BTI - British American Tobacco: Pathways To Growth High Yield And Strong FCF Remain Attractive

2024-01-17 23:02:15 ET

Summary

- UK cigarette retail sales trends continue to be weak, prompting British American Tobacco to focus on next-generation products.

- BTI aims to grow its market share in the US and sees potential in its next-gen products, including vaping and modern oral products.

- Despite weak sales growth, the Company remains undervalued with high free cash flow and offers a high dividend yield.

- Shares have held in the upper $20s after the negative write-down news in December, and I highlight key price levels to watch ahead of earnings next month.

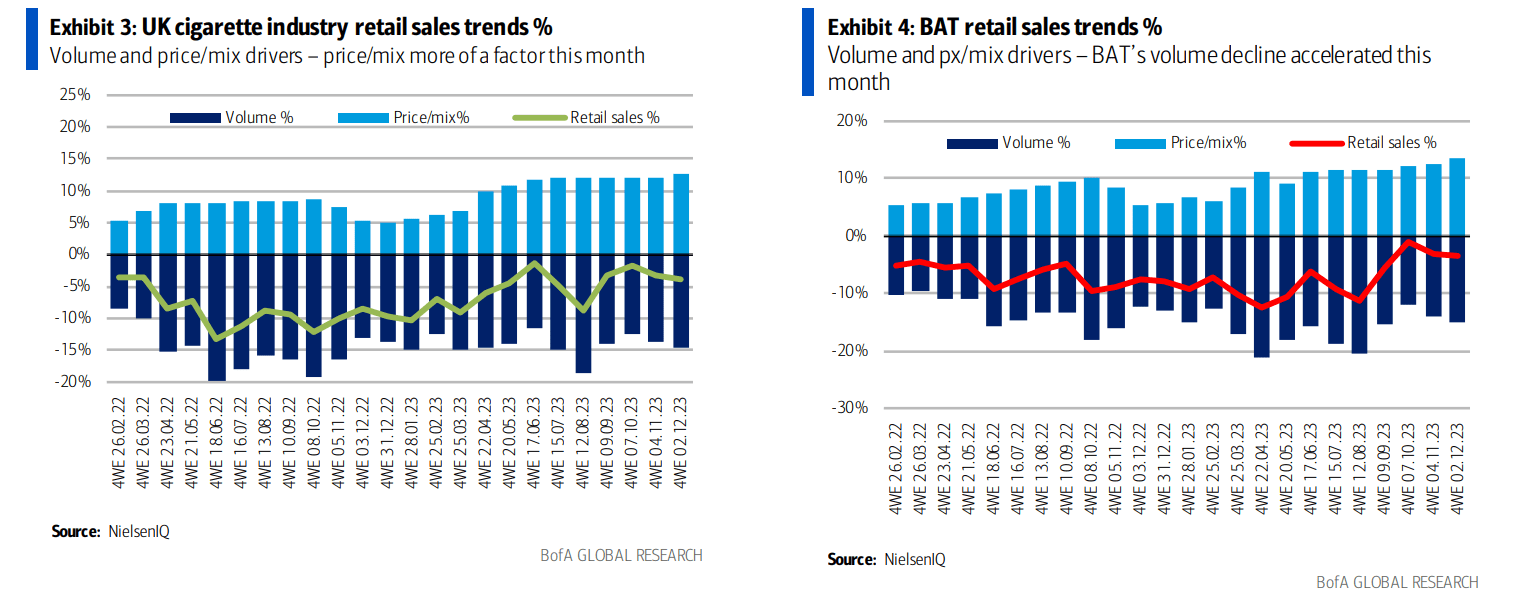

UK cigarette retail sales trends continue to be weak. That's no big surprise, and it's the general trend seen around the world. British American Tobacco (BTI) sees tepid sales growth as the large-cap company aims to refocus on next-generation products, including vaping, heated tobacco, and modern oral products.

For now, I reiterate my buy rating on BTI. I continue to see the stock as undervalued with high free cash flow. A GBP 25 billion impairment charge announced in early December 2023 was initially met with selling activity in the stock, but BTI has held around the $30 level. I will outline important price points to watch ahead of earnings due out next month.

UK Cigarette Sales Growth Negative YoY

{kind=link}

According to Bank of America Global Research, British American Tobacco is the largest European tobacco company with operations in most major markets across the globe. The company's biggest market is the US, where it generates around 55% of EBIT. BAT's main brands are Kent, Dunhill, Lucky Strike, Pall Mall, Rothmans, Newport, Camel, and Natural American Spirit. The company also plays in the Heated Tobacco category with its brand glo, in vaping where its main brand is Vuse, and in Modern Oral with Velo.

The London-based $66.7 billion market cap Tobacco industry company within the Consumer Staples sector trades at a low 6.5 forward non-GAAP price-to-earnings ratio and pays a high 9.5% trailing 12-month dividend yield. Ahead of earnings due out in early February, shares trade with a low 19.5% implied volatility percentage while short interest on the stock is not listed.

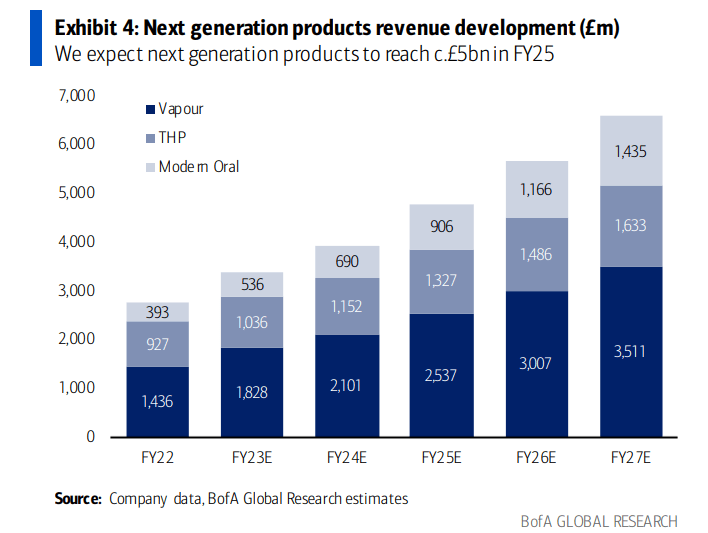

While sales of traditional cigarettes continue to decline domestically and in Europe, BTI's new focus on next-gen products offers a pathway to some growth, though it may take time, and I assert we need to see earnings accretion before the fundamental outlook can improve with confidence. Still, the firm sees a stabilizing US market share after a modest dip lately given the new focus. BTI's Modern Oral is expected to contribute over $1 billion in revenues by 2026, for instance.

Overall margin growth should help the company since sales growth is seen hovering around current levels. What's more, the management team continues to work on deleveraging its balance sheet along with rewarding shareholders with a high dividend and a possible restart of buybacks. BTI remains a high-moat stalwart with brand loyalty as governments limit new industry entrants, allowing BTI some pricing power.

BTI: Optimism Around Next-Gen Products

{kind=link}

Following the impairment news, sellside analysts came out in defense of BTI. Jefferies noted that US sales may actually reverse higher this year and other non-cigarette niches are forecast to produce growth over the quarters ahead.

Key risks include regulatory risks, particularly in the US, weaker sales trends in vaping, global market share declines, and the broader trend of lower combustibles revenue.

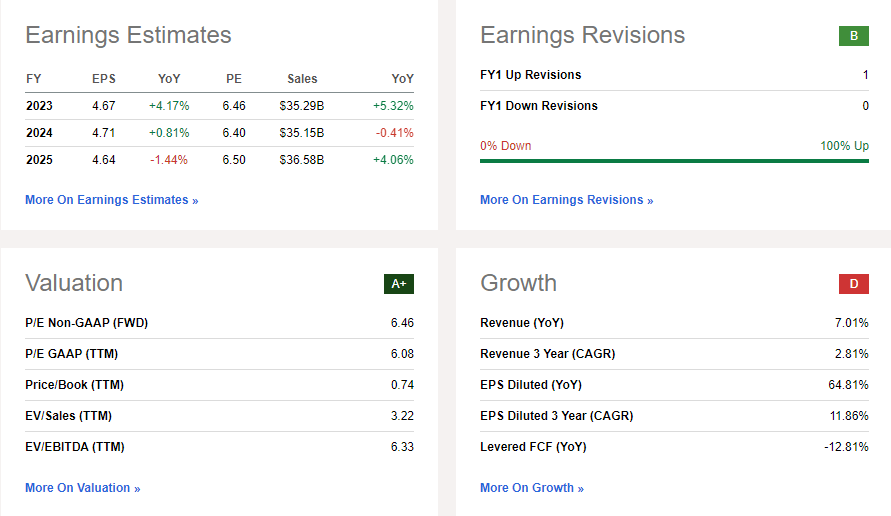

On valuation , analysts at BofA see earnings rising this year after a tepid year of EPS growth in 2023. Per-share profits are expected to increase by 1.8% while a profitability acceleration is expected in 2025. The consensus outlook, however, is less sanguine, according to Seeking Alpha. As pictured below, non-GAAP EPS is forecast to hover around $4.70 over the coming years while sales growth may be in the red for 2024.

Still, dividends are forecast to continue to rise, per BofA, over the coming quarters, which could make for a yield north of 11% by the out year. Furthermore, shares are priced cheaply with a 6-handle P/E and an EV/EBITDA multiple of less than 7, about half that of the S&P 500's.

BTI: Earnings Outlook, Mid-Single-Digit P/E

{kind=link}

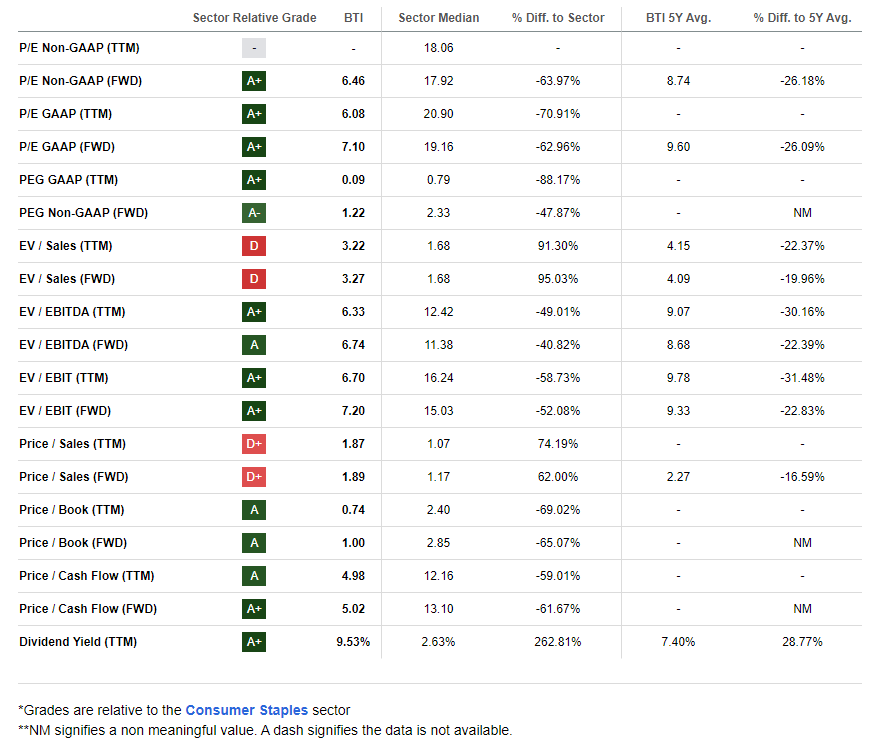

If we assume the more pessimistic $4.70 consensus EPS figure and apply the stock's 5-year average earnings multiple of 8.7, then shares should be priced near $41, making the stock undervalued today. Along the way, investors are paid a lofty dividend, and BTI has been buying back shares. Most other valuation metrics are attractive, too. With a very high free cash flow yield of just under 20%, the firm should continue to reward shareholders.

BTI: Compelling Valuation Metrics

{kind=link}

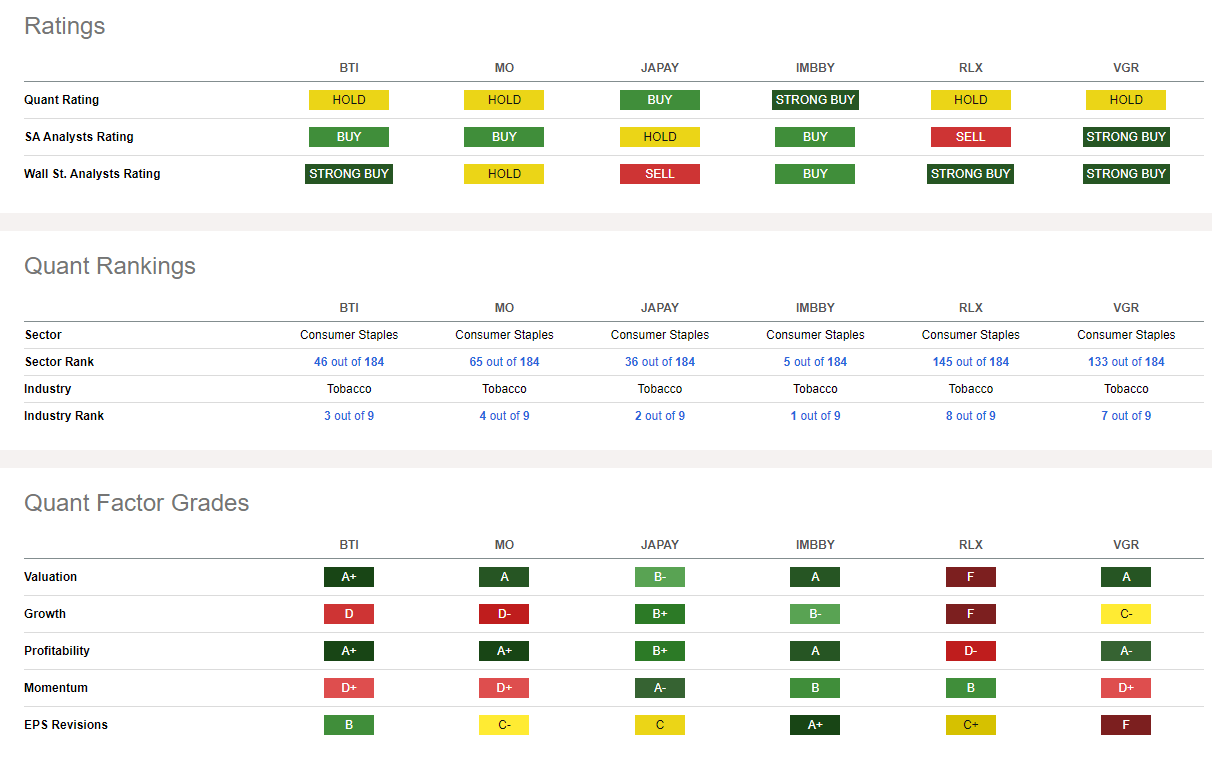

Compared to its peers , BTI features the strongest valuation rating, though growth trends are admittedly quite weak as the industry shifts away from combustibles. Still, profitability trends are highly impressive and EPS revisions , despite the massive write-down news late last year, are on the good side. Finally, share-price momentum has been exceptionally soft over recent months, and I will detail key price levels to watch later in the article.

Competitor Analysis

{kind=link}

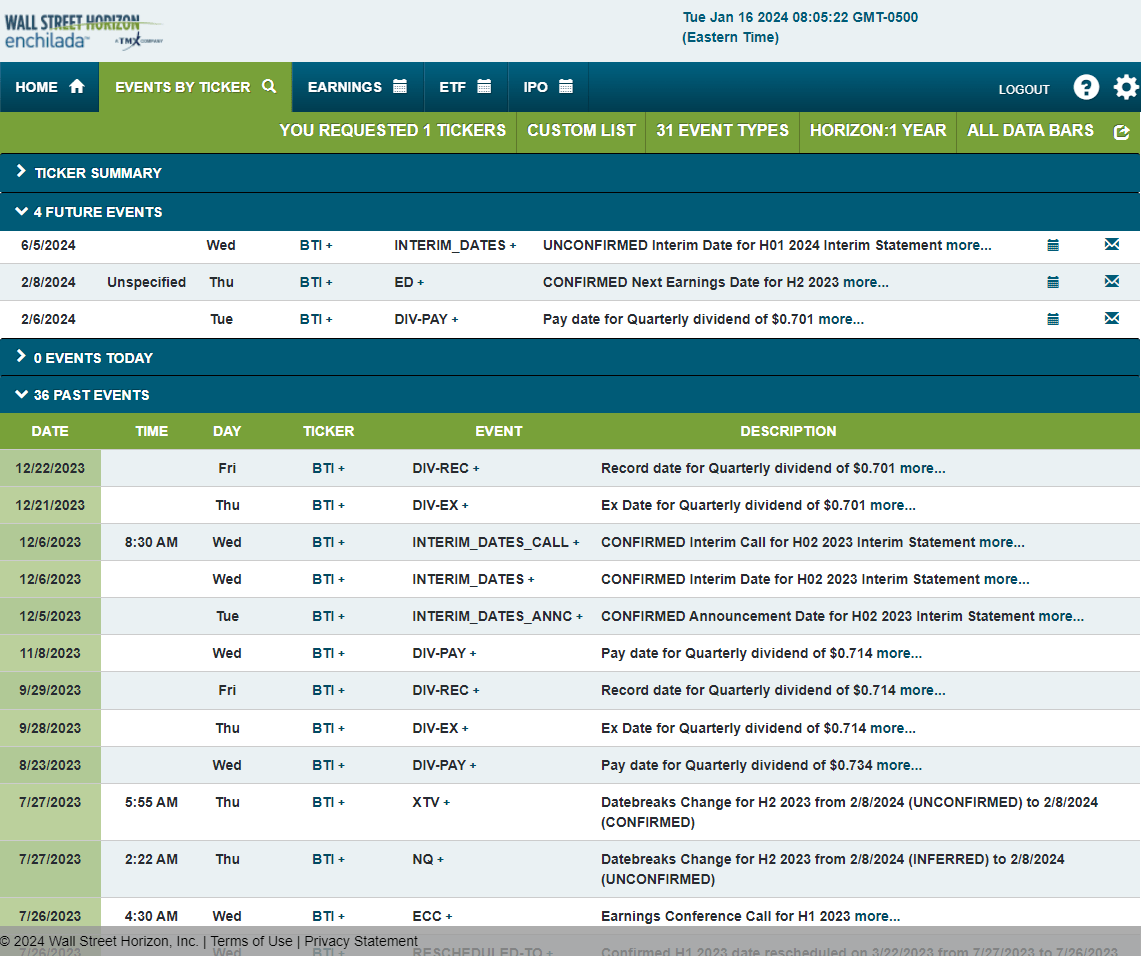

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed H2 2023 earnings date of Thursday, February 8. Before that, the stock trades ex a $0.701 dividend on Tuesday, February 6.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

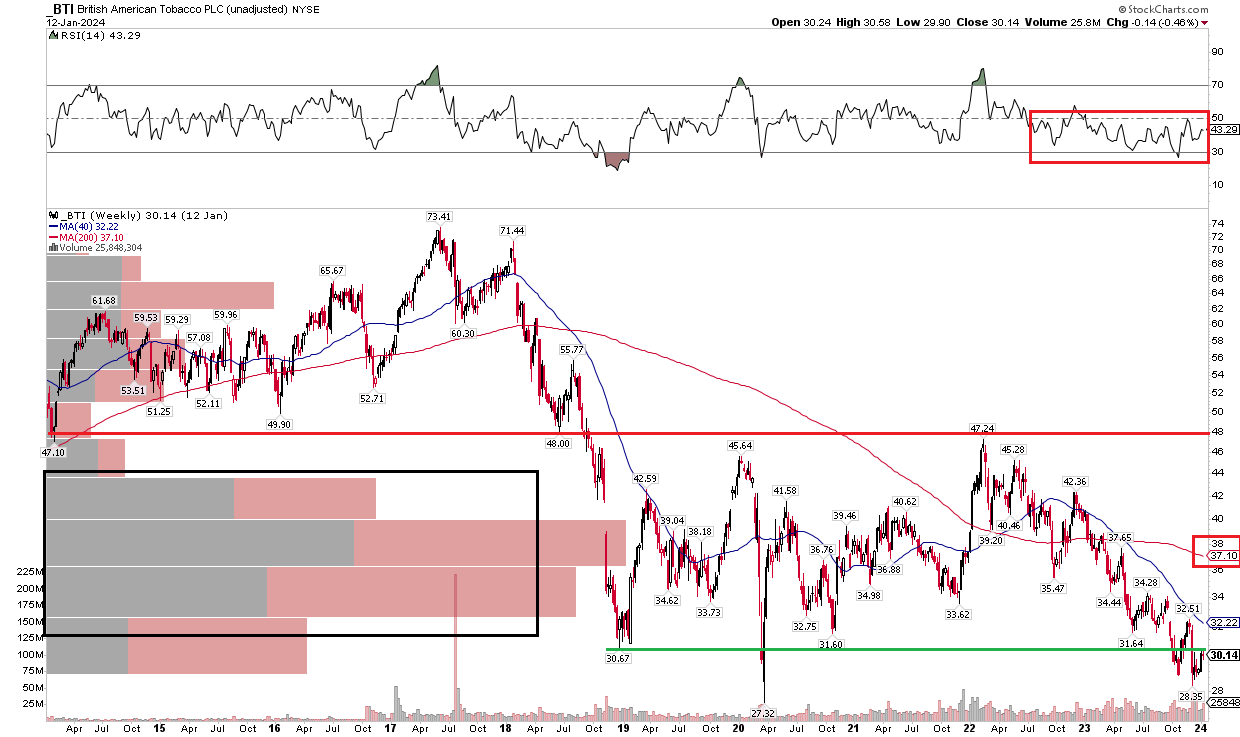

Since I initiated a buy rating on BTI last summer, the stock has wavered. Notice in the chart below that shares are now under key support I highlighted in July 2023. That is a technically vulnerable position. Moreover, the RSI momentum gauge at the top of the graph is firmly in a bearish range - I would like to see the stock rally back into the low $30s on better momentum for a sustained move toward my fundamental intrinsic value target.

But with a long-term 200-day moving average that is negatively sloped and a high amount of volume by price from $30 up to the mid-$40s, the bulls will have their work cut out for them in order to turn BTI into a bullish technical story. Long-term resistance is seen in the upper $40s. For now, the stock looks weak technically on both an absolute basis and relative to its sector and the global stock market. These are negative factors, so the technicals remain a risk.

BTI: Bearish RSI Trends, Shares Wobble Around Long-Term Support

{kind=link}

The Bottom Line

I reiterate my buy rating on BTI. The write-down news last month appeared largely priced into the stock, but shares are still under key support. I see the valuation as attractive, and BTI's high yield is backed up by strong free cash flow.

For further details see:

British American Tobacco: Pathways To Growth, High Yield, And Strong FCF Remain Attractive