PM - British American Tobacco: Mind The Vulture

2023-04-27 09:24:35 ET

Summary

- The article offers a deep dive into British American Tobacco's 2022 results, which were pretty good - but only on the surface.

- I'll focus on earnings and cash flow, take a look at how BTI's smoke-free portfolio has performed, and whether the growing debt on the company's balance sheet is still manageable.

- I also delve into the sizable 9% stake held by secretive billionaire Kenneth Dart, best known for his aggressive vulture fund.

- While Kenneth Dart's sizable wager likely fuels confirmation bias among many minority shareholders, I also point out an extreme tail risk associated with this holding.

Introduction

My regular readers know my bullish stance on big tobacco companies in general and British American Tobacco ( BTI , OTCPK:BTAFF ) in particular. While the stock performed quite well during the bear market in 2022, 2023 has not been pretty for shareholders so far. The S&P 500 ( SPY ) has performed rather well, up more than 8% year-to-date, while the British tobacco giant's stock is down nearly 9% on the year.

In my last article from early February 2023, published just prior to the release of the annual results, I shared my earnings expectations, focusing on BTI's combustibles volume and its smoke-free portfolio. In this update, I'll review the company's full-year 2022 earnings and cash flow in detail, take a look at how BTI's smoke-free portfolio has performed, and whether the growing debt on the company's balance sheet is still sustainable. I will also discuss the sizable stake held by Kenneth Dart, the mysterious Cayman Islands based billionaire investor. While I don't think it's necessarily a good idea to engage in "whale watching" or to follow such individuals blindly into their holdings, I do think it's important to consider the possible motives of a major shareholder. After all, large shareholders do not necessarily act for the mutual benefit of minority shareholders, as the example of Dell Technologies Inc. ( DELL ) shows (see my recent coverage here and here ).

BTI 2022 Results Review

How Did BTI Perform In Terms Of Earnings And Free Cash Flow?

The company reported its annual results on February 9, 2023 - on that day, BTI shares plunged about 6% on the London Stock Exchange in an initial reaction, recovered over the next few days, and have returned to the earnings low since. Clearly, investors were not satisfied with the results.

In 2022, revenues (net of duties, excise and other taxes) were up 7.7%, which sounds good on paper, but was largely due to exchange rate tailwinds. It should be noted that British American Tobacco reports its profits in sterling and pays its dividend in sterling, but generates most of its revenue outside the United Kingdom. Currency-adjusted earnings per share ((EPS)) increased by 12.9% year-over-year ((YoY)), or 5.8% at constant exchange rates. While earnings and revenues experienced currency-related tailwinds, weak sterling adversely impacted BTI from a financing cost perspective. As a result, and also due to the sharp rise in interest rates, the company recorded a 10.5% increase in net financing costs. BTI's debt service ability is discussed in a separate section below.

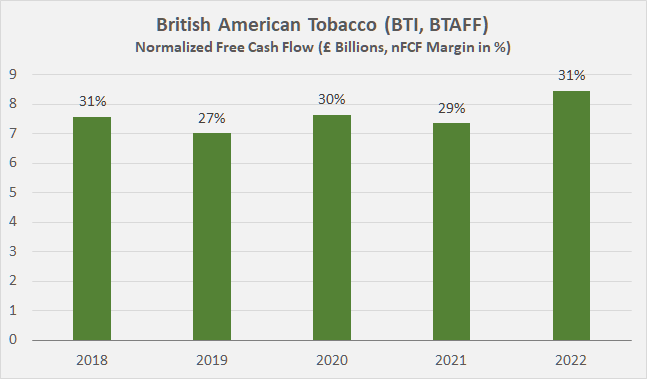

Free cash flow ((FCF)) on an unadjusted basis was £8.3 billion, compared to £7.7 billion in 2021. Given the expected ongoing investments in vaping, oral products, and heated tobacco, I am quite positive about management's expectation of £40 billion FCF over the next five years. The annualized figure is slightly higher than BAT's average FCF for 2018 to 2022 of £7.6 billion, after adjusting for working capital movements and stock-based compensation. Normalized FCF for 2022 of £8.4 billion was a slightly positive outlier due to exchange rate tailwinds and is expected to moderate going forward. BTI's FCF margin is very robust and stable, as expected for a tobacco company with a strong brand portfolio. After paying the generous dividend (current yield of 7.8% after the recent hike), the company has about £3 billion left for debt repayment and acquisitions.

{kind=link}

Figure 1: British American Tobacco’s [BTI, BTAFF] free cash flow, after normalization for working capital movements and adjustment for stock-based compensation (own work, based on the company’s 2016 to 2022 annual reports)

Capital expenditures in 2022 were 5.5% of normalized operating cash flow (OCF), below the 2018-2022 average of 6.9%. Granted, competitor Philip Morris International ( PM ) has invested much more aggressively in the business (averaging more than 10% of its normalized OCF since 2016), but I wouldn't go so far as to conclude that BTI has intentionally neglected organic investments in favor of strong FCF. 7% of normalized operating cash flow reinvested in the business is definitely no mean feat, and there's no denying that BTI has the strongest smoke-free portfolio after Philip Morris International. In stark contrast, Altria Group ( MO ) has so far not only failed to develop a meaningful vaping (investment in Juul Labs) and heated tobacco business (IQOS patent dispute with BTI), but has also reinvested relatively small amounts of cash flow back into the business - 2.9% on average over the last six years. Those who want to dig deeper into Altria should take a look at my recent coverage and older articles.

How Has BTI’s Smoke-Free Portfolio Evolved In 2022?

Revenues from "New Categories" (i.e., heated tobacco, vapes, pouch products) increased by almost 41% YoY and now account for over 10% of total revenues. The category still lost £366 million, but the loss narrowed by over 60% YoY. While it sounds bad that BTI is still losing money with its smoke-free portfolio, it's important to remember that management previously expected the category to be profitable in 2025, but is now confident it will reach that goal as early as 2024. By 2025, BTI is targeting new category revenues of £5 billion, which doesn't strike me as an overly aggressive goal. New Categories performance has been particularly strong in the U.S. (e.g., 63% YoY growth in vapor pods revenue).

BTI's Vuse vapor product line achieved national market leadership with a value share of nearly 41%, up 8.4% YoY. In the last two years , premarket tobacco product applications ((PMTAs)) have been granted for Vuse Solo, Ciro and Vibe, while PMTAs are pending for BTI's newest device - Vuse Alto. In 2022, BTI had to pay an insignificant sum of $95 million to Altria because its Vuse Alto product infringed three patents. Going forward, BTI can be expected to pay a 5.25% royalty on sales of Vuse Alto products. While that sounds like a lot and certainly reduces the profitability of BTI's latest vaping product, I wouldn't overstate the financial damage.

More importantly, all of the PMTAs mentioned relate to tobacco flavored products and the Food and Drug Administration (FDA) recently denied marketing of two Vuse Solo menthol products. From this, it could be inferred that the FDA not only wants to ban conventional menthol cigarettes, but probably also all vaping and heated menthol-flavored tobacco products. In this context, however, it is interesting to note that Philip Morris' Smooth Menthol and Fresh Menthol Heatsticks (to be used in its IQOS system) not only received PMTAs, but were also designated as modified risk tobacco products (MRTPs).

PM is clearly the leader in heated tobacco, as I discussed in my February article . Personally, I think BTI's glo platform is inferior due to its form factor (single battery system with no holder like IQOS), but it comes close enough to a traditional cigarette to help smokers who want to switch from a haptic (cigarette-like filter) and sensory (similar taste and throat feel). Tobacco Heating Products (THP) shipment volume grew to 24.0 billion sticks (+25.6% YoY), significantly less than IQOS, which is expected to reach 150 billion sticks in 2024. Slide 56 of BTI's earnings presentation shows glo's market share performance in selected key markets (presumably the fastest growing), confirming that glo is far behind IQOS. Russia and Ukraine were key growth markets for both IQOS and glo, so the planned - but difficult - exit of Russia (and Belarus) will also negatively impact glo's future growth.

In oral tobacco, traditional products (Grizzly, Kodiak and Camel Snus) saw volumes decline by 8.3% YoY, while revenues increased by 8.2%, mainly due to exchange rate effects and strong pricing. This confirms that Swedish Match, the dominant player in this market, continues to outperform and expand its market share - welcome news for PM shareholders given the recently completed takeover of the owner of market leader ZYN. BTI's nicotine-containing bags, known under the Velo brand, grew 21.7% in volume and 45.3% in revenues YoY, but 2022 sales of just £398 million are hardly moving the needle.

Overall, the relatively weak performance of BTI's New Categories portfolio, particularly heated tobacco and snus products, has certainly been a factor in the uninspiring share price performance since early February. At the same time, it should be remembered that heated tobacco is generally a more profitable business than vaping, so it will be difficult for the business to match - let alone exceed - the cash flow productivity to which Big Tobacco investors have become accustomed. Altria's acquisition of NJOY is also likely going to be a headwind for BTI, as it can be expected that NJOY benefits massively from Altria's distribution network, and NJOY ACE is currently the only pod-based product with FDA market authorization. Still, I wouldn't be too quick to write off BTI's smoke-free portfolio, largely due to the company's success in vaping.

How Did BTI’s Combustibles Volumes Evolve In 2022?

Primarily due to its significant exposure to the U.S. (particularly Newport menthol), BTI reported a 5.1% YoY decline in cigarette shipments. The reasons are the same as those cited by Altria's management: inflation, pandemic-related normalization, prior-year inventories unwind, lower year-end inventories, and category trade-down. U.S. cigarette volume was down a whopping 15.5%, while European volume was down 9.9%. Considering that Altria released its full-year results a week earlier (see my earnings review ), the U.S. numbers were not a surprise and should not be over-interpreted due to expected inventory normalization in 2023. Premium brand market share in the U.S. remained solid (volume share decline by 50 basis points), while the low-end segment grew volume share by 90 basis points. In Europe, BTI performed significantly worse than PM, which reported its full-year earnings on the same day and saw a 2.5% decline in shipments in the European Union and an 8.2% decline in Eastern Europe. It should be noted that the higher percentage in Eastern Europe is partly due to Russia and Ukraine.

I do not believe that the planned exit from Russia and the ongoing war in Ukraine played a role in the sell-off after the earnings release, considering that both countries together account for only about 3% of BTI's total revenues (2021 figure). BTI's comparatively sharp volume decline in Europe was likely another key reason for the negative investor sentiment and shows that Philip Morris is also ahead in conventional cigarettes.

Is BTI's Debt Still Manageable In The Current Interest Rate Environment And Given The Weak Sterling?

There are four reasons why it's worth taking a close look at BTI's debt following the release of its 2022 results:

- BTI's disproportionate volume decline could be a sign that elasticity is increasing, which could limit the company's pricing power and thus its ability to offset declining volumes with price increases. This, of course, has a negative effect on debt servicing.

- BTI's smoke-free portfolio is strong, but still lags behind PM's, particularly in heated tobacco and, since the Swedish Match acquisition, in oral products. As a result, the U.K.-based company may be forced to increase its investment in this area or make acquisitions.

- The strong dollar and sharply higher interest rates are significant headwinds to BTI's ability to service its debt. A continued disproportionate decline in U.S. cigarette volumes and resulting weaker earnings could put further pressure on the company's interest coverage ratio, as could upcoming maturities.

- On a net basis, BTI's already high gross debt actually increased by more than 10% YoY as dollar-related headwinds more than offset net debt repayments.

BTI completed its £2 billion buyback program in 2022, but did not announce a new program for 2023. Instead, the company will focus on debt reduction. As a conservative, long-term investor, I welcome this decision, also in view of the aspects mentioned above.

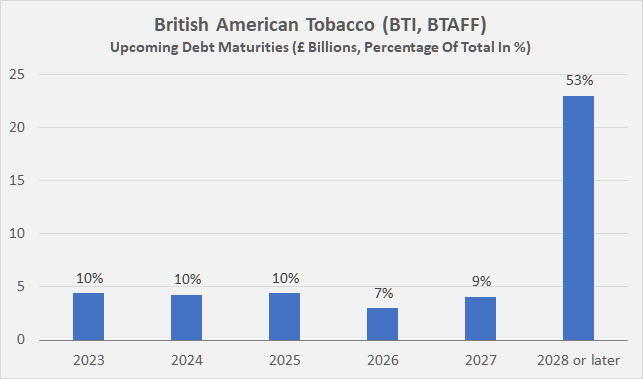

I have already pointed out that the company currently generates excess FCF of around £3 billion, which means that it has a substantial amount available for debt repayment each year. BTI's upcoming maturities are shown in Figure 2 and confirm that the company can pay off a large portion of its notes as they mature off the balance sheet. Therefore, I do not believe that the current interest rate environment will have a material negative impact on the company's ability to service its debt. The reported YoY increase in debt is largely attributable to the significant depreciation of sterling since the end of 2021.

However, it should also be noted that BTI also has a significant amount of floating rate debt. At the end of 2022, the ratio of floating to fixed interest rates was 12:88 after accounting for the impact of derivatives (p. 104, 2022 annual report ).

{kind=link}

Figure 2: British American Tobacco’s [BTI, BTAFF] upcoming debt maturities (own work, based on the information found on p. 256 of the company’s 2022 annual report)

Management reported leverage of 2.9 times adjusted net debt to EBITDA at the end of 2022, down from 3.0 times and 3.3 times at the end of 2021 and 2020, respectively. From a 2018-2022 average normalized FCF perspective, it would take BTI more than five years to pay off all of its net debt (including lease obligations). Based on 2022 normalized FCF, it would still take the company 4.8 years. This thought experiment assumes that BTI suspends its dividend. While this is certainly a significant amount of debt, I don't think it represents an excessive amount of risk. Much of the debt was taken on when Reynolds American Inc. was acquired in 2017, and BTI has made good progress in reducing debt. By comparison, Philip Morris took on significant debt to fund its acquisition of Swedish Match, and therefore currently faces a leverage ratio of about four times net debt to normalized FCF, as I discussed in my article last week . Like BTI, PM does not currently expect to repurchase shares until its leverage is back in check.

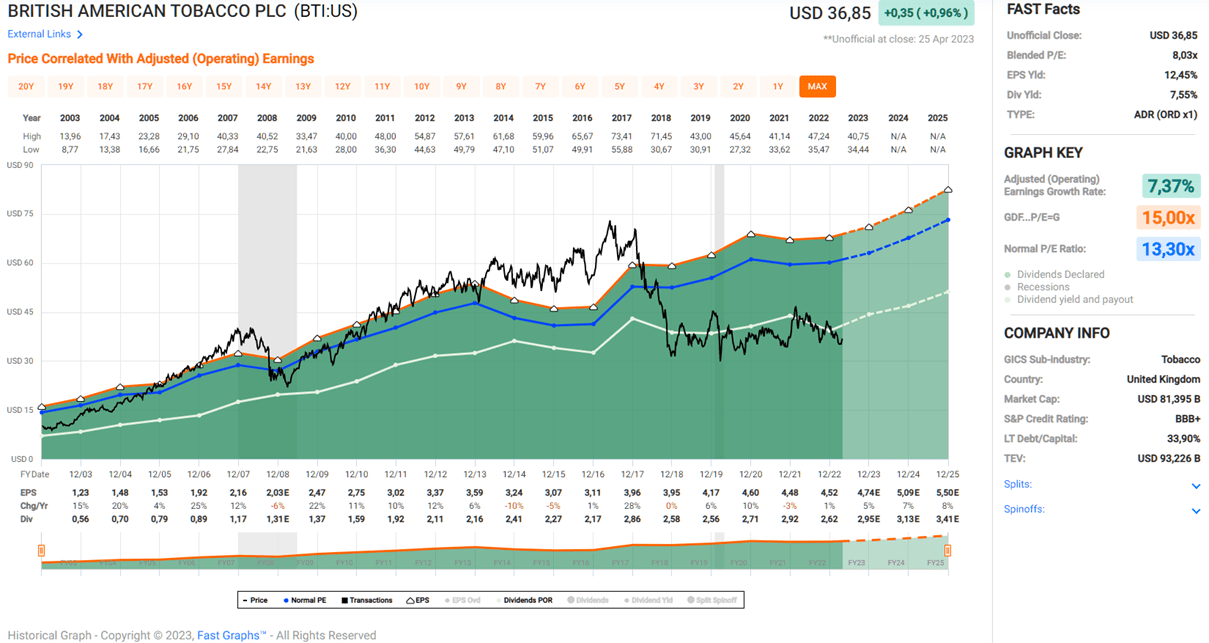

In contrast to PM - which has already indicated very small dividend increases in the near future - BTI rewarded investors in February with a fairly solid 6% dividend increase, effective with the May 2023 payment. As a long-term shareholder, I strongly welcome this move. Considering the current weak share price (Figure 3) and the high dividend yield of almost 8%, the reinvestment of dividends is a very effective contribution to the compounding effect. At the same time, the dividend increase is a testament to management's confidence in the business, while the focus on debt reduction is a sign of management's prudence and conviction to maintain the investment grade rating.

Moody's has maintained BTI's Baa2 (BBB S&P equivalent) credit rating, last affirmed in February 2020, with a stable outlook to date. S&P rated British American's long-term debt one notch higher (BBB+) and recently affirmed the rating , albeit with a negative outlook. A look at BTI's credit default swap (CDS) spreads confirms that investors are not currently very concerned about the tobacco giant's debt. The five-year CDS spread is currently around 105 basis points, below the 150 basis points reached at the peak of the bear market in 2022 and at the height of the pandemic in March 2020.

{kind=link}

Figure 3: FAST Graphs chart of British American Tobacco ADRs [BTI] (obtained with permission from www.fastgraphs.com)

What To Make Of Kenneth Dart’s Stake In BTI?

Unlike, for example, Ray Dalio (Bridgewater), Warren Buffett and Charlie Munger (Berkshire Hathaway, BRK.A , BRK.B ) or Carl Icahn (Icahn Enterprises, IEP ), Kenneth Dart is not really well known. He is an heir to the founder of Dart Container Corp., the world's largest manufacturer of foam cups and containers . Mr. Dart renounced his U.S. citizenship in the 1990s and is apparently a citizen of the Caymans, Belize and Ireland. Dart controls his operations from the Cayman Islands, primarily through Dart Enterprises, which owns a significant portion of the Cayman real estate market, including Camana Bay , the Kimpton Seafire Resort , and the Ritz Carlton .

Dart operates what is often referred to as a vulture fund, stepping into distressed sovereign debt and eventually getting governments to repay the debt at par. For example, Dart profited handsomely from the Brazilian government’s default in 1993 or during the Greek debt crisis .

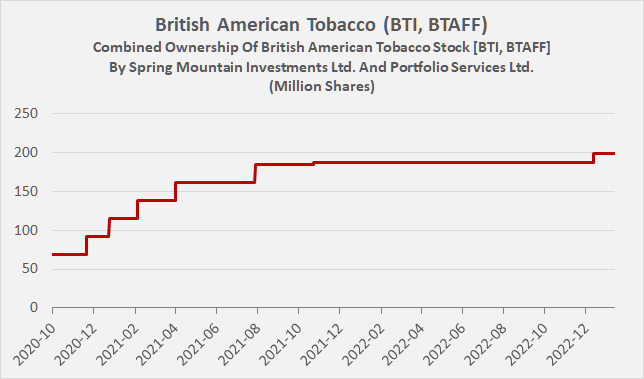

Dart started building a position in British American Tobacco (and, for that matter, its competitor Imperial Brands , OTCQX:IMBBY , OTCQX:IMBBF ) in 2020 or earlier years, but reached the 3% reporting threshold in 2020. To be precise, on October 20, 2020, BTI was informed that Spring Mountain Investments Ltd. ((SMI)), one of Dart's companies, owned about 69 million shares (p. 382, footnote 3, 2022 annual report). The development of Dart's BTI shareholding is shown in Figure 4. Annual 13G filings with the Securities and Exchange Commission ( 2020 , 2021 , 2022 ) confirm Dart's holdings through Portfolio Services Ltd. ((PSL)), likely SMI's holding company. BTI's 2022 Annual Report does not detail the last increase of 11.3 million shares, which occurred sometime in 2022, likely because the shares were acquired directly through PSL or an affiliate of PSL. Thus, at the end of 2022, Dart owned 8.9% of BTI's shares, a value of nearly $8 billion, although the weakness of the British pound must be taken into account.

{kind=link}

Figure 4: Combined ownership of British American Tobacco stock [BTI, BTAFF] by Spring Mountain Investments Ltd. and Portfolio Services Ltd. (own work, based on the information found on p. 382, footnote 3 of the company’s 2022 annual report)

At first glance, Mr. Dart's decision to bet big against the ESG trend that started to come into vogue in 2020 is certainly impressive and shows great conviction. While his net worth is difficult if not impossible to estimate, I think that owning around 200 million shares worth nearly £6 billion is probably a pretty substantial investment. While I'm not a fan of blindly following billionaires into their own investments - after all, they could have different interests - I think Mr. Dart's holding in this case confirms the high value that BTI stock represents since 2019.

It should also be borne in mind that BTI could buy back more than 100 million or 5% of its outstanding shares each year (£3 billion annually, current share price or more if the share price declines further), indirectly increasing Dart's stake, which may have grown over the years. A shift in priority to massive buybacks instead of dividend increases or an outright dividend rebasement in the future could be seen as a sign in this direction. However, don't forget I am only hypothesizing about a "worst case" scenario here.

Although it seems unrealistic for a single investor to buy up such a large tobacco company on the cheap during a bear market, I am still keeping an eye on the development of Dart's holding. Since the Cayman Islands-based investor may have taken advantage of the recent drop in BTI's share price, it makes sense to ask BTI Investor Relations for an update. I have no idea what Kenneth Dart's actual net worth is or whether he is in a position to finance an acquisition that large, and I frankly think it is unrealistic that he could take over an $80 billion tobacco empire. However, history shows that minority shareholders occasionally fall by the wayside in the process, and especially when a particular stock underperforms significantly, a takeover at a low valuation can lock in painful losses. Dell, for example, went private in 2013 in a $25 billion deal .

In conclusion, I am somewhat ambivalent, but basically positive about Mr. Dart's big bet. However, I am a bit concerned about his past record of successfully making big bets against governments and the presumed size of his empire. A leveraged buyout of BTI certainly represents extreme tail risk and cannot be ruled out. However, considering that Kenneth Dart has also built a comparatively small stake in rival Imperial Brands (a quarter the size of BTI by market cap), which traded at even lower valuations in 2020 and 2021, I would not overstate the risk of a takeover. I think the hypothesis that Dart will acquire and merge both Imperial Brands and British American is untenable, not only from a financial perspective, but also from an antitrust perspective. Nevertheless, it is of course important to closely monitor further developments. Perhaps Mr. Dart is like many other investors in BTI: He appreciates the excellent valuation, reliable cash flow, globally diversified portfolio and, in his case, nearly £500 million of dividends per year.

Concluding Remarks

British American Tobacco reported good results on the surface. However, digging deeper, it becomes clear why investors have turned a bit more cautious.

Cigarette volumes declined quite sharply, with results in Europe significantly worse than those of rival Philip Morris International. Earnings and free cash flow experienced a nice FX-related tailwind, but that should be considered a one-off and certainly didn't please U.S.-based shareholders. The weak sterling led to a drop in the value of the shares in U.S. dollars and also a lower dividend payout. Of course, things can turn around, but the currency is definitely one of the main risks to consider before investing in BTI from a U.S. perspective.

BTI's smoke-free portfolio showed strong performance in vaping, but the likely growing competition from NJOY after the Altria acquisition (significant distribution power) should not be underestimated. In heated tobacco, glo is well behind Philip Morris' IQOS. In oral tobacco, PM has also taken the lead through its recently completed acquisition of Swedish Match. BTI's Velo nicotine pouches are seeing strong growth, but are still an insignificant revenue contributor, while shipments of traditional snus products are declining. On a positive note, the company now expects its portfolio of smoke-free products to become profitable a year earlier than previously expected, and considers a contribution of around 20% to net revenues by 2025 to be realistic.

Debt has increased due to currency headwinds, as have the company's financing costs. As a result, BTI is now prioritizing debt reduction over further buybacks, but the 6% dividend increase was definitely encouraging to see. As a conservative long-term investor, I welcome management's focus on debt reduction given the current interest rate environment and potential ESG-related lending restrictions.

Even though the deep dive into earnings definitely revealed quite mixed results, I am still a happy and convinced shareholder of British American Tobacco. The stock is cheaply valued with a normalized free cash flow yield of 11.8%, a blended price-to-earnings ratio of 8.0 according to FAST Graphs (Figure 2), and a dividend yield of nearly 8% after the last raise. As a result, I recently added to my position, which now represents 2.8% of my total portfolio value. I believe British American Tobacco is inferior to Philip Morris International, but the significant valuation difference is not justified in my opinion. From a price-to-earnings perspective, PM stock trades at a 100% premium to BTI stock.

Considering that British American Tobacco is the second-best investment in the tobacco space by almost all objective operating metrics and considering all major risks (see my previous coverage), and taking into account the cheap valuation that has characterized the stock since its sharp decline in 2018, I can understand why secretive billionaire Kenneth Dart has built up a massive stake over the years. He now owns nearly 9% of the company and generates nearly £500 million from dividends each year. I also started building my stake in British American in 2020 and got heavily into the stock in 2021. I have also added to my position occasionally in 2022 and took advantage of the recent dip.

I became aware of Mr. Dart's stake in British American Tobacco in mid-2021. I don't blindly follow billionaires into their investments and do my own due diligence, but I think Kenneth Dart's involvement confirms the strong risk-reward profile of BTI/BTAFF stock. However, given the character of the investor and the apparent sheer size of his empire, I continue to keep a close eye on Mr. Dart's holding. While acquiring an $80 billion tobacco empire sounds unrealistic, it's important to remember that such large deals are not impossible (and have happened in the past), especially considering the availability of cheap debt and a strong asset base that can be posted as collateral. After all, Mr. Dart owns a substantial real estate portfolio in the Caymans. At this point in time, however, I don't think this extreme tail risk is really relevant, but I will still inquire with BTI's investor relations department about a possible further increase in Mr. Dart's holding.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

British American Tobacco: Mind The Vulture