PLDGP - Broadstone Net Lease: A Tempting ~7% Yielding Diversified REIT

2023-12-12 04:31:29 ET

Summary

- Broadstone Net Lease is a REIT with an attractive and sustainable yield, which has been increasing since its public debut.

- BNL has a diversified portfolio with a focus on industrial properties, which is beneficial due to the continued demand in the e-commerce sector.

- The company has a solid debt maturity schedule, a strong portfolio with diverse tenants, and a high occupancy rate, positioning itself well in the current environment and into the future.

Written by Nick Ackerman.

Broadstone Net Lease ( BNL ) is a diversified real estate investment trust ("RIET") sporting an attractive yield. However, just because a yield is attractive doesn't mean it is sustainable - in this case, they not only deliver a ~7% yield currently, but it is well covered and looks set to grow. This particular REIT might not have been on the public market for long, but they have been able to bump up the dividend semi-annually since it hit the market.

With debt maturity spread out primarily several years down the road, debt doesn't seem to be a significant headwind, relatively speaking. Additionally, the REIT is trading at a fairly attractive valuation. So this all lines up to mean this income play could be worth considering for investors.

About BNL

BNL might have hit the public market through an IPO in 2020, but it was founded in 2007 and grew assets through this period. Thus becoming a larger operation and internalizing management, which is generally a positive before coming to the main stage for public investors. Internalized management often means fewer conflict of interest issues popping up compared to external management teams.

While they are a diversified REIT, they tilt toward being an industrial-focused one, which I believe is another positive for them as demand in that space from e-commerce continues to be there. On the other hand, they do have some office exposure, which is a cause for concern for some investors - including myself. Demand in that space seems only to go lower while supply rises as the work-from-home trend becomes more popular. That said, this is a small allocation of their overall empire .

BNL Property Type Breakdown (Broadstone Net Lease)

"Empire" might be too strong of a word for BNL because, relatively speaking, it isn't nearly as large as its most popular peer, which would be W. P. Carey ( WPC ), which is often what BNL gets compared to. WPC is about 4x larger than BNL. However, WPC also just became a bit smaller through the spin-off of their own office properties into Net Lease Office Properties ( NLOP ) - as the dust settles there, WPC could be worth revisiting before too long.

Ycharts

A Look At Earnings And Growth

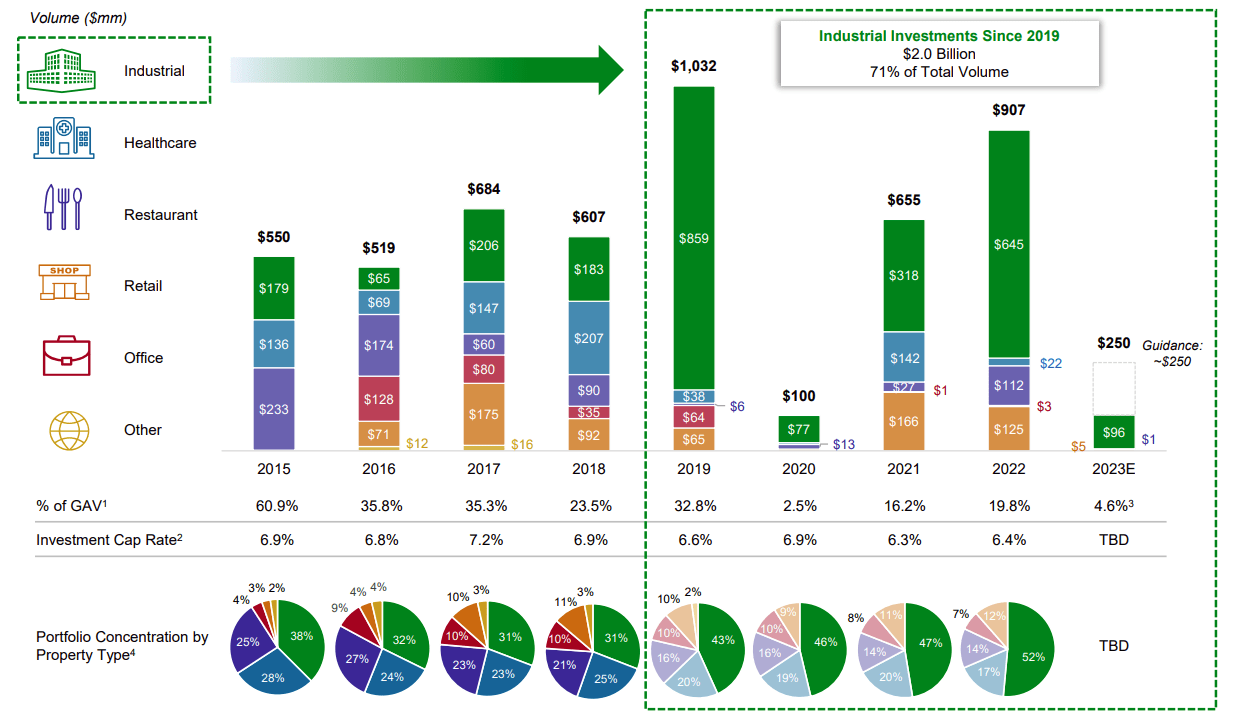

Looking forward and even more recently, in the last couple of years, BNL has not been allocating any further capital to office exposure. Instead, they continue to spend even more, pushing further into the industrial sector. That said, guidance for this year in putting any investment capital to work is much lower than the last couple of years. This can make sense in a higher interest rate environment and when share prices remain depressed.

BNL Portfolio Transition (Broadstone Net Lease)

{kind=link}

That does seem like a positive, but at some point, it is interesting to consider that the sector is getting quite popular. After all, this is exactly what WPC is also doing after it divested its office exposure; it wants to push even further into the industrial space. The industrial space also has its own REITs focused specifically on acquiring warehouses and logistics facilities too, such as Prologis ( PLD ) and STAG Industrial ( STAG ).

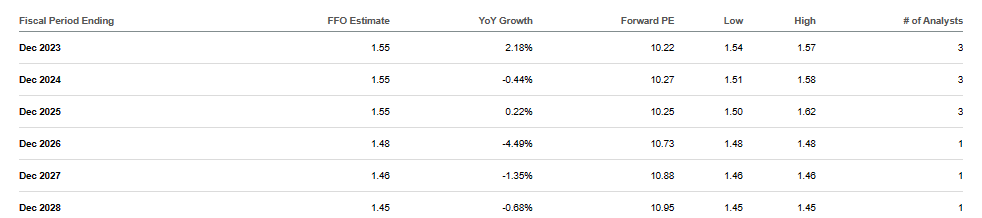

Being a smaller operation means they don't get quite the same attention from Wall Street Analysts. With that being said, the few analysts who do look at BNL suggest that there would be no growth going forward in the next couple of years. Even worse, earnings could start to contract, but that's only according to one analyst.

{kind=link}

That can initially be something that's concerning on the growth outlook. However, BNL's management is at least a bit more hopeful as they expect AFFO growth to be in the low single digits. Low single-digit numbers might not be the most encouraging or optimistic outlook, but any growth is better than zero or contracting earnings.

Spenser Allaway

Okay. That's really helpful. And then do you guys have a sense of what your AFFO growth would be next year absent any external growth?

John Moragne

Yeah. I think I'd point you towards a low single-digit figure based on our embedded lease bumps of 2%. Run rate for us is in that low single-digit growth.

If rates come down and the price of their shares rises, they could be in a much better position for putting additional capital to work in acquiring properties - with the idea that those properties and capital spending will lead to accretive FFO growth. Sometimes, walking away and being more patient is the best outcome rather than getting stuck in a deal that isn't in the overall best interest of all stakeholders. Walking away from a deal is something they noted on their most recent earnings call as well.

Of particular note, we recently walked away from a large significant late-stage investment opportunity as we could not agree on final pricing terms amidst the rapid increase in rates. The lag we are seeing in cap rates and risk-reward trade-offs has been a persistent theme for this year and the recent run-up in interest rates and treasuries only exacerbated the disconnect further. Despite that, we remain opportunistic in sourcing investment opportunities; and are committed to the prudent, patient and disciplined capital allocation strategy we have employed throughout 2023. We continue to believe that strategy will be key to avoiding missteps in such an uncertain market and providing long-term shareholder value.

Patience and discipline for long-term success over short-term gains are things that I view as positive from the management team, so seeing this statement was certainly encouraging. Additionally, at a forward P/FFO of around 10.24x based on the $1.55, it's a decent value here at a bit of a discount to WPC's 11.35x valuation.

No Near-Term Significant Debt And Long Leases

Net debt to adjusted EBITDAre comes in at 4.9x, which certainly seems high but isn't overly elevated for a REIT. For some context, WPC is running a net debt to adjusted EBITDA of 5.7x. Realty Income ( O ), while using a different playing field, comes in with net debt to Adjusted EBITDAre of 5.2x.

For BNL, over the last year, they've been working on taking down their leverage, as it stood at 5.5x a year ago. Debt holders of BNL can rejoice as they are assigned a BBB investment-grade credit rating.

Perhaps even more important than the overall debt burden itself in the current higher interest rate environment is the debt maturity schedule. For BNL, we are looking at maturities that are spread out with no meaningful debt until 2026. Then, from there, the maturities are fairly even for the following years.

BNL Debt Maturity (Broadstone Net Lease)

This can be an important distinction because, with a higher rate environment, we are going to start to see higher costs for refinancing. While rates are anticipated to be cut into 2024, that would certainly help relative to what we could expect rates to increase to if refinanced today. However, rates are still not anticipated to go to zero - or if they do, it's likely because we are in a deep recession - which has its own negative implications for a REIT in a different way.

What can provide more reassurance is the solid portfolio that they put together. Along with their diversified property diversification, of course, comes a diverse set of tenants. Even better is that no single tenant represents an abnormally large part of the annual base rent for BNL. This means that if one company fails, they won't feel it as drastically on their rent collection, and finding a replacement for a smaller portion of their properties should be easier.

BNL Top Tenants (Broadstone Net Lease)

The weighted average lease remaining came to 10.5 years, and they collected 99.9% of their rent. Occupancy is strong on their 800 total properties of 99.4%. Their portfolio runs a 2% average rent escalation, with 85.5% of their contracts coming in with fixed increases and 11.8% CPI-linked. In total, they list that 80.3% of their leases come with annual increases. Combining this with their solid debt maturity schedule, I believe they are in a solid position going forward.

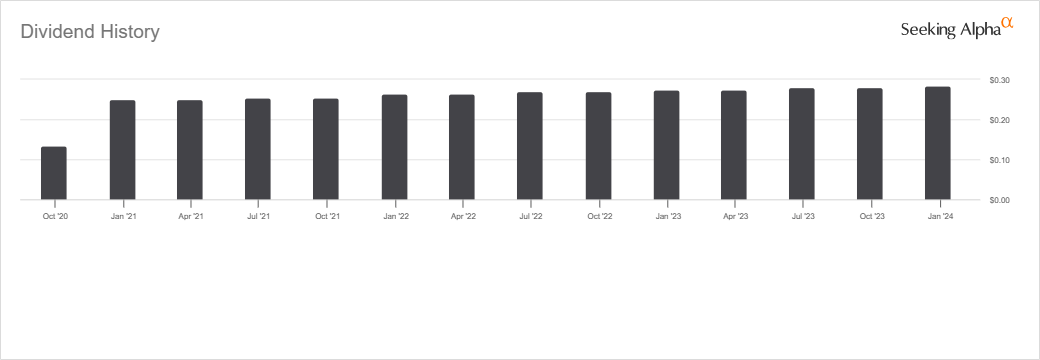

6.96% Dividend Yield

The latest annualized payout for BNL comes to $1.14, but that has increased every other quarter since they hit the public market. The latest dividend declared of $0.285 works out to an increase of 3.64% year-over-year. The raises might be small, but they can set them up for a long legacy of increases or leave more aggressive increases in the future. Again, in my opinion, this is prudent and patient management that is showing from this team.

BNL Dividend History (Seeking Alpha)

{kind=link}

With all of the above going on for this REIT, suffice it to say that I believe the dividend yield here is quite solid because it seems secure. Even with no expected growth from analysts - coverage here looks good, with plenty of room to continue to increase in the future.

Conclusion

Overall, BNL might be a smaller REIT player in terms of its enterprise value size, but they have just as good or even better debt metrics. Spread-out maturities leave them in a fairly envious position when the refinancings start. While growth might be slow going forward, it seems they are set to become a steady grower over the long term and are currently in a good position to continue to grow their attractive dividend. Risk-free rates have receded more recently, and that's allowed BNL's share price to rise rather meaningfully and recover more recently. At the same time, it still seems like a decent value trading below 10x P/FFO.

For further details see:

Broadstone Net Lease: A Tempting ~7% Yielding Diversified REIT