IMBBY - British American Tobacco: Combustible Volumes Fell Double-Digits In U.S. And Europe

Summary

- British American Tobacco p.l.c.'s 2022 results this morning disappointed investors, with shares down 3% in London as of 2 pm local time.

- Adjusted EPS grew by 5.8% in 2022 and New Categories revenues grew by double-digits, but the Combustibles business was weak.

- Combustibles volumes fell double-digits in both the U.S. and Europe. Buybacks are paused while debt is paid down to a new target.

- The company's progress in New Categories continued to be mixed, but an 8x P/E and a 7.7% Dividend Yield provide a margin of safety.

- With shares at 2,999p, we expect a total return of 74% (24.3%annualized) by 2025 year-end. Buy.

Introduction

British American Tobacco PLC ( BTI ) (referred here as "BAT") released its full-year 2022 results this morning (February 9). Even though key headlines were already released in December in a "pre-close update," the full results were disappointing to investors, and the BAT share price is down 3% at 2,999p as of 2 pm local time.

BAT’s share price has been weak in the past year, with its U.K.-listed shares down 7.9% (in pounds) and its American Deposit Receipts (“ADR”) down 15.5% (in dollars), though dividends have offset part of these losses:

| BAT Share Price Performance (Last 1 Year) Source: Google Finance (09-Feb-23). |

Compared to the level at which we originally upgraded our rating to Buy in March 2020, BAT shares have gained 41% (including dividends) in pounds in just under 3 years, including 26% since the end of 2020.

2022 results were mixed. Adjusted EPS grew by 5.8% in 2022 and is guided to grow by mid-single-digits in 2023 (all figures in local currencies). New Categories saw revenues grew by strong double-digits in each category losses narrowing by 61%. However, Combustibles volume fell by double-digits in both the U.S. and Europe; outside New Categories, operating profit fell 0.8% year-on-year. Within New Categories, BAT is leading in Vapour and European Modern Oral, but has lost the U.S. Modern Oral market and made limited progress in Tobacco Heated Products. BAT has decided against announcing new buybacks in 2023 to pay down debt. Headwinds against the Combustibles business, and the market’s move to Reduced Risk Products, may both be turning stronger. On balance, we believe BAT is well-placed, and its low valuation (8.1x P/E, 7.7% Dividend Yield) provides a margin of safety. Our forecasts indicate a total return of 74% (24.3% annualized) by 2025 year-end. Buy.

British American Tobacco Buy Case Recap

BAT is a global tobacco company, but relies on the U.S. market for half of its segmental Profit from Operations ("PfO", equivalent to EBIT) and most of its PfO growth; non-U.S. PfO was roughly flat in 2017-19 and fell in 2020 and 2021:

| BAT Profit from Operations by Region (201 5 -202 2 ) Source: BAT company filings. Key: EEMEA = Eastern Europe, Middle East & Africa; ENA = Europe & North Africa; AMSSA = Americas & Sub-Saharan Africa; APME = Asia-Pacific & Middle East. NB. Figures include the impact of currency movements. ENA has been renamed Europe in 2022 with North Africa moved to the APME region. |

Our investment case on BAT is based on the following:

- A broadly stable U.S. cigarette market, where Vapour is the main threat but growing only moderately (led by BAT)

- Mostly stable non-U.S. cigarette markets, with Heated Tobacco having an only limited impact on BAT earnings

- A mid-single-digit ex-currency EPS CAGR over time, thanks to broadly stable cigarette revenues, expanding margins and buybacks, but limited by BAT’s poor performance in New Categories in most markets

- A long-term P/E multiple of 10x, implying a Dividend Yield of 6.5%

COVID-19 was an overall positive for BAT, as the boost to tobacco consumption in Developed Markets (approx. 75% of BAT revenues) more than offset the hit to that in Emerging Markets (approx. 25%). Excluding currency, BAT Adjusted EPS growth was in a narrow range of 5.5%, 6.6% and 5.8% respectively in 2020-22:

| BAT Adjusted EPS & EPS Growth (2017-22) Source: BAT company filings. |

2022 results were mixed, with solid headline results but potentially showing stronger headwinds against its Combustibles business and the market moving faster to Reduced Risk Products than we anticipated.

BAT 2022 Results Headlines

In 2022, BAT Adjusted EPS grew by 5.8% year-on-year excluding currency, and by 12.9% in U.K. pounds:

| BAT Profit & Loss (202 2 vs. Prior Year) Source: BAT results release (2022). |

Excluding currency, total Net Revenues grew 2.3% year-on-year; PfO grew 4.3% year-on-year, faster than revenues, as PfO margin expanded 150 bps.

Including currency, Adjusted Net Income grew 11.7%, roughly in line with PfO, with Net Finance Costs up 12.3%; Adjusted EPS grew 12.9%, faster than Net Income, after buybacks reduced the average share count by 1.3%.

By region, excluding currency, each of BAT’s four regions contributed to PfO growth, though Net Revenues fell 2.8% in the U.S. after a strong 9.2% growth in the prior year:

| BAT R evenues & PfO By Region (202 2 vs. Prior Year) Source: BAT results release (2022). NB. North Africa moved from Europe to APME region in 2022 but impact was “immaterial.” |

We look at BAT’s revenues and volume in more detail.

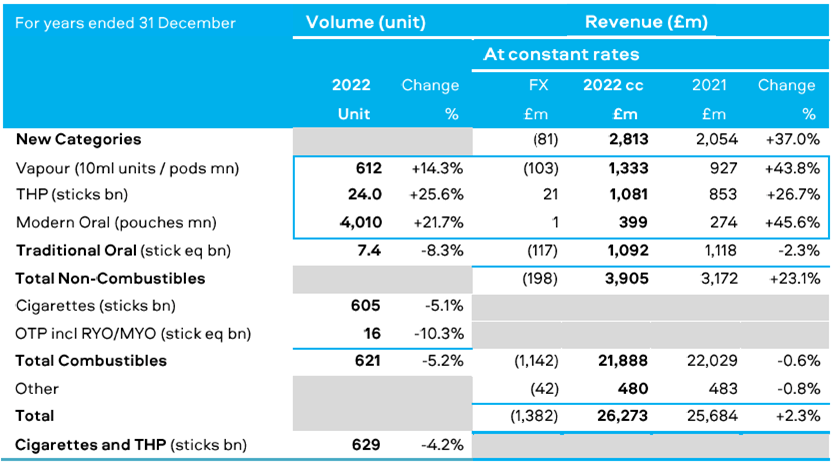

Strong Double-Digit New Categories Growth

Within BAT revenues, excluding currency, Combustibles declined by 0.6% (on a volume decline of 5.2%), while each of the three New Categories grew by strong double-digits:

{kind=link}

Vapour and Modern Oral revenues grew much more than volumes, while Tobacco Heated Products (“THP”) revenues grew roughly in line with volume.

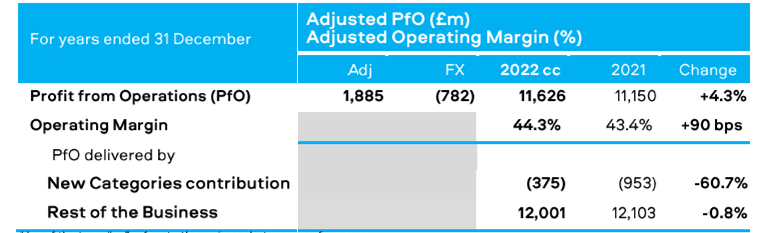

Earnings Driven by Lower New Categories Losses

BAT’s 4.3% constant-currency PfO growth in 2022 was driven by New Categories losses shrinking 61% year-on-year (from £953m to £375m); outside New Categories, PfO actually fell 0.8% year-on-year in local currencies:

| BAT P rofit from Operations – New Categories vs. Rest of Business (2022) Source: BAT results release (2022). |

{kind=link}

BAT’s Combustibles business saw double-digit volume declines in both the U.S. and Europe, its two largest regions which together contributed more than 70% of its PfO in 2022.

Double-Digit Combustible Volume Declines

BAT’s Combustible volumes fell by 15.5% year-on-year in the U.S and by 10.0% in Europe:

{kind=link}

Management attributed BAT’s U.S. volume decline mainly to macroeconomic headwinds, with BAT doing worse than the industry because of company-specific inventory movements. As CFO Tadeu Marroco said on the earnings call :

“Combustible industry volume was down around 10% mainly reflecting post COVID normalisation of consumption patterns and macro-economic deterioration through the year. Our volume was down 15.5% additionally reflecting the partial unwind of our prior year inventory movements, volume share loss, and lower retail inventory levels across the industry at year end.”

This is consistent with what we have observed from Altria’s ( MO ) Q4 2022 results . Altria’s Smokeable volume fell 9.7% year-on-year in 2022 (9.5% if adjusted for inventory) and 12.1% in Q4 (11% adjusted), even as industry Vapour volumes stagnated after Q1. BAT’s 2.8% local-currency revenue decline was similar to Altria’s 1.7%. THPs are currently not available in the U.S., and Modern Oral is a small category.

The picture in Europe was more worrying. We believe most of the 10.0% Combustible volume decline was real, with management highlighting volume declines in key markets including Turkey, Germany and France, though an undisclosed part of the decline was due to North Africa volumes having been moved to the APME region this year. BAT’s Combustible revenues also grew by only 1.2% (excluding currency) in 2022.

BAT’s cigarette volume decline in Europe was also worse than Philip Morris ( PM ), whose Q4 2022 results imply a cigarette volume decline of just 4.6% in Europe (consisting of declines of 2.5% in the European Union and 8.2% in Eastern Europe, the latter including Russia & Ukraine):

| Philip Morris Cigarette Volumes by Region (2022) Source: PM results release (Q4 2022). |

Poor macroeconomics alone are unlikely to explain the weak performance of BAT’s Combustible business in Europe.

We see Europe as a bellwether region, because its demographics and tobacco taxes are both more mature than the U.S., and it a region with where BAT and Philip Morris are both actively pushing THP and Vapour products. On that basis, BAT’s weak European Combustible volumes is negative for its stock, as well as for Imperial Brands ( IMBBY ).

BAT’s Mixed Progress in New Categories

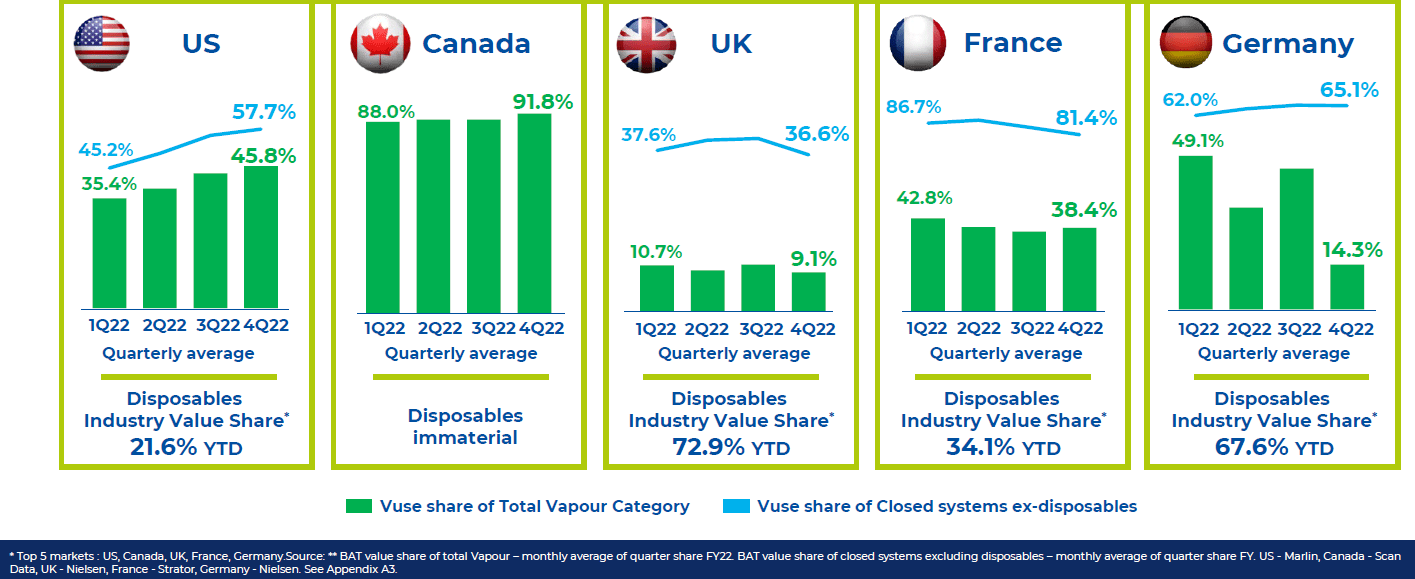

Within New Categories, BAT is leading in Vapour and European Modern Oral, but has lost the U.S. Modern Oral market and there is little progress in Tobacco Heated Products.

In Vapour, BAT is now #1 in the U.S. with a 45.8% value share (including disposables) as of Q4, and it has a similarly strong 38.4% Vapour value share in France. However, its value share has been falling in in France, as well as in the U.K. (where its market share had always been smaller) and Germany (where the market is much smaller):

{kind=link}

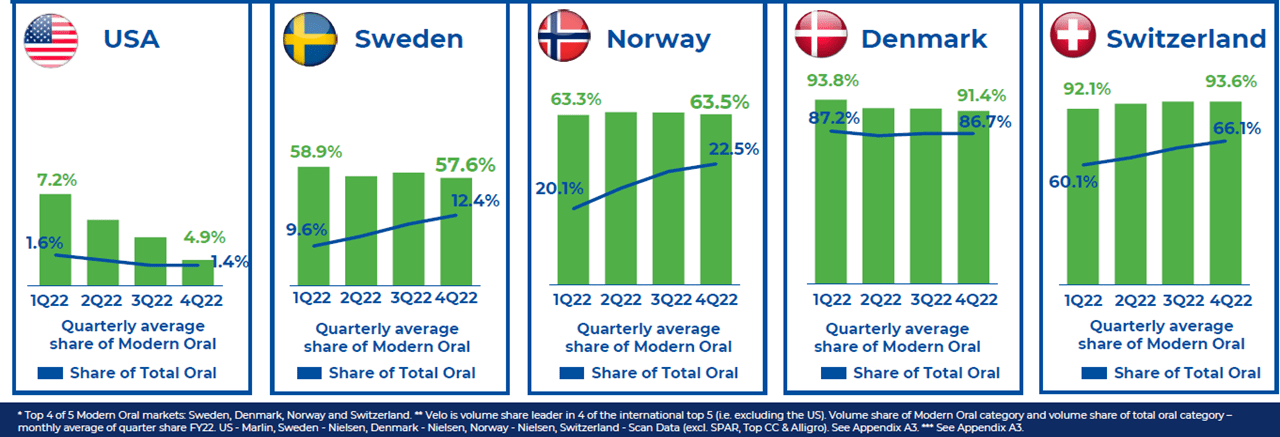

In Modern Oral (nicotine pouches), BAT’s Velo continues to dominate the fast-growing category key Europe markets, but has seen its category share collapse from 7.2% to 4.9% in the U.S.:

{kind=link}

BAT has applied for PMTA marketing approval to bring some international Velo products to the U.S., but this will take time and we do not believe it will make a difference to the dominance of the number one player there, Swedish Match’s ( SWMAY ), now part of Philip Morris.

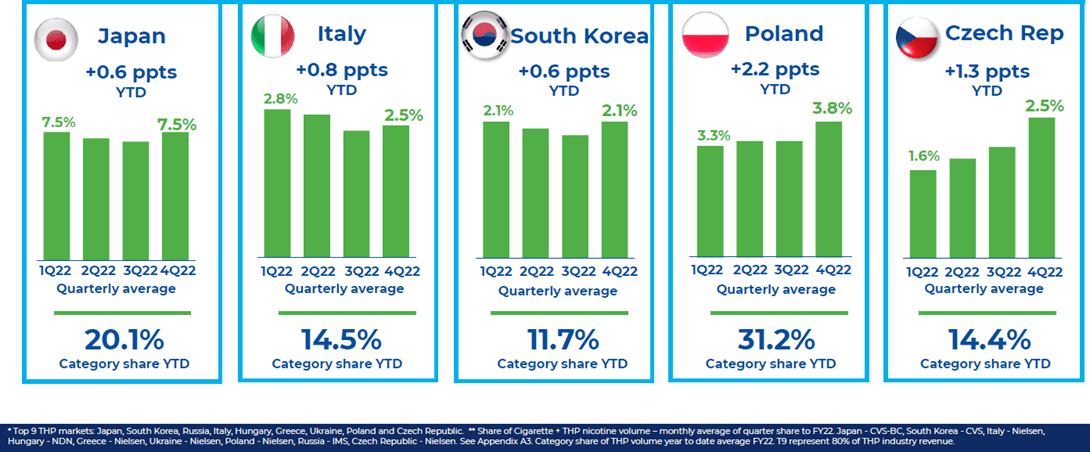

BAT’s glo has made little progress in THP. Its share of the tobacco market is flat in Japan and down in Italy between Q1 and Q4 of 2022, which imply declines in category shares because THP is gaining share within tobacco:

{kind=link}

Glo’s category share appears to have grown in Poland (from 25.2% in Q4 2021), but this is just one country and Romania is no longer shown (unlike last year), so BAT may be showing only countries where it is growing.

In any event, glo’s category share year-to-date is 20% or below in four out of the five countries shown, likely implying that Philip Morris’s IQOS has continued to dominate the category.

No New Share Buybacks in 2023

BAT has decided against announcing new buybacks in 2023 to pay down debt. CFO Tadeu Marroco said on the call:

“Given our incremental investment plans in 2023 to further accelerate our transformation and in light of the uncertain macro environment, higher interest rates, outstanding litigation, and regulatory matters, the Board has decided to prioritise strengthening the balance sheet. … We aim to reduce leverage more quickly towards the middle of our target 2-3x corridor.”

Marroco stated at the same time that management “strongly believe” that buybacks “have an important role” and promised to keep them under review as BAT moves through 2023.

BAT’s Net Debt / EBITDA was at 2.89x at 2022 year-end, with Net Debt actually growing by 8.2% (£3.0bn) in 2022, primarily due to foreign exchange impact of £3.0bn. 18% of BAT’s debt is exposed to floating interest rates and management expects Net Finance Cost to increase in future years (for example from £1.6bn to £1.9bn in 2023).

We expect BAT to reach its new Net Debt / EBITDA target towards the end of 2023. Adjusted Net Debt was £38.1bn and 2022 EBITDA was £13.2bn. Assuming a 5% EBITDA growth, a 2.5x ratio would allow £34.7bn of Net Debt by 2023 year-end, requiring £3.4bn of debt repayments. This could take the whole of 2023, with Free Cash Flow at £8bn in 2022 and the new dividend costing just over £5bn.

Valuation: BAT Dividend Yield is 6.2%

With shares at 2,999.0p in London as of 2 pm local time, BAT shares are at an 8.1x P/E and an 11.8% FCF Yield:

| BAT Net Income, Cashflow & Valuation (2019-22) Source: BAT company filings. |

With guidance implying a 12% growth in Adjusted EPS in pounds, shares are at around 9x 2022 Adjusted EPS.

The dividend has been raised 6% (in line with ex-currency Adjusted EPS growth) to 230.9p, which implies a Dividend Yield of 7.7%. BAT still targets a 65% Payout Ratio, but now on a “medium to long term” basis, though its dividend policy is also “progressive” (i.e., growing the dividend every year).

British American Tobacco Stock Forecast

We update the assumptions in our forecasts to remove buybacks from 2023:

- Net Income growth of 3.0% annually (unchanged)

- No share buybacks in 2023 (was 2.5%)

- Share count to fall by 3% annually from 2024 (was 2.5%)

- Dividends to grow with EPS on a Payout Ratio of 65% (unchanged)

- 2025 P/E at 10x P/E (unchanged).

Our new 2025 EPS forecast is 431.3p, 1% higher than before (427.0p):

| Illustrative BAT Return Forecasts Source: Librarian Capital estimates. |

With shares at 2,999p, we expect a total return of 74% (24.3% annualized) by 2025 year-end, in just under 3 years. Earnings growth, dividends and an upward re-rating contribute roughly one third each to the forecasted return.

Is British American Tobacco A Buy? Conclusion

We reiterate our Buy rating on British American Tobacco p.l.c., but will monitor the business closely.

For further details see:

British American Tobacco: Combustible Volumes Fell Double-Digits In U.S. And Europe