BKD - Brookdale Senior Living: Economic Growth Factors Clamping Equity Gains Reiterate Hold

2023-08-30 11:55:25 ET

Summary

- Brookdale Senior Living shares have seen a reasonable increase, but the economic realities of the company's business growth don't appear investment-grade.

- Q2 FY'23 showed positive growth in resident fees, revenue per available room, and occupancy rates.

- The company's unit economics and return on investment are not favorable, and further asset disposals may be necessary to finance growth.

- Net-net, reiterate hold.

Investment briefing

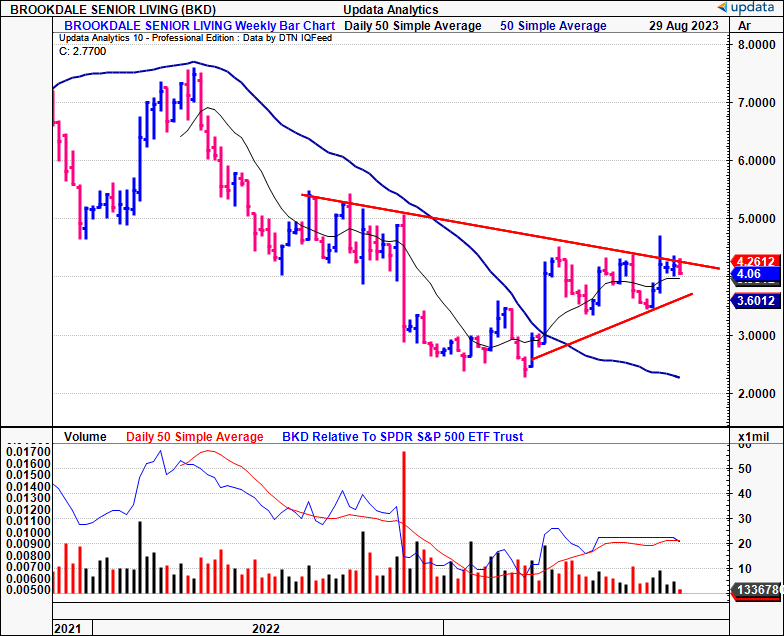

Shares of Brookdale Senior Living ( BKD ) have caught a reasonable bid since the January publication, and now sell 50% higher off the $2.87/price when that report was posted. Despite numerous positive points from its latest numbers, including: fixed cost leverage on lower labor rates, top-line growth, and a return to pre-tax earnings growth - the economic realities of BKD's business growth suggest it is still not investment-grade in my view.

This is a capital-intensive, profit-light business—you've got ~$5Bn in capital deployed producing just $1.20 in TTM NOPAT/share, otherwise 6% return on investment. As residual claim holders, equity investors are interested in the profits earned per $1 of capital their company deploys into its operations. As such, you'd want your company to be doing more than long-term market rates offer—typically around 10–12%. This, combined with unsupportive valuations, keep me neutral on BKD as a long-term holding, by keeping in sync with our focus on unrelenting quality in our equity risk budget. I'd like to stress this rating is based on the strategic side, from 1) long-term positioning, and 2) economic business factors that relate to long-term factors. There may be scope to allocate to BKD on the tactical side, with shorter-term holding periods in mind. Nevertheless, I reiterate hold.

Figure 1.

{kind=link}

Critical investment updates to reiterated thesis

Q2 FY'23 insights

BKD put up resident fee revenues of $719.2mm in Q2, up ~11% YoY, but down ~50bps sequentially. Revenue per available room ("RevPAR") has exceeded pre-pandemic levels for 2 consecutive quarters now, reaching $4,544 in Q2. This was underscored by a 190bps increase in occupancy rates, as well as an 8.8% rise in revenue per occupied room ("RevPOR"). It pulled this to adj. EBITDA of ~$81mm, an incremental increase of $30mm. Looking at the segment and P&L highlights:

- Senior housing ("SH") revenues were up 11% YoY, underscored by the growth in occupancy rates and RevPAR. Both move-in and move-out volumes also displayed positive improvements compared to Q1 FY'23. As a result of the top-line momentum in this segment, management now projects RevPAR growth of 10%—10.5% by year end. Figure 2 outlines the rolling occupancy rates, recorded at month's end, from January—July '23.

Figure 2.

BIG Insights

- Critically, occupancy levels bounced from the seasonal dip in Q1, and by the end of June, the company had achieved consistent monthly growth, ahead of the corresponding 2022 year-end level. I'd also point out that the 11.6% YoY RevPAR aligns with BKD's forward guidance. Within the same community ("SC") portfolio, RevPAR was up 11.9% YoY, underlined by a 210bps growth in occupancy and an 8.9% rise in RevPAR.

- Moving down the P&L, facility OpEx was flat YoY at $531mm, and labor expense—which makes up ~66% of OpEx—contracted 500bps YoY at the margin.

- This point was essential to the firm's operating numbers. Principally, it saw reasonable fixed cost leverage with the higher rate on cost, and this could be a potential tailwind leading into the back end of the year, as 1) contract labor utilization is down 80%, and 2) operating margin was up 560bps YoY. Should it keep this trend in place, another 1–2 points in operating margin aren't an unreasonable expectation. Finally, quarterly CapEx on maintenance came to $65mm. Critically, management expects c.$200mm in " non-development" CapEx for the entire year, excluding expected reimbursable remediation costs.

Detailed analysis of economics and business capital

One of the critical points to BKD's unit economics is length of stay ("LOS"). Across its portfolio, its avg. LOS is ~2 years. The spread is:

- Alzheimer's/memory care = the shortest

- Assisted living = midway

- Independent living = the longest LOS.

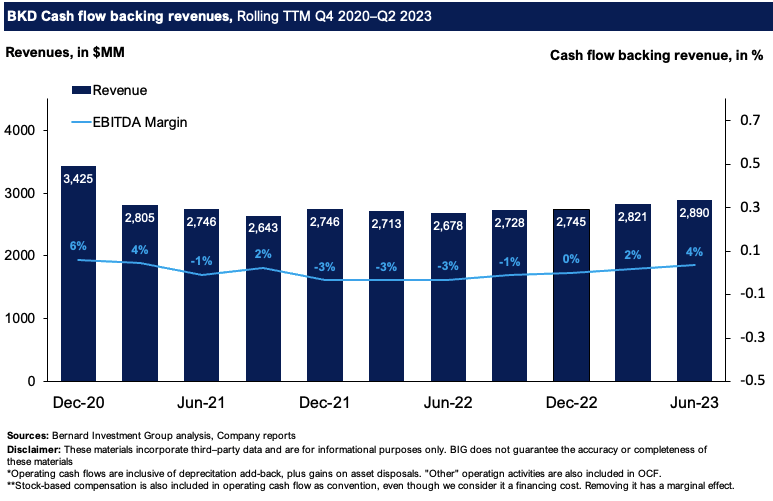

Management confirmed it is looking to increase the 2 year avg. LOS rate on the call. This would be critical in my view, to increase the length of cash collections from its 'customers'. Figure 3 outlines the amount of operating cash flow backing its total revenue print on a rolling TTM basis. All sources/uses of operating cash are used in the calculus, including gains/losses on asset disposals.

What shows is the firm is collecting paper-thin cash receipts on its revenue print each period. Indeed, revenue growth has been relatively flat, but the percent of OCF underneath these hasn't benefitted. The company has to get cash from somewhere to fund its operations, let alone any planned growth. With 0–4% of turnover as "cash revenues", I'd suggest further asset disposals might be necessary to finance CapEx and other ventures.

Figure 3.

{kind=link}

I'd also point out that, regarding its revised lease agreements with LTC Properties—this was set to mature at year end—that the firm reached an agreement with LTC to retain 10 communities under a new agreement. This will be a 10-community lease, and BKD has optionality to acquire all 10 assets in the contract. Perhaps most attractive, is that LTC agreed to provide additional " landlord-funded CapEx" for each community.

Both the CapEx option and renewed lease are critical features in the debate here. This is an asset-heavy business that requires tremendous amounts of cash reinvested into the operations just for maintenance charges, notwithstanding any growth spend.

Figure 4 outlines the cash BKD has spun off for shareholders on a rolling TTM basis since 2020–2023. FCF is considered "owner earnings" here and captures net operating profit after tax, less the tax shield from its interest payments, less cash diverted to capital commitments (asset disposals are considered a source of cash, and subtracted from gross investment). Such commitments are recorded as NWC and CapEx, but only that CapEX above the maintenance capital charge is considered as growth investment. This maintenance is considered to be roughly the depreciation charge for each period. Note, BKD hasn't diverted any of its cash flows to growth operations over the testing period.

Owner earnings have been unstable over this period and largely in the negatives. In Q2, shareholders had a $93mm outflow attributed to them after negligible moves in working capital (all cash is included) and a $344mm maintenance CapEx charge. This data supports a neutral view in my opinion.

Figure 4.

BIG Insights

Being that it's such a capital-intensive business, it's critical to observe the profits BKD generates as a percentage of the capital it has invested into its operations. This is shown in Figure 5, that depicts the reconciliation of owner capital to owner and economic earnings for BKD each rolling TTM period.

Critically, $5.95Bn of capital produces $300mm in trailing post-tax earnings, up from $177mm on $5.4Bn this time last year. The core assets/capital in question are a combination of land, buildings, leasehold assets and so forth, as shown in Figure 6. Given the heavy cash load in its current asset account, cash is recorded at 2% of sales as "operating cash", and all non-interest-bearing current liabilities are subtracted, as in the last publication.

For shareholders, the relevance of Figure 5 is thus:

- Investors have provided the company with $4.3Bn of capital (debt, equity) by Q2 FY'23. BKD has put 119% of this at risk, deployed into the business.

- As such, $27/share in capital at risk produces just $1.20 in trailing earnings after-tax (earnings = NOPAT). This is a tight 6% return on investment.

- This translates to $1.20 in trailing FCF/share (with asset disposals included as a source of cash).

These numbers remain largely unchanged on values booked 2 years ago, and by all measures, it would appear there is a challenging road ahead to improve the scene here to unlock long-term value. The key point here that you'll see me mentioning regularly— l ong-term value creation.

Perhaps most critically, given the firm's return on capital at risk is below long-term market returns on capital, you've got a series of negative economic earnings produced on the assets in question. This is otherwise "non-valuable" capital in my view, because anything above a 12% ROIC would be accretive to value. This was outlined extensively in the last publication, and the trends continue to this day.

Figure 5.

BIG Insights

Figure 6.

BIG Insights

Valuation and conclusion

The stock sells at 16x forward EBITDA and ~1.5x book value, with the former priced at a premium of 26% to the sector. I'd say BKD is valued more realistically as a function of its net assets and/or capital deployed, given its business model. To this, Figure 7 is helpful. It shows what EV multiple the company trades at to the capital it has put at risk in the business ("EV/IC"). This shows 1) the market value created from its investments, and 2) what kind of growth it expects going forward. A multiple >1 is preferred, with 1x suggesting fairly valued.

We can take it a step further. By incorporating the value–differential obtained from BKD's return on capital deployed vs. the hurdle, it shows what potential growth isn't "priced in". The ROIC is less than the 12% hurdle, so it's difficult to see anything not priced in. Findings support this notion—on the calculus, it appears more than 2.1x of any business growth and/or intrinsic value growth has already been priced into BKR's EV at its current mark. This supports a neutral view in my opinion. At 1.03x EV/IC, this gets me to an enterprise value of $5.39B, implying there's potentially little-to-no further upside from here (note: enterprise value is different to market capitalization. It is calculated by taking the market cap of $784mm, subtracting $432mm in cash, and adding the $4.9Bn in debt from the balance sheet).

Figure 7.

BIG Insights

In short, whilst BKD's equity has caught a bid this year, fundamental indicators of value creation are absent based on this analysis. This is an asset-heavy business that requires ongoing reinvestment of earnings into maintenance CapEx, leaving little organic cash to spin off to shareholders. Instead, asset disposals are the funding of choice for BKD recently. Further, you've got $5Bn in capital at risk producing just $1.60 in NOPAT/share (TTM basis), just 6% return on capital deployed. If, as an equity holder, you 'own' the capital tied up to a business, and you're getting 6%—well, long-term market rates tell you to expect 10–12%. The money is better off in your own hands, than in BKD's, based on this. Net-net, reiterate hold.

For further details see:

Brookdale Senior Living: Economic Growth Factors Clamping Equity Gains, Reiterate Hold