AVGO - Broadcom: Still Hold-Rated - 'Soft-Landing' Underway

2023-09-03 08:49:51 ET

Summary

- We remain hold-rated on Broadcom.

- Management is now talking about a soft landing in its business and guided conservatively for its October quarter.

- The company outlook now reflects our cautious view about customers' inventory correction and capex spending optimization.

- We still believe AVGO’s cloud A.I. growth will be offset by weaker demand for traditional cloud compute, communications service providers’ inventory correction, and weaker demand in the enterprise market.

- We expect financial performance to moderate further into 1H24; thus, we recommend investors remain on the sidelines.

We continue to be hold-rated on Broadcom ( AVGO ) after Q3'23 earnings results. Management has now confirmed the soft landing in its business and guided lower than consensus for Q4'23; current-quarter revenue is estimated to be $9.27B versus consensus at $9.28B. We think the Q3'23 earnings results and outlook confirm our negative thesis of a growth rate slowdown in FY23 due to inventory correction cycles and weaker capex spending. This quarter , sales grew 2% QoQ and 5% Y/Y to $8.9B, relatively in line with consensus. AVGO's semiconductor business, which accounts for 78% of total sales, grew only 2% QoQ to $6.94B, largely driven by stronger wireless demand, with management noting semiconductor sales would be flat without A.I.-related sales. We think this reflects our cautious view about customers' inventory correction and capex spending optimization impacting sales.

The stock is up 8% since our downgrade to hold in early June, outperforming the S&P 500 slightly by 3%. The stock slipped 6% yesterday in response to yesterday's guidance; we continue to recommend investors remain on the sidelines as we expect financial performance to moderate further into 1H24.

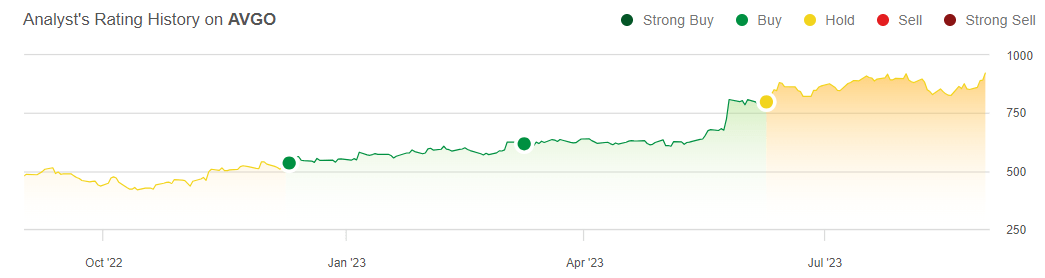

The following graph outlines our rating history on AVGO.

{kind=link}

A.I. growth offset by "soft landing"

While AVGO continues to push the A.I. growth narrative, management has confirmed the soft landing environment; CEO Hock Tan noted on the earnings call yesterday, "Without the benefit of generative AI revenue in Q3, our semiconductor business was approximately flat year-on-year," signaling weaker capex spending and inventory corrections. Management now expects quarterly semiconductor revenue, excluding A.I., to stabilize at $6B and A.I. spend to represent +25% of semiconductor revenues in FY24, but visibility past 2024 remains unclear.

We think the market is too optimistic about AVGO's A.I. growth potential in the current macro environment, and management's lower guidance for next quarter put into perspective that gen A.I. tailwinds cannot drive higher guidance in 2H23. Networking, where management noted a significant impact from gen A.I. demand, grew to $2.8B, up 4.5% QoQ and over 20% Y/Y; networking accounts for roughly 40% of semiconductor revenue. We think the strength of cloud A.I. demand in networking was offset by demand weakness in enterprise and Telecom markets. We continue to see a trend of A.I. growth being offset by either demand weakness or inventory corrections in the back half of the year.

Management achieved low single-digit sequential growth in end-markets and declines in broadband and industrial-related business sales; the results, combined with the outlook for next quarter, confirm that AVGO won't live up to expectations of being one of the biggest beneficiaries of the A.I. boom behind Nvidia ( NVDA ). AVGO's exposure to sluggish end-market demand, including smartphones, telecoms, and non-A.I. server segments, is weighing on growth. The discrepancy between NVDA's guidance and revenue beat earlier this month versus AVGO's results and outlook puts into perspective where the bulk of cloud capex dollars spent is going: NVDA. We expect the uncertain macro environment combined with the increased industry adoption of A.I. servers to cannibalize capex dollars from traditional computing hardware, negatively impacting AVGO in 2H23. Furthermore, we think AVGO's ethernet offerings will face higher competition from NVDA's InfiniBand.

The following graph outlines AVGO's YTD performance against NVDA and Marvell ( MRVL ), highlighting the real A.I. growth versus market-hyped A.I. growth.

YCharts

Additionally, while we're constructive on the pending VMware ( VMW ) deal and expect it to provide a competitive advantage in the cloud, we don't expect to see tailwinds materialize into meaningful growth in the near-term given the cost-cautious environment and limited capex spending.

Valuation

AVGO is not cheap. The stock is trading at 11.3 EV/C2023 Sales versus the peer group average of 5.9x. On a P/E basis, the stock is trading at 20.4x C2023 EPS $42.50 compared to the peer group average at 30.3x. We don't see attractive entry points into the stock at current levels.

The following chart outlines AVGO's valuation against the peer group.

TSP

Word on Wall Street

Wall Street doesn't share our bearish sentiment on the stock despite management owning up to the soft landing on the earnings call. Of the 27 analysts covering the stock, 22 are buy-rated, four are hold-rated, and the remaining are sell-rated. Management and investors continue to be confident about AVGO's growth potential in the A.I. market. We think this confidence is misplaced as we think most capex dollars spent will continue to favor NVDA in the A.I. market over AVGO and other players.

The stock is currently priced at $872 per share. The median sell-side price target is $950, while the mean is $942, with a potential 8-9% upside.

The following charts outline AVGO's sell-side ratings and price-targets.

TSP

What to do with the stock

We remain hold-rated on AVGO; Q3'23 results and outlook confirmed our concerns over the uncertain macro environment weighing on financial performance in 2H23. AVGO rallied up 57% YTD, outperforming the S&P 500 by 38%, alongside MRVL on investor confidence in A.I. growth potential. We think the market is now waking up to the reality that AVGO's cloud A.I. growth will be offset by weaker demand for traditional cloud compute and enterprise weakness coupled with inventory corrections in communications service providers. We don't see a favorable risk-reward profile for the stock yet; we recommend investors stay on the sidelines for the near-term.

For further details see:

Broadcom: Still Hold-Rated - 'Soft-Landing' Underway