedish Match. Still, I don't think it's a stretch to consider BTI the clear number two in smoke-free products.

While Altria is developing its own heated tobacco products ( see this article ) and recently acquired e-vapor company NJOY Holdings, Inc. , the company's future in the smoke-free space remains rather opaque. Therefore, and due to the comparatively weak performance in cigarette volumes and brand concentration risk, I consider the U.S.-focused company to be the weakest in terms of portfolio quality and concrete future prospects.

All in all, of the "Big 3" I would sell Altria stock if I had to, and feel most comfortable with my investment in Philip Morris International (but as so often safety comes at a price). However, that doesn't mean I really think Altria stock is a sell. The main reason why I will hold on to my position - despite the portfolio weakness/uncertainty - is the fact that cigarettes are still very affordable in the U.S., with a pack costing similar to Russia, Sweden, Bulgaria, Switzerland and Mexico on a purchasing power parity basis. Furthermore, it is really surprising to see that, unlike most countries in the world, the affordability of cigarettes in the U.S. has not really changed between 2010 and 2020. Of course, investors should also take note of the "fat tail" risk arising from the regulatory perspective, which is particularly relevant for Altria.

The Weakest Play From A Profitability Perspective

Tobacco companies are known for their extremely high profitability. Cigarettes are very cheap to manufacture, all major players have highly developed distribution capabilities and the industry is consolidated. Since cigarette advertising is banned in most countries, marketing expenditures are also very low. The Master Settlement Agreement, as mentioned earlier, treats small companies more favorably, but it is fair to say that the costs involved are manageable.

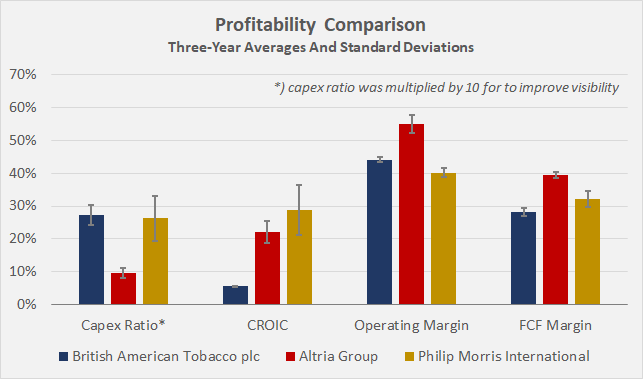

Figure 3 compares four key profitability ratios. The capex ratio (capex divided by net sales) - which has been scaled by a factor of 10 for better visibility - is broadly identical for BTI and PM, which spent almost three times as much on capex as Altria in the period 2020 to 2022. At first glance, this suggests that Altria is the most profitable.

{kind=link}

Figure 3: Comparison of four profitability metrics for Altria Group, Philip Morris International, and British American Tobacco plc (own work, based on company filings)

However, in my view, the low capex ratio is a sign that Altria continues to under-invest in the business. Granted, maintaining the core Marlboro brand does not require much maintenance capex (recall Figure 1 - Marlboro continues to gain share in the premium segment). However, I think the difference in capital expenditure is largely due to PMI and BTI making significant investments in heated tobacco and vaping products. Considering that Altria has started developing its own heated tobacco device (SWIC, serving a small consumer niche ) and expects to commercialize heated tobacco products under the Ploom brand ( joint venture with Japan Tobacco) in the U.S., it is only reasonable to expect an increase in capital expenditures and thus a decrease in free cash flow profitability. However, Altria's underlying profitability is still significantly higher than PM and BTI, both in terms of operating income and cash earnings, so I would not over-interpret the expected increase in capex ratio. However, considering the already quite payout ratio, the need for higher investments is likely one reason for the company's revised dividend policy .

With regard to achieving appropriate returns for shareholders, I compared the three major tobacco companies in terms of cash return on invested capital (CROIC). This is a derivation of the well-known ROIC, which takes into account free cash flow instead of net operating profit after tax. As an aside, I have adjusted free cash flow for stock-based compensation and working capital movements on a three-year rolling average basis.

British American Tobacco is by far the worst performer in this context, with a three-year average CROIC of just 5.6%. This is well below its CAPM-derived (Capital Asset Pricing Model) derived cost of equity, which varies between 10.5% and 15.8% depending on the beta selected. However, the apparently poor result is partly due to the acquisition of Reynolds American Inc. by BTI in 2017, which added a significant amount of goodwill to the balance sheet. Excluding goodwill, BTI's cash return on invested capital has averaged 8.4% over the last three years. That's better, but still pretty poor for a tobacco company. Moreover, it is debatable as to whether goodwill should be excluded when calculating CROIC.

In connection with the adjustment of invested capital for goodwill, it should be noted that PMI also has a considerable amount of goodwill on its balance sheet ($19.7 billion at the end of 2022, which corresponds to almost a three-fold increase compared to 2021 year-end), which is largely attributable to the acquisition of Swedish Match. As a result, PMI's CROIC was only 21% in 2022, compared to 36% in 2021. Obviously, the sharp decline in 2022 is also the main reason for the high standard deviation. The decline is worrying at first sight, but it should be kept in mind that the cash flow contribution of Swedish Match (at least $500 million with strong growth) is only partially reflected in PMI's 2022 cash flow statement due to the timing of the acquisition. Going forward, it is therefore (and also due to the still largely untapped synergy potential) only reasonable to expect PMI's CROIC to recover, although it will probably take some time before it reaches the 30% mark.

Taken together, all three companies are - as expected - solidly profitable, but I consider BTI to be the weakest due to its poor CROIC (even on a goodwill-adjusted basis). However, from a cash profitability perspective, I would not overstate Altria's top position, as higher capex spending will likely be required in the future to (finally) gain traction in the heated tobacco and vaping space. Given BTI's strong position in e-vaping, PMI's upcoming launch of the leading IQOS franchise in the U.S., and of course the dominance of Zyn nicotine pouches, there is a risk of potential malinvestments at Altria (acquisition and capex-wise), in an effort to play catch-up and thereby potentially sacrificing some of its still very solid profitability.

A Look At The Balance Sheet Quality Of Altria, British American Tobacco, And Philip Morris International

It's common knowledge how Altria Group blemished its balance sheet with the costly acquisition of its minority stake in Juul Labs. The company's equity ratio turned negative in 2021 and showed a shareholders' deficit of $3.4 billion at the end of the third quarter of 2023. However - and I don't want to be misunderstood as excusing the missteps of Altria's management - I don't think this development is worrying. In another article , I explained why I don't give much weight to a negative book value (assuming operating fundamentals are strong) and why I prefer to look at net debt relative to free cash flow and interest coverage instead.

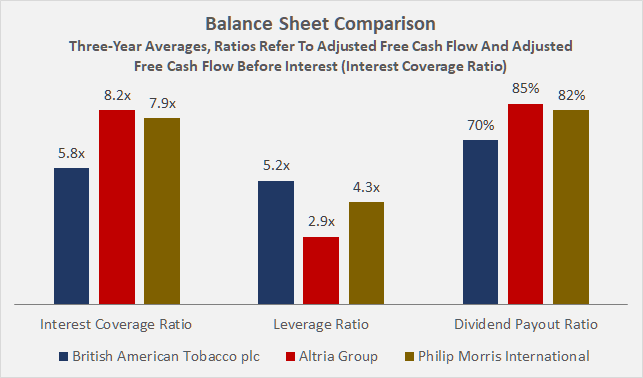

Altria's net debt has remained relatively stable since the transaction and currently stands at $23.5 billion. As Figure 4 shows, its leverage ratio remains well under control at three times adjusted free cash flow and an interest coverage ratio of more than eight times free cash flow before interest. It is also worth noting that Altria has a significant "hidden" asset on its balance sheet - its stake in Anheuser-Busch InBev SA/NV ( BUD ). Altria owns 185 million restricted shares and 12 million common shares, which had a total market value of $11.9 billion at the end of 2022 (carrying value $9.0 billion). The value of the stake peaked at almost $13.2 billion at the end of March 2023, then fell to $10.2 billion - mainly due to the Bud Light controversy - but consequently recovered to $12.4 billion currently. By selling its stake at a price that is still below what I personally believe is fair value for BUD stock, Altria could reduce its leverage to 1.4 times adjusted free cash flow. That's pretty impressive, but if management decides to move forward with the transaction, I expect a combination of debt reduction and share buybacks (Altria stock is currently a very good deal with an 11% free cash flow yield).

{kind=link}

Figure 4: Assessment of the balance sheet quality of Altria Group, Philip Morris International, and British American Tobacco plc (own work, based on company filings)

Speaking of "hidden" assets, I think it's worth highlighting British American's 29% stake in ITC Ltd. (a major Indian consumer goods, packaging, software, and until recently also hotels conglomerate). Fundamentally, BTI's leverage looks quite concerning, at more than five times adjusted free cash flow. However, considering that the stake in ITC was worth more than £12 billion at the end of 2022 (£1.9 billion book value) and has since increased to almost £16 billion, I don't think the leverage is overly concerning. Although I highly doubt that management has any intention of selling this prime asset, the transaction could theoretically reduce leverage to three times adjusted free cash flow.

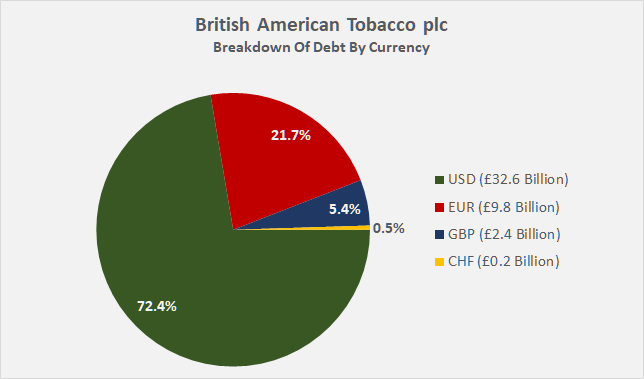

That being said - and I believe this is one reason for the stock's poor performance - investors should also be mindful of BTI's sizable U.S. dollar-denominated debt (Figure 5). If a menthol ban goes into effect and the company experiences significant sales declines due to increased smoking cessation and switching to other non-menthol brands (potentially from competitors), a material portion of its dollar-denominated cash flow would be jeopardized, which in turn would hurt its ability to pay down debt and weaken its interest coverage ratio. In addition, a menthol ban would likely result in a significant impairment of goodwill and likely a write-down of intangible brand assets. For example, if BTI were to write off all of its goodwill from the acquisition of Reynolds American (approximately £48 billion), its equity ratio would fall from 49% to 18%.

Nevertheless, I think Big Tobacco will be able to manage the looming menthol ban in the U.S. (several countries in the E.U. serve as good examples). However, while BTI is positioned quite well through its broadly diversified brand portfolio, it suffers from a concentration risk in Newport cigarettes ( market leader in U.S. menthol) , and I believe that Altria is better positioned from the perspective of smokers switching to non-menthol alternatives, as Marlboro cigarettes are known to be available with and without menthol flavor.

{kind=link}

Figure 5: British American Tobacco plc (BTI, BTAFF): Breakdown of debt by currency (own work, based on data from the company’s website)

Finally, PMI's debt looks much more serious than a few years ago, which is of course related to the recent heavy investments in smoke-free products (acquisition of Swedish Match and IQOS marketing rights consideration paid to Altria):

{kind=link}

Figure 6: Philip Morris International Inc. (PM): Net debt since 2019 (own work, based on company filings)

Including Swedish Match's contribution of $500m in free cash flow, PMI's leverage ratio at the end of the third quarter of 2023 was 4.3 times adjusted free cash flow. I estimate its current interest coverage ratio to be slightly less than eight times free cash flow before interest, based on the current outstanding bonds, their interest rates, and an assumed 3.5% interest PMI receives on its $3.0 billion in cash and cash equivalents.

For the amount of debt the company took on last year, this is actually quite solid, and I think PMI is very well positioned to pay down debt. Granted, the dividend payout ratio is currently 80% of free cash flow, but management has stated that it will de facto suspend share repurchases and only slowly increase the dividend until the debt is back in check. I think this is a very sensible approach, even though the company could manage its current debt load even if interest rates indeed stay "higher for longer". In the context of free cash flow growth and hence improved ability to pay down debt, investors should note PMI's strong growth prospects and also the highly favorable economics of heated tobacco sticks and oral nicotine pouches.

The focus on reducing debt after such a significant acquisition is also wise from a credit rating perspective. The company currently has a long-term credit rating of A2 from Moody's with a stable outlook. The rating was only recently affirmed , and although the agency highlighted PMI's business prospects quite positively, it does not expect the company to return to a " Moody's-adjusted gross leverage [of] 2.5x " before the end of 2025 - a year longer than previously expected.

In comparison, Altria's long-term credit rating is A3 (stable outlook), largely due to regulatory fat-tail risk. British American ranks the weakest ( Baa2 ), but Moody's has recently upgraded the rating outlook to positive , largely due to solid developments in the smoke-free segment ( faster than expected profitability ) and the current strong earnings performance (partly due to favorable currency effects, of course).

Taken together, I think each of the three companies has a stable balance sheet and I find it difficult to identify an obvious laggard in this context. British American benefits from its more or less well-known stake in ITC, which makes its leverage far less severe than the pure debt figure suggests. However, the rather high percentage of U.S. dollar denominated debt (more than 70% of total debt) despite only modest U.S. sales (45% of 2022 net sales) is a risk to keep an eye on. Altria has the lowest leverage ratio in the group - which would even fall significantly if the proceeds from a hypothetical sale of the BUD stake were used entirely to pay down debt - but it is worth keeping an eye on the suspected underinvestment and comparatively weak portfolio outlook, which could lead to significant future investments and thus a weakening of the leverage ratio. The increase in Philip Morris' leverage is understandable, and I think it's safe to assume that the undisputed market leader in smoke-free products will be able to gradually return to a normal (2 to 2.5 times free cash flow) leverage ratio.

Conclusion

In this article, I took a somewhat critical stance when considering an investment in Big Tobacco.

Reframing the question from "What to buy?" to "What to sell?", several specifics were discussed that identified Altria Group a clear laggard from a portfolio perspective. Apart from the company's failure to gain a foothold in smoke-free products, its focus on selling Marlboro cigarettes (almost 90% of cigarette volume) is a concentration risk worth considering, even if the company continues to gain market share in the premium segment.

From a profitability perspective, BTI is the worst performer due to its poor CROIC (even after adjusting for goodwill) and its free cash flow margin below 30%. The latter is somewhat surprising given the company's exposure to the highly profitable U.S. market (45% of net sales in 2022), but is in fact an indication of brand diversification and higher exposure to lower-priced cigarettes - not a bad position in a high inflation environment.

However, I would not overstate Altria's leading profitability, as higher capex spending will likely be required in the future to (finally) gain traction in the heated tobacco and vaping space. Given BTI's strong position in e-vaping, PMI's upcoming launch of the leading IQOS (ILUMA) franchise in the U.S., and of course the dominance of Zyn nicotine pouches, there is a risk of potential malinvestments at Altria (acquisition and capex-wise), in an effort to play catch-up and thereby potentially sacrificing some of its still very solid profitability.

From a balance sheet perspective, I find it difficult to identify an obvious laggard. British American benefits from its more or less well-known stake in ITC, which makes its leverage far less severe than the pure debt figure suggests. However, the discrepancy between U.S. dollar-denominated debt and sales is a risk to keep an eye on. Altria has the lowest leverage of the three companies, and a sale of the BUD stake and subsequent debt repayment would further derisk the balance sheet. However, the suspected underinvestment and comparatively weak portfolio outlook could lead to significant future investments and thus a weakening of the leverage ratio a decline in free cash flow profitability.

For these reasons, I consider Altria to be the weakest of the three companies discussed in this article. However - and I think I've made it clear that it would be Altria stock if I had to pick one to sell - I want to emphasize that I don't think the French bulldog next to the two larger dogs in the headline image is a fair representation of Altria compared to British American Tobacco and Philip Morris International Inc. Altria still has a lot going for it, such as its strong brand power through Marlboro, solid balance sheet, leading profitability, and shareholder-friendly management. Therefore, I will definitely stick to my position.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

British American, Altria And Philip Morris - Which One Stands Out As The Weakest?