BTAFF - British American Tobacco's $31.5B Write-Down: Big Fear Creates Big Opportunity

2023-12-08 15:00:52 ET

Summary

- British American Tobacco announced a $31.5 billion write-down, causing its stock prices to plummet significantly.

- I will explain why the market has overreacted to the write-down, creating an unusual opportunity for investors.

- I do not expect any material impact on its profitability due to this write-off.

- The company's capital-light business model and strong brand names make it resilient and able to transition into alternative products.

$31.5B write-off in focus

This Wednesday, British American Tobacco p.l.c. ( BTI ) announced a $31.5B write-down . The write-down was caused by a combination of factors. To me, the gist is probably best summed up by its CEO Tadeu Marroco , who described it as "accounting catching up with reality." Anyway, the purpose of this article is not to analyze the cause of the write-down.

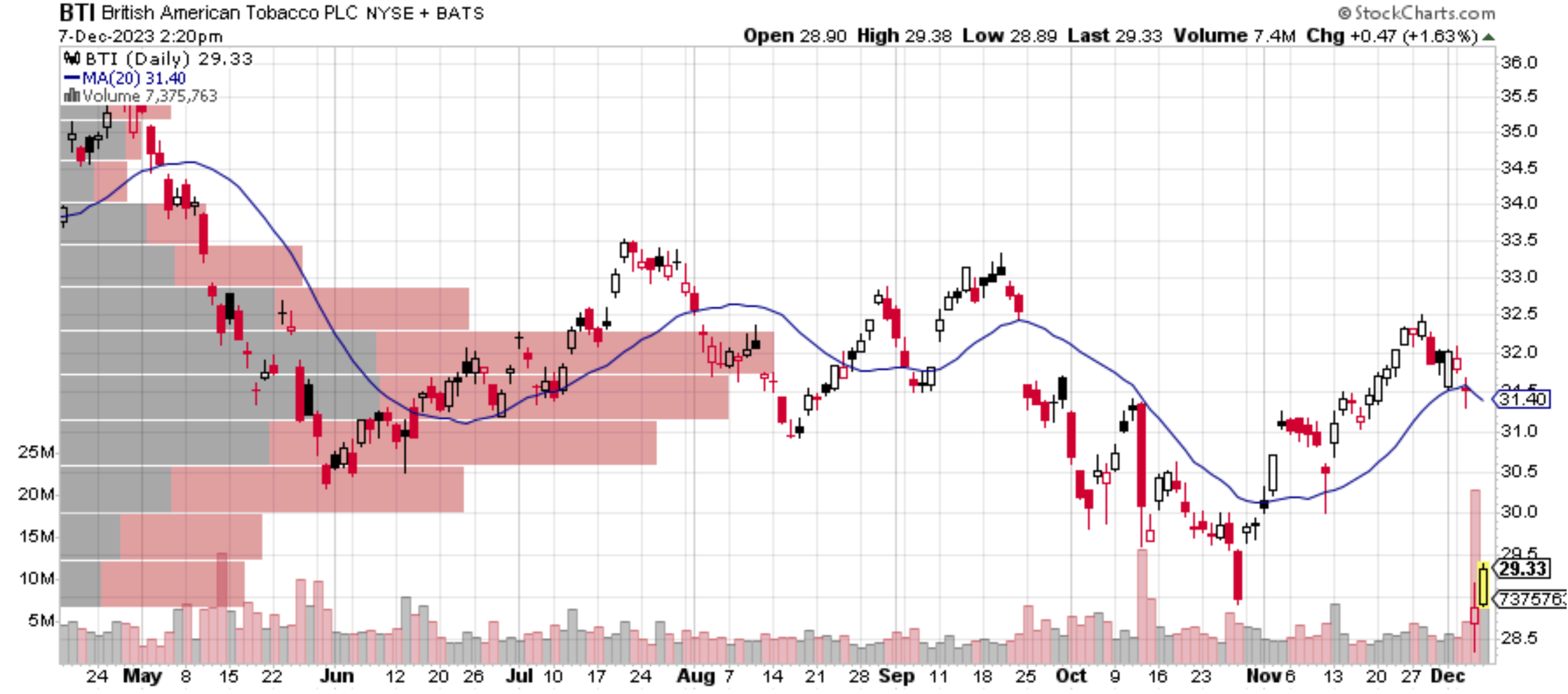

Instead, the purpose of this article is to argue that the market has overreacted to the write-down and thus created an extraordinary opportunity. As seen in the chart below, BTI stock prices plummeted after the news came out, dropping by about 10% during intraday trading on extremely heavy volume, a classical sign of extreme fear. In the remainder of this article, I will argue why the market has overreacted, and my arguments will be primarily anchored around 2 considerations:

- To start, the business enjoys an extremely capital-light model. Therefore, I do not expect any material impact on its profitability due to this adjustment. Furthermore, I also do not expect an extraordinary amount of capital investment for it to pursue alternative products.

- Admittedly, a $30 billion write-off is substantial by any measure for a company with a market cap of around $60B and can certainly impact its valuation. But I will argue that: A) the P/BV multiple is not the best metric given its capital-light model, and B) even if we apply the P/BV ratio anyway, its valuation multiple is still very attractive.

{kind=link}

Extremely capital-light business

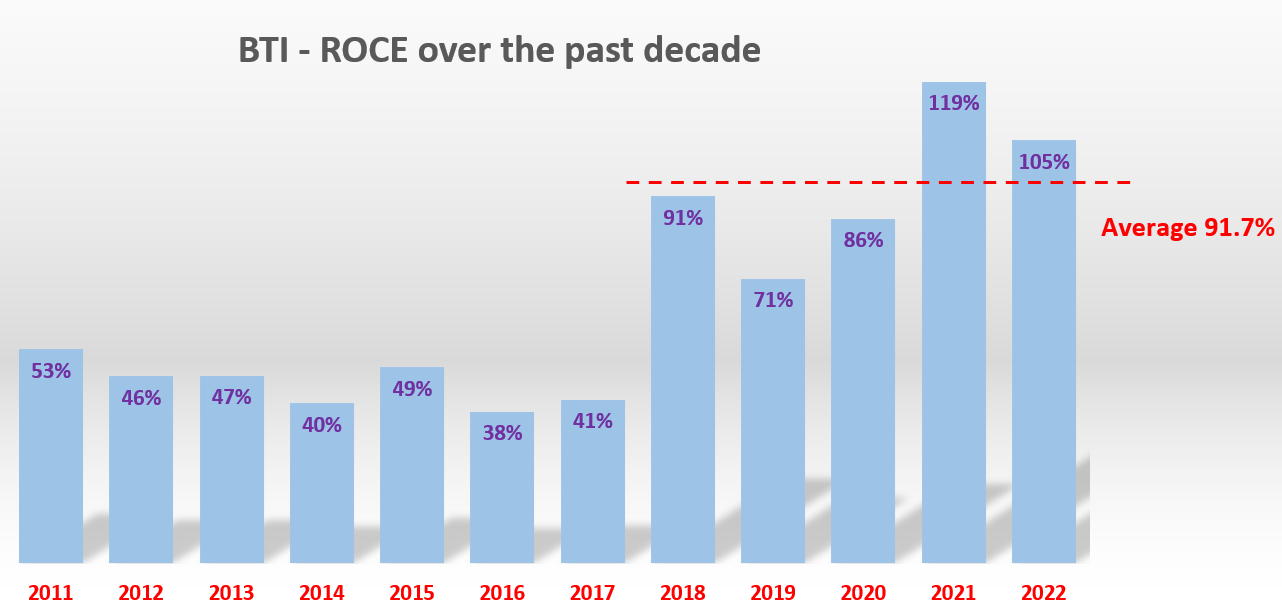

The tobacco industry is famous (or notorious) for its capital-light business model. As Warren Buffett once pointed out, they "cost a penny to make, sell for a dollar, and enjoy fantastic brand loyalty." These words so accurately capture the moat of BTI. As a reflection, the next chart shows its ROCE (return on capital employed, see our earlier writings for more details). As seen, it has been maintaining an average ROCE of ~91.7% in recent years, not only competitive when compared to its tobacco peers but also on par with some of the most lucrative tech businesses, including Apple (AAPL).

In the case of BTI, the root causes for such superb ROCE are exactly as Buffett described. It owns a strong brand portfolio (e.g., Dunhill, Kent, Lucky Strike, et al.), with high brand recognition and loyalty. Production does not require high capital investment. In addition, BTI has a long history of efficient operations, further improving its profitability and return on capital.

Against this background, let's get back to the write-down. Regardless of the cause of the write-down (either due to accounting adjustment or due to the decline of the U.S. cigarette market), I do not expect the write-down to cause any material impact on future profitability. Furthermore, due to the capital-light nature of its business and strong brand names, I believe the business can transition into alternative products (such as E-cigarettes and vapor products) with a relatively small amount of capital investments.

{kind=link}

Valuation still too cheap

Nonetheless, investors should not and cannot pretend that nothing has happened when a $60B company writes off $30 billion from its balance sheet. Such a write-off certainly should impact its valuation. Here I will evaluate the impact from two different approaches and argue that the valuation is still too cheap by either approach.

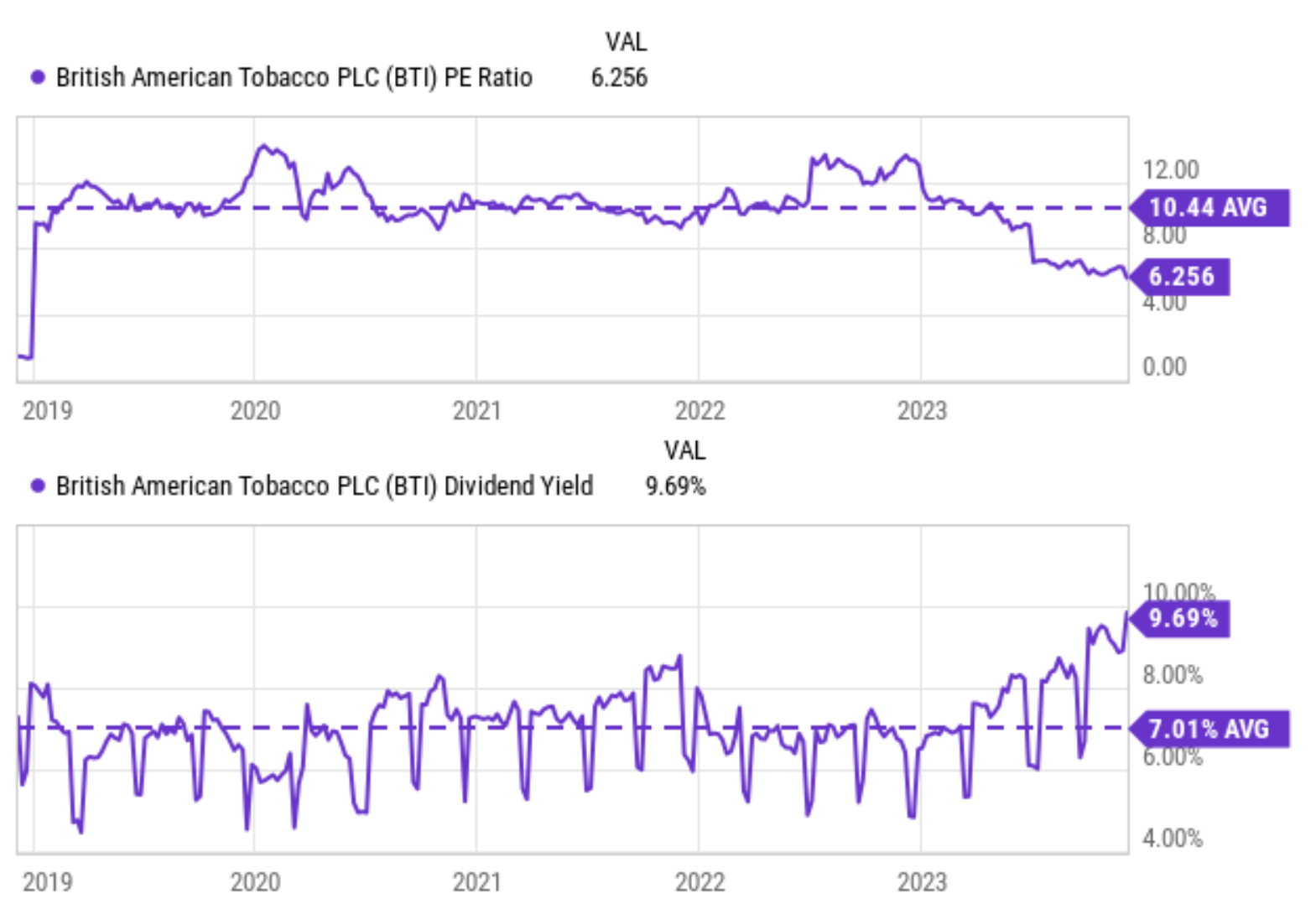

First, if you agree with my analysis of its capital-light model and the write-off's impact (i.e., the lack of impact) on its future earnings, the P/BV multiple is not the proper metric to value the business. A profit-centric measure such as EPS or dividends is a more relevant measure. As shown in the chart below, by either earning yield or dividend yield, BTI is trading at very compressed multiples in absolute terms, compared to its historical averages, or compared to the overall market.

{kind=link}

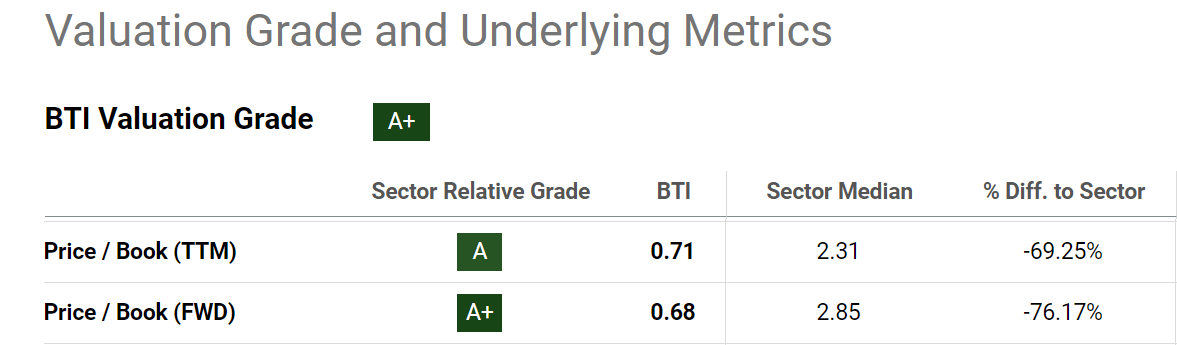

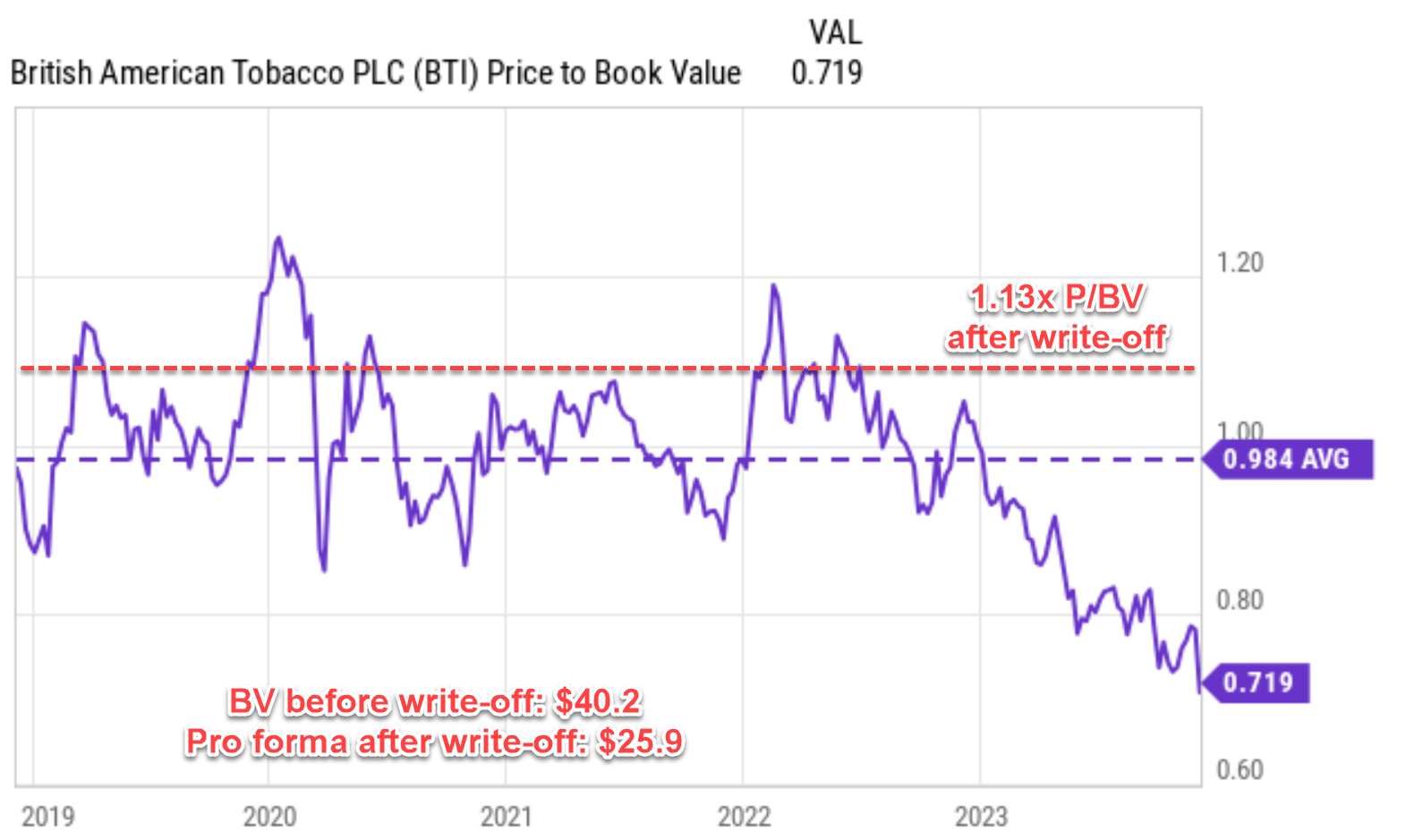

Now, if we insist on applying the P/BV ratio, let's perform a pro forma estimate. To provide a baseline, the chart below shows BTI's price-to-book (P/BV) ratio in comparison with the sector average before the write-off. As seen, BTI was trading below book value (with a P/BV ratio around 0.7x) and also far below the sector average (with a P/BV ratio above 2x).

BTI's book value was around $40.2 per share (by which I mean per ADS and will stick with ADS hereafter) before the write-off based on its most recent earnings statement. With its current share counts, the $31.5B write-off translates into about $14.3 per ADS. As a result, my pro forma estimate of its book value after the write-off is around $25.9 per ADS. Thus, at its current price of around $28.3 at the time of this writing, its pro forma P/BV ratio is about 1.1x after the impact of the write-off is adjusted. It is still a very attractive level compared to the sector's median and also compared to its historical average, as seen in the second chart below.

{kind=link}

{kind=link}

Other risks and final thoughts

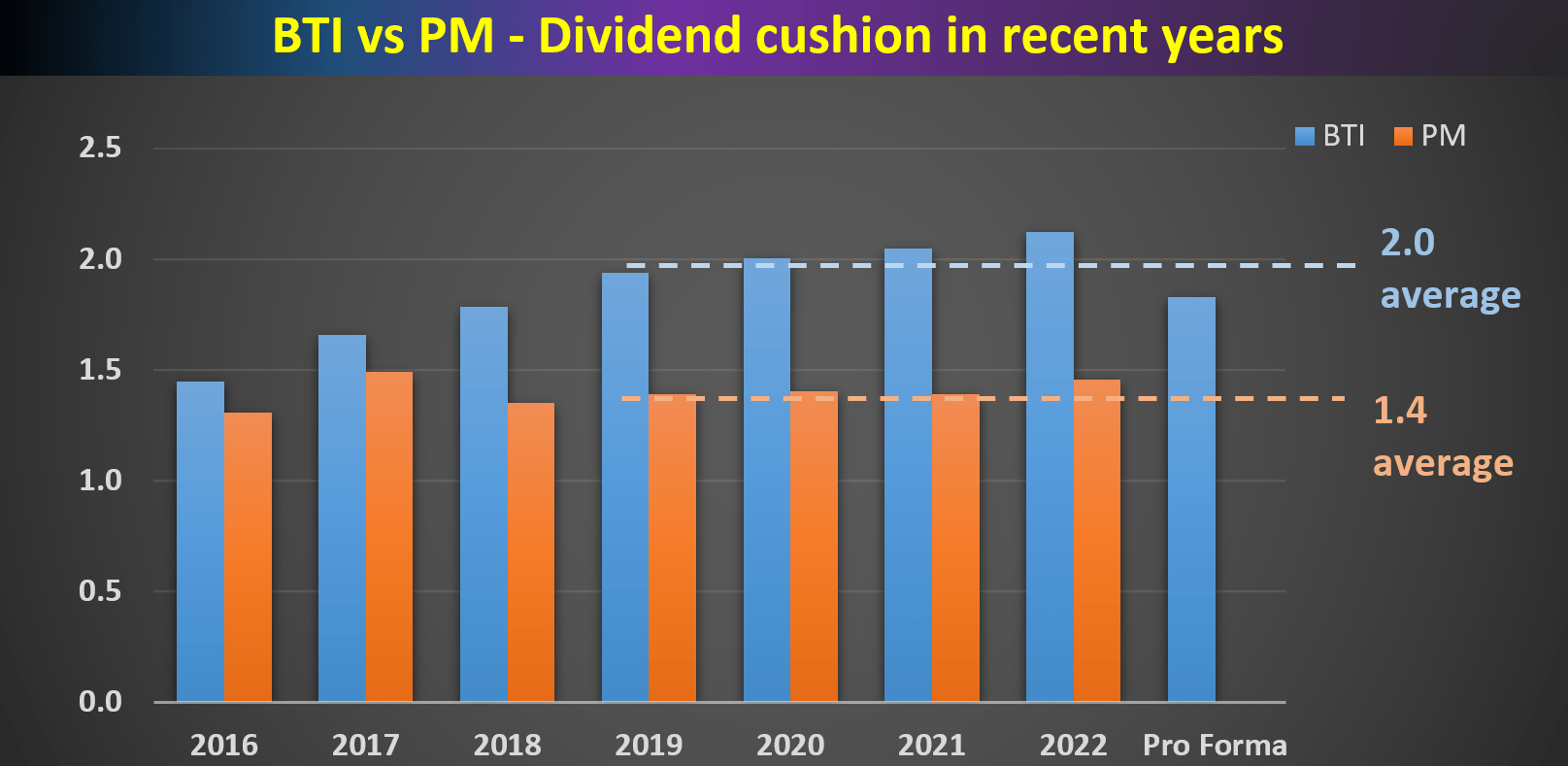

Before closing, I'd like to point out one more key upside risk and also a key downside risk in my mind. Due to the price correction, the stock is now yielding close to 9.7%, which is a solid return already in itself. Furthermore, the dividend is well covered in my view. Again, if you agree with my above argument that the write-off has no impact on its profitability, then the write-off will have no impact on its future payout ratios, either. Balance sheet strength should have an impact on dividend safety, and a good metric to capture the impact is the divide cushion ratio ("DCR"). The concept is detailed by Brian Nelson in his book entitled Value Trap . The gist is to include the balance sheet strength in the evaluation of dividend safety. Specifically:

The DCR is calculated by A) summing up the existing net cash (total cash less total long-term debt) a company has on hand (on its balance sheet) plus its expected future free cash flows (cash from operations less all capital expenditures) over the next five years, and B) dividing that sum by future expected cash dividends (including expected growth in them, where applicable) over the same time period. If the ratio is significantly above 1, the company generally has sufficient financial capacity to pay out its expected future dividends, by our estimates. The higher the ratio, the better, all else equal.

As shown in the chart below, BTI's DCR has been on average far better than the 1x threshold in the past. The write-off would hurt its DCR as expected. But my pro forma estimate is still around 1.8x, still a safe level either compared with the 1x threshold or its close peers such as Philip Morris (PM).

{kind=link}

Now, downside risks. BTI faces all the common risks generic to the tobacco sector, and I won't repeat them here. Here, I will focus on a key downside risk that is unique to BTI but not to other tobacco stocks. And this risk is its lack of geographic diversification - in relative terms - in my mind. Compared to other tobacco companies like PM and Imperial Brands, BTI is primarily exposed to the U.S. and U.K. markets. It has a limited presence in key emerging markets in comparison. This lack of diversification could limit BTI's future growth opportunities and also make it more susceptible to regulatory changes, especially for its alternative products. The U.S. regulatory ruling regarding JUUL and its impact on Altria Group ( MO ) serves as a recent example of the downside of concentrated geographical exposure.

To conclude, my thesis is that the market's extreme reaction to BTI's write-down has created an extreme opportunity. I see the upside risks far outweigh the downside risks. To recap, the key pillars on which my thesis rests are: A) I do not expect any material impact from the write-down on its future profitability; B) P/BV ratio is not the proper metric to value a capital-light business like BTI; and C) even if we insist on the use of P/BV ratio, my pro forma estimates still show attractive valuation after the write-off.

For further details see:

British American Tobacco's $31.5B Write-Down: Big Fear Creates Big Opportunity