AVGO - Broadcom: I Am Increasingly Bullish On This Company (Rating Upgrade)

2023-09-05 11:29:46 ET

Summary

- Broadcom Inc.'s Q3 results beat expectations, showing positive growth driven by AI exposure and infrastructure spending by hyperscalers.

- The company's margin profile remains strong, with impressive cost flexibility and resilient semiconductor and software segments.

- The pending acquisition of VMware and the Apple licensing deal further improve Broadcom's risk-reward profile, allowing for a higher valuation multiple.

- The impact of AI and the company's improved resilience lead to an improved medium-term growth projection.

- While the balance sheet is far from pretty, Broadcom's cash generation ability partly offsets this risk. I view the debt load as manageable.

Investment thesis

I upgrade my rating on Broadcom Inc. ( AVGO ) from a Hold to a Buy following its fiscal Q3 results , which beat the consensus and showed that Broadcom is able to keep reporting positive growth, in part fueled by its AI exposure.

My investment thesis for Broadcom has mostly stayed the same. I remain enthusiastic about the company and its fundamentals. The last two quarterly reports have highlighted that the company is seeing material improvements in its growth outlook due to infrastructure spending by hyperscalers, boosting my growth expectations. Furthermore, the VMware ( VMW ) deal is increasingly likely to be completed before October 30, which should remove another overhang on the share price.

Overall, the risk profile has improved over the last few months, further improving the attractiveness of Broadcom shares. This is what I previously wrote about the company:

The networking product segment, particularly in the AI space, presents significant opportunities for Broadcom, with projected growth and increasing demand from hyperscalers. In fact, I believe Broadcom is one of the most underestimated beneficiaries of the AI boom. Furthermore, the company's focus on networking semiconductors, strong gross margins, and the introduction of AI-specific chips position it favorably in the market. Also, Broadcom's software offerings and the pending VMware, Inc. acquisition provide diversification and stability to the business. Finally, the recently announced Apple Inc. ( AAPL ) licensing deal also removes a key overhang and improves the risk-reward profile.

Overall, with solid financials, a favorable position in the AI market, and ongoing diversification efforts, Broadcom is well-positioned for long-term growth. Add a solid dividend yield of above 2%, strong dividend growth, and the fact that this company is a free cash flow ("FCF") machine with an FCF margin approaching 50%, and we get a very attractive investment proposition.

In this article, I will take you through the latest developments and update my estimates and view on the company accordingly.

Broadcom’s Q3 results show resiliency and a strong margin profile

I rated Broadcom a hold prior to its Q2 results a couple of months ago as the incredible share price performance in the previous six months made me more cautious. Even more so as I saw only a 5% upside to my price target. Since that article, Broadcom shares have indeed underperformed the SP 500 (SP500) by around 240 basis points despite two very solid quarterly financial reports.

The latest was its fiscal Q3 results , which it reported last week, and these really offered very few surprises. Broadcom reported revenue of $8.88 billion, up 5% YoY and sitting roughly in line with the Wall Street consensus and my own expectations.

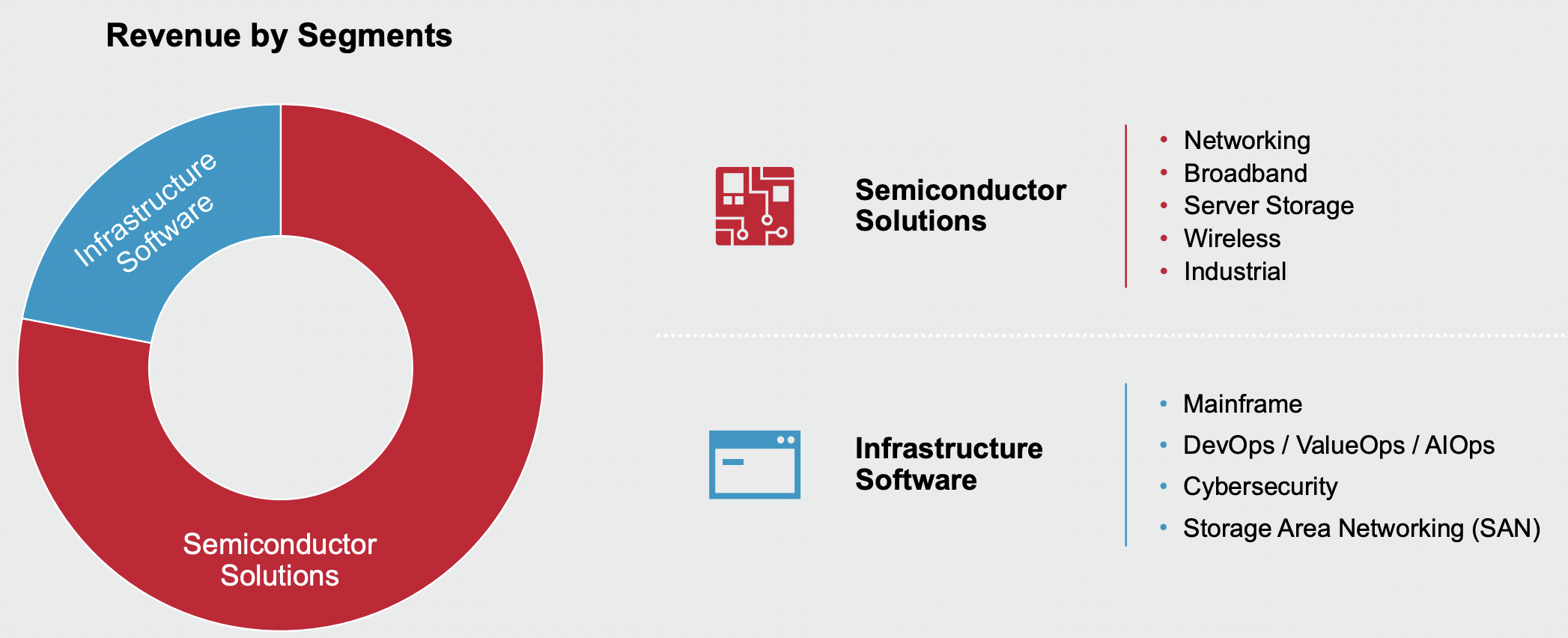

Growth was driven by both the semiconductor and infrastructure software segments, both up 5% YoY. However, the performance of the semiconductor segment, in particular, was quite impressive and much better than what analysts projected.

Broadcom continued to see strong resilience in the semiconductor part of the business as demand for its products remains higher than we can see for the overall industry, in which many companies and Broadcom peers have been reporting negative growth rates over the last year. In fact, none of its semiconductor segments reported significant declines YoY and revenue growth in its software operations accelerated.

Moving to the bottom line, Broadcom continues to report incredible margins without any form of weakness visible despite a slowdown in top-line growth. Broadcom’s margin profile sits comfortably above the peer and industry averages by about 40%, which is quite impressive.

The company is showing excellent cost flexibility as it was able to bring down operating expenses by 8% YoY. However, I am less keen on the fact that the company lowered its R&D investments by 8% YoY. I prefer semiconductor companies to keep R&D investments high to maintain their technological lead at the cost of short-term margins. Broadcom chooses a different strategy here to preserve margins and cash flows. While this is not my preferred strategy, I have confidence in CEO Hock Tan to ensure the company maintains its leadership, so I am not overly concerned.

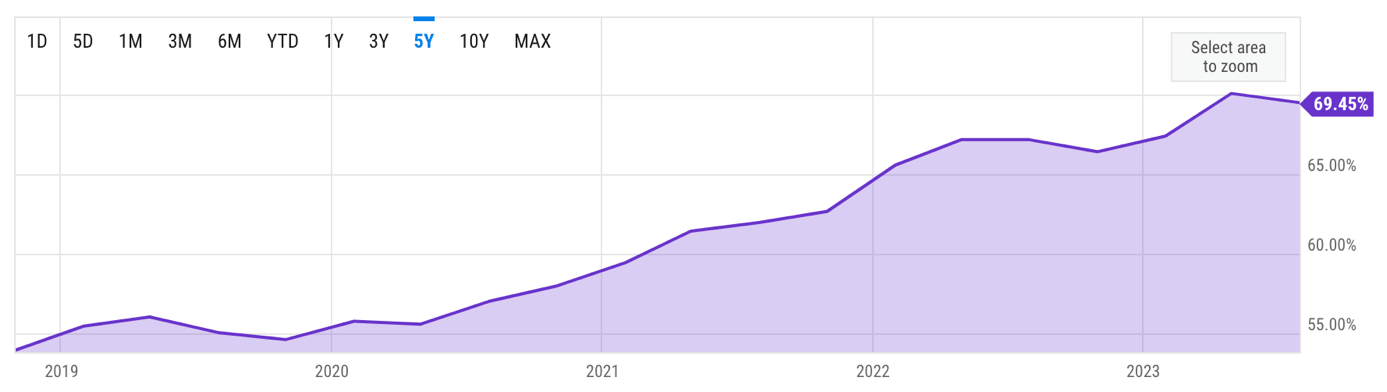

On a more positive note, as a result of these cost savings, the Q3 gross margin ((GAAP)) expanded by 230 basis points YoY to 69.4% (non-GAAP gross margin of 75.1%, down 80 basis points), continuing the uptrend the margins have been in over the last several years despite the economic and demand challenges. Broadcom has always been able to maintain an impressive margin profile, but it is now showing that it can maintain this even as top-line growth slows.

{kind=link}

{kind=link}

From a non-GAAP perspective, the semiconductor segment gross margin was down 160 basis points to 70%, driving the non-GAAP decline in gross margin due to a less favorable product mix. Meanwhile, the gross margin in the software business remained impressive at an industry-leading 92%.

This resulted in a non-GAAP operating income of $5.5 billion, up 6% YoY and representing an operating income margin of 62%, up 100 basis points YoY. EPS of $10.54 beat the consensus by $0.11 and was up 8.3% YoY.

The Q3 free cash flow margin also once more improved YoY by 200 basis points to 52% or $4.6 billion. Broadcom’s ability to turn revenue into free cash flow ("FCF") remains incredible. It is the leading reason I am not overly worried about the significant net debt position of the company, amounting to $27.2 billion.

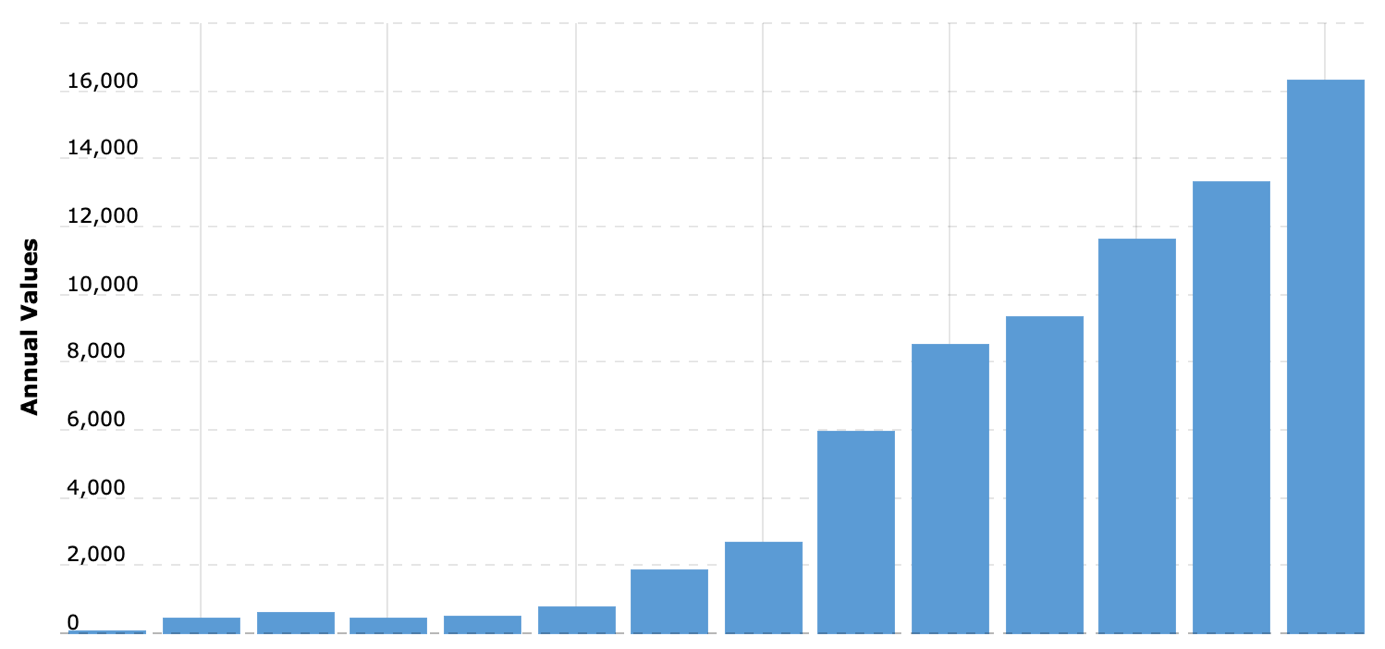

Broadcom has grown its free cash flow rapidly, with the YoY growth only falling below 10% in a single year in the last ten years. The company generated $16.3 billion in FCF in 2022 and is well underway to beat this record high in 2023.

{kind=link}

Yes, acquiring VMware will increase the debt position further, but Broadcom has shown in the past that it has an incredible ability to integrate new businesses and turn these into cash-generating machines. From the start, VMware will add another $4 billion in FCF to the total, while synergies and structural business improvements should allow Broadcom to massively expand the declining margins from VMware in the first couple of years. Looking at Hock Tan’s track record, I believe investors have no reason to doubt the viability and potential of this acquisition.

{kind=link}

I remain very positive about Broadcom’s bottom line and see few negatives. The debt position is far from positive but manageable in my eyes. I believe acquiring VMware will significantly increase the company’s cash flow potential. Investors should not get scared away by the debt load and should focus on the bigger picture, including the margin improvement potential and synergies.

Finally, the company’s cash generation abilities and solid cash position also allow it to keep returning cash to shareholders through dividends and share repurchases. In Q3, the company returned $1.9 billion, primarily through $1.7 billion in share repurchases. However, I expect these repurchases to slow down over the next few years, as the VMware acquisition will shift the capital allocation focus to paying down debt.

However, this should not worry investors, as the current dividend yield of 2.11% is nothing to complain about either. Broadcom has been growing the dividend for 12 straight years now and I expect it to keep growing, albeit at a slower pace compared to the 5-year growth rate of 23%. High-single digits to low-teens seem more likely in the years ahead. Still, with a payout ratio of just 44%, the dividend is well covered and should be sustainable.

The impact of generative AI is becoming more significant on Broadcom’s financials

The reason for this outperformance by Broadcom last quarter and the strong overall performance of the semiconductor segment was largely the result of the increased spending by cloud service providers, which drove a strong outperformance in Broadcom’s hyperscaler business and networking segment.

The latest quarterly report from Nvidia has perfectly shown that the AI hype is now actually resulting in material financial results. Nvidia is reporting incredible growth in its datacenter segment as hyperscalers are rapidly building capacity to run AI programs. AI is no longer a hype but is becoming the future of technology. This also benefits Broadcom as the company is a crucial supplier of networking semiconductors used by these hyperscalers. This is what I wrote in my last article on Broadcom regarding the company’s exposure to AI:

Simply put, networking semiconductors are crucial for AI applications as they enable the fast and efficient communication that is necessary for processing large amounts of data quickly and accurately. In reality, without top-performance networking solutions, AI models with billions of parameters would not be able to work. And still, current advanced AI systems are limited by the available bandwidth.

As a result, the company’s networking segment continues to report impressive growth in Q3, driven by the scaling out of AI clusters among the hyperscalers, which drove demand for the company’s switches, routers, and custom silicon AI engines. This is supported by the company’s early focus on AI-specific networking products like the Jericho3-AI chip. Illustrating the significance of these products and Broadcom’s leading position, this is what I wrote previously:

According to Broadcom, the chip is capable of bringing together 32,000 GPUs while bringing down the completion time frame by 10%, allowing AI accelerators to run 10% more efficiently compared to any alternative. Without getting too much into the technical details, Microsoft Corporation ( MSFT ) is currently running its GPT training runs using older systems with half the speed offered by this new Broadcom chip, making switching to this system very attractive for Microsoft.

Broadcom is not even shipping these new AI-specific products yet but has already reported substantial orders and plans to start shipping these products over the next 6 months. This should support continued growth in networking, especially as the company is looking strong technologically versus competitors.

Networking revenues grew 20% YoY in Q3, in line with my earlier predictions for the segment to maintain a growth rate of above 20% for the foreseeable future and a potential acceleration in FY24. Management even guides for growth to accelerate in Q4 already. This growth is easily supported by the AI wave, massive investments made by hyperscalers, and the above-mentioned new products. Management even guides for 50% sequential growth and 2x YoY in generative AI-related revenue in Q4.

Q3 networking revenue was $2.8 billion, now accounting for 40% of semiconductor revenues and beginning to become a larger share of Broadcom’s overall revenues. Again, a trend I expect to persist. AI, through the company’s networking products, should become a more meaningful and stable growth driver in the medium term as the company is well positioned from a technological perspective.

As stated before, I believe the networking segment will continue to grow at a rate of above 20% in the medium term, with this accelerating towards 25-30% in Q4 and into FY24.

Long story short, AI is starting to drive significant revenues for the company, and its technological lead in AI-specific networking solutions will boost its revenue and growth potential.

Excluding the impact of AI, the semiconductor segment shows resilience, while growth in software accelerates

And there is more in the semiconductor business of Broadcom to be excited about when looking at the Q3 results. The overall important term is resilience. While when excluding the impact of AI, Broadcom’s semiconductor revenue was flat YoY, causing little excitement, it is also showing a stabilization.

Looking at the different semiconductor segments, none reported any significant revenue declines YoY as most reported flat growth. This resilience in a challenging operating environment is a testimony to Broadcom’s strength compared to peers and its deep partnerships with customers.

Enterprise and telco end-market spending moderated in Q3, impacting Broadcom’s performance. However, the wireless segment continued to report flat YoY growth, which is truly impressive when considering the significant slowdown we have seen in technology hardware sales worldwide.

{kind=link}

Overall, Broadcom’s semiconductor segment remains in excellent health and continues to perform roughly in line with my expectations, which definitely is a positive when considering the challenging operating environment. Broadcom deserves some credit for navigating this exceptionally well and is showing that demand for its products makes the company less cyclical compared to the semiconductor industry as a whole. The company continues to see a soft landing this fiscal year and expects growth to return by the start of its FY24.

Further supporting the company’s counter-cyclical performance is the software segment of the company. Software revenue in Q3 was $1.9 billion, up 5% YoY and now accounting for 22% of total revenue. The growth rate showed a decent improvement from Q1 when the company reported a 1% software revenue decline and Broadcom expects this trend to persist over the next couple of quarters with YoY growth accelerating further as the demand environment improves.

{kind=link}

The software part of the business creates a form of stability for Broadcom, highlighted by the fact that 90% of renewal value in Q3 came from recurring subscriptions and maintenance. As a result, this business is much stickier, and as it grows to become a larger part of the business (especially after the completion of the VMWare deal), it should become a crucial cash flow machine for Broadcom, in part due to the incredible margins of the software business, even when the operating environment deteriorates. Furthermore, a Q3 renewal rate of 117% for core software products is also very decent.

VMware and Apple

I have already mentioned VMware several times throughout this article, and this is because the acquisition is increasingly likely to be closed before the end of October. Together with the Apple licensing deal, the potential acquisition has been a leading factor impacting the share price and valuation over the last year or so.

Broadcom now expects to receive regulatory approval before October 30. This is what management said regarding the regulatory approval during the earnings call :

We have received legal merger clearance in Australia, Brazil, Canada, the European Union, Israel, South Africa, Taiwan, and the United Kingdom and foreign investment control clearance in all necessary jurisdictions. In the US, the Hart-Scott-Rodino pre-merger waiting periods have expired, and there is no legal impediment to closing under US merger regulations.

Today, the two largest hurdles seem to be approval from China and the U.S., although I do not see any major issues that could jeopardize the deal. The recent clearance by the European Union and the UK were crucial and has solidified my belief that this acquisition should be completed in this fiscal year.

The acquisition of VMware will meaningfully grow Broadcom’s software business to slightly over 40% of total revenue, improving its revenue stability and more importantly, massively improving its software offering. I have explained in earlier articles that I am not impressed by Broadcom’s current software offering. Whereas the company is a leader in certain semiconductor areas like networking and broadband, its software offerings seem to be superior to many software peers, which does not make an interesting investment case.

However, I do quite like VMware’s virtualization and cloud computing products, which in fact are industry-leading, highlighted by its 45% market share in the virtualization market. Therefore, I expect this to meaningfully strengthen Broadcom’s infrastructure software offering. Also, the acquisition gives Broadcom access to a large and loyal customer base, giving it excellent cross-sell opportunities and room for synergies. The potential for Broadcom through this deal should not be underestimated, and I believe it will nicely fit the conglomerate.

Finally, as the new Apple licensing deal announced earlier this year is crucial in the Broadcom investment case as this has long been a drag on its awarded valuation multiple due to the revenue risk, I will quickly repeat a part of my previous article below for those who missed it:

On May 23, Broadcom and Apple announced a new multiyear, multibillion-dollar agreement. The current licensing agreement was set to expire in July, so it was a matter of time for this news to come out as Apple was not ready yet to replace these Broadcom components with in-house manufactured alternatives.

Most importantly, the deal means Apple will not replace Broadcom components before 2027, removing a key overhang for the stock as Apple is responsible for a little under 20% of Broadcom revenues. This percentage has been trending down over recent years with other segments growing faster and Broadcom diversifying the business by acquiring software companies. Therefore, the impact of losing Apple as a customer by 2027 will most likely be no more than 3-4% of FY27 EPS.

Outlook & AVGO stock valuation

Broadcom has guided for Q4 revenue of $9.27 billion, up 4% YoY. This should be driven by low-to-mid-single digit growth in semiconductor revenue and infrastructure software revenue to be up mid-single digits YoY. This guidance perfectly aligns with the expectations from analysts before the earnings release and is slightly above my own projections.

Management does expect the gross margin to decline further in Q4, driven by an unfavorable product mix. This should result in a gross margin of around 74.3% (Non-GAAP).

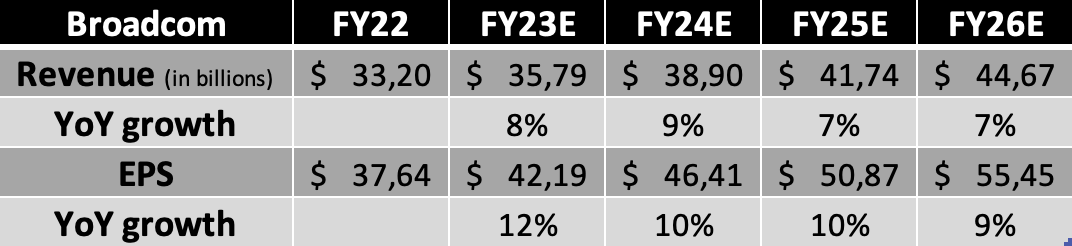

Following the company’s fiscal Q3 earnings report, business updates, and its guidance for Q4, I now expect the following financial results through FY26.

{kind=link}

(This includes Q4 revenue of $9.27 billion and EPS of $11.)

The last two quarterly reports have revealed two critical factors: 1) The remarkable resiliency of the company, which should become even more pronounced once the VMware acquisition is completed, and 2) the fact that AI is not a hype but a reality that results in a growth boost for those with exposure to it. These factors have contributed to my improved outlook for Broadcom in the medium term. I have boosted my revenue and EPS growth expectations from FY24 onward and the strong performance in the last two quarters has also resulted in an upgraded FY23 EPS expectation.

I continue to see a solid growth outlook for Broadcom, boosted by AI. In addition, I believe there is still more room for margin improvements, especially as the demand environment improves over the next year. This should lead to even faster growth in EPS at around the 10% mark.

As for the valuation, whereas I have previously chosen to go with a lower valuation multiple due to a number of factors, I believe the risk profile has improved, in part due to a new licensing deal with Apple, a high probability of the VMWare acquisition being cleared by regulators, and an improved long-term growth expectation. As a result, it is unfair to compare the valuation to its historical averages, which indicate the company is valued at a significant premium of around 30-40% when looking at different valuation metrics. Investors should not forget that the risk profile has changed dramatically, and the company is seeing new growth drivers.

Therefore, I increase my fair P/E estimate to 21x. The company has a very solid growth outlook and while the debt load is a little high for my taste, the company’s cash flows are excellent, which makes me confident that it should be able to pay down this debt over the next few years, while sustainably growing the dividend, which is another factor contributing to the attractiveness of this stock.

The market has long discounted Broadcom, but with the risk profile now improved, I see significant potential for this company over the next couple of years. Therefore, based on a P/E multiple of 21x and my FY24 EPS estimate, I increase my target price from $861 to $975.

Going with an annual return of 10% (12% when including the dividend), I believe a current fair value sits at around $865 per share, meaning shares are currently trading around fair value.

Conclusion

I maintain my bullish stance toward Broadcom, as I like the company’s technological lead in several semiconductor end markets, its exposure to infrastructure software, its remarkable management team, and its long-term prospects boosted by AI.

Overall, my thesis remains essentially unchanged, and I remain of the opinion that Broadcom is a must-own company at the right price. Today, I believe the risk-reward profile is attractive enough to warrant a buy rating as shares are trading around fair value and should offer very solid long-term returns at a current price of around $870, based on my current growth outlook.

Therefore, I upgrade my rating on Broadcom to a Buy (from a hold).

For further details see:

Broadcom: I Am Increasingly Bullish On This Company (Rating Upgrade)