VMW - Broadcom: The Beauty Within - And VMware Will Add To It

2023-09-06 07:46:19 ET

Summary

- Investors appeared to have misunderstood Broadcom's long-term strategy and were disappointed by the lack of an "AI boost" in Q3 results.

- Broadcom's investment thesis is focused on generating strong free cash flow for dividend growth, share buybacks, and strategic acquisitions.

- Despite moderate revenue growth, Broadcom delivered strong free cash flow and growth in FCF/share, aided by share buybacks.

- Broadcom trades at par with the S&P500 on a TTM and forward P/E basis, yet its free cash flow margin is ~3x that of the S&P500. AVGO is a BUY.

If the reaction to Broadcom's (AVGO) Q3 earnings report is any indication, many investors (and professional money managers) still don't understand the company's long-term strategy and its primary investment thesis. As a result, they appear to have been expecting a significant "AI boost" to Q3 results (and Q4) and, apparently, were disappointed when it did not live up to their lofty expectations. Newsflash: Broadcom is not Nvidia (NVDA). There is no other Nvidia. Nvidia dominates the AI-centric high-performance-computer ("HPC") market (at least for now ...), and also has a broad suite of AI software tools to complement its HPC hardware. It's actually very similar to Broadcom's dominance of the global high-speed networking market, in which it too has a strong software development platform. However, to have expected Broadcom's quarterly revenue growth to be anywhere near Nvidia's was simply misguided. Meantime, Broadcom continued to be really good at what it does: delivering strong free cash flow and growth in FCF/share. Let me explain.

Investment Thesis

The investment thesis in Broadcom is relatively straight-forward: it is a high-margin enterprise that generates strong free cash flow to fund excellent dividend growth, share buybacks, and the opportunity to grow through strategic acquisitions - like the pending VMware (VMW) acquisition (more on that deal later).

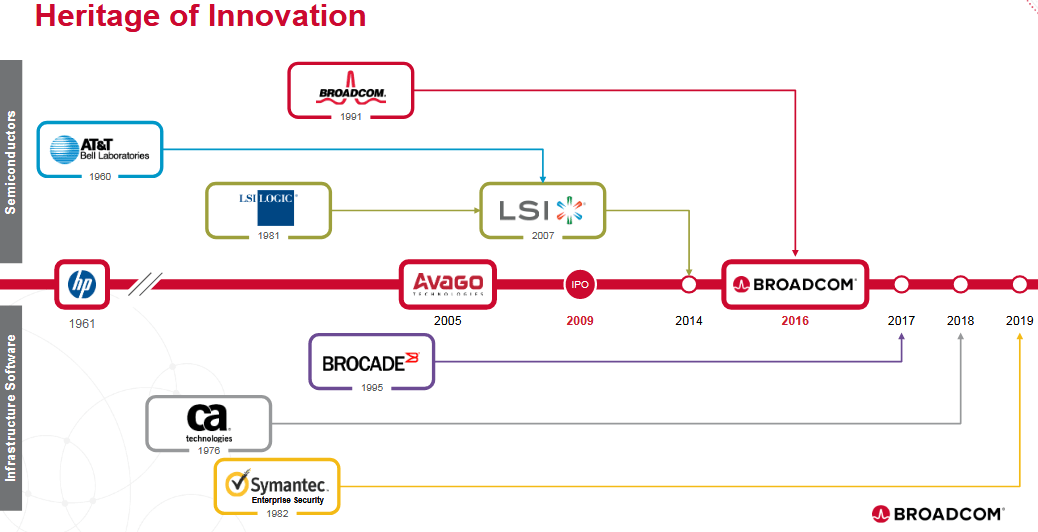

As a recent slide in the August Investor Presentation shows, Broadcom CEO Hock Tan has a proven track-record when it comes to making strategic acquisitions and ringing out strong margins:

{kind=link}

In the early years, the acquisitions were primarily semiconductor companies (i.e. LSI & Broadcom, shown on top of the red-line in the above graphic). But in 2017 Hock Tan pivoted to scooping up enterprise software companies Brocade, CA Technologies, and Symantec (below the red-line in the above graphic). For each of these major acquisitions, there were investment community concerns about Broadcom's strategy, its debt, etc. So let's take a look at Broadcom's most recent earnings report to see how this strategy has been working (and working very well).

Free Cash Flow

Though many (and perhaps relatively new ...) Broadcom investors appear to have been disappointed by Broadcom's Q3 report last week, I was certainly not one of them. The company delivered pretty much what I expected: continued strong performance of moderate revenue growth that delivered strong free cash flow, and - perhaps more importantly - growth in FCF/share. Let's take a look at the yoy comparisons:

| Q3FY23 |

| Q3FY22 |

| Growth yoy |

| Revenue |

| $8.876 billion |

| $8.464 billion |

| 4.9% |

| Free Cash Flow |

| $4.60 |

| $4.31 billion |

| 6.7% |

| Free Cash Flow Margin |

| 51.8% |

| 51.0% |

| 0.8 percentage pts |

| Free Cash Flow/Share |

| $10.77 |

| $9.89 |

| 8.9% |

The important thing to notice here is that while Q3 revenue grew only 4.9% yoy, free cash flow grew by 6.7% .

Share Buybacks

In addition, due to Broadcom's meaningful stock buyback plan, the average fully-diluted share count was reduced by an estimated 9 million shares yoy. And that was despite the mandatory conversion of Convertible Preferred Stock into AVGO common stock during the fiscal quarter ended October 30, 2022. As shown in the table above, and helped by the reduction in shares outstanding, FCF/share jumped 8.9% yoy . Not bad. Not bad at all.

In Q3, Broadcom bought back 2.9 million shares for $2.167 million. That equates to an average price of an estimated $747.24/share. At pixel time, AVGO shares are currently trading at $877 and change.

Bottom line: Broadcom's share buyback plan is delivering solid returns for ordinary shareholders.

Forward Guidance

On the Q3 conference call , CFO Kristen Spears gave the following guidance for Q4:

Guidance for the fourth quarter of fiscal 2023 is for consolidated revenues of $9.27 billion and adjusted EBITDA of approximately 65% of projected revenue. In Q4, we expect gross margins to be down 80 basis points sequentially on product mix. We note that our guidance for Q4 does not include any contribution from VMware.

If Broadcom hits that guidance (note the company typically under-promises and over-delivers ...), it would be up 3.8% as compared to revenue of $8.93 billion in Q4 of last year. However, the adjusted EBITDA guidance ($6.02 billion), would be +5.2% as compared to the $5.72 billion in Q4 of last year. The point is, in Q4 investors can expect Broadcom will continue to deliver strong FCF and FCF/share growth that is significantly above top-line revenue growth.

The VMware Deal

As you know by now, Broadcom has already received legal merger clearance in Australia, Brazil, Canada, the European Union, Israel, South Africa, Taiwan and the UK. In the US, the Hart-Scott-Rodino pre-merger waiting periods have already expired, so under US merger regulations there is no legal impediment to closing the deal.

That leaves approval by China as the last remaining hurdle. A recent article in Barron's observed that while China failed to approve of the Intel (INTC) takeover of Tower Semiconductor (TSEM), that deal was obviously in the strategic semiconductor sector. The VMware acquisition is in the software sector, wherein China recently approved big mergers - including Microsoft's (MSFT) acquisition of Activision (ATVI). See: Broadcom's VMware Takeover Is Approved by U.K. China Could Be the Last Hurdle.

CEO Hock Tan summed up the current status of the acquisition bid during the previously referenced Q4 conference call:

We continue to work constructively with regulators in a few other jurisdiction and are in the advanced stages of the process towards obtaining the remaining required regulatory approvals, which we believe will be received before October 30th. We continue to expect to close on October 30th, 2023.

Originally valued at $61 billion, the VMware acquisition is obviously a big deal even for a company the size of Broadcom (currently market-cap $360 billion). And while there have been the usual concerns about debt, strategy, etc. - note those are all the same concerns that were voiced over Broadcom's previous software acquisitions as well. Yet on the Q3 conference call, CFO Kristen Spears summarized the infrastructure software segment's results as follows:

Revenue for the infrastructure software segment was $1.9 billion, up (5%) year-on-year and represented 22% of revenue. Gross margins for infrastructure software were 92% in the quarter, and operating expenses were $337 million in the quarter, down 10% year-over-year. Infrastructure software operating margin was 75% in Q3 and operating profit grew 13% year-on-year.

Note, once again, that infrastructure software operating profit grew faster than revenue. And this is what CEO Hock Tan has been able to do time and time again with all of the major M&A deals he has arranged: on-going improvement in efficiency, margin, and free cash flow. The VMware deal will likely be no different.

Speaking of FCF, note an often overlooked attribute of VMware: strong free cash flow generation. TTM free cash flow generation for VMware is as follows:

- Q2FY23: FCF = $350 million

- Q1FY23: FCF = $1.65 billion

- Q4FY22: FCF = $1.51 billion

- Q3FY22: FCF = $1.16 billion

The point here is that VMware has the potential to add an estimated ~$6 billion of incremental annual free cash flow to Broadcom. As a reminder, the original deal announcement of the stock-and-cash transaction included Broadcom assuming an estimated $6 billion of VMware net-debt. At that time, Broadcom was targeting ~$8.5 billion of pro forma EBITDA from the acquisition within three years of closing the deal.

Meanwhile, it is instructive for Broadcom shareholders to take a closer look at VMW's Q2 report released last week: while revenue of $3.41 billion was up only 2% yoy, note that Subscription and SaaS ARR (annual recurring revenue) exiting the quarter was $5.31 billion: +36% yoy. GAAP net income for Q2 was $477 million ($1.10/share), +34% yoy. Clearly, VMW has been getting itself "all cleaned up" in anticipation of the deal closing at the end of next month.

The bottom line here: VMware is a very profitable company that generates strong free cash flow. As a result, the acquisition is ready-made for a CEO like Hock Tan who prioritizes efficiency and shareholder value with M&A deal integration. Longer term, VMWare is, today, a multi-cloud digital workspace and virtualization leader. The company offers services for application optimization, cloud management, cloud infrastructure, networking, and security across its platform. As a result, VMW is the kind of enterprise software platform that Broadcom should be able to grow and leverage across its existing software offerings. The company is also an excellent fit within Broadcom's networking and storage solutions businesses as well.

Dividends

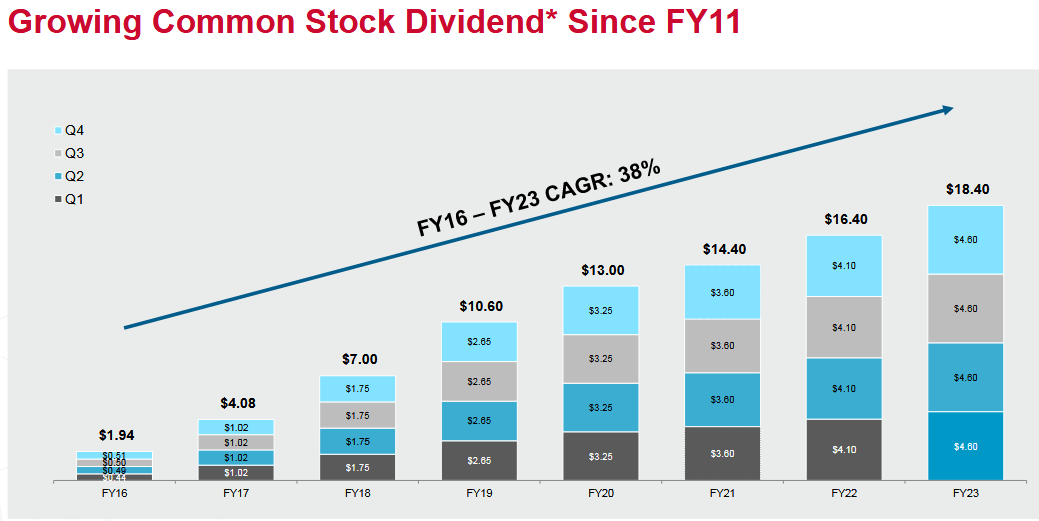

As most of you know, Broadcom - even through its many acquisitions - has demonstrated a strong track-record of dividend growth:

{kind=link}

Now, Broadcom ended Q3 with $12.1 billion in cash. That obviously bodes well for shareholders considering the current annual $18.40/share dividend obligation on its average of 427 million shares is an estimated $7.86 billion annually. Given AVGO's strong free cash flow profile, and its current ample cash position, and despite the pending VMW acquisition (itself a strong FCF generator), investors should expect another large dividend increase when it releases its Q4 and full-year F23 earnings. Last year, Q4 earnings were released on December 8th and included at 12% increase in the quarterly dividend (to the current $4.60/share). I estimate the increase in the quarterly dividend this year to be ~10%, to $5.06/share ($20.24/share annually).

For investors who might be concerned about the VMware deal's potential negative impact on Broadcom's dividend growth going forward, I once again refer them to Hock Tan's demonstrated track-record in that regard (see graphic above) and AVGO's strong FCF profile. I would also point out that VMW does not pay a dividend and the company ended Q2 with $6.8 billion in cash.

Valuation

Broadcom stock has been quite volatile this year, but has generally followed a robust upward trajectory (+58.5%). The stock currently trades at a TTM P/E of 27.5x and a forward P/E = 20.7x. The current yield is 2.11%. That's a slight premium to the S&P500 on a TTM basis ( P/E = 25.7x ) and it trades at par on forward basis. However, Broadcom's yield is 50 basis points higher than the S&P500 (1.51%).

However, according to the graphic below from CSI Market :

CSI Market

As you can see, Broadcom's free cash flow margin last quarter (51.8%) was ~3x that of the S&P500 as a whole (17.4%). That being the case, I regard AVGO stock to be significantly undervalued relative to the broad market.

Summary & Conclusion

Broadcom continues to execute very well on its long-term growth strategy. While top-line growth in the most recent quarter was not that impressive, free cash flow generation and growth in FCF/share was - at least in my opinion. And that was despite a generally stagnant Apple business which faced difficult yoy comparisons. Indeed, as Hock Tan said on the Q3 conference call, without the benefit of generative AI revenue (i.e. Ethernet switches), AVGO's semiconductor business would have been about flat yoy.

I expect the VMware deal to close at the end of next month just as Hock Tan predicts. I expect VMW to be another in a long-line of very successful M&A deals and for it to significantly add to AVGO's already strong free cash flow profile. Indeed, after the acquisition, Broadcom's revenue will be roughly 50/50 between semiconductors and enterprise software. Perhaps more importantly in the short-term, I expect another robust dividend increase announcement in early December.

Bottom line: AVGO is a BUY because it is one of the best dividend growth companies in the entire S&P500 yet the stock trades at roughly the same valuation level as the S&P500 while having a free cash flow margin that is ~3x that of the S&P500.

For further details see:

Broadcom: The Beauty Within - And VMware Will Add To It