BTAFF - British American Tobacco: What To Make Of The £25 Billion Bombshell

2023-12-06 15:39:11 ET

Summary

- British American Tobacco p.l.c. today announced a £25 billion impairment charge, mainly relating to its U.S. cigarette brands, sending BTI stock tumbling.

- The impairment charge is due to the change in the estimated useful life of the U.S. combustible brands (Newport, Camel, etc.) to 30 years, implying zero value after 2053.

- In this update, I share my take on the impairment charge employing management's previous remarks and its impact on the valuation of BTI stock.

- I also discuss my hypothesis on the possible sale of British American's 29% stake in ITC Ltd., which is currently worth around £16 billion.

Introduction

On December 6, 2023, British American Tobacco p.l.c. ( BTI , BTAFF ) published its full-year pre-close trading update .

The company reaffirmed its previous earnings per share ((EPS)) guidance and reported a de facto break-even for most of the New Category segment (e-vapor, heated tobacco and oral nicotine products). While overall growth was solid in Asia Pacific, Middle East and Africa ((APMEA)) and also overall in the Americas and Europe ((AME)), the company continues to see macroeconomic pressure in the U.S. and thus in its combustible products segment there.

However, management spooked investors (who sent the stock tumbling by roughly 8% at the time of writing) with the announcement of a £25 billion impairment charge, mainly relating to its U.S. brands, which it acquired in 2017 ( Reynolds American Inc., "RAI"). BTI stock now trades at a blended price-to-earnings ratio of 6.1 (according to FAST Graphs) and a free cash flow yield of over 14%. Clearly, Mr. Market is increasingly doubting the long-term viability of British American Tobacco.

In this update ( I cover BTI stock regularly ), I share my take on the impairment charge and how I think it affects the fair value of BTI stock. I also share my hypothesis about the possible sale of the more or less "hidden" asset on the balance sheet - British American's 29% stake in ITC Ltd., which is currently worth around £16 billion.

What To Make Of BTI's £25 Billion Impairment Charge

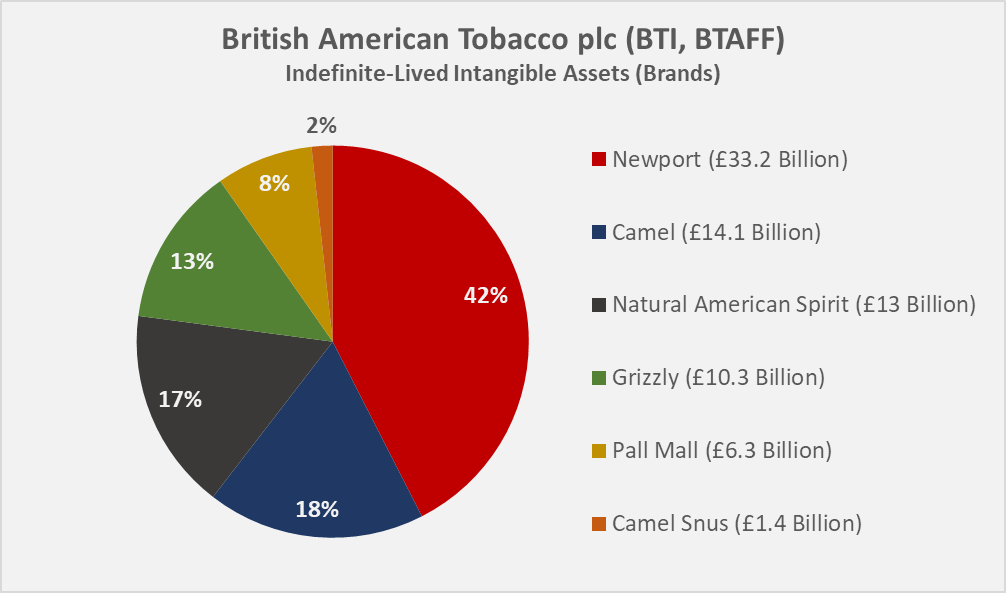

Mainly due to the acquisition of Reynolds American in 2017, BTI has a high proportion of goodwill and other intangible assets on its balance sheet . At the end of 2022, goodwill amounted to almost £48 billion, of which £37 billion was attributable to RAI. Intangible assets with indefinite useful lives had a carrying amount of more than £78 billion at the end of 2022 and were attributable to the following brands:

{kind=link}

Figure 1: British American Tobacco p.l.c. (BTI, BTAFF): Brand-attribution of indefinite-lived intangible assets (own work, based on company filings)

Clearly, a ban on menthol-flavored cigarettes in the U.S. would have a significant negative impact on the estimated value of Newport (market leader) and other brands for which menthol variants are available. This is of course nothing new and is explained in detail in BAT's 2022 annual report (p. 229 f., note 12 e/V), and the company has also taken a ban into account in the scenario analyses underlying the impairment tests.

In total, British American had £129 billion of goodwill and other intangible assets on its balance sheet at the end of 2022, of which a large proportion (almost 90%) is attributable to Reynolds American Inc. At the end of 2023, the company will recognize an impairment loss of approximately £25 billion. This is expected to lead to a decline in the equity ratio by approximately 10 percentage points, or from 49% to around 39%.

Details on the impairment charge will only be disclosed in the company's upcoming annual report. So far, we only know that the impairment is due to the fact that the company now measures the carrying value and useful economic life of the U.S. combustible brands over 30 years. Previously, management used a discrete five-year model, which is grown into perpetuity thereafter (p. 227, 2022 annual report).

The change in the estimated useful life of the assets to 30 years implies that management considers the value of brands such as Newport and Camel to be zero from 2053 and consequently no longer expects any present value cash flow contribution from this date.

While it is a proven fact that conventional cigarettes are in decline (and have been for several decades), I think it is also reasonable to expect that cigarettes will not disappear completely. To ascribe a value of zero to Newport and other brands after 30 years (even in the event of a ban on menthol cigarettes) is, I think, overly conservative. That said, it is important to understand that impairment charges are not taken lightly and there are strict rules on how cash-generating units (CGUs) must be tested for potential impairment (i.e., International Accounting Standard 36 ).

While management obviously has a solid basis for believing that Newport and other brands are worthless (from a present value perspective) after 2053, as a conservative investor I have always viewed British American's cash flows as being in (slow) terminal decline. The potential for cash flow growth of tobacco companies (ignoring smoke-free products) is increasingly limited, as I explained in one of my recent articles on Altria Group, Inc. ( MO ), due to steadily decreasing potential for continued operational efficiency improvements and, most importantly, the increasing price elasticity of demand.

In my view, it is currently impossible to accurately estimate the impact of the impairment on the valuation of BTI stock in terms of a change in the present value of the cash flows. However, based on management's comments in note 12 (Intangible Assets, p. 226 et seq., 2022 annual report), I consider a back-of-the-envelope estimate of the impact to be feasible.

On page 230 of the report, management illustrates the impact of a given change in the pre-tax discount rate or the long-term growth rate on goodwill. A 0.93% increase in the pre-tax discount rate for the Reynolds American CGU would have a negative impact of £13.3 billion, while a 0.85% decrease in the long-term growth rate would have a similar impact of £13.0 billion.

However, management calculated a headroom of £11.8 billion before a goodwill impairment is triggered, which means that a 0.93% increase in the discount rate or a 0.85% decrease in the long-term growth rate would trigger an impairment of only £1.5 billion and £1.2 billion, respectively. In order to trigger a goodwill impairment of £25 billion, I estimate the long-term (i.e., after five years) growth rate of RAI's cash flow would therefore have to be around 3.6% lower than previously assumed.

As an aside, this estimate is based on the assumption that management continues to use a five-year discrete discounted cash flow model and a terminal growth rate thereafter. Given that management is now assessing the carrying value and economic life of the U.S. cigarette brands over a 30-year period, the actual growth implied by management's current estimates must be more short-term in nature. However, I expect this difference in assumption to have an insignificant impact on the valuation of BTI stock.

Considering that BTI generated 45% of its 2022 net sales in the U.S., and given the comparatively higher profitability of this market, I believe it is reasonable to estimate that the company generates approximately 50% of its free cash flow from cigarette sales in the U.S., or around £3.7 billion, based on the average free cash flow over the last three years (adjusted for stock-based compensation).

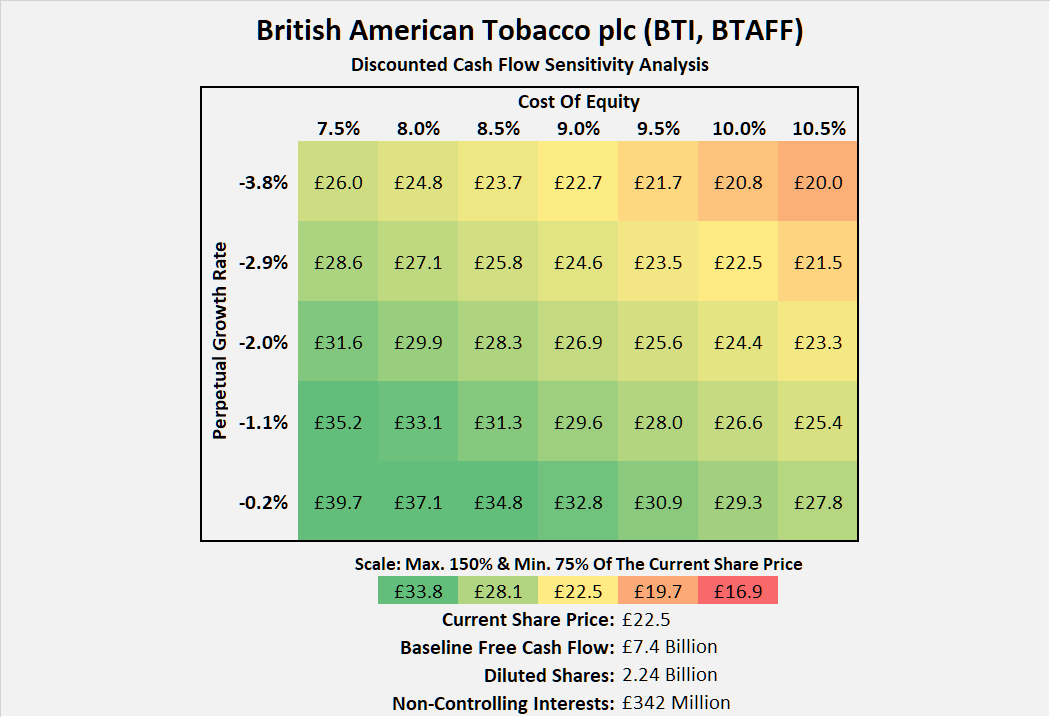

The hypothesized 3.6% reduction in the growth expectation for RAI is therefore roughly equivalent to a 1.8% reduction in the growth expectation for the consolidated free cash flow (ignoring tax implications). If we move up two lines in the discounted cash flow sensitivity analysis shown in Figure 2, we can conclude that the impact on the valuation of the company is likely to be around -14% to -18%, depending on the expected cost of equity (discount rate) and the originally implied perpetual decline rate. Given today's 8% decline, it is therefore reasonable to assume that the market has already priced in a faster decline in free cash flow than management originally expected. This is only reasonable given that a ban on menthol cigarettes is increasingly likely (California has already moved forward with a ban in late 2022 ).

{kind=link}

Figure 2: British American Tobacco p.l.c. (BTI, BTAFF): Discounted cash flow sensitivity analysis (own work, based on company filings)

British American's Hidden Asset And A Big "If"

I clearly do not want to be misunderstood as trying to squeeze the upcoming impairment charge into a positive context. However, I do think that it is nonetheless worth considering BTI's stake in ITC Ltd.

ITC is a major Indian consumer goods, packaging, software, and until recently also hotels conglomerate ). In the 2022 year-end balance sheet, the 29% stake had a book value of £1.9 billion, but was worth more than £12 billion from a fair value perspective (ITC stock price). Over the course of 2023, BTI's stake has appreciated to a value of almost £16 billion.

Of course, it is only reasonable to expect that the £25 billion impairment has been made in accordance with BTI's auditor and as a result of this year's impairment testing and updated expectations for the Reynolds American CGU. However, if (and that's a big if, considering my lack of knowledge of U.K. tax laws) the impending impairment is tax-relevant, it could be used to offset the gain on the potential disposal of BTI's stake in ITC.

Of course, a sale of the stake would help to significantly reduce leverage. Directing all of the proceeds (assuming the impairment is tax deductible) towards debt paydown, BTI's leverage ratio would decline to three times adjusted free cash flow. However, it is also worth considering the potential positive impact of a combination of debt reduction and share buybacks. In this context, I would not rule out Kenneth Dart, the company's largest individual shareholder, having a say in the matter ( see my article on his holding and possible intentions). Of course, we will have to be patient until the publication of the 2023 accounts. Only then will we have clarity on whether the impairment is actually tax relevant and whether British American Tobacco has recognized a tax asset in the process.

Summary And Conclusion

British American Tobacco p.l.c. released its full-year pre-close trading update today and shocked investors by announcing a £25 billion impairment charge in relation to its U.S. cigarettes business. The information provided by management in the press release and prepared remarks was very limited, so in my view it is pointless to engage in seemingly "accurate" calculations and thus fall victim to false precision.

In brief, management believes that the present value of U.S. cigarette brands such as Newport and Camel will be zero after thirty years. Incorporating management's comments in the 2022 annual report, I estimate the impact on the implied perpetual growth rate of U.S. cash flow to be around -3.6 percentage points, or around -1.8 percentage points on consolidated growth, assuming Reynolds American is responsible for 50% of the group's free cash flow. Admittedly, this is a rough approximation, due in part to the neglection of tax effects.

This back-of-the-envelope estimate suggests that the fair value of BTI stock has - theoretically - declined by 14% to 18%, but one should keep in mind that the market was likely already expecting a faster decline than management's previous impairment tests implied. Therefore, I think it is understandable that the actual decline in BTI's share price today was less pronounced than the discounted cash flow sensitivity analysis suggests.

In any case, it will be very important to look closely at management's updated comments on the impairment tests in the upcoming annual report and find out why they have concluded that the assets in the U.S. now have a useful life of 30 years. I don't think the regulatory environment in the U.S. has changed significantly in recent months in relation of the impending menthol ban (the White House even announced a delay in the decision on the ban today) or a nicotine content cap. That said, it is only reasonable to assume that the impairment charge was taken in view of the potentially upcoming menthol ban and the possibly faster than previously expected decline in cigarette volumes. The latter is likely the reason why Altria shares also fell today.

However, with a free cash flow yield of over 14% and a well-covered dividend with a current yield of 10% (see my previous articles for a deep dive into BTI's fundamentals and valuation), I consider British American Tobacco stock to be a compelling value opportunity, despite the likely faster decline in U.S. combustibles volumes than previously estimated. I have added modestly to my already sizable position today, but remain cautious so as not to create concentration risk and will re-evaluate after the publication of the 2023 financial statements.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

British American Tobacco: What To Make Of The £25 Billion Bombshell