BNL - Broadstone Net Lease: High Yield With A Limited Downside

2023-11-03 14:57:17 ET

Summary

- BNL is a smaller net lease REIT with around 800 properties diversified between multiple sectors.

- The REIT's operational performance has been stellar and rivals the best in the industry.

- Moreover, valuation is now appealing with an 8% dependable dividend yield and a 400bps spread to 10-year treasuries.

Dear readers,

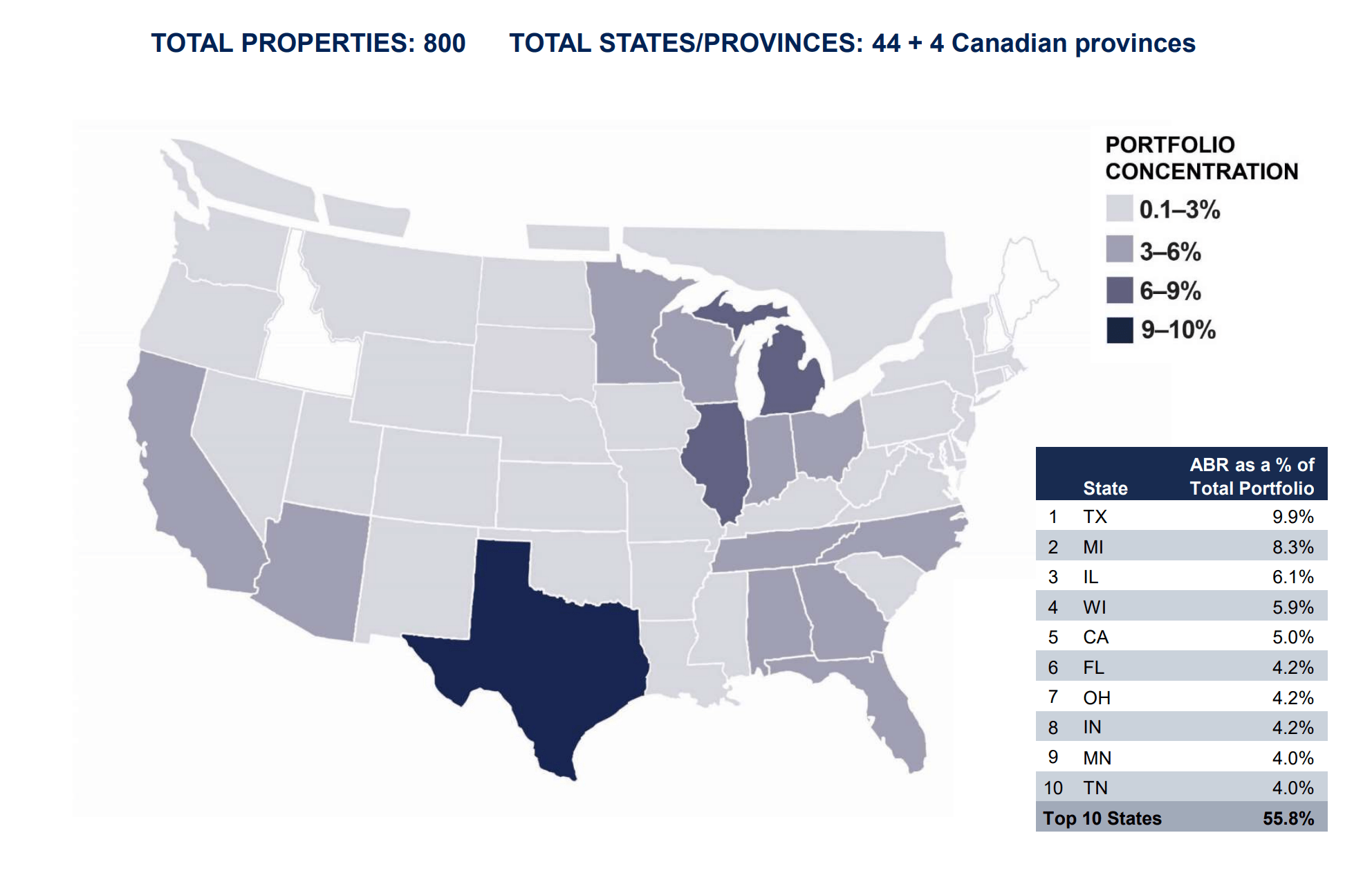

Broadstone Net Lease ( BNL ) is a net lease REIT which has a 15-year history, but has only IPOed recently in 2020. The REIT is relatively small with around 800 properties located across the US. Texas is their main market and accounts for 9.9% of ABR. This is followed by Minnesota at 8.3%, Illinois at 6.1% and California at 5%.

{kind=link}

One of the main criticisms that I have is that the REIT lacks a clear focus, which is especially evident from the sector allocation of their properties. Industrial accounts for 51%, followed by healthcare at 18%, restaurants at 13%, retail at 11% and office at 6%. Given their small size, they may be spreading themselves too thin as they try to become a "jack of all trades", rather than gain deep expertise in one sector. This is likely to impact BNL's valuations as the market usually prefer specialized REITs and tends to give them a premium.

I covered the REIT back in April, gave an overview of the business and issued a BUY rating at $16 per share. The investment seemed attractive, because BNL had one of the highest dividend yields in the net lease sector and traded at a significantly lower valuation than its peers, more than pricing-in the "jack of all trades" discount. Since then, my RoR has been negative at around 10%, but the REIT's operational performance has been pretty good as confirmed by several quarters of earnings, most recently Q3 2023 . Moreover, the REIT now trades at a sufficiently high spread to 10-year yields, providing a substantial margin of safety in my view.

Broadstone's performance

On an operational basis, BNL's portfolio rivals the best in the sector. Occupancy is exceptionally high and stable at 99.3%, rent collections are at 100% and rent coverage stands at 3.1x. As a result, BNL's rental revenue is very visible and dependable.

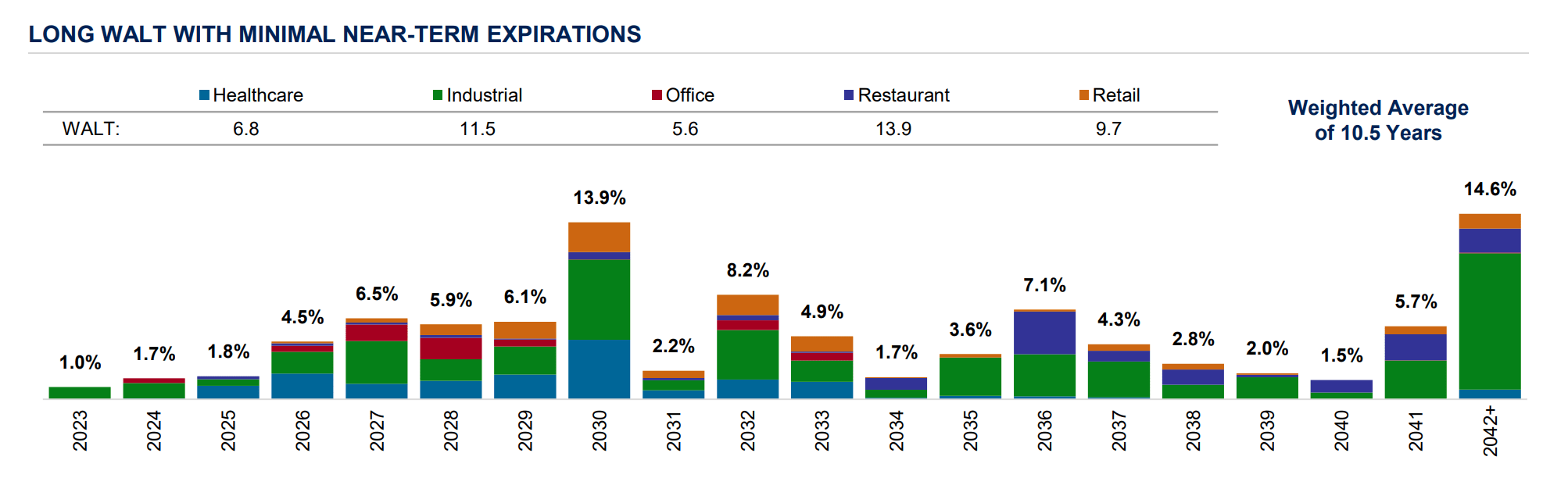

All net lease REITs have long lease agreements and BNL is no different. Their WAULT stands at 10.5 years and their lease expirations in the following years are very low. Only 4.5% of leases will expire before 2026.

{kind=link}

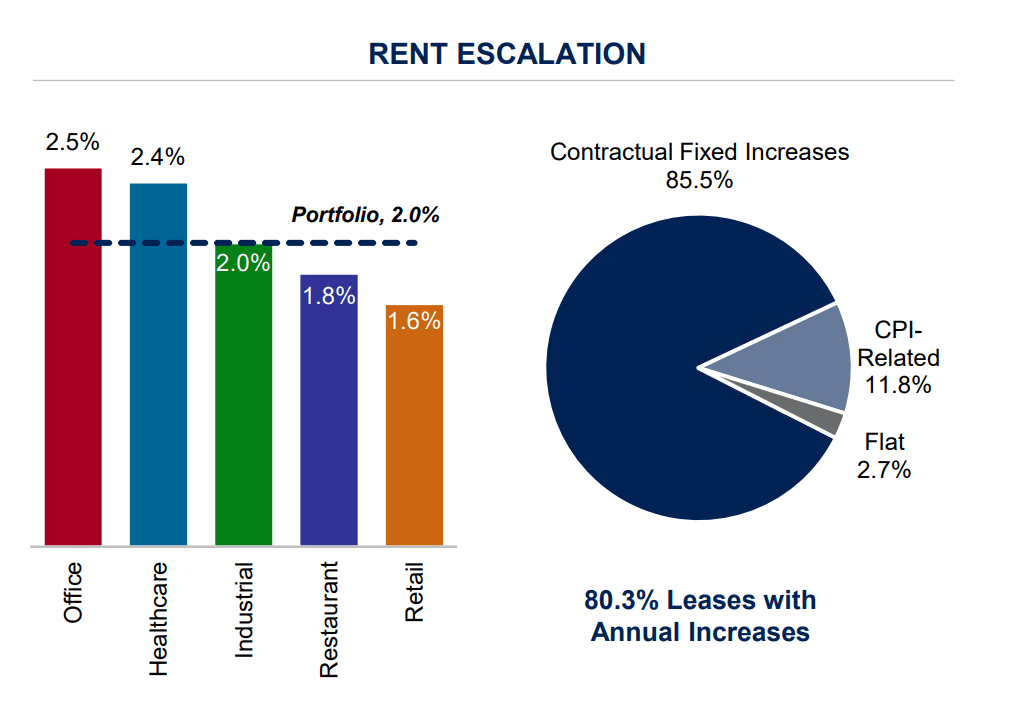

Long-term leases make for very predictable cash-flows, but also reduce the REIT's ability to increase rents in an inflationary environment, which can be risky if inflation and interest rates stay high. BNL's portfolio averages 2% built-in fixed rent increases on 85% of leases and 12% of leases have CPI-related indexation (mostly with 3% caps).

{kind=link}

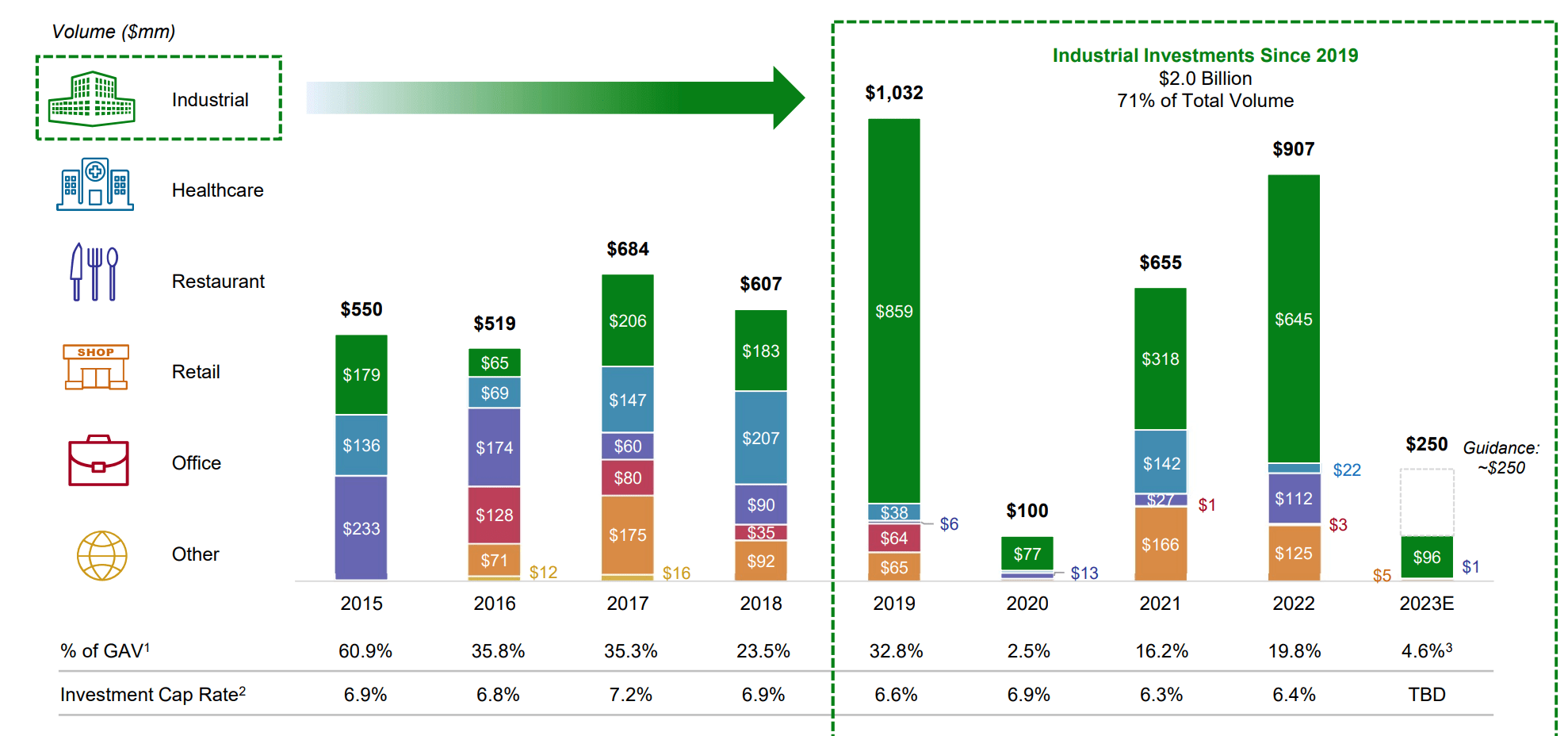

Because internal growth of 2-2.5% isn't very appealing, the REIT has historically pursued an aggressive acquisitions strategy to increase their total growth prospects.

This has worked quite well historically, but this year investment into new acquisitions has slowed significantly. Back in April, management was targeting total investment volume of $300-500 Million for this year, which would increase BNL's gross assets by 7-8% YoY. But the target has been recently revised down to $250 Million. Management has stated that the reason for the downward revision is that they remain highly selective as cap rates on new deals still lag the pace of rate increases, which reduces their investment returns. I largely agree with that statement and would like to see management as least consider share buybacks instead, as the implied cap rate of their own stock is now significantly above what they can achieve from acquisitions.

Over the first nine months of this year, BNL has only invested $101 Million, including $25 Million in new acquisitions, $26 Million in revenue-generating CAPEX and $50 Million in development funding. This means that even their reduced target is still relatively far away.

{kind=link}

With regards to dispositions, year-to-date BNL has sold $180 Million of properties at an average cash cap rate of 5.9% and management has confirmed their full year target at the top-end of previous guidance of $200 Million.

While disposals at 5.9% are accretive (vs acquisition at 7.1%), I don't like that the REIT's portfolio is effectively shrinking as they sell more than they buy. With no external growth, rental revenue is likely to grow by no more than 2% per year.

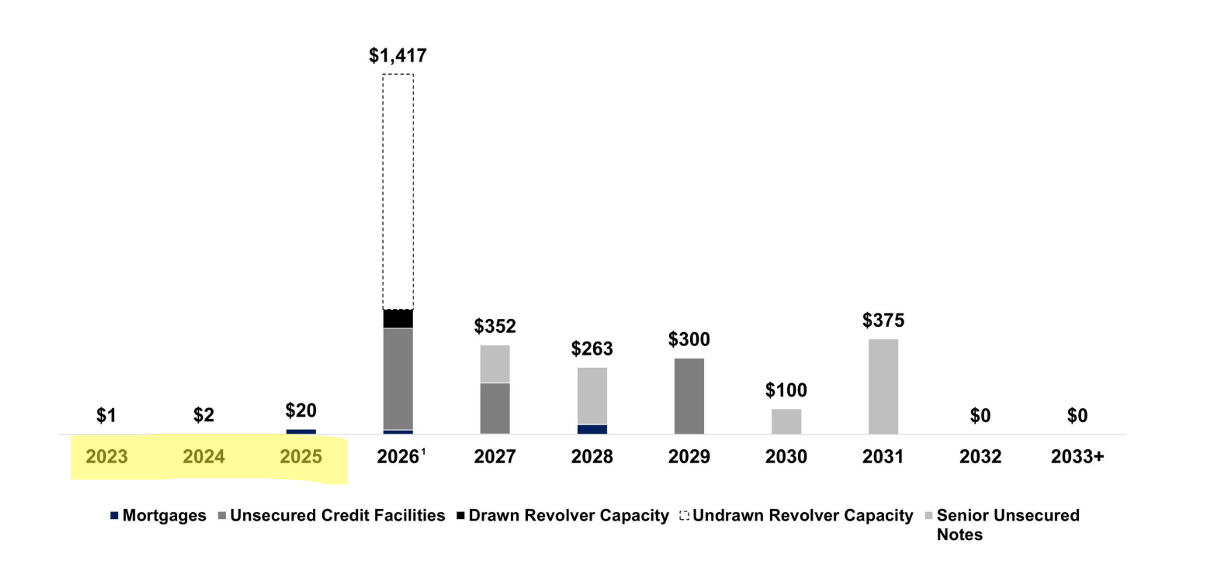

The good thing is that BNL's net interest expense won't increase much either so cash flow should be stable even if interest rates stay high until 2026. BNL has a BBB rated balance sheet with a net debt/EBITDA of 4.9x. I also want to point out that the REIT has very low interest rate risk as 100% of their debt is fixed rate and they have no material debt maturities prior to 2026. What this means is that even if rates stay high until 2026, the REIT's FFO will still have grown by about 5-6%.

{kind=link}

Valuation

BNL pays a 7.9% dividend yield, which is reasonably covered with a forward payout ratio of 80%. While I don't expect the dividend to grow, given the stable cash flow, a risk of a cut is minimal here. That's important, because a nearly 8% dividend alone can make an investment worthwhile for income investors.

The REIT trades at 10.2x FFO which is substantially below the average for the purely net lease peer group of 12x FFO, but this is expected. W. P. Carey ( WPC ), which makes for a good comparison due to its heavy exposure to industrial properties, trades closer to 11x FFO, but once again a premium is likely justified here given WPC's longer track-record. All things considered, I see BNL as fairly valued relative to peers.

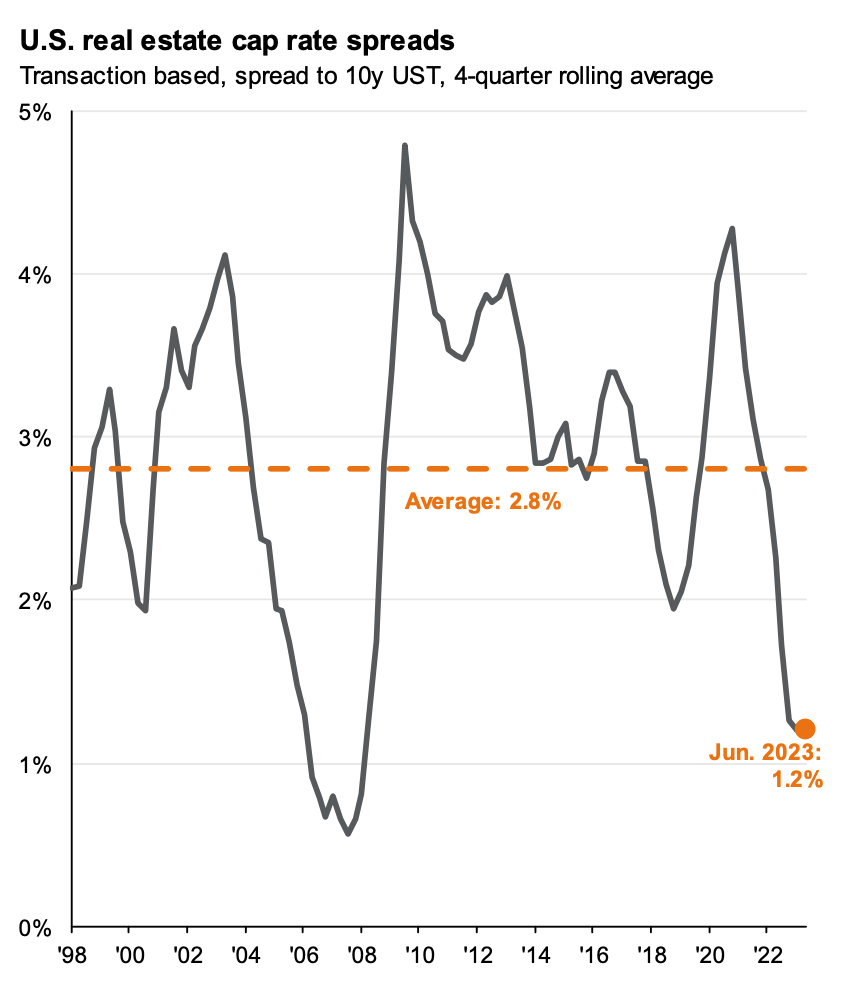

Future price action will depend, for the most part, on what happens to interest rates and yields. Currently, the implied cap rate stands at 8.7% which is 400 bps above 10-year treasury yields. That's comfortably above the 25-year average spread on real estate transactions of 280 bps ( reported by JPMorgan ), which leads me to believe that the downside for BNL is quite limited here, even if interest rates stay at today's level. If/when interest rates decline, I expect substantial upside to get unlocked. Following Q3 results, I see no reason to move my previously established price target of 13.5x FFO or $20 per share, which represent upside of about 33% from today's level.

{kind=link}

In summary, BNL can help diversify net lease exposure and can be reasonably expected to:

- pay a 7.9% dividend yield

- grow its FFO by 2% per year

- and potentially re-rate to 13.5x FFO (assuming interest rates decline) leading to 33% upside

That's very appealing from an income investing perspective which is why I rate the stock a BUY here at $14.40 per share.

For further details see:

Broadstone Net Lease: High Yield With A Limited Downside