BTAFF - British American Tobacco And Imperial Brands: The Sunak Black Swan?

2023-09-28 09:10:31 ET

Summary

- Shares of British American Tobacco and Imperial Brands fell after British Prime Minister Rishi Sunak hinted at introducing anti-smoking measures similar to those in New Zealand.

- Investors are concerned that stricter regulations could lead to an even faster decline in cigarette volumes, limiting the companies' leeway for price increases.

- The article estimates the impact of a loss of the UK market - an arguably pessimistic expectation - on both companies' sales, free cash flow and, consequently, dividend safety.

Introduction

On Monday, September 25, 2023, shares of international tobacco companies Imperial Brands PLC ( IMBBY , IMBBF ) and British American Tobacco p.l.c. ( BTI , BTAFF ) were hit particularly hard (-6.8% and -3.9%, respectively), while Philip Morris International Inc. ( PM ) was down comparatively little (-1.7%).

What was it this time, and why the disproportionate decline in Imperial Brands and British American shares?

It was due to British Prime Minister Rishi Sunak, who shook investors with his announcement that he was considering introducing similarly draconian anti-smoking measures to those recently passed by the New Zealand parliament. While the country is restricting nicotine content and plans to reduce the number of retailers allowed to sell tobacco products by 90% to just 600 by the end of 2023, it was the age-based ban that caught Sunak's interest. New Zealand was the first country to introduce an annually increasing smoking age and ban the sale of cigarettes to anyone born on or after January 1, 2009.

Investors in tobacco companies with an exposure to the UK are likely to fear that cigarette sales in this market may soon decline even faster than previously thought. At some point, tobacco companies may no longer be able to offset this accelerated volume decline by raising prices.

In this article, therefore, I will take a closer look at the impact of such legislation on the revenues, earnings and cash flows of the two UK-based tobacco companies, British American Tobacco and Imperial Brands.

As an aside, I ask you to weigh ethical arguments on a personal basis before investing in the tobacco sector. Just because I have written this article does not mean that I am a proponent or advocate of smoking, let alone that I discourage action against smoking. The sole purpose of this article is to address the potential impact of potential legislation such as that described above.

How The New Zealand Blueprint Could Impact British American Tobacco And Imperial Brands

Before we begin, I would like to emphasize that in making this assessment I am assuming the worst-case scenario and thus risk being seen as too conservative.

I assume that draconian anti-smoking laws will be enacted in the UK, resulting in a complete loss of this market. This is certainly not very likely, given that at least some of the lost supply will be replaced by black market cigarettes, from which the internationally diversified cigarette manufacturers benefit anyway. Indeed, the New Zealand government has acknowledged that the amount of tobacco smuggled into the country has increased significantly over the years. So why should it be any different in the UK? Nevertheless, I will make an estimate of the impact on IMBBY's and BTI's revenues and earnings, assuming that UK sales fall to zero.

The most likely outcome, in my view, is a slightly faster decline in the number of smokers than at present, but I would not over-interpret the impact of such a law. I've already pointed out the likely impact of black market cigarettes, and it's also worth remembering that the first people to be covered by this law in New Zealand only turned 14 this year, so they're still four years away from the legal age of 18 (the same is true in the UK). This means that the new laws in New Zealand do not prohibit anyone from buying cigarettes who is already allowed to (or will be allowed to in the near future).

The Potential Impact On Imperial Brands

In terms of net revenue, Imperial is the smallest of the Big Tobacco companies, with net revenues of £7.8 billion in 2022. By comparison, BAT generated £27.7 billion in 2022 net of excise and other duties. Imperial has three segments in which it reports the performance of its tobacco business, Europe, the Americas, and Africa, Asia and Australasia.

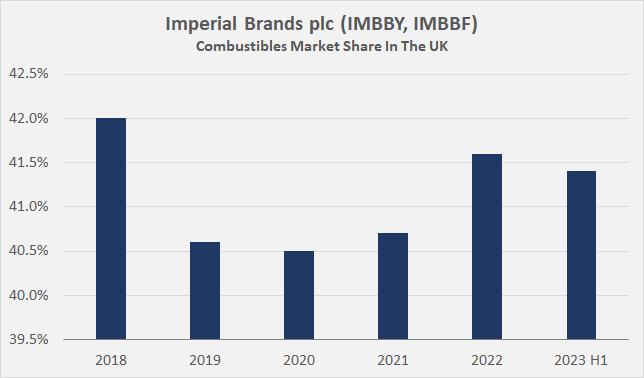

Imperial Brands has a solid presence in the United Kingdom with a market share of 41.6% in 2022 (p. 67, 2022 annual report ):

Figure 1: Imperial Brands plc (IMBBY, IMBBF): Combustibles market share in the UK (own work, based on company filings)

{kind=link}

A market share of over 40% sounds great, but of course not in the context of discussion of potentially draconian anti-smoking measures. The UK is part of Imperial's Europe segment, which was responsible for 45% of consolidated net revenues in 2022. The remaining 55% of revenue is split approximately 65/35 between the Americas segment and the Africa, Asia and Australasia segment.

As Imperial identifies the UK as one of its "priority markets," it reports the segment's relative revenue contribution, which has ranged from 7% to 9% of group net revenue over the last three years, or 8% on average. This means that Imperial is likely to generate net revenues of around £600 million from the sales of combustibles in the UK each year, which puts the implied significance of Imperial's high market share into some perspective.

The company is surprisingly profitable overall despite its comparatively small size. Imperial's free cash flow margin, normalized in terms of working capital movements and adjusted for stock-based compensation and dividends paid to non-controlling interests, is around 29% when looking at the 2019 to 2022 period. The company's average adjusted operating margin for the same period was 46%, or 34% when based on UK - adopted IFRS operating earnings. Assuming that the group-wide margin can be applied 1:1 to the UK business, Imperial thus has free cash flow of around $180 million each year, or operating profit of between £230 million (IFRS) and £290 million (adjusted) theoretically at risk.

Of course, investors in tobacco stocks are mainly in it for the dividend. Imperial Brands' stock currently has a yield of about 8.6%, relatively on par with other stocks (with the obvious exception of PM, the undisputed leader in smoke-free products). Imperial had to cut its dividend in 2020, largely due to an unsustainable dividend policy in earlier years and a fairly leveraged balance sheet. However, the situation has improved over the years and the company is currently conducting a £1 billion share buyback program. In 2022, Imperial paid dividends of £1.3 billion, which compares quite favorably to its three-year average free cash flow (adjustments as above) of £2.3 billion. The payout ratio is about 50% to 60%, and if we assume Imperial loses all of its UK business tomorrow (which is an unrealistically negative expectation), the payout ratio rises by five percentage points, to 55% to 65% of free cash flow.

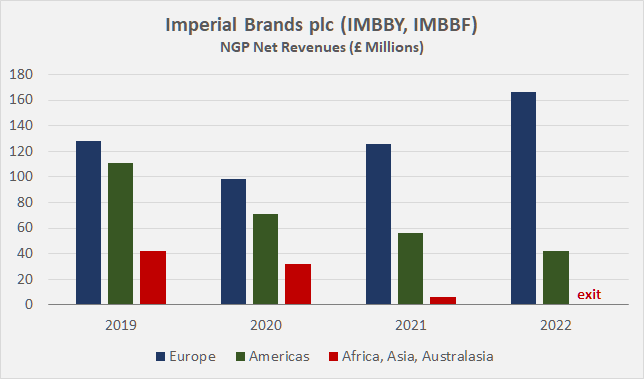

Now, it could be argued that the move to smoke-free alternatives will offset the potential loss of revenue due to anti-cigarettes regulations. However, Imperial Brands is the obvious laggard within its peer group in this regard. It is no exaggeration that there is not much reason to talk about Imperial's efforts in oral tobacco, vaping products, or heated tobacco products, which the company refers to as next generation products ((NGP)). Imperial's strategy in this segment has been very poor, and the company has failed to gain a foothold in any of the three categories. Philip Morris (see my articles on the company, e.g., here and here ) and British American (see my article on Kenneth Dart's involvement ) are the clear leaders, as is also evident when looking at Imperial's NGP sales (Figure 2). The company even decided to discontinue its NGP efforts in the Africa, Asia and Australasia segment last year (largely Russia and Japan). NGP net revenues in 2022 represented only 2.7% of total net revenues (£208 million, p. 8 f., 2022 full-year press release ) - dwarfed by BTI's 14.8% (£4.1 billion, p. 3, 2022 full-year press release ).

Figure 2: Imperial Brands plc (IMBBY, IMBBF): Next generation products - NGP - revenue in each segment (own work, based on company filings)

{kind=link}

The Potential Impact On British American Tobacco

In contrast to Imperial Brands, British American does not report country-specific revenue contribution, so a different, arguably approximate approach is required.

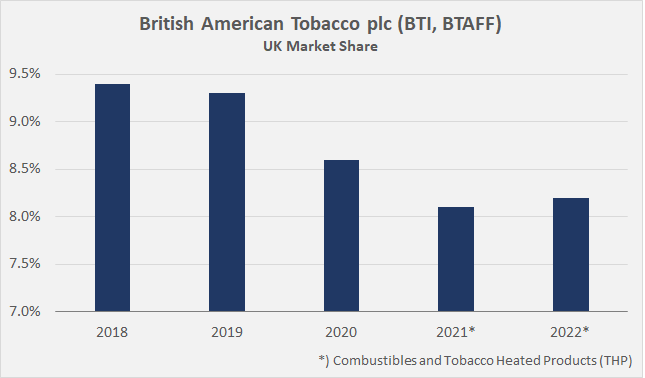

In its earnings presentations (e.g., slide 58 f., 2022 presentation ), the company provides country-specific market shares. Figure 3 shows BAT's market share in the UK combustibles market. The 2021 and 2022 figures include tobacco heated products ((THP)), however, knowing that British American lags well behind Philip Morris in heated tobacco, I do not consider the contribution significant.

Figure 3: British American Tobacco plc (BTI, BTAFF): Combustibles market share in the UK, 2021 and 2022 include THP (own work, based on company filings)

{kind=link}

Knowing Imperial's market share in the UK, we can derive the size of the market to be around £1.5 billion in terms of net revenue. Of course, this is only an approximation, as we do not know whether Imperial reports its market share based on net or gross revenues, or perhaps even volume.

Considering that British American currently claims only about 8% of the UK market, this would imply net revenues of £110 million to £130 million. This estimate may seem too low, but consider the small market share and the fact that Europe (including Russia and Ukraine) contributes only about 22% (£5.0 billion) of BAT's total 2022 net combustibles revenues. In other European countries, BAT has a significantly larger market share than in the UK - e.g., France 15%, Germany 21%, Italy 18%, Poland 25%, Romania 50%, Russia 24%, Switzerland 33%, and Ukraine 27%.

As a result, British American's net revenues, and hence free cash flow, are unlikely to be materially affected even if smoking is banned in the UK. The three-year average of BAT's normalized free cash flow margin is 27%, which translates to a theoretical loss in annual free cash flow of £30 million to £40 million - hardly significant considering that BAT's annual free cash flow is around £8 billion. Consequently, the company's dividend payout ratio is also not materially impacted and is expected to remain in the mid-60% range (average 2020 to 2022).

Conclusion

Tobacco stock investors were startled by British Prime Minister Rishi Sunak's recent statement about plans to push for stricter anti-smoking laws similar to those recently enacted in New Zealand. Given the company's leadership in smoke-free products, it is only logical that PM stock was not really affected by this news. However, I believe the market overreacted by punishing IMBBY and BTI by almost 7% and 4%, respectively.

Imperial's market share in the UK is very high, but given the small size of the market overall, and even given Imperial's mostly unsuccessful efforts in smoke-free products, I don't think the looming regulation in the UK will have a material impact on the company's free cash flow and dividend safety. British American's presence in the UK is small, so the company's revenues and free cash flow are unlikely to be affected even if the market is lost entirely - which is an obviously unrealistically pessimistic expectation.

In my view, investors increasingly fear that New Zealand could actually serve as a blueprint for other countries, and a more or less worldwide introduction of such a draconian policy would certainly have a significant impact on the earnings and cash flows of tobacco companies. However, this is not really news, considering that the news from New Zealand emerged back in 2021 . Importantly, I believe that such measures would take a very long time to implement, so the impact on company valuations should still be quite insignificant given the time value of money and the very strong near-term free cash flows of tobacco companies. At the same time, a thriving black market and lost tax revenues should not be ignored when weighing the likelihood and severity of such measures. Finally, these laws are directed against the consumption of conventional cigarettes, so the companies that have strong smoke-free franchises should be fairly well insulated - Philip Morris being, of course, the best (but also most expensive) of the breed.

I remain very confident about my investment in BTI shares and will also maintain my small position in Imperial Brands. However, since the latter company definitely has the worst prospects from the perspective of cigarette alternatives, I will not increase my position. I would increase my BTAFF position (I own the original shares bought on the London Stock Exchange) if it were not already of an appropriate size for my risk appetite (3% of my portfolio).

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

British American Tobacco And Imperial Brands: The Sunak Black Swan?