VNQ - Broadcom: 3 Reasons Why This Future Aristocrat Is A Must-Have For Dividend Investors

2023-12-26 08:00:00 ET

Summary

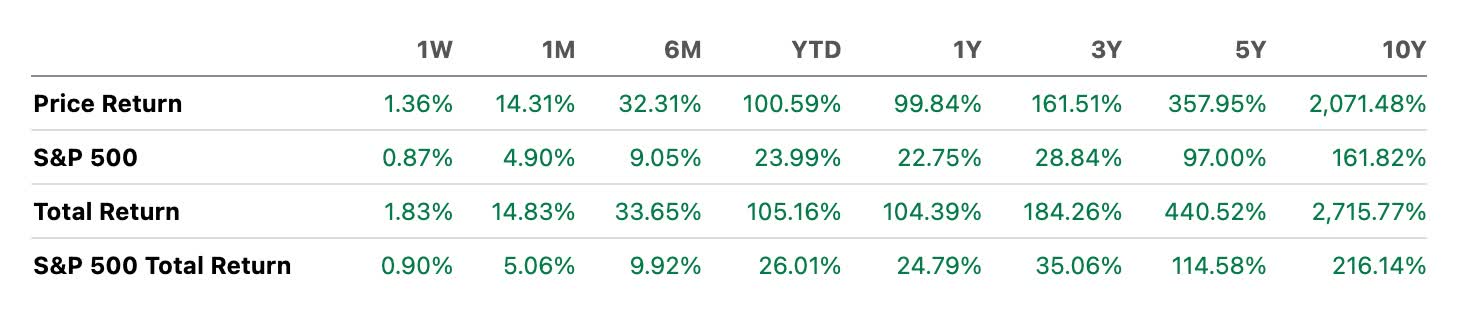

- Broadcom has outperformed the S&P in price & total returns YTD.

- Due to their aggressive share repurchases, growing cash flows, and high dividend growth, the stock is a must-have for long-term dividend investors.

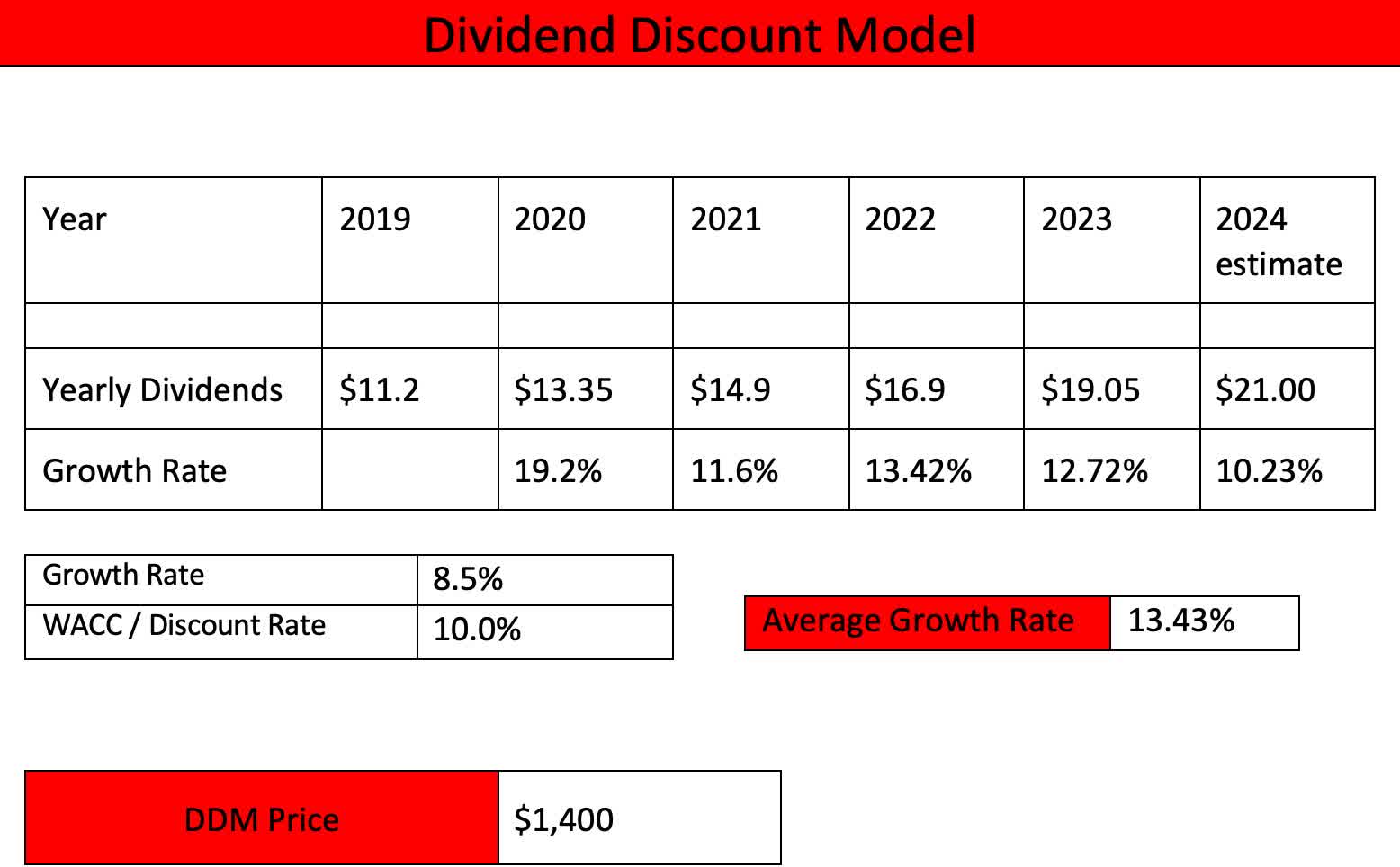

- Using the Dividend Discount Model, I have a price target of $1,400 offering investors more than 25% upside from the current price.

- Due to their run up in price over the last year, one risk the company could have is a decline in price. Another risk is a slowing economy which is expected in 2024.

- Broadcom is expected to grow earnings & revenue by double-digits over the next 3 years.

Introduction

As a dividend investor, I try to constantly balance my portfolio between yield and growth. Supplementing my income in retirement is the main goal but getting some capital appreciation with my holdings also factors into my strategy. Sometimes investing in certain stocks/sectors can cause you to give up one or the other while some stocks/sectors can give you both. As my readers may know I'm an avid REIT ( VNQ ) and BDC ( BIZD ) investor because of the stable income they provide. They can give investors some capital appreciation as well, especially if you buy them at the right price. They are not known for their significant high dividend growth, but for their low-to-single digit growth over time.

Then there are some stocks that not only give you high dividend growth, but significant capital appreciation as well. One of these is Broadcom ( AVGO ), a specialized company focusing on the design of semiconductors, primarily centered around CMOS and analog lll-V technologies. In this article, I give 3 reasons why this stock is perfect for dividend investors.

Long-Term Outperformance VS The S&P

Broadcom is a global infrastructure technology leader that focuses on technologies that connect our world. They are focused on technology leadership and category-leading semiconductor and infrastructure software solutions. From high-performance connectivity at our jobs & homes to the wireless (connectivity) in our automobiles, the company has a hand in connecting everything we do or use in our lives. And the company continues to be a heritage of innovation. Despite the volatility in the stock market during the year, AVGO has performed exceptionally well over this period. In the chart below you can see the company notably outperformed the S&P over the same period and beyond.

{kind=link}

As a buy-and-hold investor I like to look at a minimum of 5 years of data when looking to invest in a company/business. This usually gives you a good story of the management/company's quality. Additionally, looking further back can also give you a look at how a company did during turbulent times. The Dot-com bust, Great Financial Crisis, COVID, or even the high-interest rates in the early 80's all are data points I examine/reference. But depending on the company and how long they've been around, you may not be able to assess how they performed during those times. But even with a few years of data, you should be able to get a decent picture.

And looking at how AVGO outperformed the S&P 500 in both price & total returns gives you a clear picture into their quality. Investing in the technology sector can usually garner some nice returns for an investor and this is the reason why a lot of stocks in the sector usually trade at high premiums. Here you can see AVGO's price increase % from the beginning of the year until now.

Despite inflation, rising interest rates, recession threats, tighter consumer spending, and surging credit card debt, all have which impacted the economy and several high-quality businesses, Broadcom has continued to outperform in the face of this downturn. And this high growth is expected to continue over the next several years.

Robust Double-Digit Future Growth

In addition to the company's strong outperformance over a 3, 5, and 10-year period, Broadcom is expected to continue growing revenue & earnings at a high rate over the next two years. One way I think the company will sustain this is with share repurchases. With the VMware Inc. ( VMW ) deal closed, the company has resumed repurchasing shares and still had $7.2 billion remaining on the current program. Furthermore, in 2023 they brought in record revenue of $35.8 billion, representing a 8% growth rate year-over-year. Net income was also up 22.5% year-over-year from nearly $11.5 billion to roughly $14 billion.

During Q4 management stated this was driven by semiconductor & infrastructure software revenue being up 9% and 3% respectively year-over-year. In the chart below, you can see AVGO is expected to grow both earnings & revenue by double-digits next year and in 2025. Revenue growth is expected to slow from '25 to '26, but still grow by more than 7%. So, the impressive growth trend is expected to continue and the company shows no signs of slowing down in the foreseeable future.

{kind=link}

High Dividend Growth & Safety

Since deciding to pay a dividend in 2011, AVGO has impressively raised the dividend for 13 years making them a contender. They also recently raised the dividend by more than 14% for an annual payout of $21.00. Even during COVID they managed to raise the dividend by double-digits when several businesses were forced to pause or cut. And management stated they expect to pay this dividend of $5.25 a share throughout 2024, pending the Board's approval.

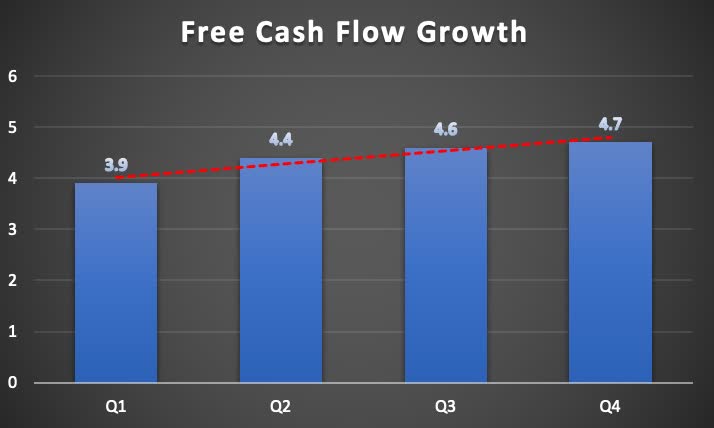

Furthermore, the dividend is well-supported by the company's cash flows. In the chart below you can see free cash flow grew double-digits as well, from $3.9 billion in Q1 to $4.7 billion in Q4. In total, the semiconductor paid out $7.6 billion in dividends which gives them a very comfortable payout ratio of 43% insinuating they have plenty of room for further increases. And with the company's strong business model and management team, I see them joining the prestigious list of Dividend Aristocrats in the next 12 years.

{kind=link}

Valuation

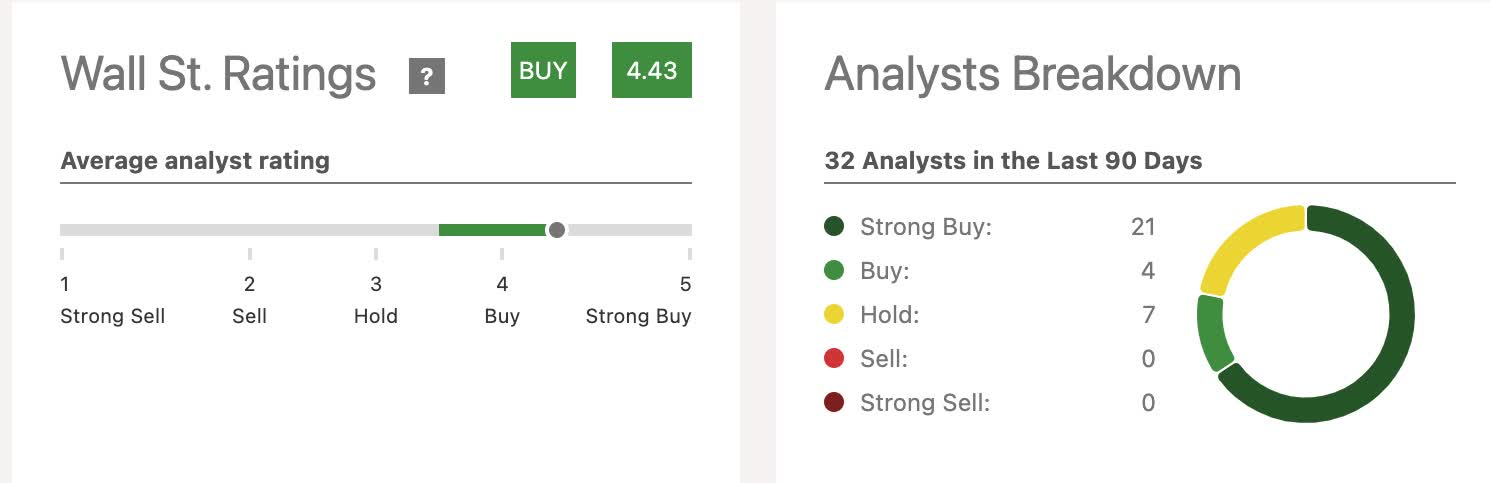

Seeing how the stock has outperformed the broader market, it's no surprise that it is considered overvalued. But despite this, Wall Street analysts still have the stock rated a buy. Currently, the stock is down more than $10 at the time of writing to $1,115 a share but still trades near its 52-week high. With a 52-week low of $542, I think it's safe to say investors will likely not see that price again.

{kind=link}

Using the Dividend Discount Model, I have a future price of $1,400 a share for the company. Seeing their high-growth supported by a strong business model, I think the stock price will continue to soar in 2024. I also used a higher WACC due to the sector and growth rate over the past 5 years. And as most of my readers know I like to be a bit more conservative to manage expectations. This gives investors more than 25% upside from the current price target.

{kind=link}

Risk Factors

A risk the company faces is the potential downside from the current price. Seeing as how the stock has rallied over this last year and the rich valuation, the stock could see a correction to its price. Using the average price target of $1,069 this could be a potential risk. But just as the company faces the risk of a price decline, the stock could soar higher. I do expect the price to experience some volatility but to still outperform over the long-term.

For investors who typically trade in and out of stocks, you could definitely see some downside here. But for those with a buy-and-hold mentality I think the stock is a buy. Another risk could be a potential slowdown in the economy which is expected in 2024. And despite the strong growth over the year, broadband revenue did decline by 9% in the fourth quarter year-on-year. And management expects this to continue into 2024 as cyclical weakness at service providers late this year is projected to continue going forward.

Bottom Line

Broadcom has performed exceptionally well this year, outperforming the S&P by sizable margins in both price & total returns. The company seems to be doing all the right things which I think makes them a Dividend Aristocrat in the making. Growing cash flows, share repurchases, and superior price & total returns against the broader market. All these along with the strong business model will continue to reward investors for the long-term. Furthermore, they have one of the best dividend growth rates in the sector with double-digit growth over the past 5 years. Although the company does face some risks going forward, I think due to the strong cash flows, 13 years of growing the dividend, and strong business model, the stock is a buy and must-have for long-term dividend investors.

For further details see:

Broadcom: 3 Reasons Why This Future Aristocrat Is A Must-Have For Dividend Investors