UBS - Bronte Capital Amalthea Fund March 2023 Letter

2023-05-04 16:04:00 ET

Summary

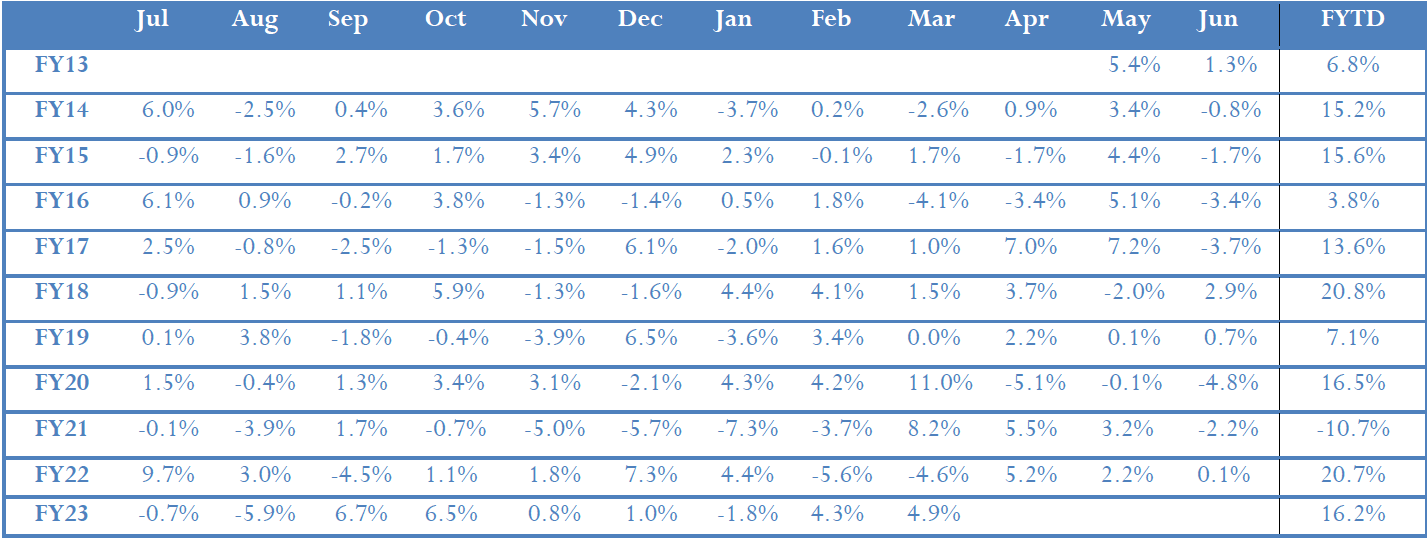

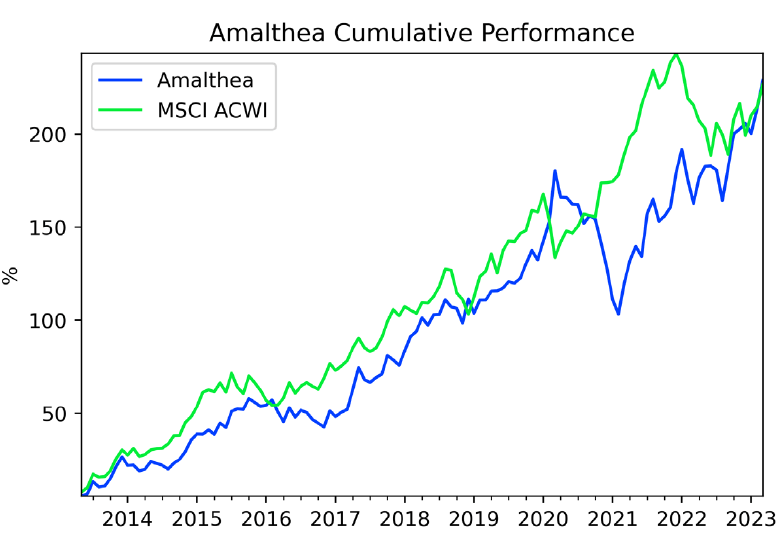

- The Amalthea fund gained 4.92% in March whereas the globally diverse MSCI ACWI (in ) was up 3.90%.

- The last week of March was characterised by a strong market, particularly in very dodgy stocks.

- Considering we had a banking crisis this quarter and the fed funds rate rose to its highest level in 15 years, you might expect to see credit issues beginning to appear.

The Bronte Amalthea Fund is a global long/short fund targeting double digit returns over the long term, managed by a performance orientated firm with a process and portfolio that we feel is genuinely different. Objectives include lowering the risk of permanent loss of capital and providing global diversification without the market/drawdown risks typical of long-only funds. We believe a highly diversified short book substantially reduces risk and enables profits to be made in tough markets

{kind=link}

The Amalthea fund gained 4.92% in March whereas the globally diverse MSCI ACWI (in ) was up 3.90%. For the quarter Amalthea was up 7.55% versus a 9.23% gain for the ACWI. This was a quarter where the indices went up, and if that was all you looked at you would think all was healthy in the markets. Alas it was far from uneventful for us. January was very strong indeed, and our performance was lackluster though not threateningly so. The most aggressive fund managers we know were up over 20 percent—about 20 percent better than us. (see over)

{kind=link}

1 Performance and analytics are provided only for Amalthea ordinary class units. Actual performance will differ for clients due to timing of their investment and the class of their units in the Amalthea fund

2 Sharpe and Sortino ratios assume the Australian cash rate as the applicable risk-free rate

3 Returns are net of all fees

Disclaimer: This report has been prepared by Bronte Capital Management Pty Limited. This report is for distribution only under such circumstances as may be permitted by applicable law. It has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient. It is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. No representation or warranty, either express or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the report. The report should not be regarded by recipients as a substitute for the exercise of their own judgement. Any opinions expressed in this report are subject to change without notice. The analysis contained herein is based on numerous assumptions. Different assumptions could result in materially different results. Bronte Capital Management Pty Limited is under no obligation to update or keep current the information contained herein. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realised.

From the middle of February to the last week in March markets were weak and our performance was very pleasing indeed. At this stage we were nicely ahead of the market for the quarter.

The last week of March was characterised by a strong market, particularly in very dodgy stocks. This week was poor for us, and we wound up marginally behind markets for the quarter.

We only state this because, if you looked at only the quarterly result, you might think we were highly market correlated—and you would be wrong.

Bank collapses

The biggest thing that happened in markets in the quarter was the collapse of three banks:—Credit Suisse, Silicon Valley Bank and Signature Bank. We have held short positions in each of these banks, but we traded them poorly and profits were smaller than they could have been.

We have also purchased the successor banks for two of them. We initiated positions in UBS ( UBS ), which has purchased Credit Suisse under advantageous terms, and First Citizens Bank, which purchased much of Silicon Valley Bank on even more advantageous terms.

We will go through each of these banks in turn as they are ((A)) interesting in their own right and ((B)) have resulted in some changes in our portfolio.

Credit Suisse ( CS )

Swiss banks were sharply weakened by the end of banking secrecy. Historically, Switzerland was a clean place to hide your dirty money and Swiss Banking was almost synonymous with tax avoidance.

Swiss banking secrecy is now extinct, and many American clients either paid their back taxes or were prosecuted.

Secrecy made Swiss banks profitable despite excessive cost structures. They had many rich customers who really couldn’t move their money elsewhere.

The end of banking secrecy left Swiss banks with unhappy clients who could now move their money elsewhere, excessive cost structures and big fines from the US Government. It wasn’t great.

Profits were going down.

Banks can of course increase their profitability by taking more risk and both major Swiss Banks (UBS, Credit Suisse) took this route. UBS however lost a lot of money in the financial crisis and sharply reduced their risk profile. They have maintained the lower risk profile ever since.

The last annual report makes this clear with a short company history:

Since our origins in the mid-19th century, many financial institutions have become part of the history of our firm and helped shape our development. 1998 was a major turning point: two of the three largest Swiss banks, Union Bank of Switzerland and Swiss Bank Corporation ((SBC)), merged to form UBS. Both banks were well established and successful in their own right. Union Bank of Switzerland had grown organically to become the largest Swiss bank. In contrast, SBC had grown mainly through strategic partnerships and acquisitions, including S.G. Warburg in 1995.

In 2000, we acquired PaineWebber, a US brokerage and asset management firm with roots going back to 1879, establishing us as a significant player in the US. For nearly 60 years, we have been building our strong presence in the Asia Pacific region, where we are by far the largest wealth manager, with asset management and investment banking capabilities.

After incurring significant losses in the 2008 financial crisis, we sought to return to our roots, emphasizing a client-centric model that requires less risk-taking and capital. In 2011, we started a strategic transformation of our business model to focus on our traditional businesses: wealth management globally, and personal and corporate banking in Switzerland.

Today, we are a leading and truly global wealth manager, a leading Swiss personal and corporate bank, a global, large-scale and diversified asset manager, and a focused investment bank.

Credit Suisse by contrast continued to take more risks (and risks inconsistent with the franchise and the skills of the staff). They got a deserved reputation as “accident prone.”

It was during this time we shorted Credit Suisse. We were aware of one accident unfolding, namely that the bank was putting a large amount of client money at risk with Greensill. John blogged about that here .

While we were short due to Greensill exposure, we made money on the short due to another “accident” at Credit Suisse that was exposed roughly simultaneously: large losses on margin loans to Archegos, an insanely aggressive family office.

We covered. We shouldn’t have. We understood just how much dross was in the bank. But we made money accidentally (on the Archegos incident about which we knew nothing) and when we make money fortuitously, we like to take unearned profit—but not undue credit— for our luck. In this case, with multiple issues appearing, we should have remained short.

Though a legal dispute over culpability rages on, Greensill was part of the reason why Credit Suisse failed, having contributed to the erosion in market confidence. Credit Suisse put clients into their fixed income funds, marketing that they were safe. They were far from safe. Later, when Credit Suisse assured clients that their deposits were safe, some of those clients did not believe them.

Regardless, the multitude of accidents eventually doomed Credit Suisse.

UBS was given Credit Suisse on favourable terms by regulatory fiat. The terms are a discount to book of tens of billions of Francs and liquidity guarantees from the Swiss National Bank.

The liquidity guarantees ensure that for the next few years UBS is immune to bank runs. There is now only one large Swiss Bank—and the large share of domestic business should ensure profitability.

We have purchased a long position in UBS, a rare new long for our fund.

Credit Suisse remains overstaffed with over-paid and risk-loving staff. We hope and expect UBS will fire many of them. If they don’t our UBS stock position probably won’t work that well. But the merger integration plans are not yet nailed down, so we consider this position provisional.

Silicon Valley Bank ( SIVBQ )

Silicon Valley Bank is a sad story. It is by far the best bank that we have ever seen fail. Indeed, it was the merits of Silicon Valley Bank that caused massive deposit inflows and a terrible investment decision that led to the failure.

This deserves an explanation.

Silicon Valley Bank was a large bank with very few (34) branches. The bank did business by being very nice to high-growth start-ups and their venture capital ((VC)) investors.

Banks tend to treat start-ups terribly. Getting credit cards for your staff for instance is hard. Getting a bank to take seriously a tech start-up run by a bunch of pimply 22-year-olds funded by a VC firm, but with no revenue and no business experience is—well—tricky.

But if you banked with Silicon Valley those problems disappeared. You gave them your deposits and they would happily integrate with your systems, offer you decent service and try to solve your problems. A bank that even tries to solve your problems is—for the most part—a bank that deserves your business.

Silicon Valley Bank was also deeply knowledgeable. We have heard nothing but good things about the competence of their biotech analysts for instance. These are unusual skills in a commercial bank.

As a result, a huge fraction of start-ups in tech and biotech banked with Silicon Valley. Silicon Valley gained large deposits for very little interest cost—but quite a deal of service cost. Being nice to start-ups was not free.

The bank’s loan book was also good. Over half of the book was loans to venture funds against capital calls the fund will make in the future. The typical fund has a right to call additional capital as needed. The timing of investments made by the fund may not match the timing of a capital call, and the funds often wanted a bridge loan to cover this gap. This was a very safe loan category where losses were nearly zero. They may not be zero in the future if some limited partners default on capital call obligations—but we do not see large losses in this loan category.

Much of the rest of the loan book is lending to technology and life-science companies. However, most of this lending is to more mature companies rather than early-stage start- ups. There is some real-estate lending from their acquisition of Boston Private. Finally, there are loans that can roughly be described as funding the hobbies of rich guys such as wineries in the Napa and Sonoma Valleys. The rest of the book looks riskier than the capital-call backed loans—but they are certainly safer than a lot of loans we see at other regional banks.

In summary, Silicon Valley was a pretty good bank that served its customers well and did not make stupid loans.

So why did it blow up?

Well, there was a massive bubble in almost everything in 2021. We have talked about that a lot. Start-ups also were in a bubble. The rate of start-up formation went vertical.

This meant the deposits at Silicon Valley Bank went up very sharply. Deposits grew as follows:

| Quarter ended |

| Deposits—billion USD |

| June 2020 |

| 62 |

| Sep 2020 |

| 75 |

| Dec 2020 |

| 85 |

| Mar 2021 |

| 102 |

| Jun 2021 |

| 124 |

| Sep 2021 |

| 146 |

| Dec 2021 |

| 171 |

| Mar 2022 |

| 189 |

| Jun 2022 |

| 198 |

After this explosive growth, deposits declined.

The problem of course was that during this explosive growth interest rates were zero. The low-risk thing to do was to take the deposits and invest in short-dated Treasury paper. After all there was no way that Silicon Valley Bank could invest the funds with any edge at the rate they flowed in.

Alas the low-risk path involved Silicon Valley Bank making no money, as they would get to invest the deposits at a zero rate. So Silicon Valley Bank did something really dumb. They invested the money in long-dated treasuries and mortgages. They took a big risk that interest rates would not rise. Well interest rates did rise—and Silicon Valley had mark-to- market losses of approximately 15 billion dollars on their securities portfolio. Those losses doomed them.

We had a small short position. We felt bad shorting this because we admired Silicon Valley Bank (and we usually only short bad people). We only had the short on because Bill Martin (of Raging Capital Ventures) explained Silicon Valley’s bank problems in a prescient twitter thread . The short was undersized and the tiny position was our fault. The problem was entirely spelled out by Bill Martin and we should have done better.

The post-bankruptcy period surprised us because Silicon Valley Bank seemed to have trouble finding a buyer. Our guess is that JPMorgan ( JPM ) would have liked to buy it but was prohibited by anti-trust concerns. The loan book and deposit liabilities were transferred with some funding guarantees to First Citizens Bank at a 16-billion-dollar discount. That discount is larger than the market cap of First Citizens. And we think the loans are likely good and First Citizens has an astonishing deal.

We could be wrong on this. We had a very rosy view of Silicon Valley Bank before its failure and that view might be wrong. The loans may be bad. But if Silicon Valley Bank was anything like as good as our preconceptions, then First Citizens is a very cheap stock indeed.

Signature Bank ( SBNY )

We have been short Signature Bank for over a year.

While we first noticed its substantial cryptocurrency exposure in 2021, the position’s origin was an article in American Banker from March 2022. To quote:

The volume of assets held by banks on the FDIC’s problem bank list — a tally of banks that received poor ratings from regulators — jumped by about $120 billion in the fourth quarter, according to the agency’s fourth- quarter banking profile released last week. That’s more than triple the previous figure of assets under problem banks, and it’s the highest that asset number has been since the third quarter of 2013.

We did not know whether the new problem assets were one bank with approximately 120 billion in assets or two banks summing to 120 billion in assets. Whatever: if it was one bank there was only one bank it could be—which was Signature Bank. No other bank was within 10 billion dollars of the required 120 billion. Regardless, we began digging.

The more we looked the less we liked Signature Bank. We shorted it. While it was mostly ancient history, Signature had a series of, well, surprising Board members over the years, including the likes of Ivanka Trump, Senators Alfonse D’Amato and Barney Frank, and a former CEO (and CFO) of Lernout & Hauspie from 1993-1996. L&H was an iconic fraud (the SEC sued them over transactions from 1996-1999) that sent John on his career of fraud hunting.

We doubted whether the deposit base was stable. We dug into the FDIC data and matched deposits to branches and looked at those branches with Google Street View. This branch for instance had $2 billion in deposits—a very large number, it seemed to us, given the location.

At $300 a share Signature Bank was one of the biggest shorts at Bronte. We covered about half the position at $120 on the way down. We did not have any idea that the complete collapse of the bank was nigh. By the time the bank collapsed our position was very small. (Again we wish we had traded this better.)

State of the Markets

Considering we had a banking crisis this quarter and the fed funds rate rose to its highest level in 15 years, you might expect to see credit issues beginning to appear. And there are some minor signs of stress.

We had a couple of our shorts trip debt covenants. Yet despite these businesses looking worthless to us, they received waivers and extended their countdown clock to bankruptcy. This is not the sign of a tight money market.

Perhaps the best example of this was WeWork, a cash inferno short-term office rental business. They were able to refinance their debt in the last few weeks. Non-Softbank holders of existing debt who chose not to contribute further capital were offered the choice:

a) third lien PIK notes due 2027 plus equity; or b) just equity. We are reminded of a quote from an (in)famous film director : “More than any other time in history, mankind faces a crossroads. One path leads to despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly.” Given these choices, people seem to have opted to defer losses.

Other New Longs

After a long time not being able to find any longs we like, this quarter we found four. Two are banks described above. The other two will remain nameless for the time being as we are not finished purchasing the stocks.

And we are chirpy about our prospects. Surprisingly chirpy given we saw a fairly bad last week in March. We are finding some reasonably priced quality businesses to buy while still finding plenty of wildly overpriced junk. We like this setup.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Bronte Capital Amalthea Fund March 2023 Letter