BNL - Broadstone Net Lease: Enjoy A High Dividend Yield

2023-06-28 11:20:00 ET

Summary

- Broadstone Net Lease offers a high dividend yield of approximately 7.2%, making it an attractive opportunity for income investors.

- The REIT has good tenant and sector diversification, with a high occupancy rate of 99.4% and an average lease term of 10.8 years.

- Despite concerns about real estate prices and rising interest rates, Broadstone Net Lease's strict capital management and favorable debt maturities make it a buying opportunity for investors.

Introduction

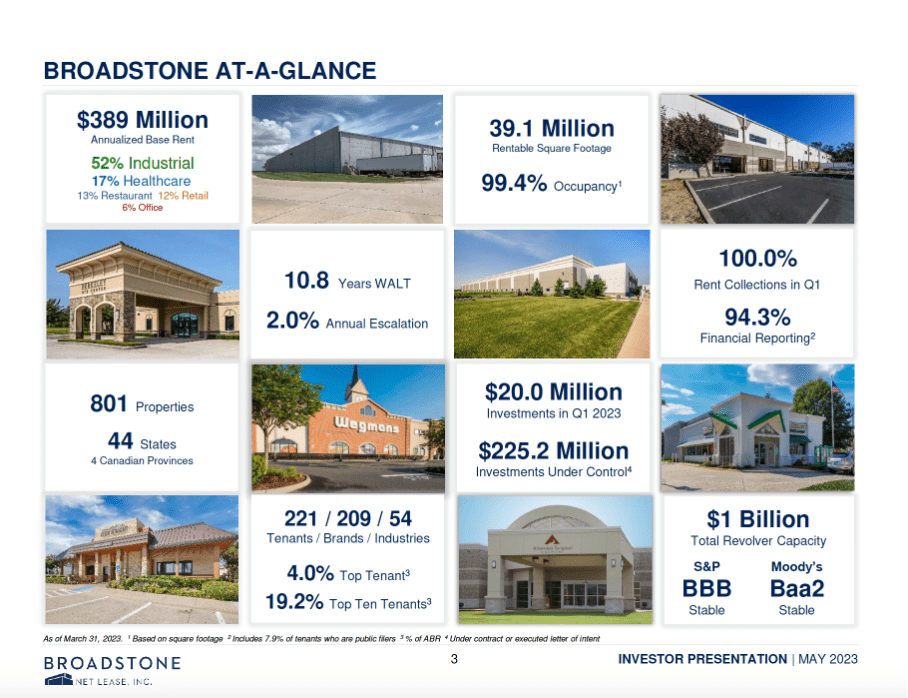

Broadstone Net Lease (BNL) is a REIT which is specialized in the rental of industrial real estate, which generates approximately half of the base rent on an annual basis. In addition, it rents out real estate in the healthcare sector, restaurants, retail, but also offices. With more than 801 properties in 44 states, 221 tenants and a good diversification of tenants, Broadstone Net Lease offers sufficient security to withstand difficult economic conditions.

In addition, the strongly corrected price offers a high dividend yield of approximately 7.2%, making this a great opportunity for income investors.

The drop in share price is not unjustified, however. Former real estate investor Charlie Munger talks about troubled office buildings, troubled shopping centers and many other troubled properties. He said that US banks are full of bad loans and will be vulnerable when bad times come and real estate prices fall. This sounds quite dramatic.

A new term in banking jargon is " criticized loans ." These loans have no subordinated payments, but are more susceptible to financial problems, such as an office building that recently lost a major tenant. This number of loans is increasing. Bank of America's criticized loans increased from $19 billion in office loans to $3.7 billion. This is certainly a significant increase, and rising interest rates don't really help either.

The office property sector is facing several challenges such as hybrid working, which reduces the demand for office buildings. Rising interest rates also lower the valuation of office buildings and make it more difficult to refinance real estate debt. Fortunately for Broadstone Net Lease, ABR from office properties is only 6% of total ABR. Therefore, I do not believe that BNL will bear any significant risk.

In my opinion, the stock has been penalized too harshly. The company is growing fast and the average rental term in combination with the rent escalations means that investors receive a stable growing dividend for many years to come. The dividend yield is decent, making this REIT ideal for income investors.

Effective Capital Management

Broadstone at a glance (1Q23 investor presentation)

{kind=link}

What I find attractive is the good tenant and sector diversification. The largest tenant accounts for 4% of annual base rent, and the first ten tenants account for only 19% of total rental income. The occupancy rate is also high at 99.4% and the average lease term of 10.8 years with annual rent escalations of 2% ensures a steady growing revenue.

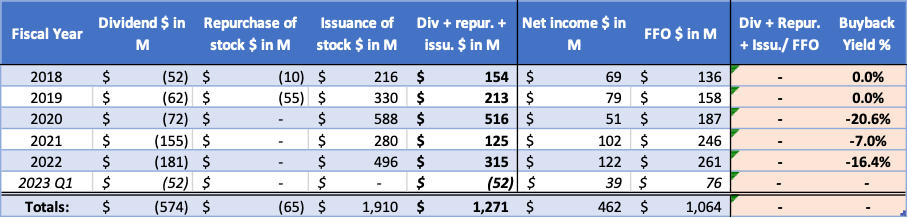

The results of the first quarter of 2023 came in with revenue growth of 6.3% over the same period in 2022 and net income growth of 12.5%. Adjusted FFO per share decreased slightly by 5.6% partly due to stock dilution. The number of outstanding shares was increased from 182,971 to 196,176 to raise capital and increase their revolver capacity.

Management has strong investment selection criteria and felt cap rates had not increased enough to make an investment attractive. As a result, only $20 million in real estate investment has been made, while disposals are approx. $52 million. Some of the dispositions include $32 million office properties. In doing so, it reduced office exposure to just 5.8% of ABR.

I think sticking to the principles, maintaining profitability and risk exposure is a strong move. When cap rates become attractive, I expect management to take steps to attract opportunities again.

The tenants' profitability and solid financial standing is also crucial. Of the 221 tenants, 94.3% report their financial reports to BNL, and 15.6% of tenants' annual base rents have an investment grade credit rating. Some of the leading profitable and publicly traded tenants include: Axcelis Technologies (ACLS), Dollar General (DG), Tractor Supply Co (TSCO) and many more.

Some tenants are closely monitored, such as Carvana (CVNA), Red Lobster, and Green Valley Medical Center. Given the current credit market conditions, these tenants may be susceptible to short-term refinancing risks. However, rental collections remain at 100% and there are no signs of concern yet.

Favorable Debt Maturities

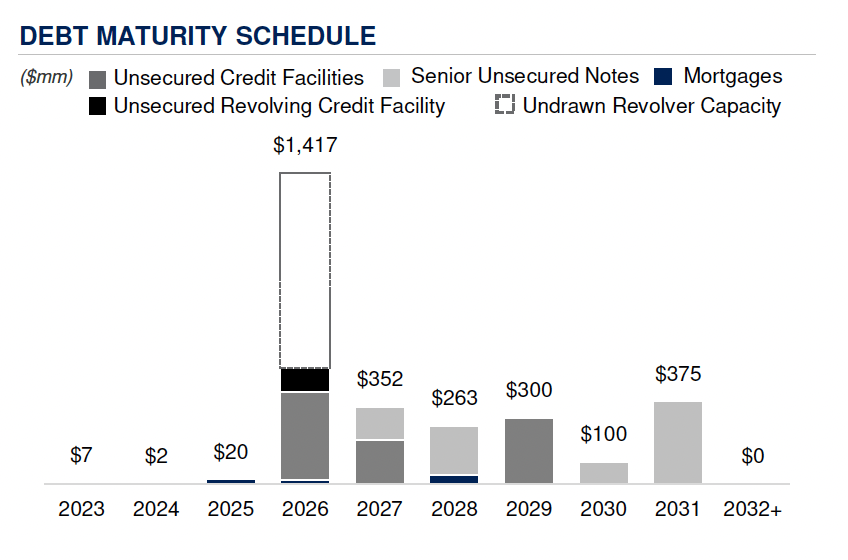

Broadstone Net Lease has a low leverage profile with Net Debt/Adjusted EBITDAre of just 5.1x. The maturities of the debts are also very favorable because major repayments will not take place until 2026. The Federal Reserve has raised interest rates sharply and many analysts expect interest rates to fall in 2025; BNL should be able to refinance its debts at favorable interest rates.

Debt maturity schedule (Broadstone's 1Q23 investor presentation)

{kind=link}

The debt, excluding the revolving credit facility, has a weighted average fixed interest rate of only 3.7%. The coverage ratio comes out at 3.9x times and the company has $907 million in liquidity. In addition to taking on debt, BNL can raise additional capital through the issue of shares. This dilutes the existing shares, but investors can enjoy higher rental income.

Dividends and Share Repurchases

REITs must pay out 90% of their taxable income as dividends. BNL's dividend yield is high at 7.2% and amounts to $1.12 per share. As earnings increase, so does the dividend. In the near term, however, I expect a slowdown in growth as BNL struggles to find real estate with a good cap rate. From 2024 I expect more acquisition activity due to possible falling interest rates.

What is also striking about the cash flow statements is the substantial issuance of shares; in 2022, shares are dilutive at a low share price. I think issuing shares is only beneficial when the stock is overvalued, not after the stock has already fallen sharply. The proceeds from the stock issue will have to be profitably invested to achieve the same dividend per share and FFO level.

Broadstone's cash flow highlights (Annual reports and calculations)

{kind=link}

Valuation

I think equity valuations of mature companies are recovering to their average valuation. Rising interest rates have had a huge impact on equity and REIT valuations. We are approaching an economic recession after which the Federal Reserve will cut interest rates, which will cause stock prices to rise. BNL is currently trading 27% below its 3-year average price/FFO ratio. If equity valuations return to their average, we can expect nice returns in the medium term.

Price to FFO ratio (Analyst' calculations)

If we compare BNL to the sector average, we see an undervaluation here as well. The average forward price/AFFO ratio is 11x, while the sector average is 14.3x (discount of 23%). One small note is the moderate short-term growth prospects. For 2023 and 2024, analysts expect an increase of only 3.2% and 1.5%.

I think BNL is a buying opportunity. Investors can enjoy a generous dividend of more than 7% and in the medium term, I expect a rise in the stock price as interest rates fall.

Conclusion

Charlie Munger has expressed concerns about real estate prices in general, and rising interest rates have contributed to many REITs falling sharply. Shares of Broadstone Net Lease have undergone a significant correction since peaking in September 2021. This REIT specializes in the rental of mainly industrial properties, but also rents out properties in the healthcare sector, restaurants, retail, but also offices. Charlie Munger expects office real estate to have a high risk of impairment. The ABR of office buildings only accounts for 6% of the total ABR because a few office buildings have been sold.

Its tenants are widely diversified, the occupancy rate is excellent at 99.4% and most tenants are financially sound. BNL is looking for real estate with a high cap rate from financially healthy companies. However, BNL has sold more real estate than it acquired because it did not see good opportunities. Its strict capital management maintains profitability and financial flexibility. When opportunities arise, BNL seizes them.

Significant amounts of debt do not have to be paid off until 2026. Many analysts expect interest rates to have fallen by then, which will benefit the refinancing of its debt. The dividend yield is attractive, and I expect investors to enjoy a high dividend yield of over 7% until 2024, after which I expect a share price increase. The bull case is intact because of falling inflation, which indicated that the Federal Reserve will cut interest rates soon. If inflation suddenly rises, I expect further rate hikes and falling stock prices. For now, BNL is buy-worthy.

For further details see:

Broadstone Net Lease: Enjoy A High Dividend Yield